Tony Anderson/DigitalVision via Getty Images

Investing in consumer discretionary stocks is out of favor now. Oftentimes, it’s a good strategy to purchase shares of market leading companies with promising growth avenues when they are placed in the out of favor basket by the market.

One of such companies is Levi Strauss (NYSE:LEVI). It’s a number one jeans brand globally, achieves high return on invested capital and has ambitious growth plans. In the past couple of years, Levi Strauss has improved its balance sheet to weather turbulent times and pays a decent dividend, while the stock is trading at modest multiples.

Selected notes on Levi Strauss

Everyone knows Levi’s jeans. The strategy of the company is to grow outside of the jeans category and internationally. Since discovering Levi Strauss stock, it’s been delightful to see people wearing Levi’s wool hats and carrying Levi’s backpacks. Based on simple observations and the results of Levi Strauss, this strategy could have some potential in it. The company has laid down an ambitious growth plan and in the table below the different initiatives and their goals are derived into dollars.

|

Initiative |

Goal 2027 |

Theoretical impact |

|

Women’s clothing |

2x, 10-12% CAGR |

+$1.9 billion |

|

Tops |

2x, 11-13% CAGR |

+$1.1 billion |

|

International |

8-10% CAGR |

+$1.5 billion |

|

Other brands |

2x, 15-17% CAGR |

+$0.3 billion |

|

TOTAL |

+$4.8 billion |

Levi Strauss aims to increase its revenues from $5.8 billion to $9-10 billion in 2027. As one can quickly notice, the numbers don’t add up. At first, the growth plan of the company seems self-promotional, although some of the initiatives must overlap each other. The strategy of Levi Strauss is to strengthen its reach in the geographies, categories and target groups where the company has been underrepresented.

In addition to above-mentioned growth avenues, the company is transforming where it sells its products. Levi’s pursues to increase heavily the share of e-commerce and direct-to-consumer sales. E-commerce represents 20% of its direct-to-consumer sales. The trends supporting Levi Strauss’ business are casualization of clothing and growth coming from developing nations. The company is still controlled by the members of Haas family enabled by the dual share class structure which ensures the members of the family majority of the voting power. The company has been turned around several times since its foundation in 1853.

There’s upside from different angles

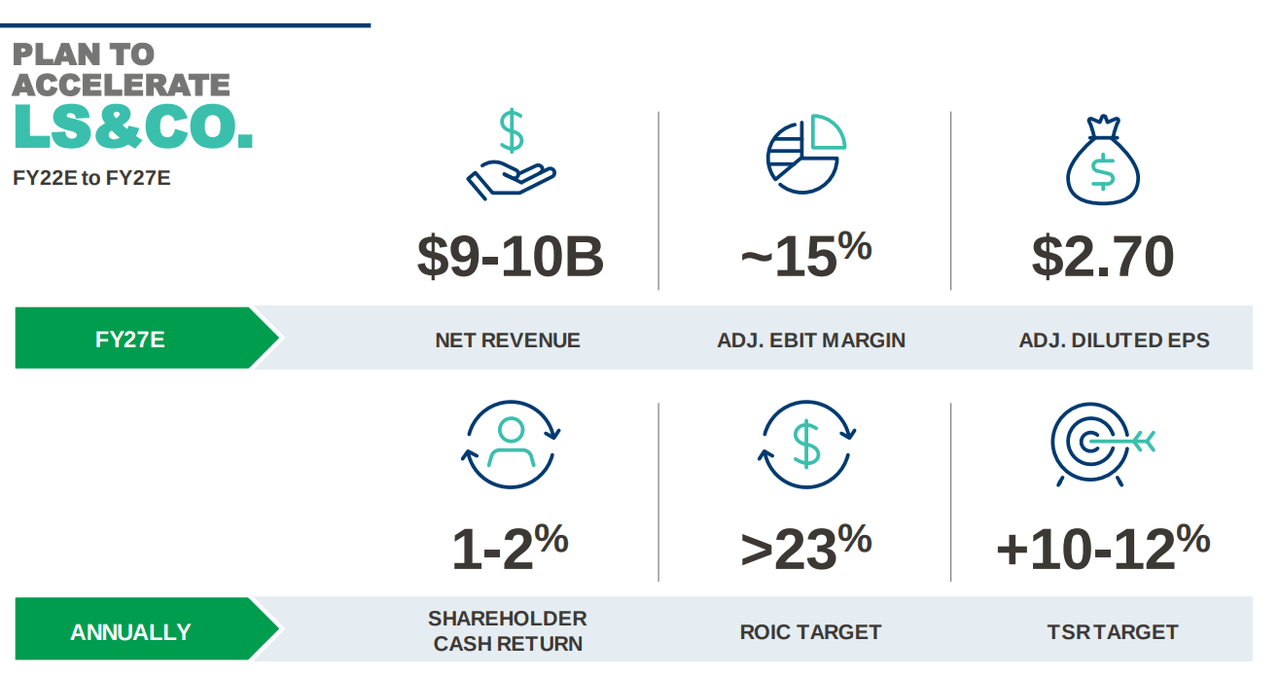

Levi Strauss aims to achieve an EPS of $2.7 by 2027. A nice play with numbers there. Let’s continue the numbers play by simply multiplying the target by the current P/E of 12. That would give us a share price of $32.4. If we discount that to the present by 10% shares would be a buy at $20.1. An investor requiring a higher safety margin could discount by 12%, which would give us a present value of $18.4. Naturally, the plans of the company have to be taken with a grain of salt and investors could further deduct an appropriate safety margin in order to come up with a target buy price.

Levi Strauss’ financial targets 2027. (Levi Strauss investor material.)

Where are the earnings going in the near future? In October 2022 the company reported its Q3 earnings, the period ending in the end of August. So looking backwards, there’s a wide time lag. The results were mixed. In the Q3 revenue grew 1%, pushed down by 19% decrease in Europe and held up by modest 3% growth in Americas and 36% growth in Asia. Other brands grew 37%. The decline in Europe was partly explained by currency fluctuations and closure of the business in Russia. Goldman Sachs recently expressed its worry about the level of orders coming from retailers and substitution effect and lowered its target price by one dollar to $17.

Fitch projects Levi’s revenue could decline in the low-single digits in 2023, driven in-part by difficult comparisons and an increased focus on services like travel and entertainment following pandemic-induced softness. –Fitch 22.12.2022

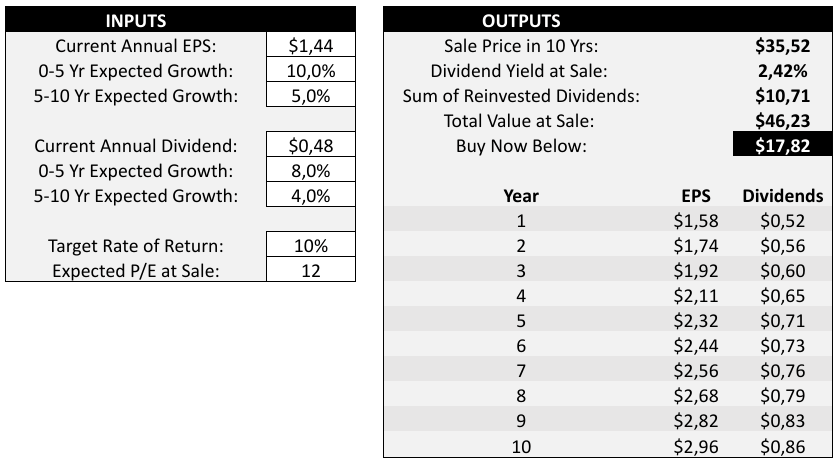

For the fiscal year 2022 the company is expecting to deliver an EPS of $1.44-$1.49. If we take the lower end as a starting point and see what would it take to achieve 12% lower EPS than the company’s year 2027 target (year 5), it would require 10% annual growth. Together with dividend growth in line with net income growth and unchanged P/E the shares would be a buy around $17.8. With a half slower growth rate, the fair value would be $15 per share. According to Seeking Alpha the three, five and ten year earnings per share growth has been around 13-15%.

Valuation based on historical growth rates. (Author, model by Lyn Schwarz Alder.)

What would be a right multiple for Levi Strauss? Let’s use a rather conservative table, presented by Vitaliy Katsenelson in the book Active value investor, which is based on growth rate and dividend yield. A 10% growth rate would give us 14.5 and a dividend yield of 3% would add 3-point on top, totalling 17.5. If we take an even more conservative approach and use a P/E of 15, the intrinsic value would be $21 per share. The average target price of analysts is $20.3, which gives support to this assessment.

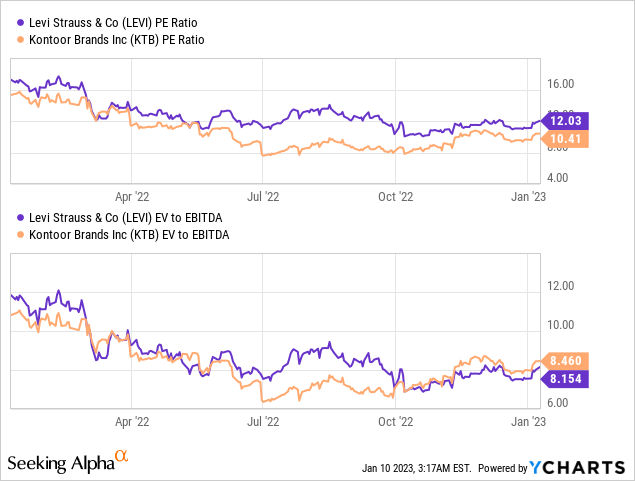

Interestingly, despite higher ROIC and historical growth, larger scale and healthier balance sheet Levi Strauss stock is trading at similar multiples as Kontoor Brands (KTB), which is known for Lee and Wrangler jeans brands. Kontoor offers a higher dividend yield compromised by a higher payout ratio. The average ROIC and ROE according to QuickFS has been 15.4% and 34.4% for Levi’s and 10.4% and 17.1% for Kontoor Brands.

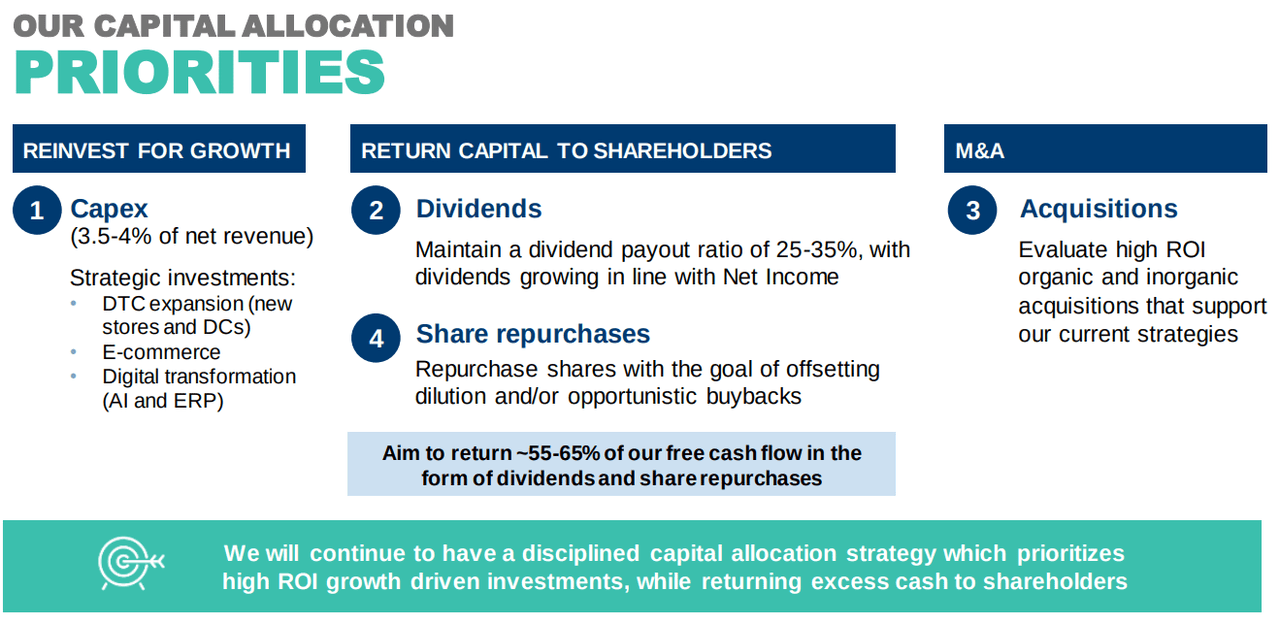

Balanced capital allocation

Levi Strauss does not intend to pay a high dividend. The company aims to grow dividend payout along with the net income. However, since its relisting in 2019 Levi Strauss has rapidly increased its dividend at a CAGR of over 40%. In the last quarter, the dividend increased by 50% year on year. Today, the annual dividend is $0.48 per share, translating to a dividend yield of close to 3%. The payout ratio stands at 30% against rolling 12 months earnings per share.

Capital allocation strategy. (Levi Strauss investor material.)

During the past couple of years, the company has reduced its indebtedness. The total debt against its adjusted EBITDA stands at 1.1x. In the last reported quarter its net debt tripled to $372 million due to lower cash position while adjusted EBITDA increased from $724 million to $925 million. In 2020 the total debt to adjusted EBITDA ratio stood at 4.9x. Half of its current debt is due in 2027 and the other half 2031. Fitch is expecting the EBITDA to moderate down to $850 million in 2023.

In September 2021 Levi Strauss acquired Beyond Yoga, a high-growth activewear brand mostly selling women’s clothes digitally in the United States. Levi Strauss paid a whopping $400 million for $100 million annual sales. Currently, Levi Strauss is investing more in the business, e.g. opening the first brick and mortar store, and its contribution to the bottom line appears to be negative. The sales of Beyond Yoga brand has been approximately $23 million per quarter for the past two quarters.

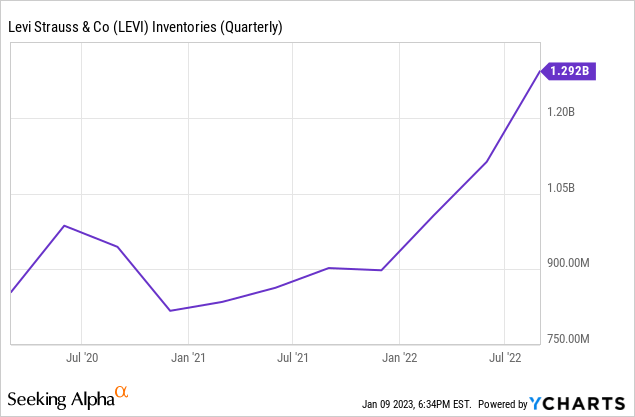

A ballooned inventory

Naturally, there are several risks with Levi Strauss. Foreign exchange rates have been a headwind to the company, and its finished goods inventory level is approximately 30% higher than normal due to supply chain challenges. If the ballooned inventory is not outdated, the unloading of the inventory can also help in the coming quarters. Approximately half of the company’s revenues come from the Americas region, and the pursuit to grow revenues internationally will continue to expose the company to forex fluctuations. Fortunately for Levi Strauss, the dollar has been weakening since last September.

The clothing and apparel industry is placed into the consumer discretionary basket, and now this basket is frowned upon. Consumer spending power is under pressure. Consumers can choose cheaper jeans brands. Due to work from home people on average wear jeans less, so one doesn’t need to replace jeans as often when wearing only sweat pants. Fortunately, Levi Strauss have chosen to seek growth in khakis with Docker’s brand and tapping into the growing activewear category with Beyond Yoga brand.

Conclusion

Levi Strauss is a market leader in a category that is now out of favor. A leader with a strong balance sheet has an opportunity to come out of the headwinds stronger while rewarding the shareholders with a decent dividend. On a longer horizon, Levi Strauss shares appear attractively priced. If the company can deliver an average earnings growth of 5-10% annually, the shares are currently a buy. A cautious investor should time the buys to see if the current uptick is just a bear market rally.

Be the first to comment