Larry Crain/iStock via Getty Images

The Biden Administration is tamping down the government’s quantitative easing (“QE”) program. That could create headwinds for the economy and fissures for the stock market. In my opinion, that puts cyclical names like LCI Industries (NYSE:LCII) in the spotlight. If the economy cools, then sales of recreational vehicles (“RVs”) could slow. That said, I have been predicting such a slowdown for a while now.

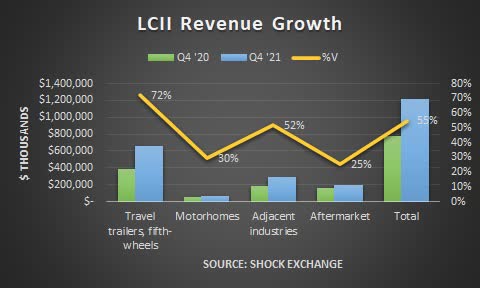

In its most-recent quarter, LCII’s revenues of $292 million were up over 50% YOY, yet rose only 4% sequentially. Each of the company’s core product categories reported double-digit percentage growth. Revenue from Trailer, Fifth-Wheels and Motorhomes was a combined $728 million, up over 65% YOY. These segments represented a combined 60% of total revenue. This illustrates that LCII has heightened exposure to the RV industry, despite efforts to diversity the company’s revenue stream over the years.

RV shipments for year-to-date February 2022 were 107 thousand, up 14% YOY. RV shipments for the month of February were up 11%, implying shipment remain robust, at least for now.

LCII Q4 2021 revenue (Shock Exchange)

The company’s content for total RV and content per motorhome also increased by double-digits, which helped amplify revenue into the RV segment. Aftermarket sales of $197 million rose 25% YOY, yet fell 10% sequentially. Sales in this sector could slow if RV shipments trail off in the second half of the year. Sales for Adjacent industries were $288 million, up 52% YOY and up 3% sequentially.

Management has beefed up this segment via acquisitions, and acquired six companies in 2021:

We ended 2021 with a $4.5 billion in revenues, up 60% year-over-year, largely driven by strong demand across all our markets. Our growth is also supported by six acquisitions, adding approximately $270 million in net sales. These acquisitions have helped us further expand our wide portfolio of innovative products, while providing entry into new and meaningful markets further establishing LCI as a global leader in the recreation space.

I was originally circumspect on LCII’s acquisition spree amid an uncertain economy, but was initially proven wrong. If the economy slows, the value of LCII’s acquisitions could decline below their acquisition costs. LCII is down over 25% YOY, which may reflect that spurring the stock price through acquisition may have run its course.

Margins Continue To Expand

LCII’s management team has done a yeoman’s job of managing costs amid the volatile RV industry, and its aggressive acquisition spree. One would expect that rising revenue would lead to economies of scale and higher margins. In Q4 the company reported gross margin of 24.1%, down from 25.2% in the year-earlier period. Gross profit on a dollar basis was $292 million, up 48% YOY. SG&A costs were $178 million, up 33% YOY. Though SG&A grew rapidly, it was still less than LCII’s top line growth.

EBITDA of $146 million was up over 65% YOY, while the company’s EBITDA margin was 12.0%, up 80 basis points versus that of the year-earlier period. The war between Russia and the Ukraine has triggered inflation in certain markets, and caused supply chain disruptions in others. Will inflation impact LCII’s input costs? Will the company be able to pass along such cost increases along to the customer? These are big questions management will have to address head on.

So far, the company has been able to navigate the volatile RV industry and contain costs in the process. Management has also been able successfully integrate acquisitions and improve margins. LCII will have to continue this balancing act going forward. However, the stock may continue to fall as the Federal reserve is removing the punch bowl and investors may focus more on earnings fundamentals rather than on momentum.

LCII’s Valuation Appears Fair

LCII ended the year with $63 million in cash, up from $52 million in the year earlier period. The company has $940 million in working capital, up from $454 million in the year earlier period. Working capital should serve as a buffer in case the RV industry or the economy turns down. Monetizing its working capital should allow LCII to actually generate positive cash flow if revenue slows or declines. Free cash flow for full-year 2021 was -$211 million. The company also spent another $194 million on acquisitions in 2021, down from $182 million in the year earlier period.

LCII has goosed growth over the past few years via acquisitions. The economy and the rise in financial markets could end as the Fed raises interest rates and removes monetary stimulus. I expect LCII to tamp down acquisitions going forward. If the company has to rely on organic growth, then revenue and earnings may have peaked. LCII has a solid balance sheet, but stagnant to declining revenue growth may not sit well with investors.

LCII has an enterprise value of $3.9 billion or 7.6x 2021 EBITDA. This falls outside of my 8x to 10x range range for cyclical industries. However, I anticipate flat to declining organic growth in the second half of the year. LCII appears fairly-valued, yet I could turn negative on the stock if organic growth stalls.

Conclusion

LCII’s share price is cracking. The stock is a hold, for now.

Be the first to comment