turk_stock_photographer

Asset-light companies are well known for rewarding shareholders with their excess cash, and Lazard Ltd (NYSE:LAZ) is no different, with robust share repurchases last year. This is especially accretive to shareholders when the stock is trading at a low price.

As shown below, LAZ trades at an under 10x PE and is still down materially over the past 12 months. In this article, I highlight why LAZ is a solid dividend buy at present for potentially strong returns. Lazard issues a schedule K-1.

LAZ Stock (Seeking Alpha)

Why LAZ?

Lazard isn’t a household name, but it is well-known in the investment community as being a leading financial advisory and asset management firm. It has a 170+ year history, and provides advisory services on mergers and acquisitions, corporate restructurings, financial strategy, capital raising, and corporate finance. At present, it has over 3,300 employees and over $200 billion in assets under management.

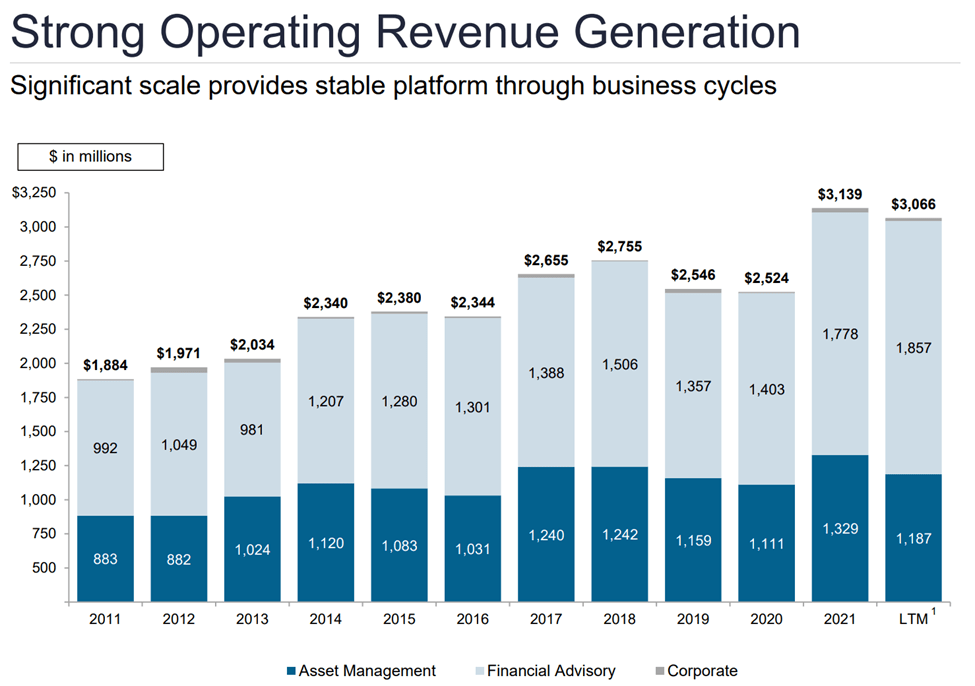

One of the key strengths of Lazard is its global reach and expertise. The firm has a presence in 26 countries, and has a team of experienced professionals with deep local market knowledge. This allows Lazard to provide its clients with a unique perspective and valuable insights on investment opportunities around the world. As shown below, Lazard’s multi-cylinder business model has delivered strong operating revenues across economic cycles over the past 10+ years.

LAZ Revenues (Investor Presentation)

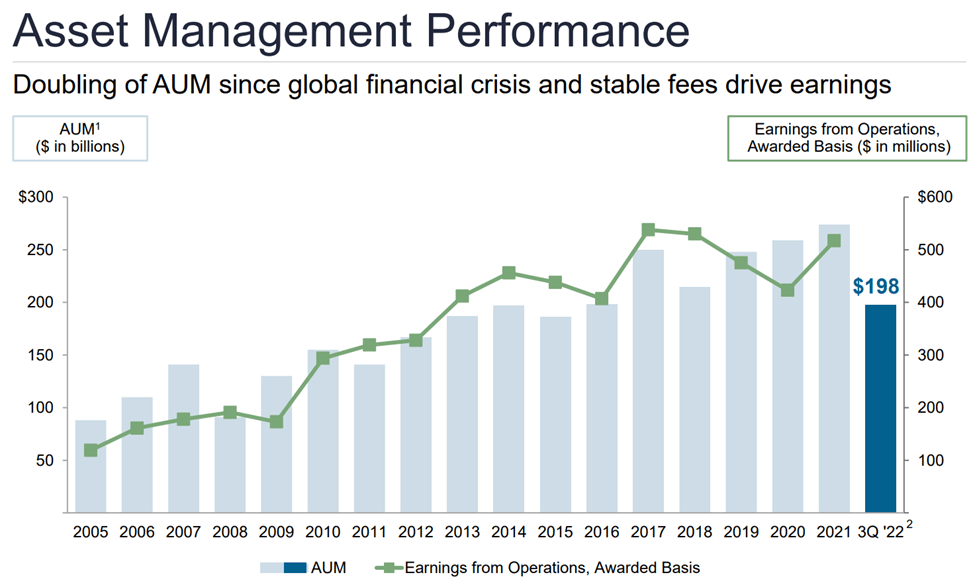

In terms of its asset management business, Lazard offers a diverse range of investment products and services, including traditional and alternative investment strategies. The firm has a strong track record of delivering strong investment returns for its clients, and has been consistently recognized as one of the top asset managers in the industry. As shown below, LAZ has doubled its AUM since the Great Recession of 2008 – 2009.

LAZ AUM (Investor Presentation)

Meanwhile, LAZ produced respectable operating revenue growth of 3% YoY to $724 million during the third quarter, representing a record for the company. This was driven primarily by the Financial Advisory business, which saw 19% revenue growth due to several high profile M&A transactions in Europe.

It’s worth noting however that Lazard’s asset management business, like that of peers such T. Rowe Price (TROW) and Franklin Resources (BEN), has been pressured as of late due to equity and fixed income market volatility. LAZ’s AUM for the month of December was down by $5 billion from November to $216 billion, but it is meaningfully above the $198 billion from the end of the third quarter. Moreover, should the January rally in equities hold up or at least stabilize, I would expect AUM for January to be higher.

Looking forward, I would expect for LAZ’s restructuring business to pick up speed, due to overleveraged companies facing financial difficulties as a result of sustained higher interest rates. This, along with potential for M&A activity in the energy space were noted by management’s comments during the last conference call:

In restructuring, although activity is still relatively low, our discussions with clients are increasing as a result of current market conditions and demand for liability management. In addition, our restructuring practice is ranked #1 globally on announced transactions year-to-date.

The energy transition continues to drive deal activity in the sectors that are less influenced by the business cycle, such as health care and reshoring and infrastructure investment are propelling a range of substantial transactions globally.

Speaking of which, two such potential energy sector deals were highlighted by Seeking Alpha in a recent report this month:

There would be “tremendous benefits” with a combination of Dominion (D) and (DUK) and a deal would make a lot of sense, Roger Conrad of Conrad’s Utility Investor told CTFN in an interview published in recent days. The utilities operate in the same space and they have similar goals as far as wind, solar and nuclear.

The utility expert also highlighted NextEra Energy (NYSE:NEE) as a name often mentioned when M&A is talked about. Conrad believes NextEra is likely focused more on acquiring electric co-ops in Florida. He said he wouldn’t be surprised if the utility may bid for something as the company wants to increase the regulated part of its business.

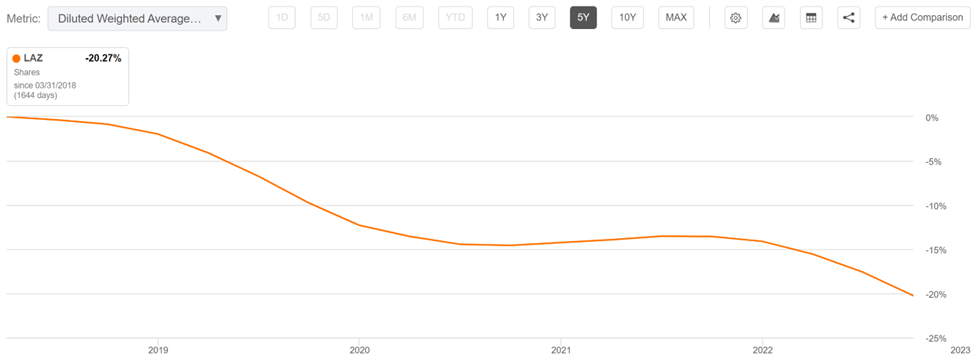

Importantly, LAZ remains a cash rich business that rewards shareholders through robust capital returns. This includes 17 million share repurchased through the first 10 months last year alone. As shown below, LAZ has retired a staggering 20% of its total outstanding float over just the past 5 years.

LAZ Shares Outstanding (Seeking Alpha)

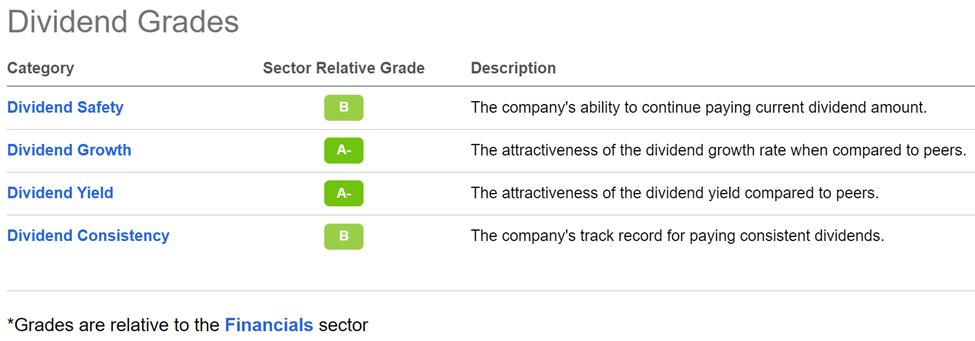

Plus, LAZ currently yields an attractive 5.3% that’s well covered by a 39% payout ratio. As shown below, LAZ earns A and B scores for dividend safety, growth, yield, and consistency.

LAZ Dividend Grades (Seeking Alpha)

Turning to valuation, I find LAZ to be attractive at the current price of $38 with a forward PE of 9.7, sitting well below its normal PE of 13.2 over the past decade. Analysts are pessimistic around 2023 with the potential for a recession (that may not even happen) and forecast a 17% earnings decline, before seeing a 17% EPS rebound next year. I view this as being overly pessimistic with the potential for LAZ to outperform expectations, especially when it can get an earnings yield of over 10% at its current valuation from share repurchases.

Investor Takeaway

Lazard is demonstrating strong operating metrics and could benefit from meaningful restructuring and M&A activity this year. Meanwhile, it’s returning significant amounts of capital to shareholders and could continue to do so at the currently low PE valuation. Lastly, Lazard offers investors a safe and attractive dividend yield and the potential for strong total returns over the long-term at current levels.

Be the first to comment