Those Are Iron Ore Pellets, Not Chocolate Timbits Maksym Isachenko

All values are in CAD unless noted otherwise.

Iron Ore Company of Canada produces iron ore pellets and high-grade concentrate in the province of Newfoundland and Labrador. Transported by a wholly-owned railway, it exports the finished product globally from its port facilities in Quebec.

Company Website

This Canadian company is operated by its majority shareholder (58.7%) and well-known name in the metals and mining sector, Rio Tinto Group (RIO). IOC has two other shareholders, Mitsubishi Corporation and Labrador Iron Ore Royalty Corporation or LIORC (OTXMKTS: OTCPK:LIFZF) (TSX:LIF:CA). Today, we will be talking about the latter.

LIORC’s bread and butter is tied to IOC. Besides dividends from its equity ownership, it receives two additional sources of income from it.

- IOC pays a 7% royalty in return for the leasing a portion of the mining leases and licenses held by LIORC. A 20% tax is levied by the provincial government on this royalty.

- IOC also pays a 10 cents per tonne commission on all sales and shipments of production from the leased portions.

Being a royalty corp, LIORC’s expense categories can be counted on the fingers of one hand. The aforementioned 20% royalty tax, amortization of mining leases and licenses, administrative expenses and income taxes. The company aims to pay the balance or net income in dividends to its shareholders minus a reasonable working capital reserve.

Another point to note is the royalty payments are made in USD and converted by the royalty corp to CAD upon receipt each month. The MD&A section of the financial report notes that LIORC does not attempt to hedge short-term exposure. We assume any difference between the base currency receivable and actual is adjusted to revenue as it’s not shown separately on the financial statements.

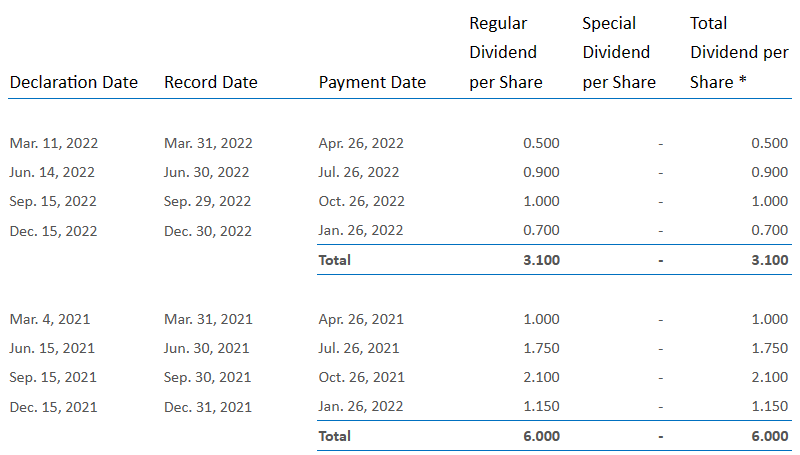

Dividends

Before December 2020, LIORC paid a quarterly dividend of $0.25 and sweetened the pot with special dividends based on the inflow from IOC. They moved away from the special dividend practice with the announcement of the December 2020 payment, and explained their move.

The company has decided to end the practice of designating dividends as either regular or special dividends. It says: “By removing the special dividend designation, the corporation believes that its dividend yield will be more accurately reported by these services in the future.”

Source: Press Release

They have retained the suspense regarding their quarterly dividend, with each being a variable amount.

Company website

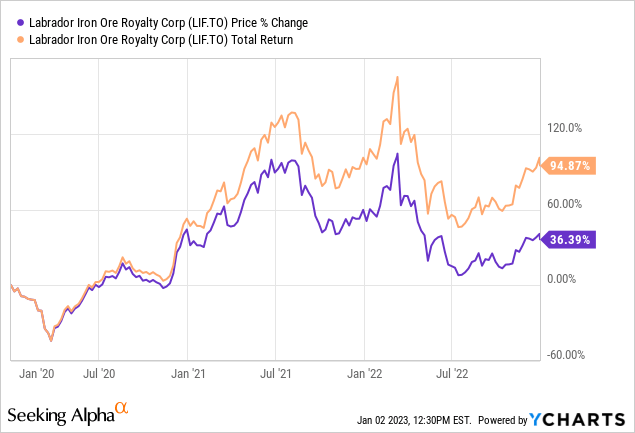

The inflows from IOC, the only source of their operating cash flow, showed a marked reduction in 2022 and that’s reflected in the difference in payouts between the two years. Based on their last payment, and the current price of $33.58, the stock yields over 8%. If you consider yourself a iron ore bull and are an income investor, you may want to take a dip in this Royalty pool.

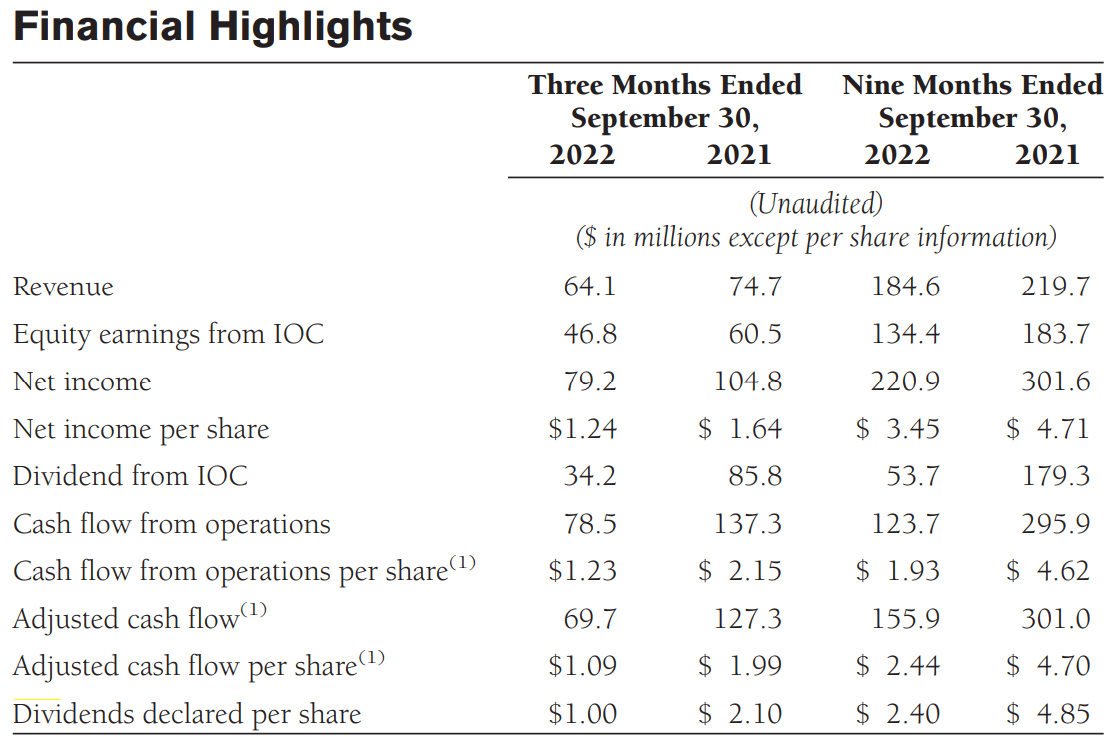

2022 Results

Steel is to iron ore what high yield is to an income investor. The latter in each case loses purpose without the former. Fiscal and monetary stimulus are a match made in property virgin heaven and this came to fruition in 2020 and 2021. Steel demand rose and iron ore went along for the ride. Royalty plays like LIORC and its shareholders, good times were had by all.

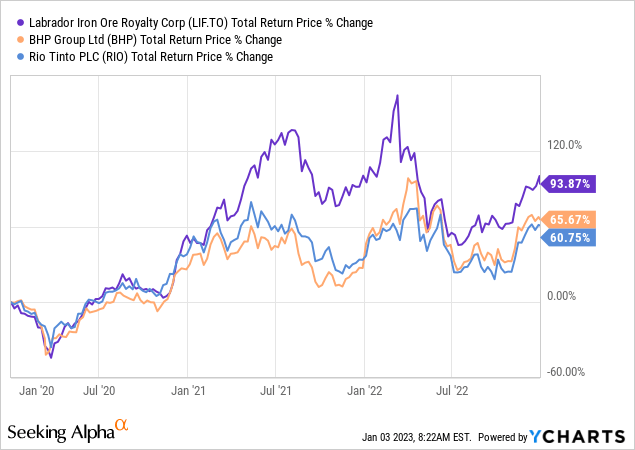

These results also outperformed the two major giants in this area.

China and the US Federal Reserve played spoiled sport in 2022. The demand for steel went down, putting a downward pressure on its price and IOC’s numbers took the same trajectory.

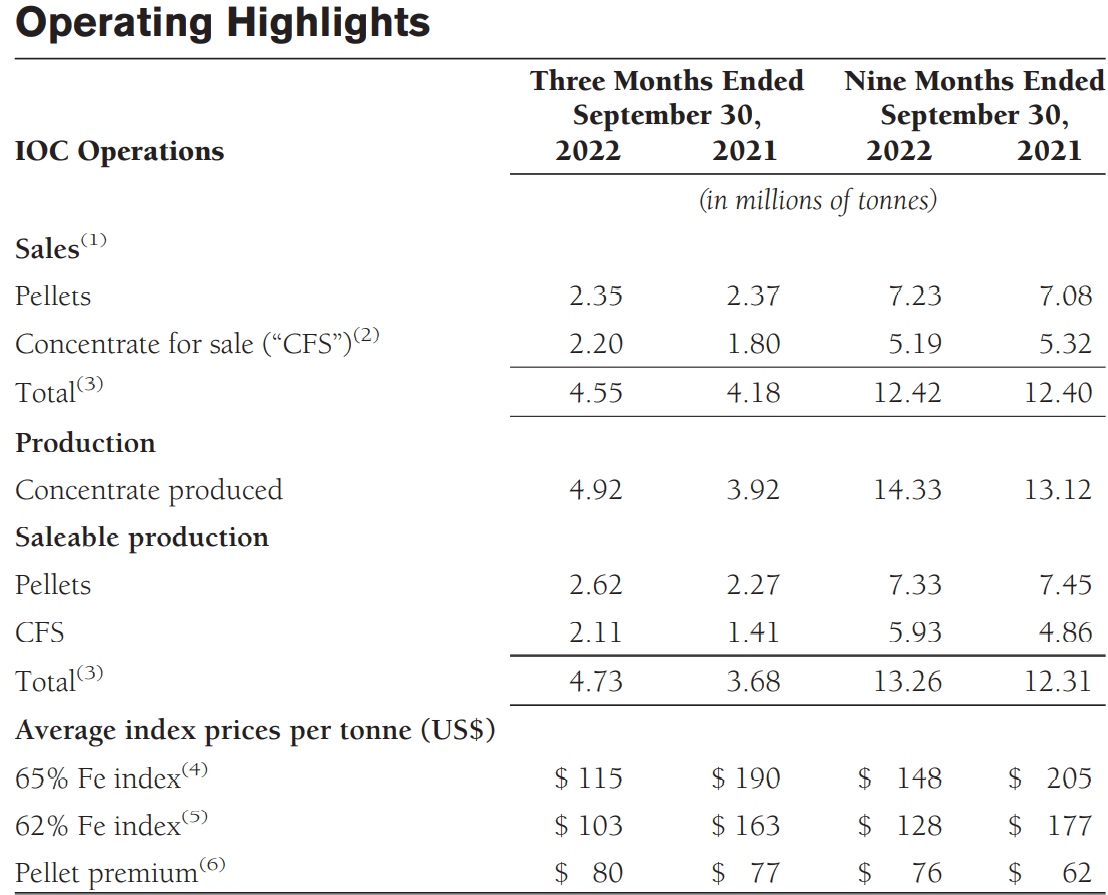

Q3-2022 Financial Report

The higher pellet premiums and concentrate for sales could not stem the flow that occurred from the lower iron ore prices. IOC made less and naturally LIORC reflected the same muted performance. As a result its shareholders also partied less.

Q3-2022 Financial Report

Outlook and Verdict

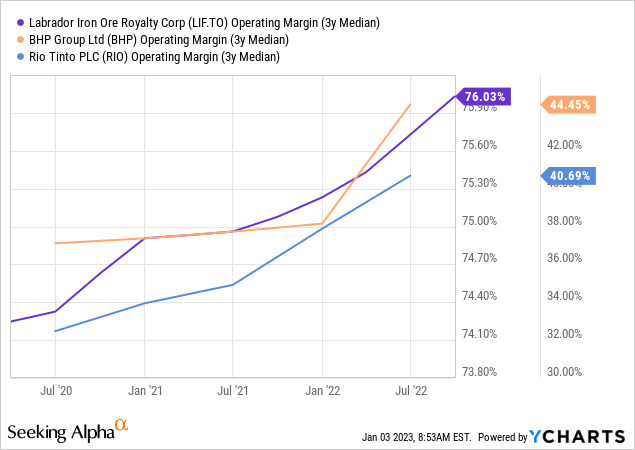

What’s the biggest perk of owning a royalty stream vs. a company directly involved in the business? The perk is that you have only top line exposure and no operating leverage. That works well in many businesses and you can see our recent bullish plays in this royalty area over here and here. On the iron ore side, a royalty structure has a smaller advantage over the mining iron ore plays like RIO and BHP Group Limited (BHP). The reason is that the cost of producing iron ore is so low relative to the current market price per ton. Nonetheless, we do see that operating margins have been far higher for LIORC and over the medium term we think this will be a big factor.

The offset here is that LIORC is hitching on one commodity in one location. LIORC’s advantage is partially offset with RIO and BHP’s scale diversification and exposure non-iron ore plays like copper. So if you wanted to own it and are bullish (we are not), the larger diversified names could give you a similar bang for your buck. This is especially true if prices go up. RIO and BHP’s margins would expand faster than LIORC’s.

The second consideration is of course the macro. We think iron ore is one commodity we least want to play for the long term, and we are in the commodity bull camp. Here, the fundamentals are exceptionally poor in our view with the bulk of the consumption coming from China’s housing bubble and the price of the commodity being way higher than the marginal cost of production. LIORC does benefit from a weaker Canadian dollar and that generally helps it when commodity prices are weak. At the current stock price, the higher margins and the benefit from the weaker currency are sufficient offsets such that we rate LIORC a Hold/Neutral. On the other hand we are short BHP and rate both BHP and RIO as Strong Sells.

Please note that this is not financial advice. It may seem like it, sound like it, but surprisingly, it is not. Investors are expected to do their own due diligence and consult with a professional who knows their objectives and constraints.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment