ArtistGNDphotography/E+ via Getty Images

The latest release of the Employment Cost Index points towards a labor market that is rapidly cooling, extinguishing any thoughts of a wage-price spiral. This is supportive of lower inflation going forward and a normalization of Fed policy, but also increases the probability of a large fall in consuming spending at some point in the next 12-18 months. Investors must balance the prospects of lower discount rates with deteriorating economic prospects, with the latter likely to become increasingly important going forward.

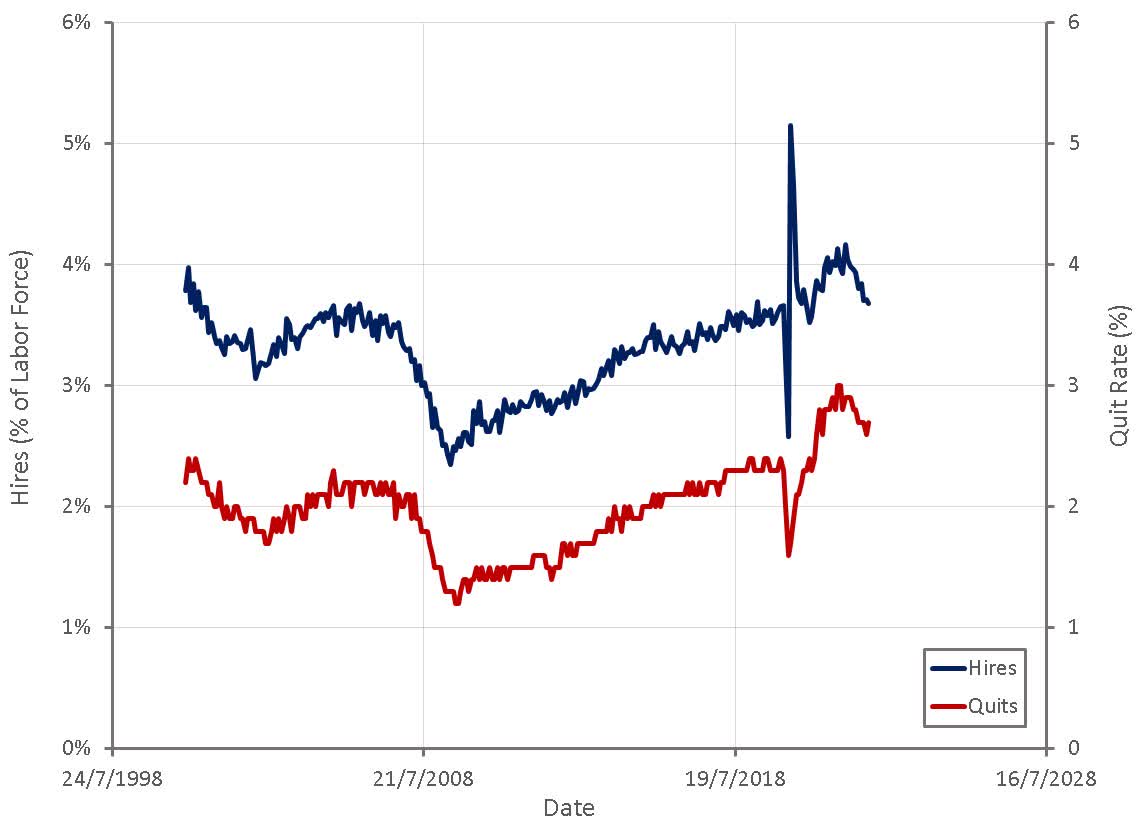

Softening wage growth may surprise some, who continue to believe the labor market is tight based on the large number of job openings and the low unemployment rate. These are both flawed measures though, and are far less indicative than the number of hires and the quit rate.

Figure 1: Job Openings and Unemployment Rate (source: Created by author using data from The Federal Reserve)

Figure 2: Hires and Quits (source: Created by author using data from The Federal Reserve)

Not only is wage growth returning to a fairly normal range, but wage pressure in industries that have been causing the most concern has also eased significantly. Given this development, it now seems unlikely that any sort of demand driven inflation will be realized.

Figure 3: Employment Cost Index by Industry – 3 Month Change (source: Created by author using data from BLS)

Figure 4: Aggregate Wage Growth (source: Created by author using data from The Federal Reserve)

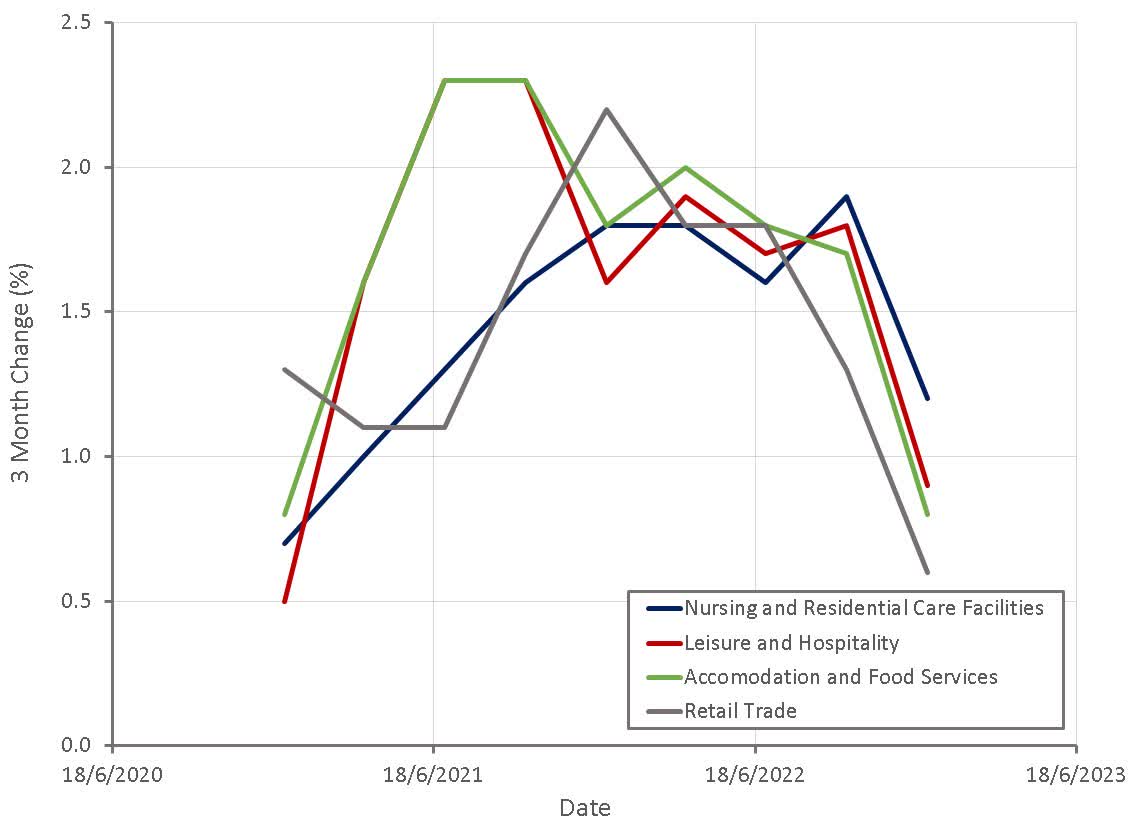

Industries that have seen a rapid normalization of employment cost growth are also generally tied to consumer spending (retail trade, accommodation and food services, leisure and hospitality). Given the importance of consumer spending and housing to the economy, any signs of weakness in these areas should be interpreted negatively.

Figure 5: Employment Cost Index Grouped by Exposure – 3 Month Change (source: Created by author using data from BLS)

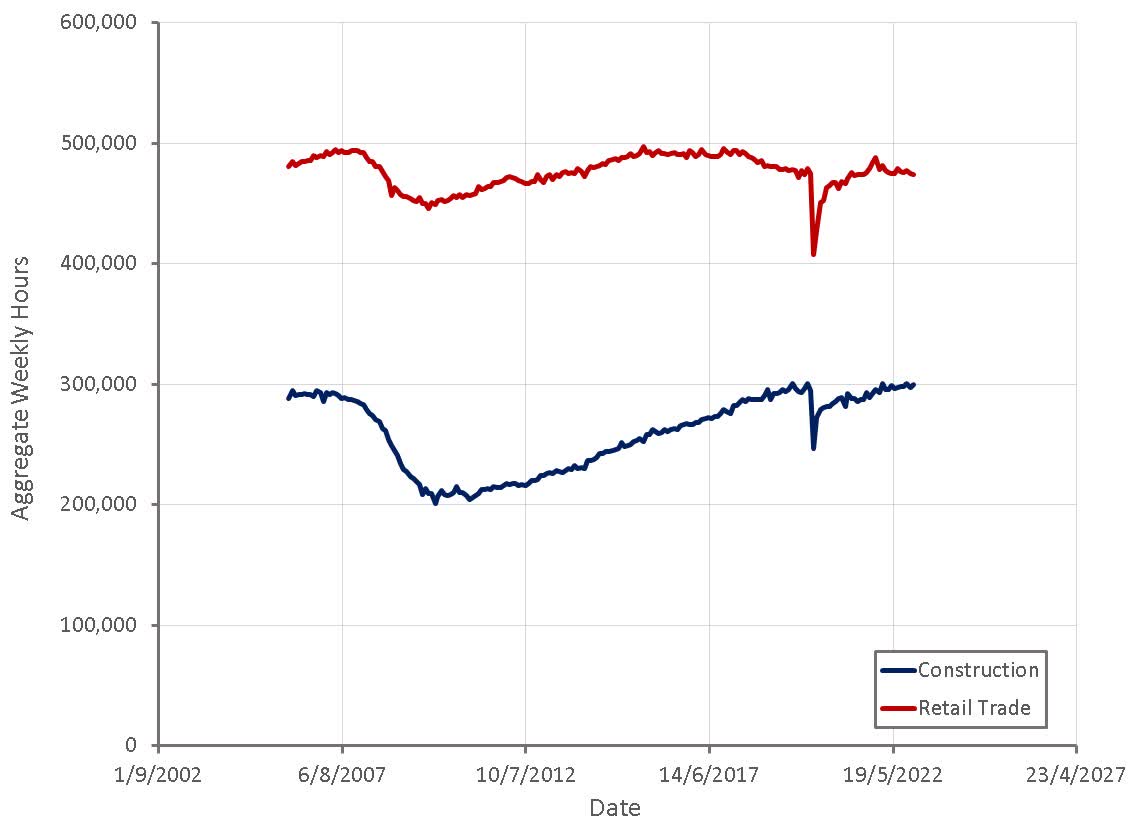

Not only is wage pressure easing in these areas, but aggregate hours worked has also begun to level off / decline. While housing and consumer spending are still holding up fairly well, the labor market is suggesting that they have weakened or are expected to weaken.

Figure 6: Aggregate Weekly Hours (source: Created by author using data from The Federal Reserve)

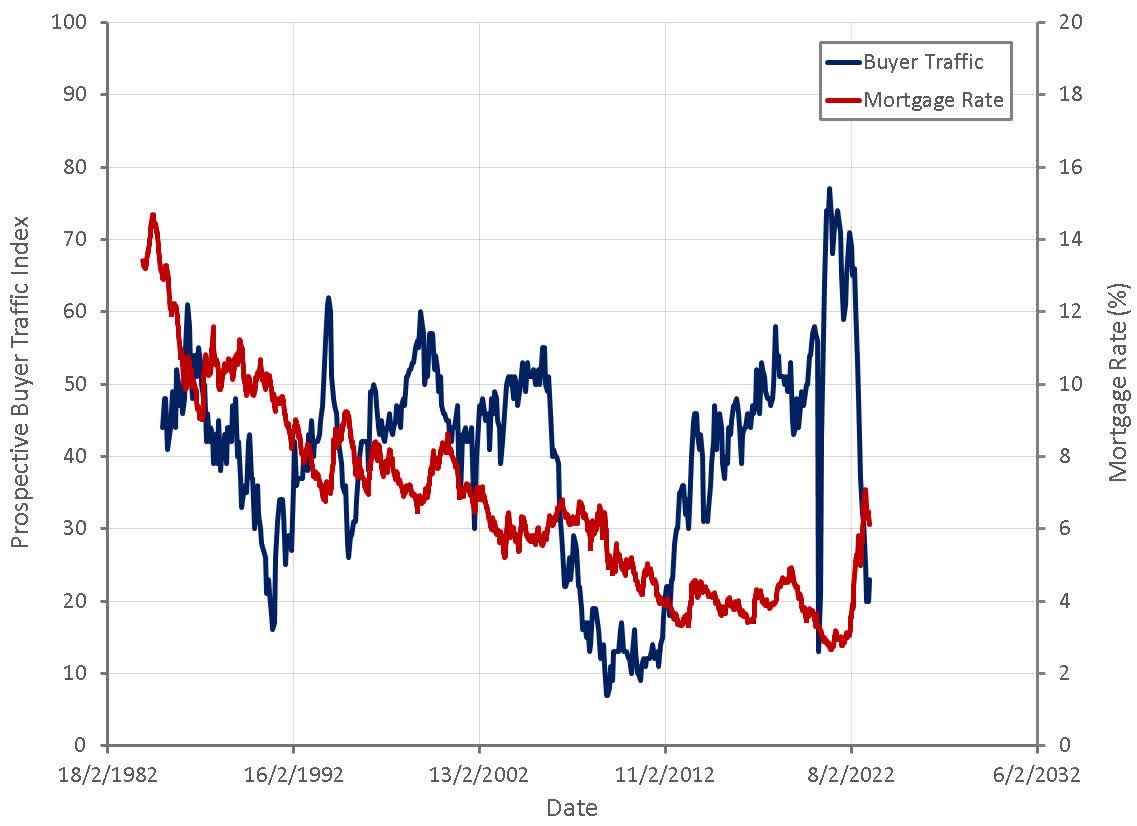

The rapid rise in interest rates has really crushed upstream activity in the housing market. The backlog of housing under construction from COVID is currently buffering employment in the construction industry, but absent a rapid decline in mortgage rates it would seem employment will get hit at some stage.

Figure 7: NAHB Prospective Buyer Traffic Index (source: Created by author using data from NAHB)

With the personal savings rate at extremely low levels and wage growth softening, it seems unavoidable that consumer spending will be hit at some stage in the next 1-2 years, depending on when excess savings are exhausted. The most feasible way of avoiding this in the near term would appear to be fiscal stimulus, but given the balance of power in congress this is a low probability scenario.

The most recent update to the employment cost index confirms that labor markets are softening, which is supportive of lower inflation and less restrictive monetary policy. Lower interest rates could help the housing market to recover, but weak wage growth is likely to become a significant drag on consumer spending. Equity markets have been largely driven by inflationary fears over the past 12 months, with bad economic news often interpreted as a positive. This appears to be changing, meaning equity markets may find it difficult to continue moving higher unless economic conditions begin to improve.

Figure 8: Correlation of Equity Returns with Economic Surprises (source: Created by author using data from The Federal Reserve)

Be the first to comment