Stuart C. Wilson

Even if you squint, you can’t tell who is in the above photo. It’s Charles III, as Prince of Wales, visiting the L3Harris Technologies (NYSE:LHX) London Training Center for pilot training. Seeking Alpha licenses a broad stock photo catalog, yet that was the most interesting pic I could find for this company, other than signage on an office building.

Contrast that to say, the sexy F-35 from Lockheed Martin (LMT). Or their Skunk Works stamp on that fictional Mach 10 fighter in the latest Top Gun movie. There’s the new B-21 stealth bomber from Northrop Grumman (NOC), the nuclear subs and naval vessels from Huntington Ingalls (HII) and General Dynamics (GD). Even Boeing (BA) has helicopters, bombers, and space.

Among the major defense contractors, L3Harris doesn’t really have flagship products which generate excitement. Perhaps this is the reason that, despite being the 6th or 7th largest, you don’t hear the name brought up much at all, relative to its seemingly more exciting peers.

Well, that may change with its pending acquisition of Aerojet Rocketdyne (AJRD). Even if it doesn’t, here’s why now is a good time to consider L3Harris for your portfolio. Even I bought it last week and as mentioned, due to current and recent valuations, I didn’t buy any defense names in 2022, aside from a couple hundred shares of Boeing at $124 back in September.

What does L3Harris do?

If you read the about us page on their website, this is what it says:

In a fast moving and increasingly complex world, L3Harris is anticipating and rapidly responding to challenges with agile technology – creating a safer world and more secure future.

Yeah, that doesn’t really tell us anything. The company profile on SA introduces it as:

…an aerospace and defense technology company, provides mission-critical solutions for government and commercial customers worldwide. The company’s Integrated Mission Systems segment provides multi-mission intelligence, surveillance, and reconnaissance (ISR) systems; and communication systems, as well as fleet management support, sensor development, modification, and periodic depot maintenance services for ISR and airborne missions.

It then describes similar details for maritime, space divisions, and law enforcement. Let’s just simplify and sum it up as this; L3Harris is a diverse electronics manufacturer for military and law enforcement.

Since these are not consumer electronics, obviously they don’t have the fanfare of cell phones, TVs, and other items you and I use daily. In terms of press coverage, that also means their inventions are not being touted at CES, but they are being disparaged in a Netflix exposé. I’m talking about the ‘Web of Make Believe’ docuseries. In short, it’s a true story about how an IRS scammer uncovers what was formerly secret spy tech made by L3Harris; the Stingray cell phone tracker. That and its successor are among their bestsellers.

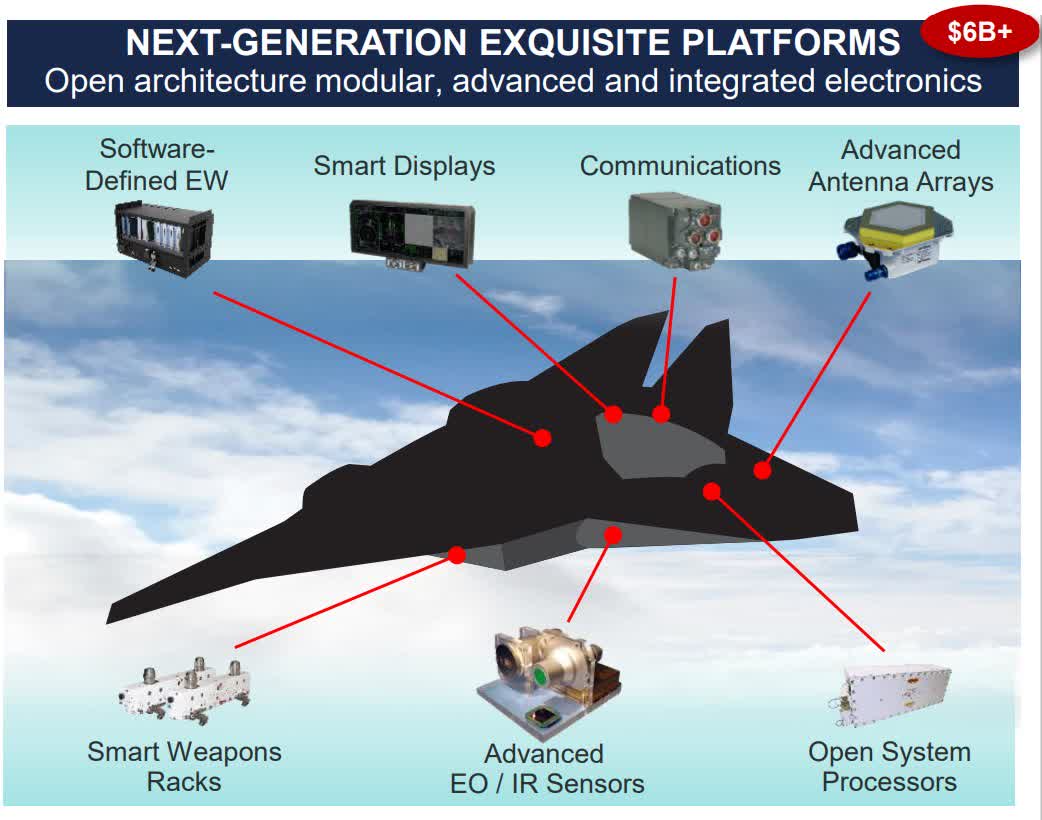

But you don’t need to necessarily know or understand their products. What matters for you as an investor is that they are supplying all sorts of electronics used in military communications, aircraft, naval craft, vehicles, and by personnel.

Examples of components made for aircraft (L3Harris investor overview, Nov 2022)

Not only are these mission-critical but being the type of technology they are, they get outdated rather quickly. The United States Air Force (USAF) has been using the B-52 bomber for a staggering 70 years. You can bet the electronic equipment inside is not nearly as old. While aircraft, ships, and the like have long replacement cycles, L3Harris benefits from their updates along the way.

This also means that L3Harris is more of a frenemy to most of the big name defense contractors. They rarely compete head-to-head and instead those contractors buy such electronics from L3Harris.

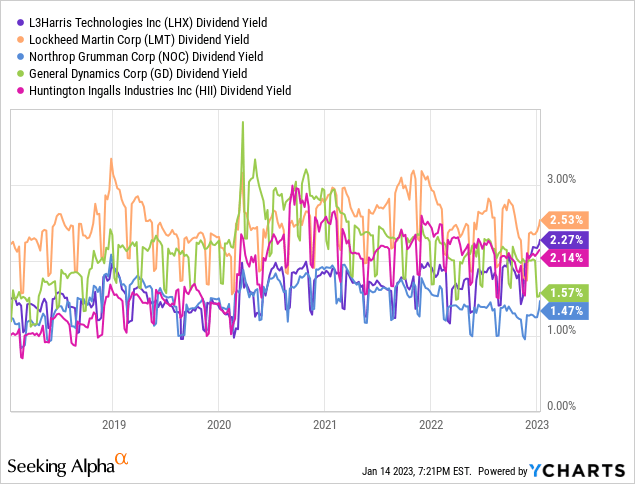

Valuations compared

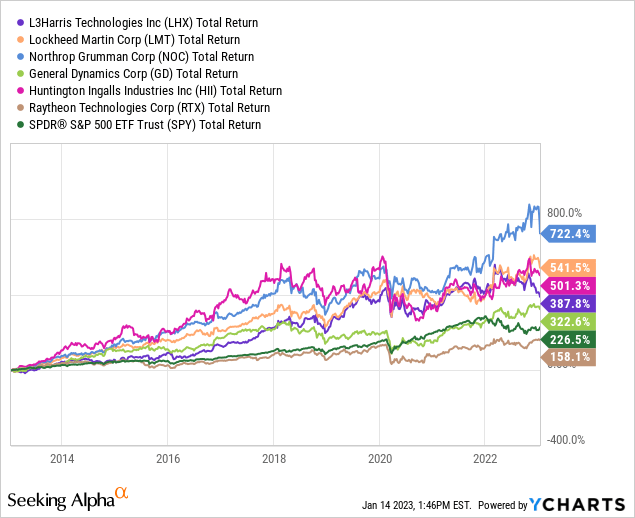

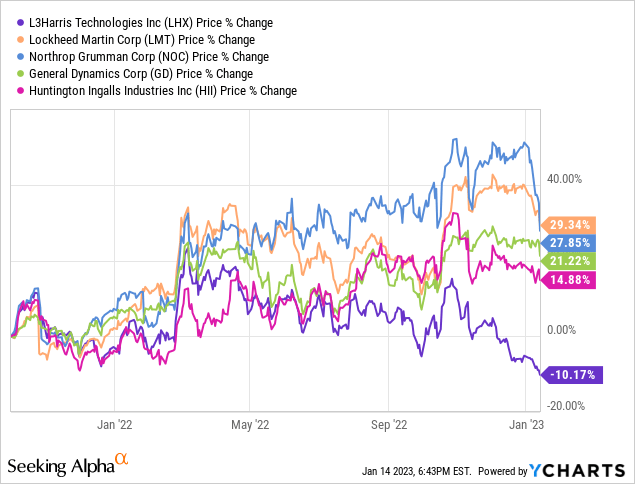

First, let’s look at the 10-year performance of several names in this space:

LHX has not been the best performer but it has produced market-beating returns. It should be noted the Raytheon (RTX) charting is a bit misleading, because it doesn’t reflect the United Technologies merger followed by the spin-offs of Carrier (CARR) and Otis Worldwide (OTIS).

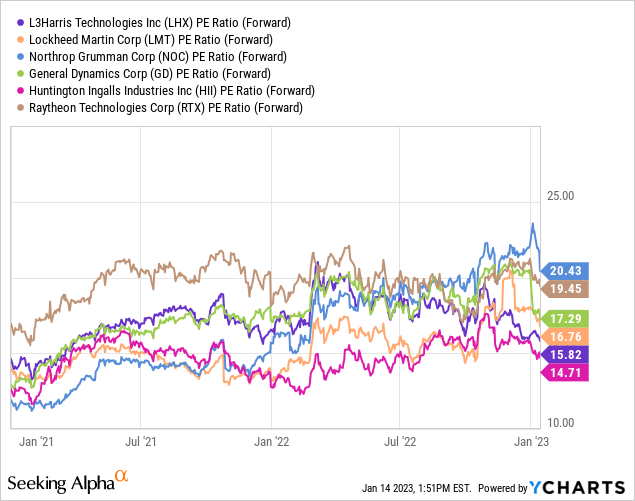

Now let’s look at how their valuations compare:

LHX is near the cheapest on forward PE. Unfortunately, I can’t chart this particular metric further back on here due to the all-stock merger of Harris and L3 Technologies in 2019.

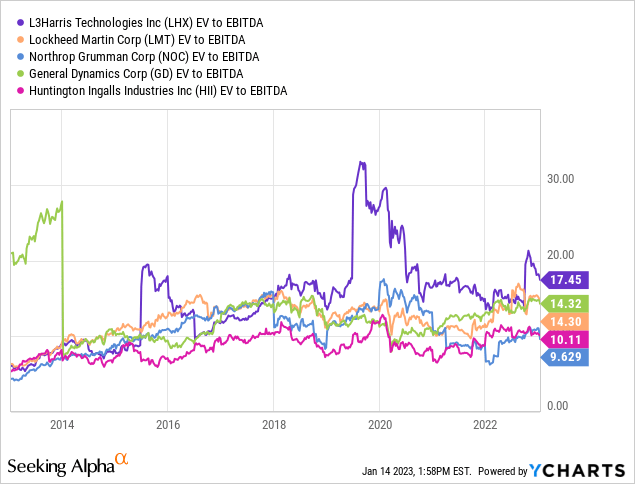

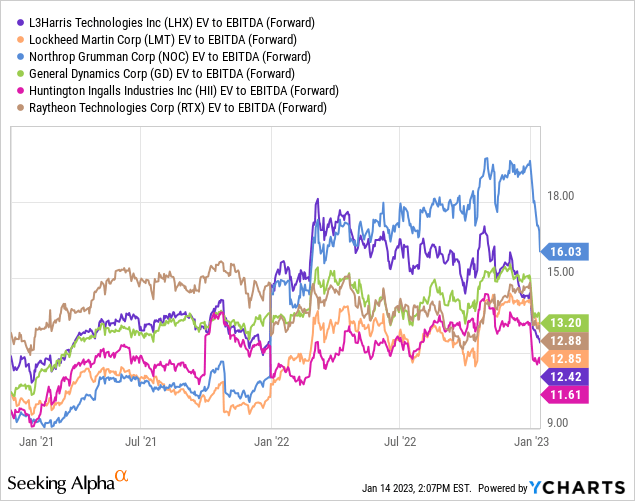

To smooth out the extremes, on this next chart I’ve removed RTX. Here are their EV to EBITDA over the last 10 years:

Historically — just as it does now — L3Harris (and its predecessor) have traded at a higher EV to EBITDA, as well as a lower dividend yield, when compared to the above names. This is because it has been viewed as a higher-growth and more nimble name. Those other guys rely on winning big multi-year and multi-decade contracts for new aircraft, ships, and subs. It can be somewhat boom-bust, when they lose out on, say, the next generation fighter or bomber.

So L3Harris has historically traded at the highest average EV to EBITDA, but what does it look like moving forward?

They go from the highest to almost the lowest!

The Aerojet Rocketdyne acquisition

Aerojet Rocketdyne provides propulsion and energetics to space, missile defense, strategic, tactical missile and armaments, both domestically and internationally.

If you’re not familiar with the drama, in December 2020 Lockheed Martin entered into an agreement to acquire them. Of course, with the overzealous antitrust regime we’ve been in lately, that deal was fought tooth and nail. Lockheed had to give up on it in February 2022.

Then L3Harris came along last month, almost 3 years to day of the LMT attempt. Never say never but it seems unlikely this deal will be blocked, since LHX has no overlap.

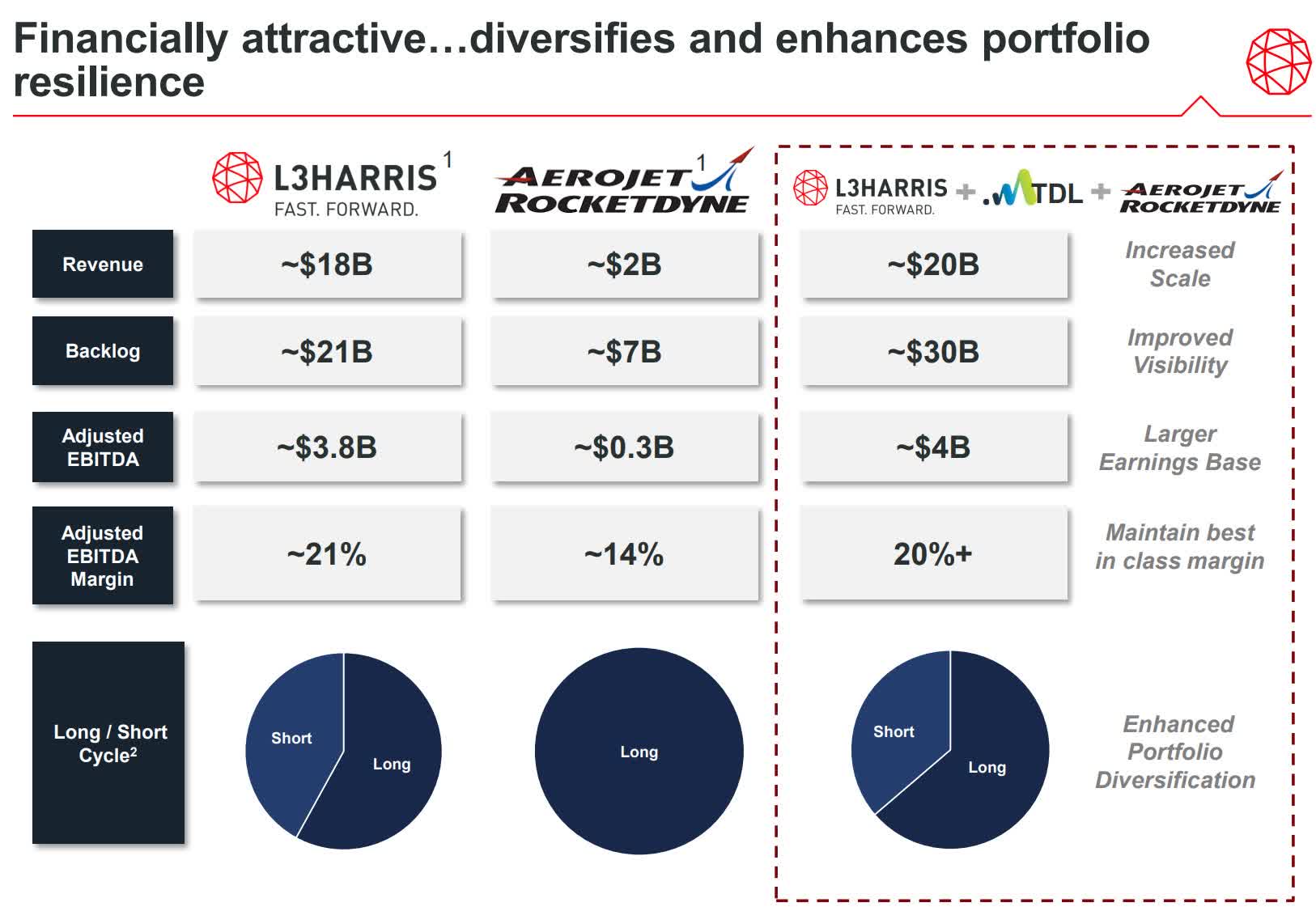

Aerojet Rocketdyne acquisition presentation (L3Harris)

As you see from the pro-forma numbers, AJRD is not adding a lot of revenue, but it is adding a lot of long cycle business. Just compare the backlogs to see that; $21B for LHX and $7B for AJRD. That’s 1/3rd the size, despite being 1/10th the revenue.

Aerojet Rocketdyne website

As you can conure, many of the above areas should add some excitement to LHX. Once the public starts associating the company with things like missile defense, I think you will be hearing more about it on financial TV and the like. You know, the places that like to talk about trends after they happen, not before.

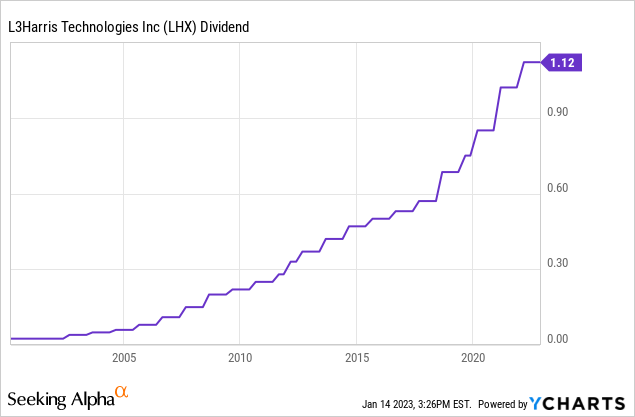

Despite its lower yield, the dividend is interesting

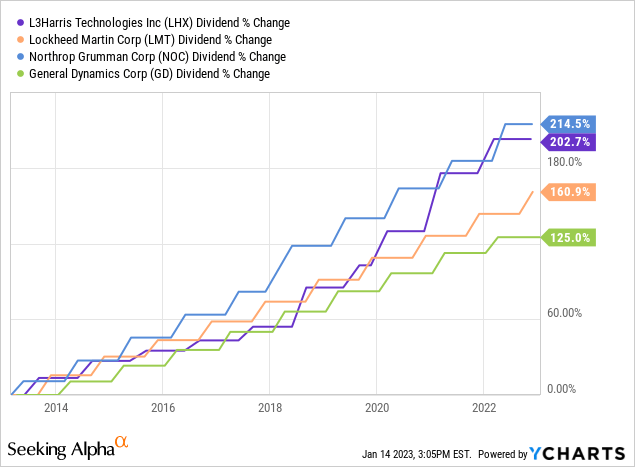

Similar to Northrop Grumman, L3Harris has historically been a lower yielding stock, since it was considered higher growth.

This is why LMT and GD have typically had much higher yields than NOC and LHX.

I have removed RTX because of the spin-offs as well as HII. You see HII was spun-off from NOC in 2011 and since the dividend essentially started at almost nothing when that happened, the growth of nearly 1,000% is a bit misleading, though it is a very strong grower.

Here’s a look at their yields for the last 5 years:

You see LHX is at a 5-year high yield, despite the fact that it, along with NOC, is typically the lowest yielding of the bunch. None of the others are at their 5-year high. With the exception of HII, they’re at average, at best. So even though you are getting what looks like an average yield relative to the sector, LHX is far above its own average.

But why do you need to think of the dividend 5 quarters from now?

Because by then, there should be not 1, but 2 more dividend increases. They announce their increases in February. While there is no guarantee, being that they’ve raised it for 21 years, I’m willing to bet they will raise it this year and next, too.

When it comes to reliable dividend growers, this timing — buying when there are 2 annual increases over the next 5 quarters — is among my favorite strategies, under the right circumstances. If a stock has sold-off and is already trading near the upper-end of its historical yield, it’s even more enticing since many people are not thinking that in about 1 year, not 1 but rather 2 dividend increases will have taken place.

Why has it been selling off lately?

In addition to not getting the fanfare of its more public-facing peers, defense overall has been under pressure so far in 2023 due to budget cut fears. You may have heard the Goldman Sachs (GS) downgrades on Friday for several names. That analyst, his thesis can be summed up as:

- Defense growth spending often consists of long cycles of 7+ years and we are currently 8 years into this cycle.

- Some estimates price in continued 5-6% growth in defense spending, while ignoring the risks of flat budgets as national debt comes into focus.

- Defense names are at or near all-time high valuations, especially LMT and NOC.

All of his points I have been well aware of long before Friday. This is why I had no interest in adding to LMT and NOC in 2022. Of course I’m rooting for them, as I have 700 shares of LMT, along with smaller positions in NOC, GD, HII, and RTX.

But in February 2022 after their prices shot up due to Ukraine, I realized the risk to downside is too great to justify buying more, because of valuations. Sure enough, LMT today is about the same price it was last February. This does not mean I advocate selling but rather, if you initiate new positions here you aren’t getting a bargain.

On the other hand, L3Harris is modestly undervalued right now. No, it’s not at the low multiples the whole cohort saw in Q4 2020 or Q1 and Q4 2021, but it’s a much better buy right now versus its fully-valued peers.

So Goldman’s argument about defense being near all-time high valuations doesn’t apply to LHX, as demonstrated by PE, EV/EBITDA, dividend yield, and share price.

As far as their argument about growth cycles in defense, that is true. But even if the Ukraine conflict is resolved, it’s hard to see the situation in the South China Sea with Taiwan de-escalating this year or next, but you can definitely envision it escalating.

Lastly, the word “growth” in defense spending is a bit of a misnomer. These long cycle contracts almost always have inflation escalators in place. While components of them may or may not keep up with the temporarily absurd CPI, they often at least have a minimum 2-3% annual increase built-in. One glaring outlier would be the new Air Force One contract with Boeing that was negotiated at fixed-price by Trump. Aside from that a few lesser known, when we talk about “cuts” to defense spending, we are only talking about cuts in excess of the rate of inflation/escalators. Only in the world of governments does a “cut” still equal increased spending.

Oh and in closing, I saw that Jim Cramer was pounding the table last week on buying Raytheon, instead of peers like L3Harris. You know what that means…

Be the first to comment