JHVEPhoto

Just before L3Harris Technologies, Inc. (NYSE:LHX) posted fourth-quarter results, defense and aerospace stocks slumped. LHX stock fell from around $210 to as low as $190. Northrop Grumman (NOC) fell even more dramatically. Shares dropped from $540 at the start of Jan. 2023 to around $438. Similar to markets reacting positively to Raytheon’s (RTX) earnings report after its Q4 report, L3Harris rose by 10% for the week.

Markets replaced their fear of governments scrutinizing military and defense spending with strong results from L3Harris.

Investors have three reasons to be bullish on L3Harris after its quarterly report.

1) L3Harris’ Strong Q4 Results

L3Harris posted revenue growing by 5.3% Y/Y to $4.58 billion in the quarter. Funded book-to-bill topped 1.08 times. Investors may compare this ratio to a speculative sector like recently listed electric vehicle companies. Firms like Lucid Motors (LCID) and Rivian (RIVN) accept small deposits for orders. They are not fully funded by customer commitments.

In the military segment, government customers cannot waver on their orders. The war economy is in the early innings after Russia invaded Ukraine. Chief Executive Officer Chris Kubasik cited the ability to communicate as critical in the war in Ukraine. The company has ENVG Goggles, which are enhanced night vision goggle-binoculars that are a key tool for soldiers. The Falcon radio product line is battle-proven. It offers soldiers secure communications.

2) Backlog Growth

L3Harris posted a total backlog growth of 5% Y/Y. Its proposed acquisition of Aerojet Rocketdyne (AJRD) will bring almost $7 billion in backlog and tailwinds to its business. It expands the company’s product line in munitions, space explorations, and hypersonics.

Markets are not concerned about Senator Elizabeth Warren’s push for the Federal Trade Commission to block the planned acquisition. It bid $58 for AJRD stock, whereas the stock is holding the $56.10 level since the announced buyout.

L3Harris should tune in to its Investor Day later in the year to appreciate the strategic fit of the acquisition and the outlook for the growing firm.

3) Healthy Margins

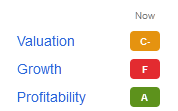

The company posted a net income margin of 6.2% in 2022 on earnings per share of $5.49. The trailing price-to-earnings ratio of 38.63 is above average. The stock scores a fair valuation grade of C-, according to the Seeking Alpha Premium service:

LHX Stock Score (Seeking Alpha Premium)

L3Harris needs to expand margins by raising profitability from older acquired technologies. Macro factors are ongoing pressures on segment margins. This includes inflated costs for material and labor.

The firm will expand its revenue by 2% to 4% this year. It may take advantage of the longer business cycle stemming from its large backlog. With more visibility, it may improve margins by renegotiating several of its multi-year programs. In addition, the privatization of Aerojet Rocketdyne will cut $50 million in costs.

L3Harris previously achieved $660 million in cost reductions in its three-year plan. As it integrates its IT systems, its ERP system costs should fall.

During the pandemic, the company absorbed unforeseen costs. It neither received any compensation for inflation on fixed-price contracts nor asked for any. This may earn L3Harris some goodwill with its customers.

Risks

The government passed a spending bill that includes defense spending. As it reaches the debt ceiling this summer, government expenditures for military equipment may pause. Once the parties resolve their differences, spending should resume.

The Aerojet Rocketdyne transaction may have integration risks. However, they capitalized on the merger of L3 Technologies and Harris by eyeing even more growth. It won multiple high-profile contracts this past summer. It also embraced a platform-agnostic model. This allowed it to complete modifications in business jets, for example.

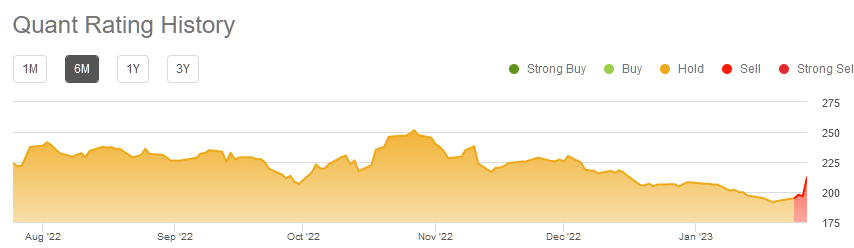

LHX Stock Rating

L3Harris has yet to earn a buy rating in the last year. More recently, the quant system issued a sell rating when the stock price fell below $195. The rating swung back to a “hold.”

LHX Quant History (Seeking Alpha Premium)

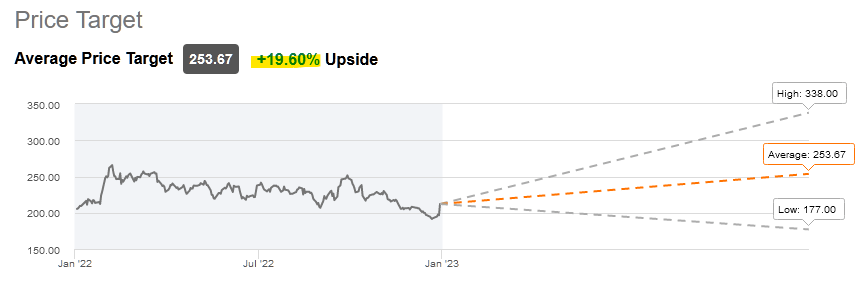

Wall Street analysts rate the stock as a “buy.” The average price target implies an upside of nearly 20%:

L3Harris Price Target (Seeking Alpha Premium)

Value investors could wait for the stock to fall on profit-taking and resume a downtrend that started in March 2022. That month, most stocks fell as markets re-assessed valuations under a Fed rate hike cycle. Inflation rates accelerated at that time.

More recently, inflation slowed. This could fuel renewed buying momentum for the defense and aerospace sector. L3Harris is among the companies that investors should consider buying.

Your Takeaway

I last rated L3Harris Technologies, Inc. as a stock to buy in Nov. 2020. The stock gained 24.47%, barely beating the S&P 500’s (SP500) gain of 22.97. I issued a fair value target range of around $188-$239. LHX stock traded above that target on March 2022 only to fall back to that range.

Investors should take advantage of the yearlong drop by buying L3Harris. The threat of war is intensifying globally. This company is among the firms that should grow its revenue in the next few years.

Be the first to comment