Scott Olson

While Krispy Kreme, Inc. (NASDAQ:DNUT) donuts may be a tasty treat, I think investors should avoid the stock. Despite growing revenues significantly from a few years ago, the company’s profitability appears to be materially lower. In fact, based on LTM GAAP earnings, DNUT is barely a breakeven business. The company also has a lot of floating rate debt that is a cause for concern as central banks keep raising interest rates.

Brief Company Overview

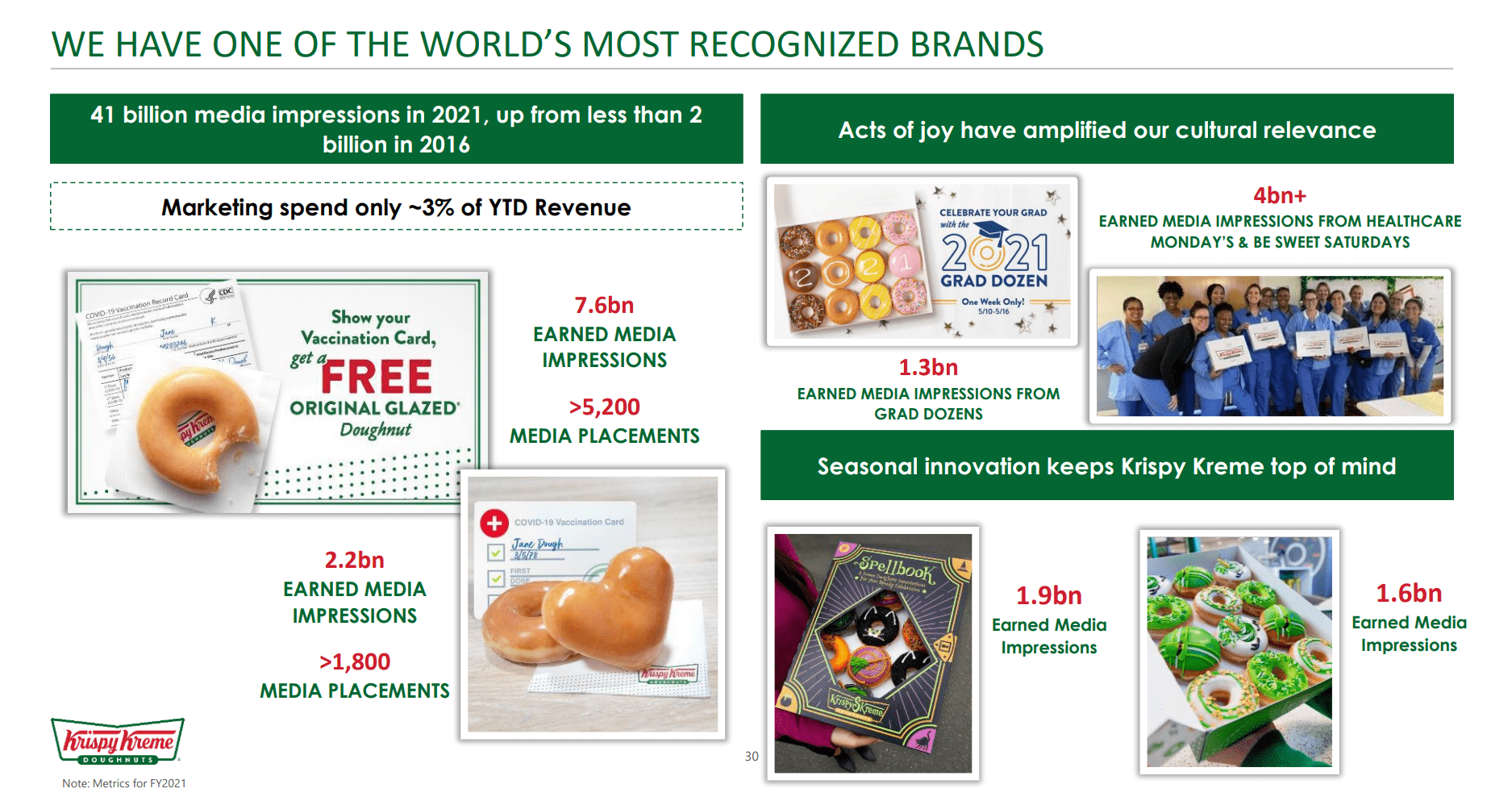

Krispy Kreme Inc. sells their iconic donuts through donut shops, kiosks, and ecommerce delivery. Krispy Kreme has one of world’s most recognizable brands, with over 41 billion media impressions in 2021 (Figure 1).

Figure 1 – Krispy Kreme Has One Of The Most Recognizable Brands (DNUT investor presentation)

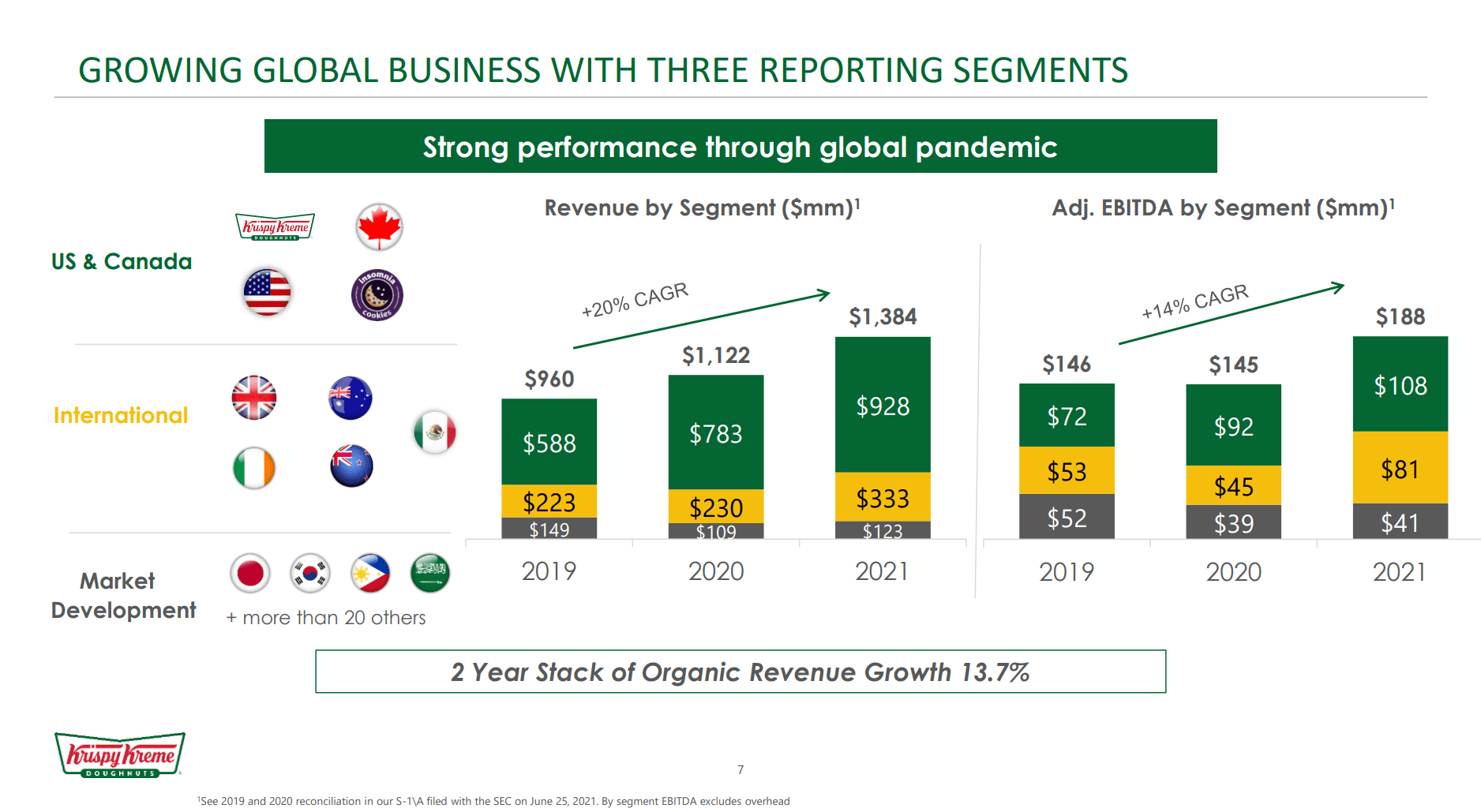

Krispy Kreme donuts are available in 31 countries around the world and the company’s business is separated into three reportable segments: U.S. & Canada, International, and Market Development (Figure 2).

Figure 2 – Krispy Kreme business segments (DNUT investor presentation)

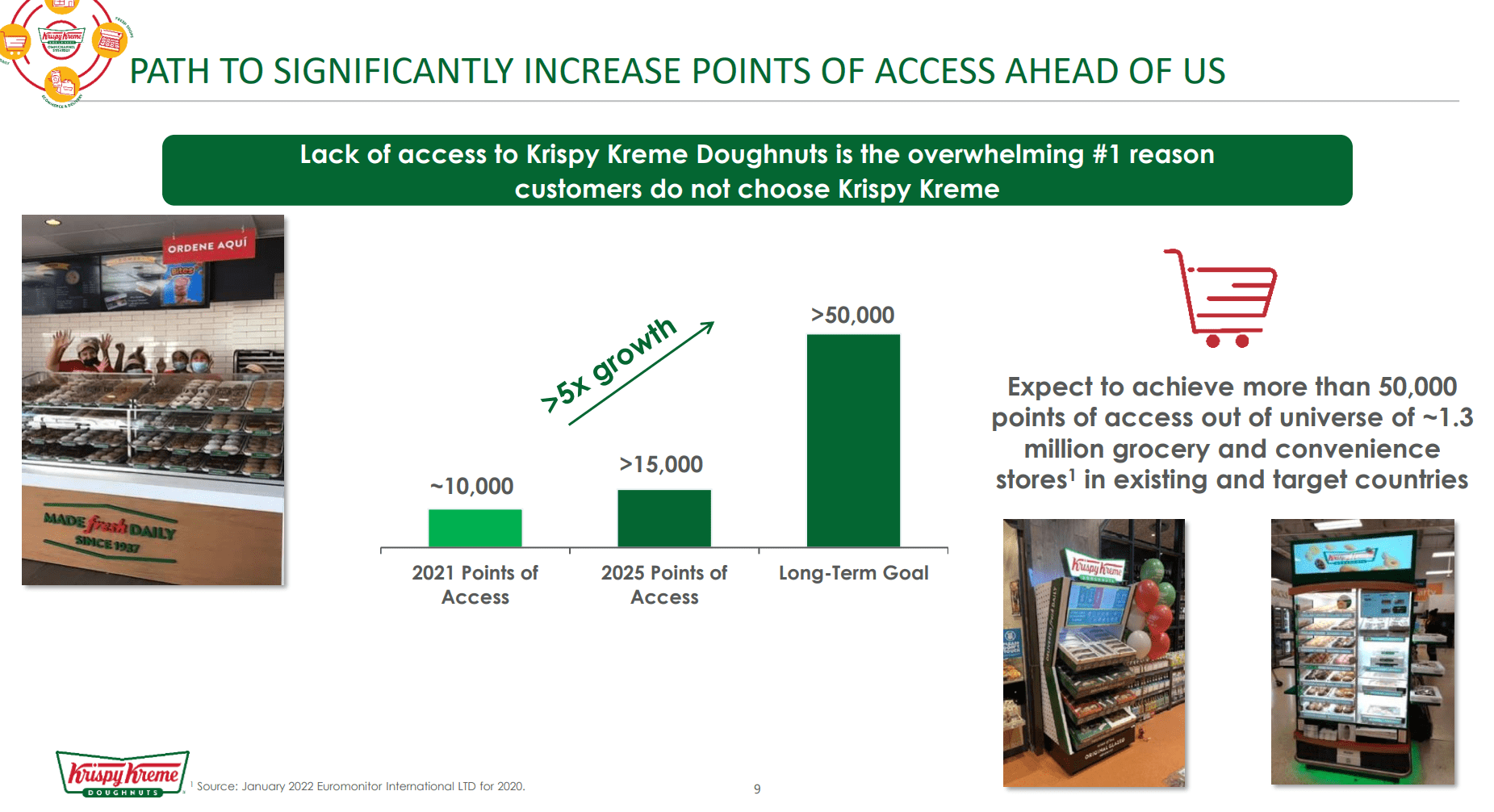

Growing Access Points To Reach More Consumers

According to the company’s research, the primary reason customers do not choose Krispy Kreme donuts is due to lack of access. Hence the company has been focused on growing the number of retail access points where customers can purchase Krispy Kreme donuts, with a long-term goal of 50,000 points of access (Figure 3).

Figure 3 – Krispy Kreme Business Strategy (DNUT investor presentation)

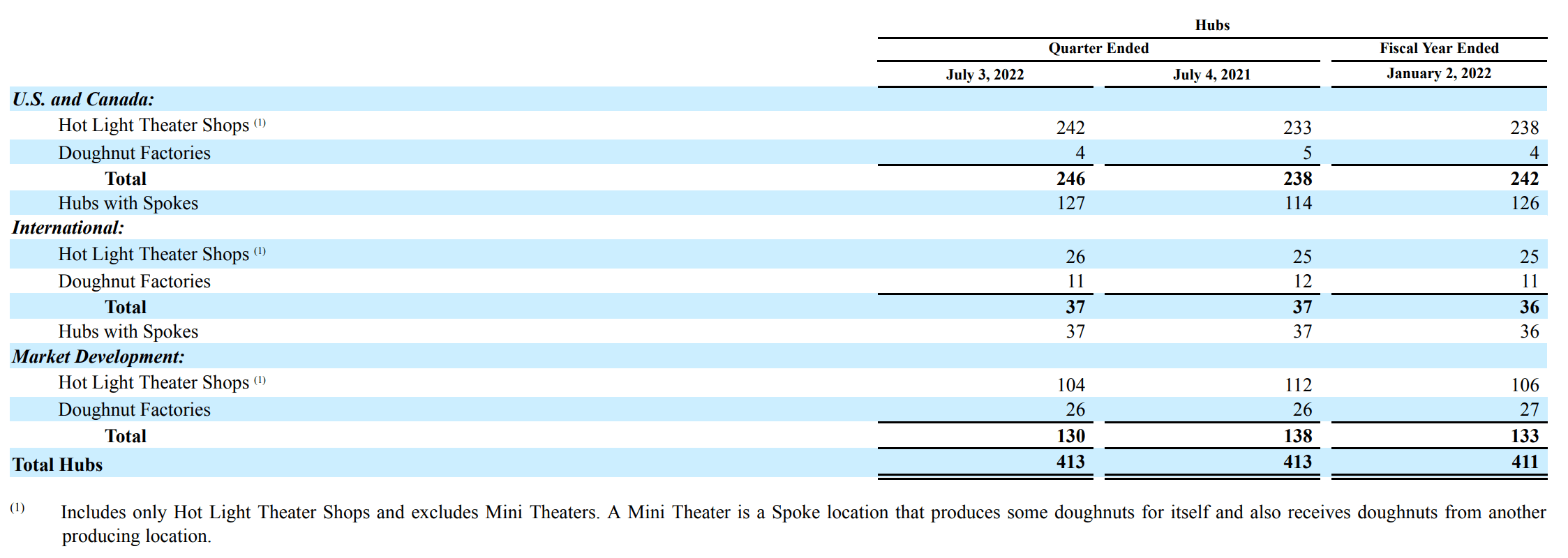

The company employs a hub-and-spoke model, where “Hot Light Theater” shops and “Doughnut Factories” act as centralized production facilities (“hubs”) delivering donuts to food trucks, kiosks and carts (“spokes”). As of July 31, 2022, Krispy Kreme had 413 hubs serving over 11,000 access points (Figure 4).

Figure 4 – Krispy Kreme Hubs (DNUT Q2/2022 10Q Report)

Krispy Kreme Returned To Public Markets

Krispy Kreme returned to the public markets in 2021 after a 5-year hiatus in a not-so-well received IPO. Krispy Kreme priced its IPO at $17 a share, far below the initial range of $21 to $24. At $17 / share, the IPO valued the company at $2.8 billion market cap, still more than double the $1.35 billion JAB Holdings paid to acquire the company in 2016.

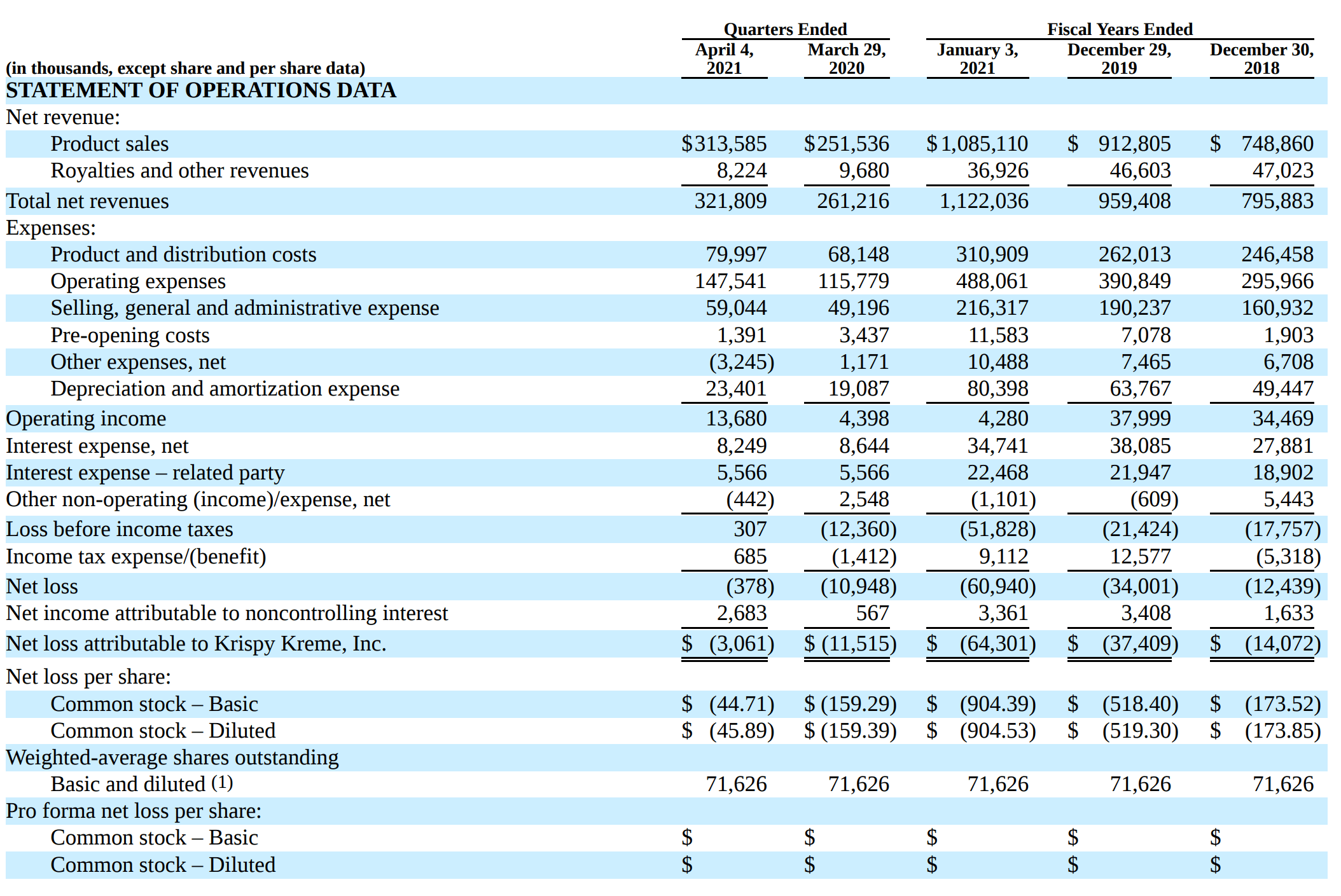

In 2015, the last year of Krispy Kreme’s operation as a public company prior to the privatization, the company generated $513 million in revenue and $32.4 million in net income. As Krispy Kreme had grown revenues to $1.1 billion by 2020, the revenue growth was used as justification for the IPO valuation (Figure 5)

Figure 5 – Krispy Kreme Pre-IPO Financials (DNUT S1 Prospectus)

Although revenues have grown rapidly at a 16.9% CAGR between 2015 to 2020 ($513 million to $1.12 billion from 2015 to 2020), investors should note that corporate profitability actually declined substantially, from 6.3% net margin in 2015 to -5.7% in 2020.

While much of the profitability decline be traced to financial leverage JAB used to acquire the company, even if we look at the operating profit line, we can see material deterioration from $52.1 million in 2015 to $4.3 million in 2020.

Public Financials Have Not Been Robust

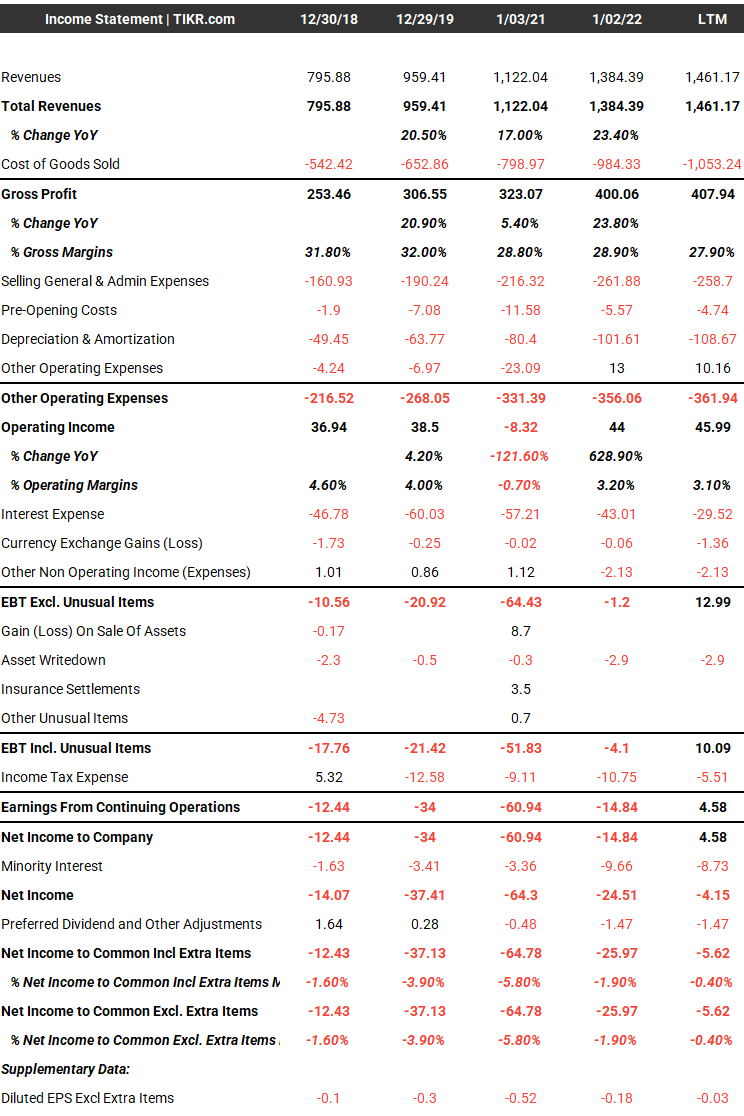

Financial results since the IPO have continued to be less than robust. In the last twelve months, DNUT’s revenues were $1.46 billion, 30% higher than calendar 2020. However, net income for the company was only breakeven (Figure 6).

Figure 6 – Krispy Kreme Financials (tikr.com)

Krispy Kreme Guiding Down 2022

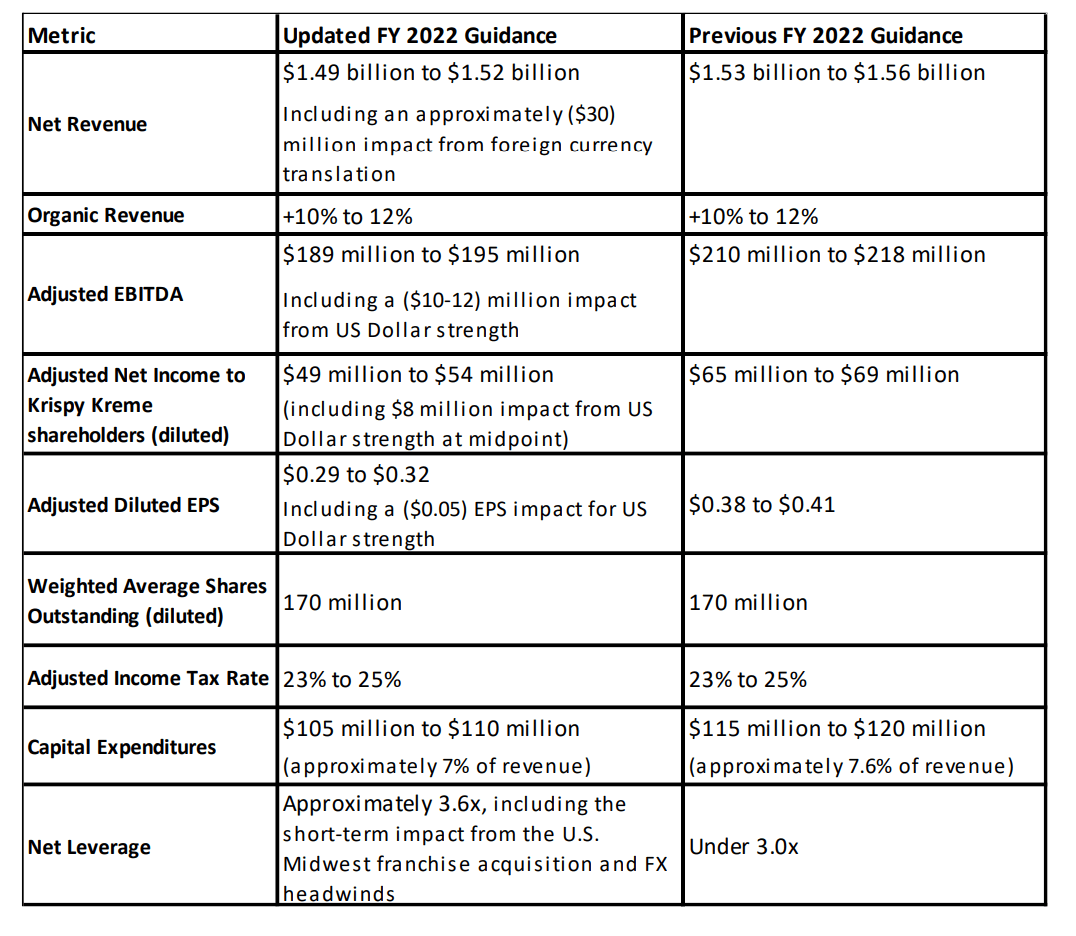

Furthermore, when Krispy Kreme reported Q2/2022 results in August, it also took down full year guidance, citing higher costs and currency headwinds (Figure 7). This caused a sharp 1-day decline in the stock price.

Figure 7 – Krispy Kreme Reduced Guidance (DNUT Q2/2022 investor presentation)

Valuation Remains Expensive

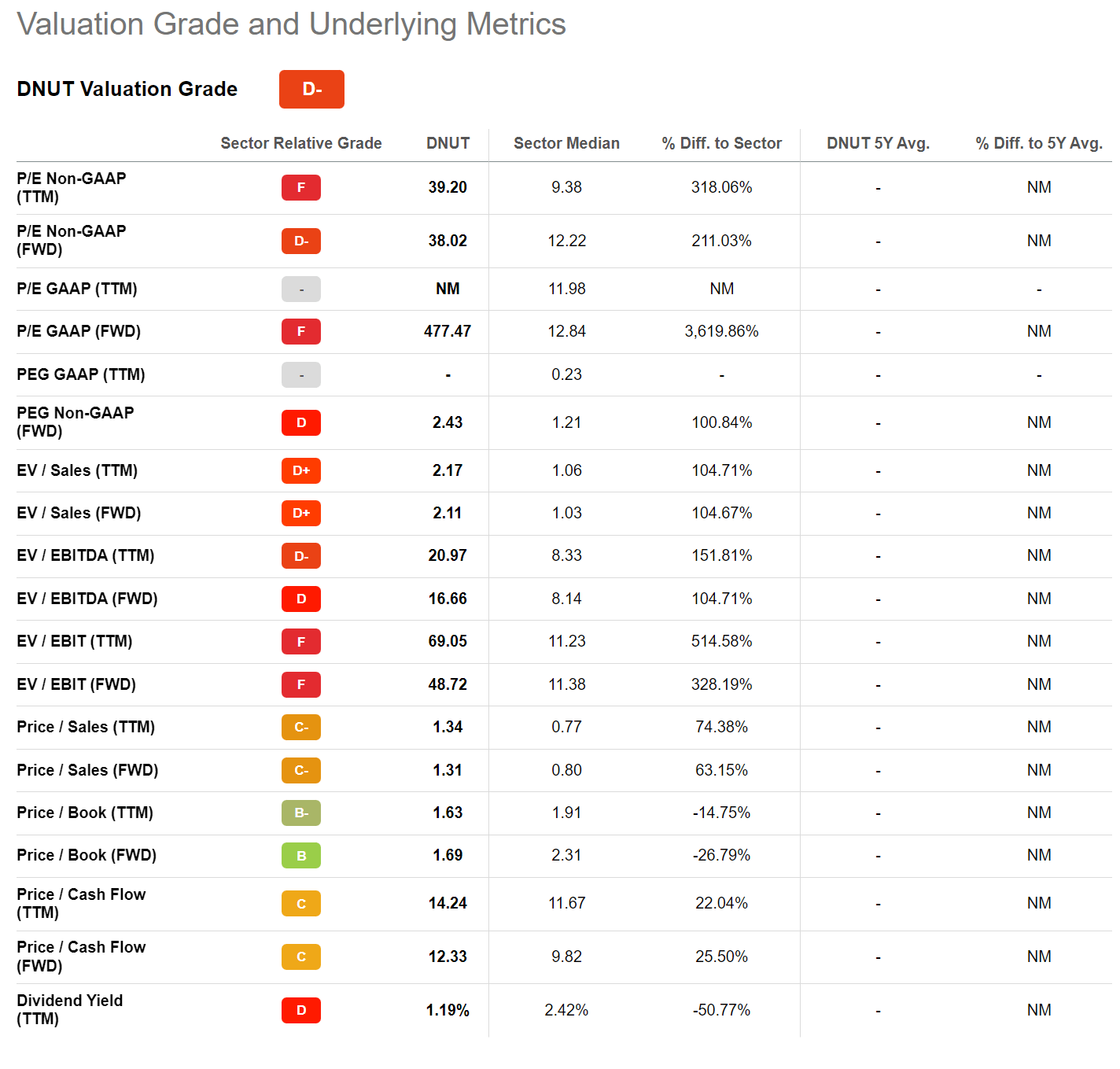

Despite the stock falling by over 30% from its IPO price to $11.50 / share recently, Krispy Kreme is still expensive on a valuation perspective (Figure 7). DNUT is currently trading at 38.0x non-GAAP Fwd P/E, far above the sector median 12.2x. On Fwd EV/EBITDA, DNUT is trading at 16.7x, more than double the sector’s 8.1x (Figure 8).

Figure 8 – Krispy Kreme Valuation (Seeking Alpha)

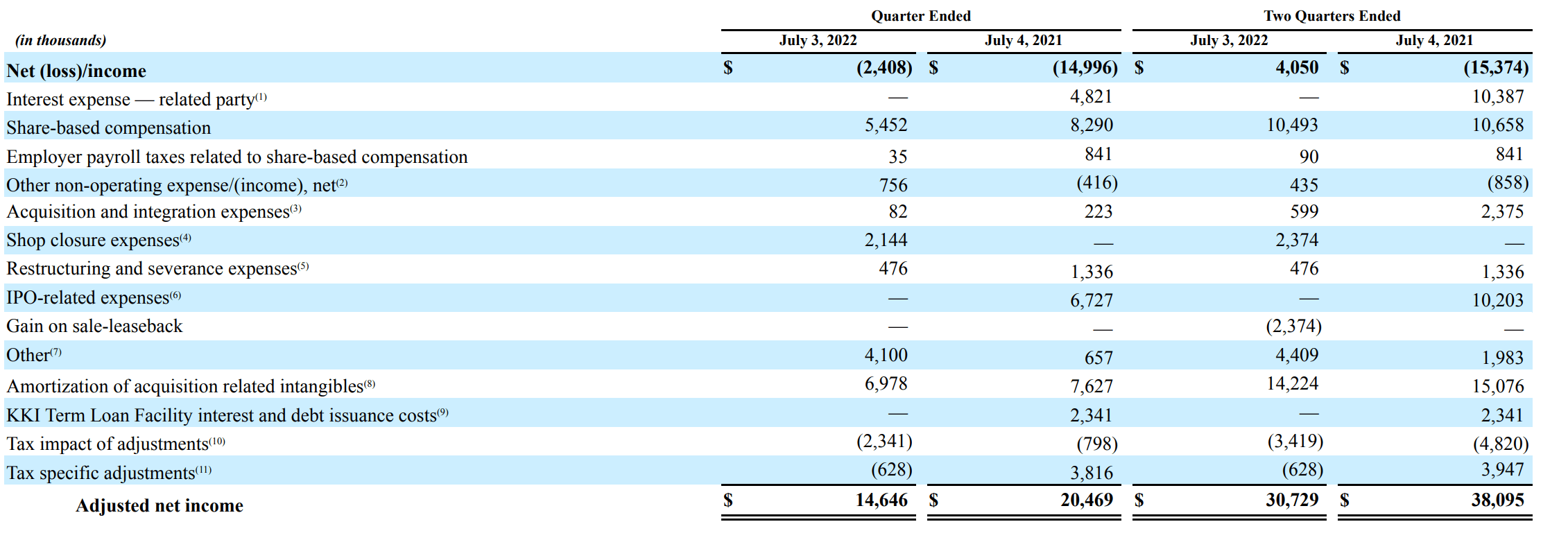

Importantly, the P/E multiple cited above is based on management’s adjusted earnings definition which excludes many line items such as share-based compensation and store closure expenses (Figure 9). If we were to look at GAAP earnings, DNUT is barely breakeven YTD and thus trades at an astronomical 477.5x Fwd P/E.

Figure 9 – Krispy Kreme Adjusted Earnings Calculation (DNUT Q2/2022 10Q Report)

Risk

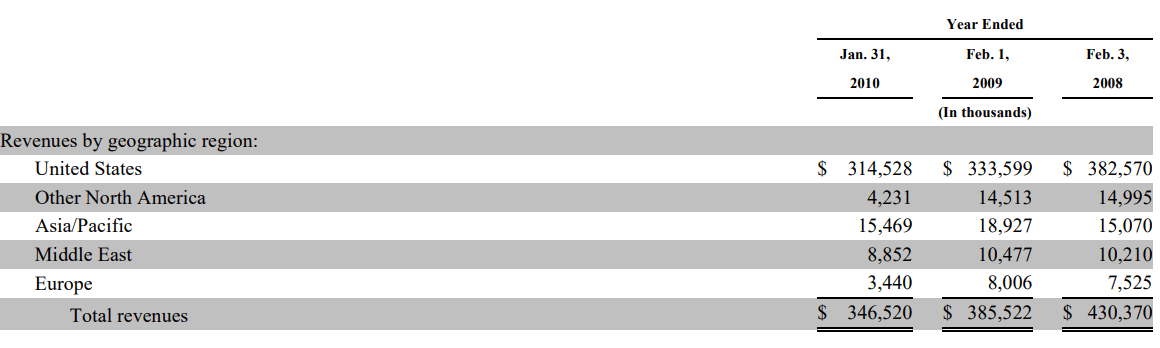

With the economy slowing down significantly, Krispy Kreme’s revenues could be at risk as well. During the 2008 global recession, Krispy Kreme’s revenues fell from $430 million in 2007 to $347 million in 2009 (Figure 10). While the current economic slowdown is not on the same scale as that of the 2008 recession, history suggests consumers may be willing to cut back on discretionary items like donuts when times are tough.

Figure 10 – Krispy Kreme Saw Steep Revenue Declines During 2008 Recession (Krispy Kreme Doughnuts Inc. 2009 10K Report)

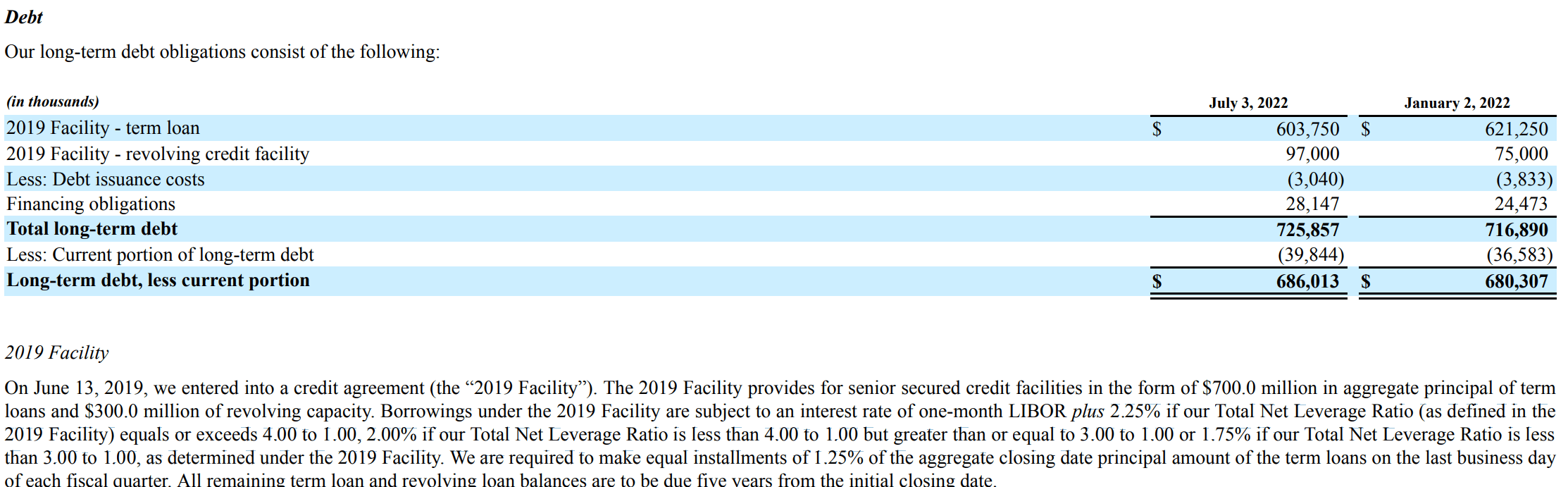

Another risk is DNUT’s relatively high leverage. Currently, Krispy Kreme has $1.2 billion in debt and capital leases, versus LTM EBITDA of $151 million. Importantly, DNUT’s $726 million in long-term debt outstanding bears interest at 1-month LIBOR plus 1.75% to 2.25%, depending on the net leverage ratio. With the Federal Reserve having dramatically increased short-term interest rates in the past few months, DNUT is now paying almost double the interest expense just a few months ago.

Figure 11 – Krispy Kreme Debt Details (DNUT Q2/2022 10Q Report)

Conclusion

While Krispy Kreme donuts may be tasty, I think investors should avoid the stock. Although management has done a good job increasing revenues, there does not appear to be a corresponding increase in profitability and earnings. In fact, based on LTM GAAP earnings, DNUT is barely a breakeven business. The company’s heavy floating rate debt load is also a cause for concern as central banks continue to ratchet up short term rates to cool inflation.

Be the first to comment