Yuriy Vinnicov

Knight-Swift Transportation Holdings Inc. (NYSE:KNX) has stood up fairly well in a very challenging economic environment that has devastated the stock price of many companies over the last year or two.

The stock hasn’t been near as volatile as many other sectors, but with the current market conditions pointing toward a drop in freight demand, along with rising expenses and cost inputs, it looks like KNX is going to have a tough year ahead of it, especially if the economy gets worse before it gets better.

Management stated it has prepared for this by reducing its exposure to the spot market, while working on cutting costs.

In this article we’ll look at some of its latest numbers, the probable impact of slowing freight demand, and how the company is likely to perform in 2023.

Some of the numbers

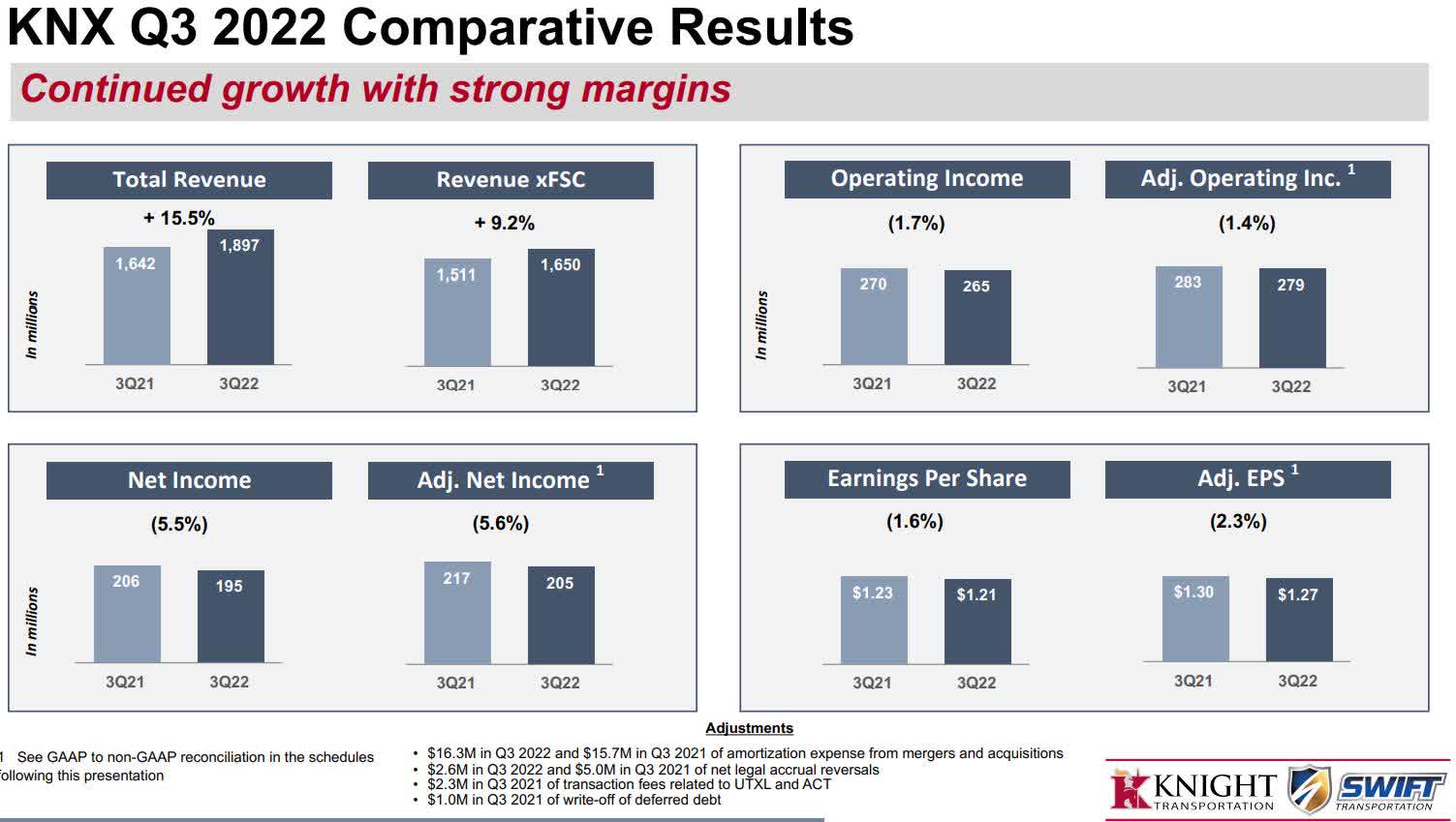

Revenue in the third quarter of 2022 was $1.9 billion, compared to revenue of $1.64 billion in the third quarter of 2021. Revenue for the first nine months of 2022 was $5.7 billion, compared to revenue of $4.2 billion in the first nine months of 2021.

Investor Presentation

Total operating expenses in the reporting period were $1.63 billion, compared to $1.37 billion in the third quarter of 2021. Total operating expenses for the first nine months of 2022 were $4.8 billion, compared to total operating expenses of $3.56 billion in the first nine months of 2021.

Net income in the third quarter was $194.8 million, or $1.21 per diluted share, compared to net income of $205.3 million, or $1.23 per diluted share in the third quarter of 2021. Net income in the first nine months of 2022 was $620.6 million, or $3.80 per diluted share, compared to net income of $487.9 million, or $2.93 per diluted share in the first nine months of 2021.

With increasing expenses and a decline in EPS in the last quarter, we should keep an eye on expenditures and cost inputs over the quarters ahead to see if there’s a pattern forming. This is especially important since the company downwardly revised EPS for full-year 2022 from $5.20 and $5.40 to $5.17 to $5.22.

The reason given for the decline in EPS was “higher interest expense, lower gain on sale, and a higher tax rate.” The impact on EPS for the quarter was approximately $0.10 per share. Taking into consideration expected increases in interest expenses going forward, downward pressure on EPS is likely to continue in 2023.

Cash and cash equivalents at the end of the third quarter of 2022 were $194.7 million, compared to cash and cash equivalents of $261 million at the end of calendar 2021. Of the $194.7 million in cash and cash equivalents at the end of the third quarter of 2022, $145 million was restricted.

The company held long-debt of $1 billion at the end of the third quarter, flat with long-term debt at the end of calendar 2021. Including its revolver which is due by September 3, 2026, total long-term debt was $1.19 million.

Segment overview

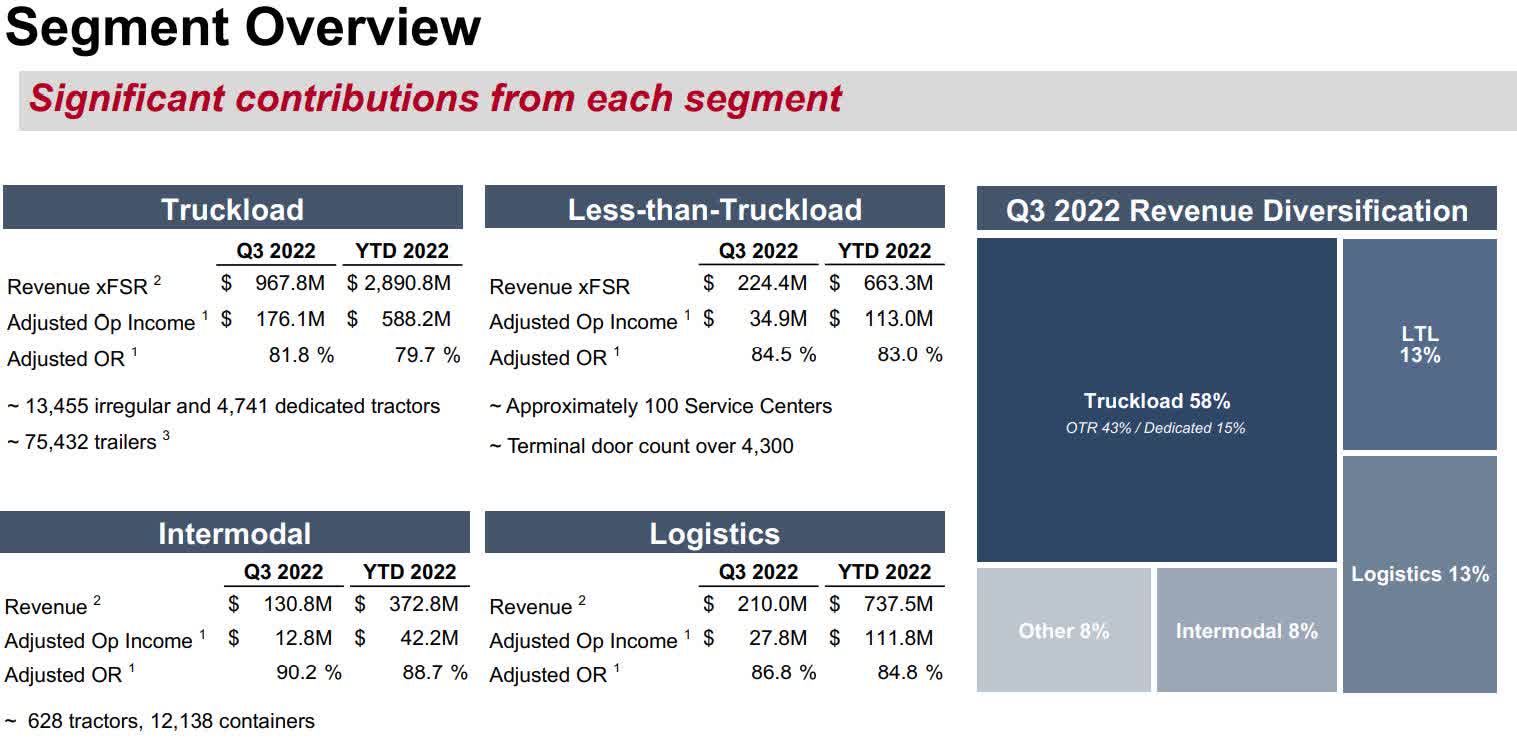

Revenue in Truckload was $967.8 million; Less-than-Truckload, $224.4 million; Intermodal 413.8 million, and Logistics $210 million. Truckload represented 63 percent of earnings, lowering the company’s risk to that segment, as it was much higher in the past.

Investor Presentation

Revenue by diversification was Truckload, 58 percent; LTL, 13 percent; Logistics, 13 percent; Intermodal, 8 percent; and Other, 8 percent.

The most important thing I want to point out here is when the next trucking downturn comes, which may already be upon the company, its diversified revenue base should help it mitigate the effects it would have had when Truckload revenue was a higher percentage of total revenue.

Market appears to be slowing down

With management pointing out freight demand started to drop below seasonal levels in the second half of the third quarter and continued on into the early fourth quarter as of the time of the earnings call, it’s highly probable the trucking market is entering into a slowdown.

Of particular note was that spot opportunities have dropped significantly in the third quarter, and consequently, the KNX said it reduced its exposure “in the bid season” to the spot market. For that reason, it expects the peak season to be down for the year.

Citing “depressed rates, higher fuel prices, higher fixed equipment costs, rising insurance costs, and now elevated interest rates that will most likely continue to rise,” the company sees this as having an impact on small carriers because they historically have more exposure to the spot market. KNX sees this result in an attrition in capacity which it believes will accelerate in the quarters ahead.

Management said it has been preparing for the truckload market to slow down and has taken steps to mitigate it in 2023 by adjusted costs and decreasing its exposure to the spot market. One piece of evidence with this is the fact there was a drop in miles per tractor by 4.2 percent, even though revenue was up 1.8 percent per tractor during the same period. For now, the company has retained some pricing power, but if economic conditions worse, that’s likely to dissipate.

Conclusion

Compared to many other sectors, KNX has been performing fairly well in a challenging economic environment, but I believe that is coming to an end, based upon slowing freight demand.

With interest rates sure to rise for at least a couple of more months, freight demand slowing, and the economy expected to slow, I think KNX may have reached a ceiling on its share price at near $59.00 or so. It could of course get a temporary upward move in relationship to momentum, but with the visibility we have today, that doesn’t appear to be sustainable.

TradingView

While the company boasts of having the largest truckload trailer fleet at over 75,000, that can be a headwind in times of economic downturn.

With expenses and cost inputs rising, with freight demand slowing down, the company is likely to have a challenging year ahead of it; especially in the first half.

Since management pointed out that its strong balance sheet provides it flexibility to take a number of actions beneficial to shareholders, including new acquisitions, increasing dividends, purchasing more shares, or pay down debt, it provides a support level that probably won’t test new lows below the 52-week low of $42.50 per share. The only thing I think could drive it below that would be a deep recession that last longer than currently expected.

On the other hand, a potential positive catalyst would be the type of acquisition that had the potential to meaningfully drive revenue and earnings up. Under the current market conditions, I don’t see that happening.

I think that best moves for the company over the next year would be to share profits with shareholders via share buybacks, increasing its dividend, or paying down debt.

Be the first to comment