rarrarorro/iStock via Getty Images

Introduction

When I last discussed KKR Real Estate Finance Trust (NYSE:KREF), I didn’t want to wait for the REIT to publish its Q3 results as I thought the preferred shares offered an interesting opportunity to pursue high yield at an acceptable risk. We are now almost three months later and I wanted to have another look at this interesting series of preferred shares, which are trading with (NYSE:KREF.PA) as ticker symbol.

The Q3 results were pretty satisfying, but Q4 may be different

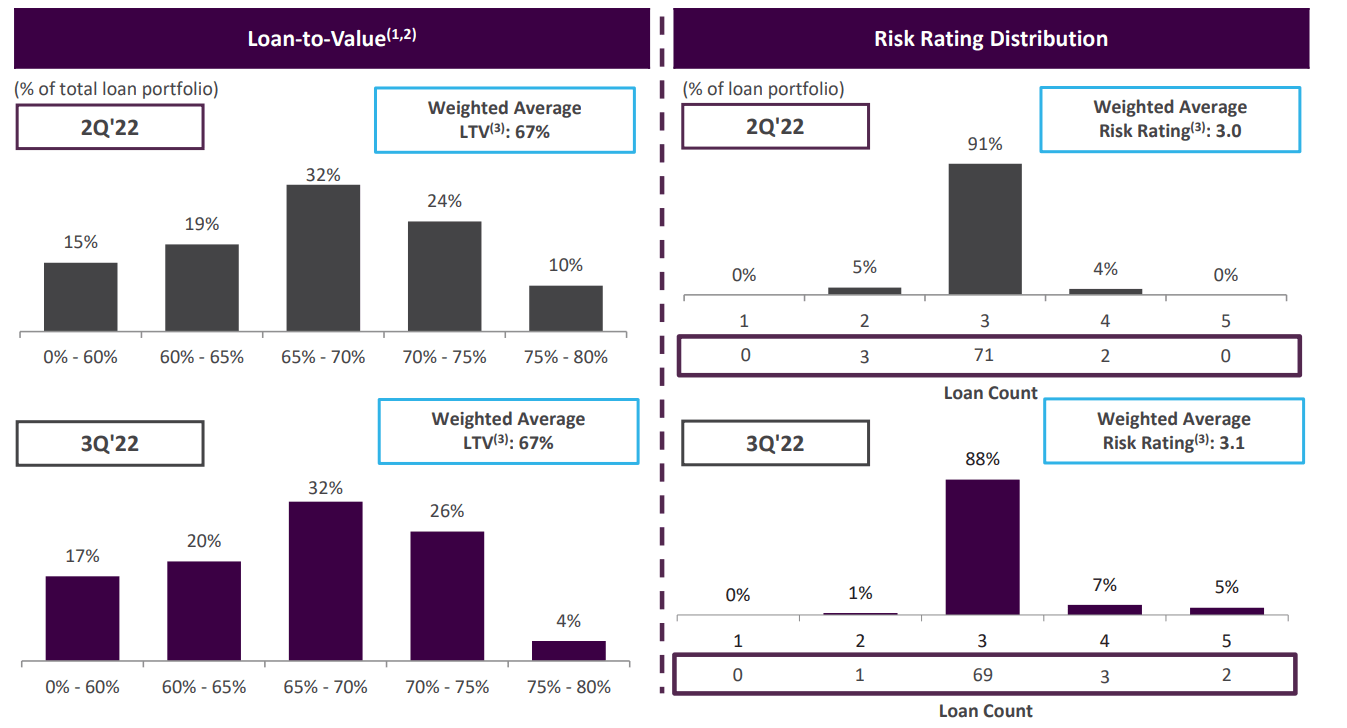

KKR Real Estate Finance Trust originates and invests in transitional senior loans backed by real estate. As of the end of September, the average LTV ratio in the loan portfolio was approximately 67% but as you can see below, the total percentage of loans in the 70%+ LTV category has dropped from 34% to 30% on a QoQ basis.

KREF Investor Relations

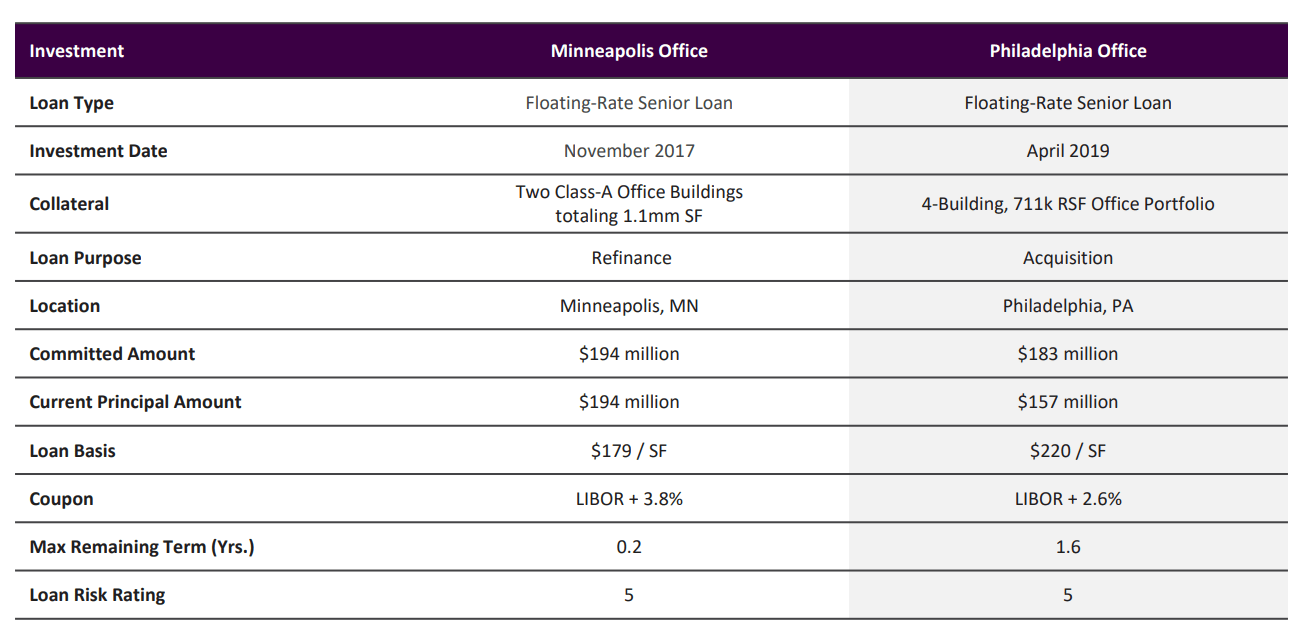

There are two loans with risk category five, and KREF has been pretty transparent about these loans as they were highlighted in the Q3 presentation (see below) and on the Q3 conference call.

KREF Investor Relations

While the owner of the Philadelphia buildings is looking to refocus its business and KREF is looking into either selling the loan or the assets, KREF didn’t appear to be too worried about the Minneapolis loan. From the Q3 conference call:

the Minneapolis loan is secured by 1.1 million square foot, two building Class A property. Our loan supported the refinance remaining CapEx and subsequent lease up of the property from occupancy of 62% at closing to an occupancy rate of 88% today.

NOI from the property generates a current debt yield of over 8%, fully covering the debt service on our loan. However, the loan has an upcoming final maturity date in December ’22. And the sponsor has indicated an inability to refinance the loan given current market conditions.

December is now behind us and unfortunately KREF has not provided an update yet on this loan, so I am looking forward to seeing the recent developments there and if KREF just plans to sell the office buildings.

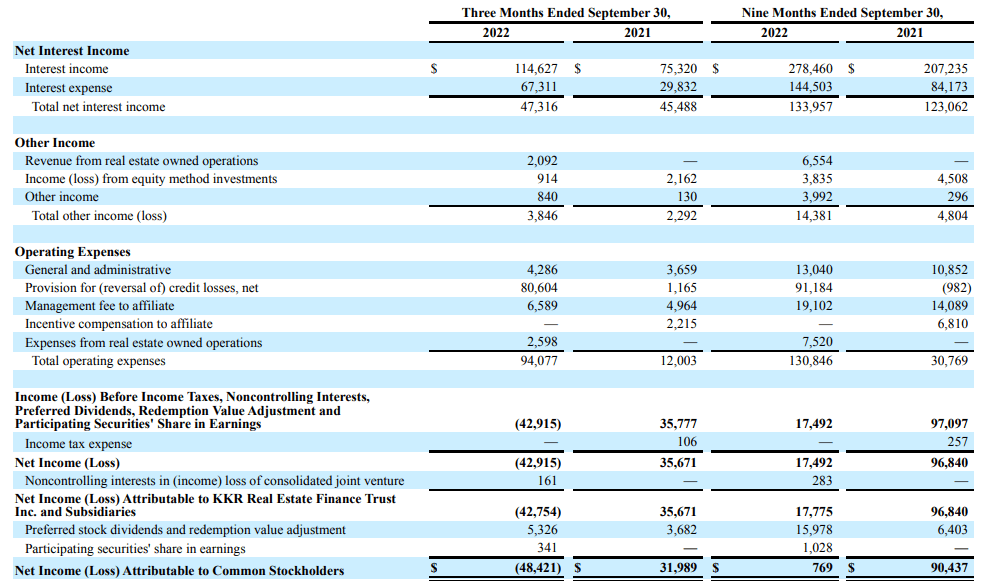

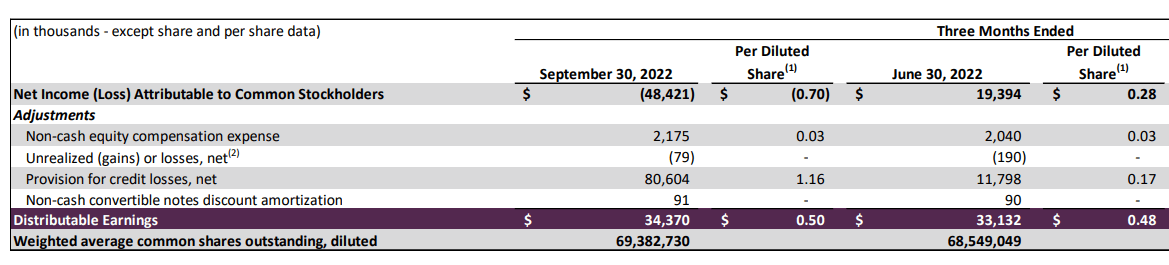

Impairment charges will weigh on the net income but the preferred shares should be pretty well shielded from that. As you can see below, KREF generated about $47M in net interest income in the third quarter of this year, resulting in a net loss of $43M after already taking a $80.6M impairment charge to cover future credit losses.

KREF Investor Relations

While this also means the preferred dividends were not covered based on the earnings and the net loss attributable to KREF’s common unitholders exceeded $48M, keep in mind those loan loss provisions are non-cash expenses and have no impact on the REIT’s ability to generate cash flow. Of course we cannot ignore that some of the loans go sour but keep in mind this will be predominantly borne by the common unitholders as the book value of the KREF common units will erode.

Looking at the distributable cash flow for the third quarter, KREF’s underlying distributable cash flow was approximately $34.4M or $0.50 per share. This means the common distribution of $0.43 per quarter is still fully covered by the distributable cash flows.

KREF Investor Relations

This means that by retaining $0.07 per quarter in distributable earnings it doesn’t pay out, KREF retain approximately $10M per year in earnings which could be helpful to shore up the balance sheet.

But what’s more important from the perspective of a preferred share investor is the implication the preferred dividends are well covered. Adding back the preferred dividends ($5.33M) to the distributable earnings means the distributable earnings pre-dividends comes in at $39.7M. Which means KREF only needs 13.4% of its pre-dividend distributable earnings to cover the preferred dividends. Or even more important: even if KREF would have to realize losses of $130M per year, the preferred dividend would still be covered. Those losses would still be non-cash losses, but it explains how much in loan losses KREF can absorb with its recurring income.

A recap of the preferred shares

As explained in my previous article: KREF has one series of preferred shares available, which were issued in April 2021. The company issued cumulative preferred shares at the normal price of $25 and with a preferred dividend yield of 6.5%. This means these securities are paying $1.625 per year in preferred dividends, in four equal quarterly installments of $0.40625 and the preferred dividend yield will remain unchanged for as long as these securities remain outstanding. (KREF.PA) can be called by KKR Real Estate Finance Trust from April 2026 on.

As the preferred shares are currently trading at $17.78, they currently offer a yield of $1.625 / $17.78 = 9.14%.

While that is indeed lower than the 12% yielding common shares, keep in mind the preferred dividends are prioritized over the payments on common units. Additionally, KREF’s preferred shares are cumulative in nature and in the event of a temporary suspension KREF would have to make its preferred shareholders whole for any missed payments before it would be allowed to pay a distribution on the common units. And just to be clear, there are no indications KKR Real Estate Finance Trust is contemplating a suspension as its Q3 results clearly showed it can easily cover all preferred dividend payments.

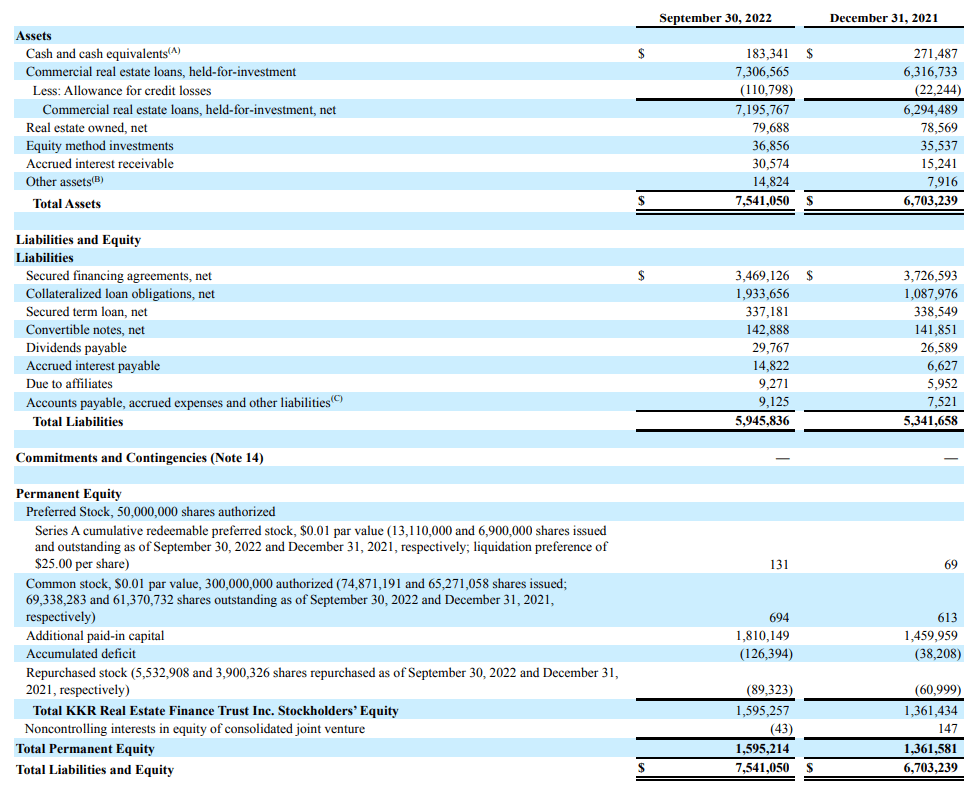

Looking at the balance sheet, KREF’s balance sheet contained just over $7.5B in assets of which almost $1.6B was equity. As there are about 13.1M preferred shares issued, the total value of the prefs is approximately $327.5M. Which means there’s in excess of $1.35B in equity ranked junior to the preferred shares.

KREF Investor Relations

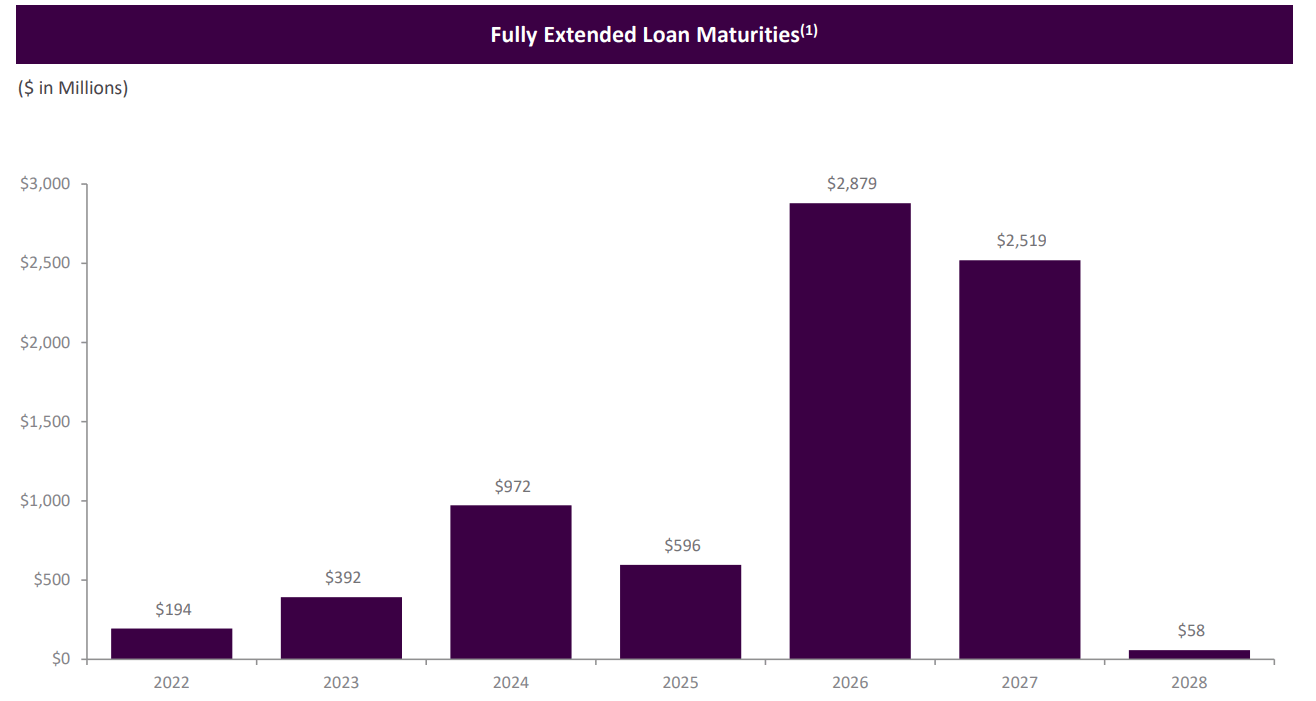

While that is a nice cushion, we shouldn’t forget KREF’s balance sheet is still highly levered. Interestingly, the vast majority of the loans is maturing in 2026 and beyond. Only 28% of the loans matures before 2026 and the existing loan loss provision of in excess of $100M should provide a decent cushion for near-term defaults. The image below shows the loan maturity dates. The $194M loan maturing in 2022 was the Minneapolis office loan I discussed earlier in this article. The other problem child, the 2023 Philadelphia loan, is included in the $392M maturing in 2023.

KREF Investor Relations

While maturities are spread out over time, it is perhaps not ideal to see about 60% of the 2022 and 2023 loan maturities are troubled loans. The other loans maturing before the end of this year are a $130M hospitality loan (risk category 3, 66% LTV) and an $81M office loan in Seattle (risk category 3, 56% LTV ratio) and hopefully these will roll off without any issues.

Based on the Q2 results presentation, the LTV ratio for the Minneapolis asset was 77%, while the LTV ratio on the Philadelphia office loans was 71%. This means the theoretical underlying value of the buildings for the $350M loans was $478M. And assuming the majority of the $80M loan loss provision recorded in the third quarter was related to these two assets, KREF will be able to avoid additional losses if it is able to recoup at least $270M for the assets.

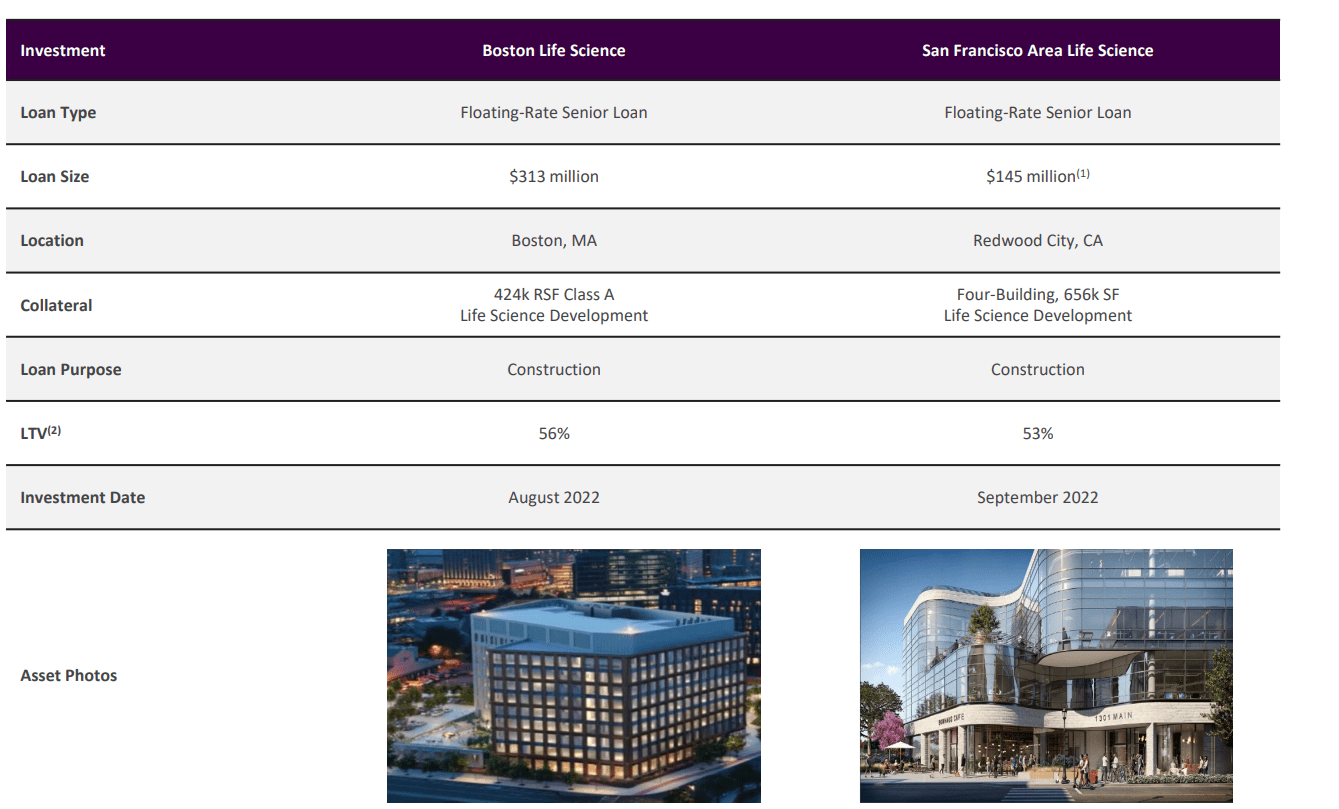

Fortunately, the short duration of the loans means KREF usually gets a pretty good idea of how the borrowers are doing. And it allows the REIT to recycle the capital and invest it in loans with a lower average LTV ratio. During the third quarter, KREF issued almost $500M in construction funding for two assets with an average LTV ratio in the mid-50s range.

KREF Investor Relations

Investment thesis

I have no intention to buy the common units of KKR Real Estate Finance Trust until I see how the two troubled loans will be dealt with. I like the more conservative approach during the third quarter as the LTV ratio for the new construction loans is relatively low. I hope the Minneapolis and Philadelphia assets can be sold without KREF losing its shirt.

This uncertainty also makes the preferred shares riskier and that’s why the preferred dividend has increased to in excess of 9%. Fortunately the higher interest rates also have a positive impact: a 150 basis point increase in the LIBOR/SOFR will increase the net annual interest income by approximately $20M per year, and this could provide an additional cushion to absorb more loan defaults.

Only time will tell. And despite the cumulative nature of the preferreds and its seniority over the common units, KREF’s preferred shares are still a bit speculative. I currently have no position in KREF.PA.

Be the first to comment