abadonian/iStock via Getty Images

Pipeline operator Kinder Morgan (NYSE:KMI) submitted its earnings sheet for the fourth quarter recently and the midstream company convinced with double-digit distributable cash flow and EBITDA growth. Kinder Morgan also maintained a very low DCF-based payout ratio which indicates that the midstream firm has considerable potential to grow its dividend over the longer term. I believe that the risk profile for Kinder Morgan, especially when considering the firm’s cash flow stability, is extremely attractive and I consider KMI a buy from a valuation, dividend coverage and yield point of view!

Strong financial results back the bull case for Kinder Morgan

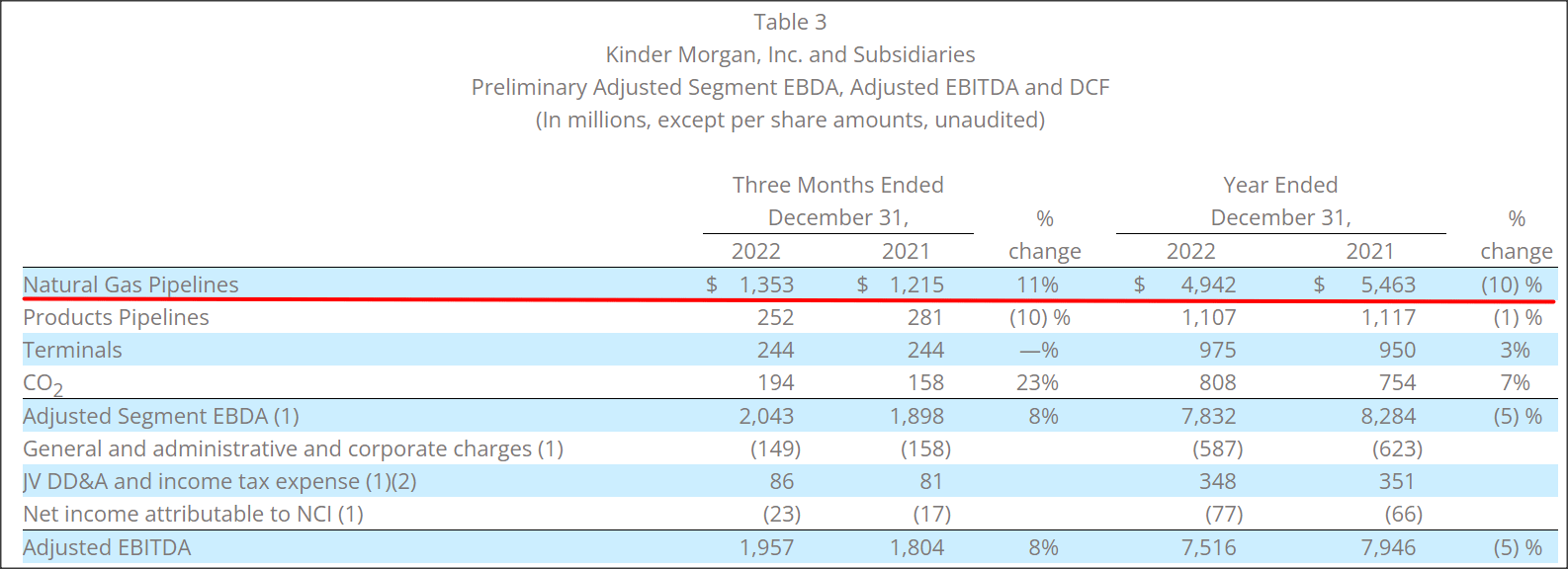

Kinder Morgan proved strong financial performance with its fourth-quarter earnings sheet in January. The midstream company’s performance was once again driven by Kinder Morgan’s natural gas pipeline business which delivered 11% year over year EBDA growth to $1.35B and the segment accounted for 66% of earnings before depreciation and amortization in Q4’22. Kinder Morgan’s adjusted EBITDA grew 8% year over year to $1.96B in the fourth-quarter, largely because of the firm’s robust performance in the natural gas business. As I indicated last year, Kinder Morgan generates the majority of its income from fee-based contracts with producers that pay the midstream firm a fixed price for the transportation of raw materials. This contract feature greatly limits Kinder Morgan’s pricing risks and translates to predictable cash flow.

Source: Kinder Morgan

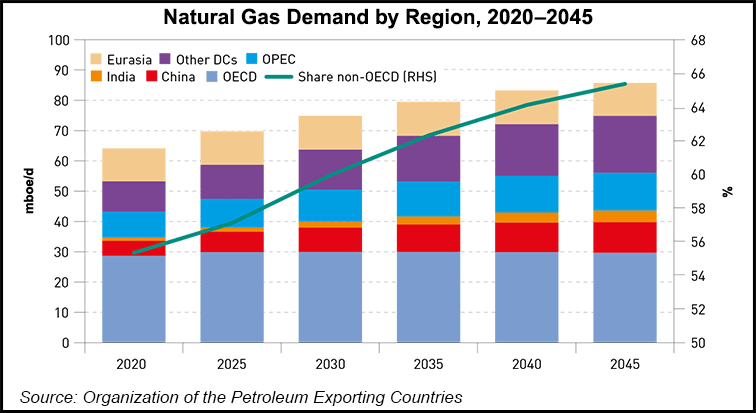

The transportation of natural gas on behalf of the company’s customers is supported by growing demand for natural gas. Natural gas is one of the cheapest forms of low-carbon energy sources and demand for natural gas is growing as a result. I believe Kinder Morgan’s natural gas focus — although the midstream also operates refined products pipelines and terminals — is a key asset for the company long term.

Natural gas demand is set to rise in all regions in the world between 2020 and 2045: the Organization of the Petroleum Exporting Countries (OPEC) projects that natural gas demand will rise from 64.2 million boe/d in 2020 to 85.7 million boe/d in 2045, showing 33% total growth.

Source: OPEC

Turning to Kinder Morgan’s distributable cash flow.

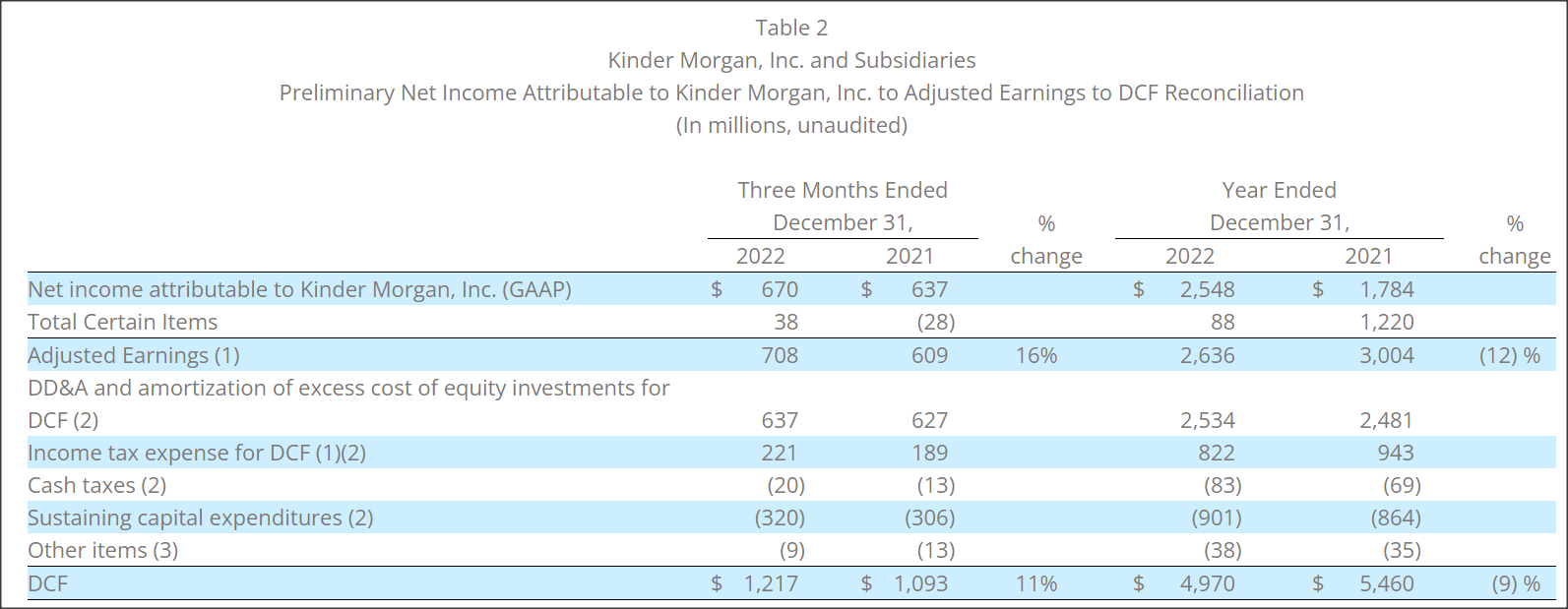

Due to Kinder Morgan’s strong results in natural gas, the firm’s distributable cash flow grew 11% year over year to $1.22B. Because of the fee-based contract basis, Kinder Morgan experiences little volatility in cash flow and it is usually more than sufficient to cover the firm’s dividend.

Source: Kinder Morgan

Kinder Morgan continues to offer dividend investors very solid dividend coverage

Kinder Morgan reported $0.54 per share in distributable cash flow in the fourth-quarter, showing an increase of 12.5% year over year (see table below). The midstream firm’s payout ratio in the fourth-quarter was 51.4% while Kinder Morgan’s payout ratio in FY 2022 was 50.7%. The dividend is therefore extremely well covered by distributable cash flow and sustainable.

|

KMI |

Q4’21 |

Q1’22 |

Q2’22 |

Q3’22 |

Q4’22 |

Y/Y Growth |

|

Distributable Cash Flow |

$0.48 |

$0.64 |

$0.52 |

$0.49 |

$0.54 |

12.5% |

|

Declared Dividends |

$0.27 |

$0.28 |

$0.28 |

$0.28 |

$0.28 |

2.8% |

|

DCF Payout |

56.3% |

43.4% |

53.4% |

56.6% |

51.4% |

-8.6% |

(Source: Author)

Outlook for FY 2023

Kinder Morgan also released its guidance for the current fiscal year which calls for $7.7B in adjusted EBITDA and $4.8B in distributable cash flow. I believe the natural gas segment could deliver a stronger than expected performance if demand remains high and the US economy doesn’t have to fight off a recession.

Source: Kinder Morgan

Kinder Morgan’s valuation

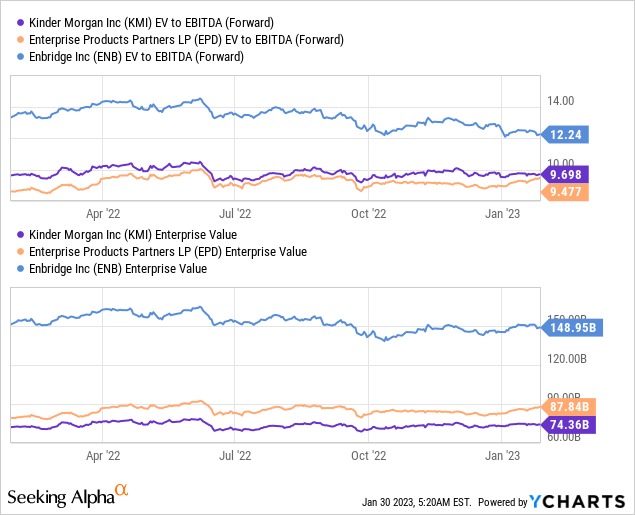

Kinder Morgan is an attractively valued large-cap midstream firm with a forward EV/EBITDA ratio of 9.7 X. Enterprise Products Partners (EPD) has a similar EV/EBITDA ratio of 9.5 X and Enbridge (ENB) has an EV/EBITDA ratio of 12.2 X. Besides Kinder Morgan, I also really like Enterprise Products from a distribution coverage and growth perspective.

Risks with Kinder Morgan

The biggest commercial risk for Kinder Morgan, in my mind, is the potential for investment restrictions in the fossil fuel sector. As political pressure grows to invest more money into green energy sources, investment opportunities in the fossil fuel industry — which includes natural gas pipeline systems and storage capacity that are Kinder Morgan’s specialty — may not get fully exploited, potentially leading to moderating distributable cash flow and dividend growth for Kinder Morgan in the future. What would change my mind about Kinder Morgan is if the midstream firm saw a decline in its distributable cash flow and a corresponding increase in its DCF-based payout ratio.

Final thoughts

Kinder Morgan is top energy holding and I believe the company’s natural gas focus is a key asset for the midstream firm as demand is expected to continue to grow going forward. With a payout ratio of 51% Kinder Morgan serves up a very healthy 6% midstream yield that is supported by long term, fee-based transportation contracts. I also consider Kinder Morgan’s valuation based off of EBITDA to be competitive and the risk profile, in my opinion, is also very favorable for dividend investors looking for stable dividend income for years to come!

Be the first to comment