MarsBars

It’s no secret that office REITs are in a tough pricing environment, with most of the names being down materially over the past 12 months. It seems, however, that the baby has been thrown out with the bathwater, as even high quality names like Kilroy Realty (NYSE:KRC) are still trading down in the dumps.

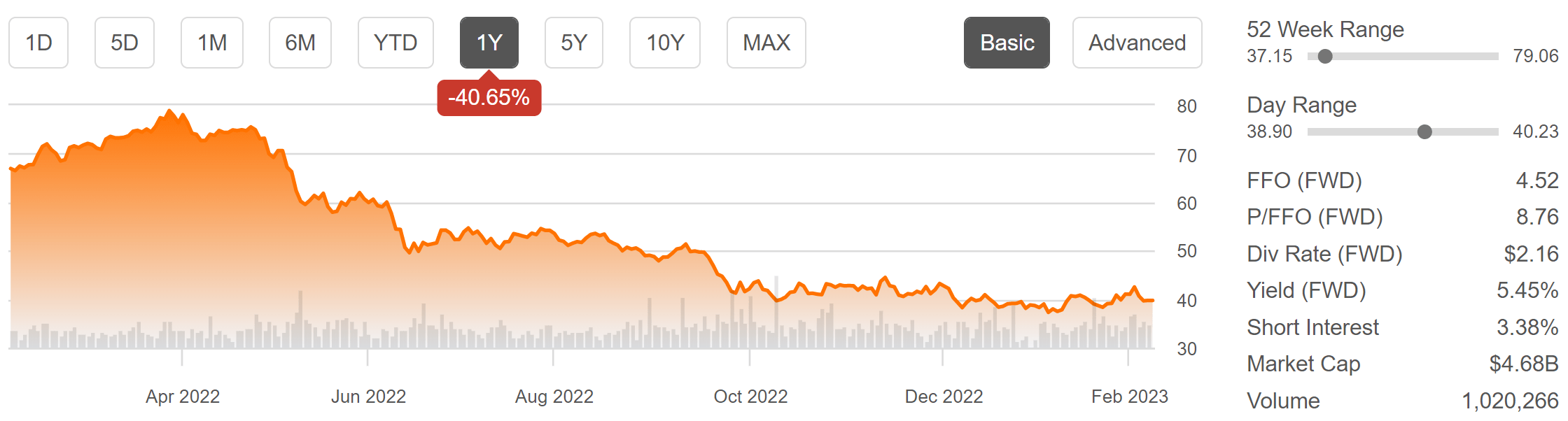

As shown below, KRC is currently trading just shy of its 52-week low and sits at close to half of its 52-week high of $79. In this article, I highlight what makes KRC an excellent buy at current levels, so let’s get started.

KRC Stock (Seeking Alpha)

Why KRC?

Kilroy Realty is an internally-managed REIT that’s been around for over 7 decades, well longer than most other REITs in the market today. It’s also a member of the S&P MidCap 400, and is focused on acquiring, developing, and managing office and mixed-use properties. KRC is led by long-term CEO and namesake, John Kilroy, who’s served as CEO since it was a private company prior to the mid-1990s.

What sets KRC apart from other office REITs is its heavy focus on owning newer Class-A buildings in high barrier-to-entry West Coast urban markets. It’s also positioning its portfolio towards the emerging life sciences category, which comes with sticky tenant relationships. This is also well-suited for KRC’s markets, as they are home to a number of leading research institutions in the higher education space.

Meanwhile, KRC is demonstrating strong growth, as it achieved 9% YoY revenue growth during the fourth quarter to $284 million. It also marks the first time in which KRC achieved annual revenues in excess of $1 billion. Importantly, growth is translating to the bottom line, as FFO per share grew by an impressive 11% YoY to $1.17.

These results were driven by an overall healthy 93% leased rate as of the end of 2022. KRC is also seeing strong demand from tenants, as it concluded 2022 with the highest quarterly leasing volume, signing 328K square feet of new and renewing leases, including 102K square feet of leases signed in the development portfolio. This is also reflected by the strong GAAP and cash rent spreads of 31% and 12%, respectively.

Looking forward, KRC has plenty of capacity to fund its development pipeline, as it has $1.7 billion of total liquidity, including $290 million worth of cash and cash equivalents on hand. It’s reasonably leveraged with net debt to EBITDA of 6x (BBB credit rating), and 95% of its debt is unsecured with no maturities until Q4 of 2024, thereby mitigating interest rate risk in the near term.

Looking ahead, Hoya Capital believes that utilization rates for office space should continue to improve and believes that the market sentiment around office REITs is skewed too negative. This was reflected by Hoya Capital’s recent report this week, noting as follows:

Based on recent survey data discussed in more detail below, we believe the ultimate post-pandemic “trend level” of utilization rates is around 60% of pre-pandemic levels in primary urban metros – up from roughly 45% today, implying a 3-day/week average in-person attendance. we have indeed seen more companies use office “mandates” as part of their workforce reduction strategies including recent examples from Disney (DIS), Starbucks (SBUX), Google (GOOG).

We believe that employers will seek to trim only about half of this incremental “unused” space in their next renewals, implying about a 15-25% reduction in “same company” demand in primary urban metros and 5-10% in secondary markets – which is likely quite a bit more optimistic for office demand than implied by office REIT valuations, which appear to imply cuts that match the lower utilization rates on a 1-for-1 basis.

Meanwhile, KRC pays a respectable 5.4% dividend yield. The dividend is well covered by a 46% payout ratio (based on Q4 FFO per share of $1.17). It also comes with a 5-year dividend CAGR of 5.1% and 7 years of consecutive growth.

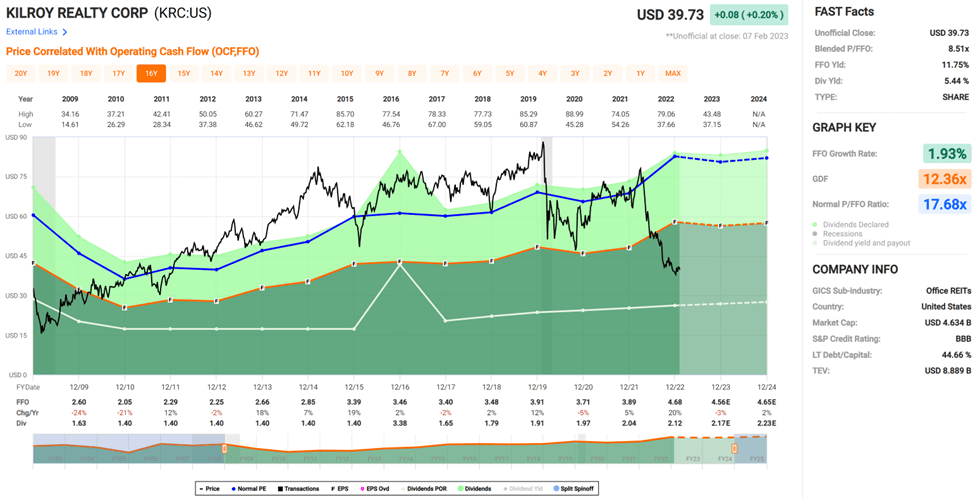

Lastly, I find KRC to be dirt cheap at the current price of $39.73 with a forward P/FFO of 8.8, sitting far below its normal P/FFO of 17.7. While analysts expect just 4% FFO per share growth next year, that should be more than ok for a quality company like KRC with such a low valuation. Analysts also have a consensus Buy rating on the stock with a conservative price target of $47.47, which could still translate to double-digit total return potential in the near term.

FAST Graphs

Investor Takeaway

Kilroy Realty is a high quality office REIT with strong operational fundamentals, solid dividend yield, and a dirt cheap valuation. It’s well positioned to benefit from the ongoing recovery of the office space market, and this is reflected by its recent strong quarterly results. Investors today get a solid yield combined with capital appreciation potential should it revert anywhere close to its normal valuation.

Be the first to comment