serts/E+ via Getty Images

Key Tronic (NASDAQ:KTCC) is a contract manufacturer of all kinds of electronics and plastics, with facilities in Mexico, the US, China, and Vietnam.

Although the company seems to be trading at a low multiple to historical earnings, its business model is destined to fail under current conditions. The company requires cash to grow, and that cash is obtained through loans that charge more than the company’s return on assets.

For that reason, the recent increase in interest rates is going to be very hard on KTCC, unless the company is recapitalized through dilution or acquisition.

Note: Unless otherwise stated, all information has been obtained from KTCC’s filings with the SEC.

The business

Contract manufacturing of electronics: KTCC started as a contract manufacturer of keyboards in Washington. The company then changed strategies to any kind of contract manufacturing related to electronics and consumer appliances. The company has manufacturing facilities in the major manufacturing centers: Mexico, the US, China, and Vietnam.

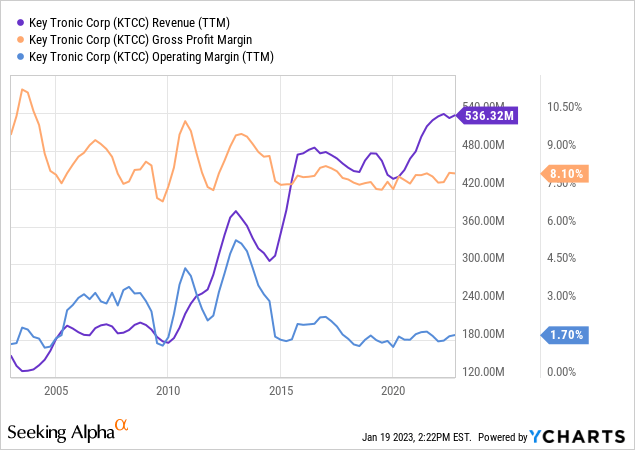

Incredible revenue growth: Since the company changed course in 2010, revenues exploded. Margins, although very low given that the company buys all components and only charges for assembling, have been relatively stable.

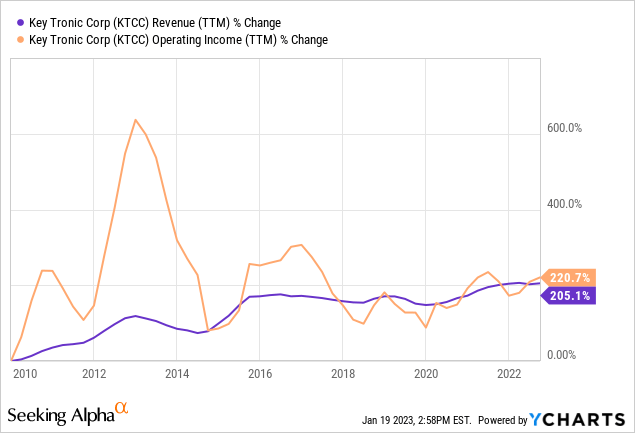

Operating leverage: Changes in revenue, although small given the company’s tremendous growth, have generally been accompanied by violent movements in operating income. This is understandable given the low margin at the operating level.

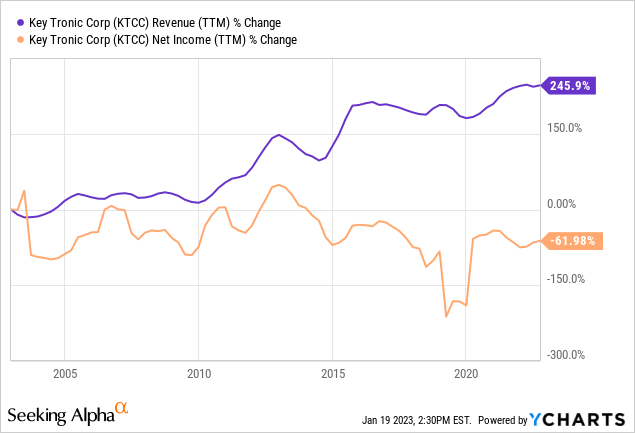

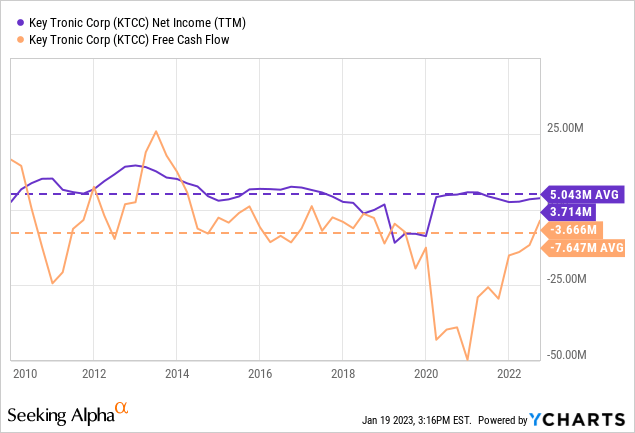

Revenue growth did not move down the income statement: Surprisingly, the tremendous increase in revenue has not translated into an increase but rather a decrease in net income.

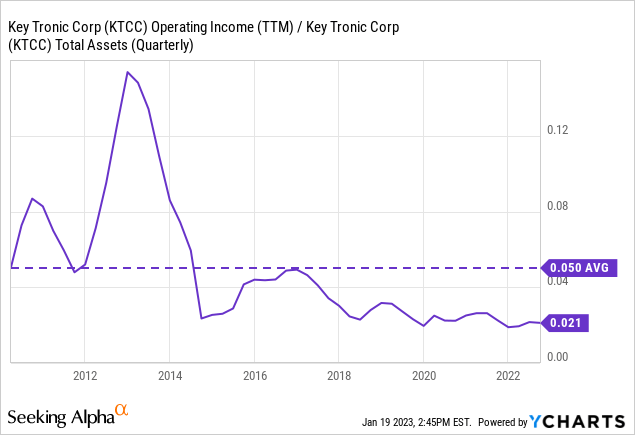

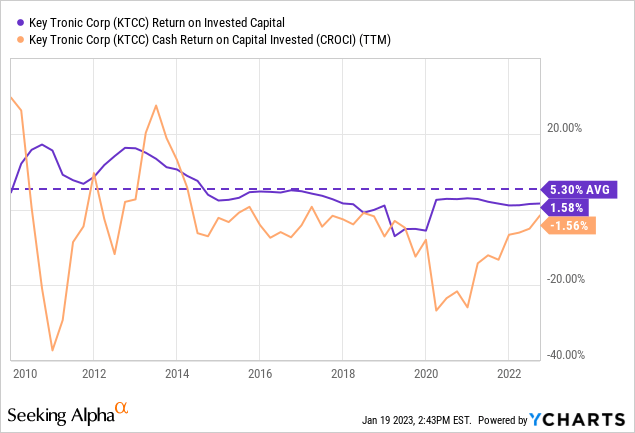

The company does not earn a good return on assets: Two measures of return on assets: operating income over total assets, and ROIC, both point to the low level of utilization of KTCC’s assets.

Unstoppable cash eating machine: The company’s net income also greatly overestimates the true capacity of the company to return to shareholders in any meaningful form. The company’s average FCF has been -$7.5 million per year, against an average net income of $5 million per year.

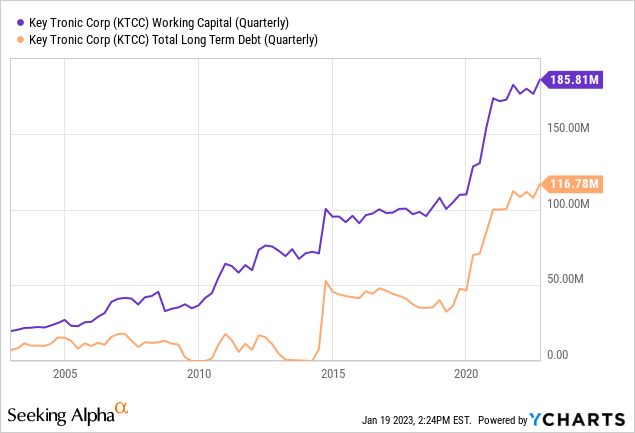

Working capital is guilty: The reason the company does not return on assets is that it has increased working capital at the same ratio as it grows revenue. Working capital in turn is financed with debt.

In my opinion, the low return obtained by KTCC is obtained through offering to its customers attractive financing, which requires increasing amounts of working capital, fueled by debt.

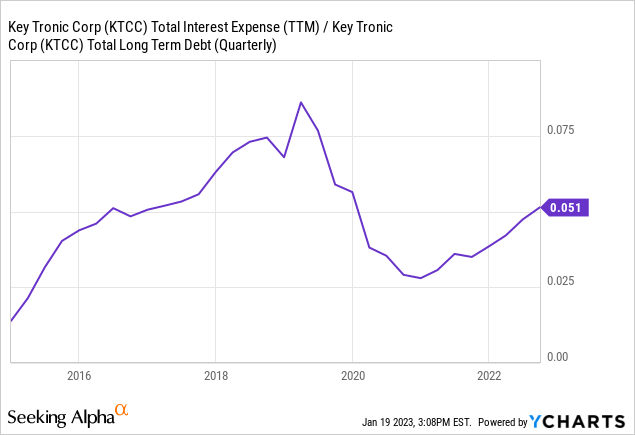

Debt is now more expensive than the return on assets: The company’s cost of debt has risen with interest rates and will continue to do so as the FED continues its tightening of credit conditions. With variable interest rates tied to the company’s credit facility, KTCC will earn less on its working capital than what it has to pay as interest.

Valuation

How to value a company that does not earn its required return: The problem with KTCC is not its prospects, or whether or not the company is cheap or expensive relative to earnings or FCF.

The problem is that the company cannot earn as much on its assets as it has to pay on its liabilities. If the company cannot cover its cost of debt, what is left for the equity?

The WC model signals a lack of competitive advantages: If the company had negotiation power with suppliers or customers, it could demand better financing from its chain. In that way, it would require less cash to finance its working capital and could reduce debts and even repay shareholders in some form. The fact that the company is financing its customers this much indicates that it cannot compete on other grounds.

Bull thesis and evidence of change

If the company simply cannot earn what it costs to sustain its assets, the perspectives ahead are not great. There are, however, some bullish pathways that I explore below.

Capitalization by dilution increases net income and EPS: The company could capitalize, diluting current shareholders. In this way, it would (for some time, while not growing revenues) hide the low earnings on assets, because it would generate higher net income. By using that capital to finance part of the working capital that is today financed by debt it would earn that interest portion to equity. The problem is that the company would be diluting current shareholders, and still earning a low return on equity.

Acquisition: KTCC could also be acquired by another contract manufacturer with more efficient management or higher competitive advantages, that can use the same assets more efficiently or even remove some of them. Maybe that acquirer would pay a premium on the stock.

Finally, my thesis could be proven wrong, or the company could prove that it has changed its business model, as evidenced by some of the following developments.

Improvement in cash flows: The most important requirement for a thesis change is for the company to show that it does not require to grow its working capital at the same speed as revenues and that it can generate positive cash flows from operations. More importantly, those cash flows should be commensurate with the company’s net income.

Increase in margins: KTCC could improve its operating margins and therefore generate more operating profits with the same level of working capital. This would improve its cash flows.

Increase in competitive strength: In general, if the company increases margins or can work with lower working capital requirements, that would signal an improvement of competitive strengths or a concentration in markets where it can compete more efficiently. Part of its lack of efficiency may come from the company’s participation in dozens of product lines.

Conclusions

Despite KTCC’s growth on the top line, the company is not generating more income for shareholders. When the non-accrual cash requirements of the company are added to the picture, KTCC’s business model flaws become more visible. The current context of high rate is only adding weight to the problem.

Like any company, KTCC could surprise me with a positive development, and I hope they do. I am also not recommending shorting the stock. However, I believe at these prices, the company is not a conservative long-term investment.

Editor’s Note: This article covers one or more microcap stocks. Please be aware of the risks associated with these stocks.

Be the first to comment