Bill Pugliano/Getty Images News

Kellogg Company (NYSE:K) is one of the major producers of cereals and other quick-and-easy foods around the world. Inflation is a growing concern, but the Inflation Reduction Act, which seeks to lower health care and energy prices, will help Americans keep their spending in check. Additionally, the recently passed law will somehow affect Kellogg’s operation, as the law includes a $4 billion fund to fight drought, which may reduce the volatility of the company’s input costs.

In North America, Kellogg has maintained its impressive performance with increases in both volume and price/mix, ending its Q2 2022 with strong top line growth and a positive outlook for FY 2022. K is currently trading nicely above its support and is fundamentally undervalued, making this stock a good buy.

Company Overview

Kellogg has been in the industry for over a decade and has played a significant role in people’s quick breakfast getaways. Their products are manufactured in 21 different countries and sold all over the world. K has divided its business into four distinct geographical regions, or “operating segments.” Their main bread and butter is their North America operation ($2,248 million), which represents 58% of their total revenue ($3,864 million) this quarter. Even though volume is going down because of bottlenecks and shortages, the company is still able to grow its sales thanks to its effective sales mix.

Volume remained pressured in quarter two by bottlenecks and shortages, but the decline was more moderate than expected. Price elasticity did not increase as much as we had anticipated. And our North America Cereal business recovered inventory and shipments faster than expected.

Source: Q2 2022 Earnings Call Transcript

A brief background: The company announced that it approved a plan to separate its North American cereal and Plant-based foods businesses on June 21, 2022. The company mentioned that they are aiming for this plan to materialize by the end of 2023.

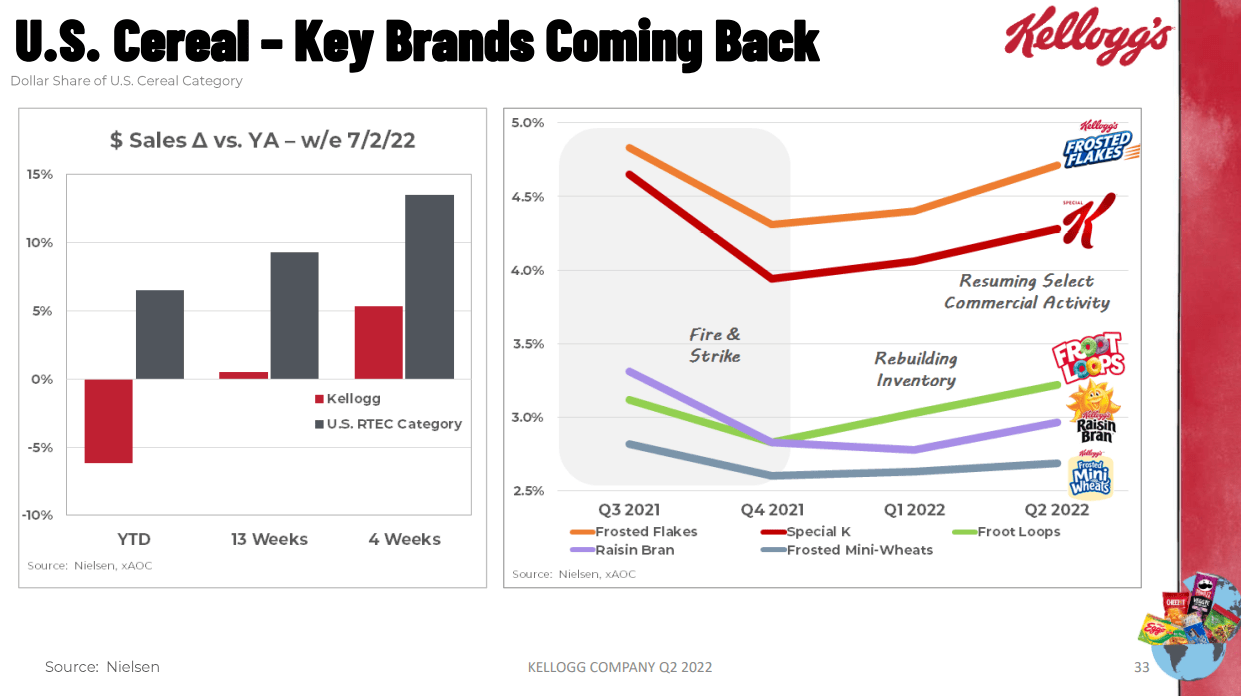

On a few points of improvement in their North America cereal business, the management stated that they didn’t recognize any fire or union strike impact this quarter, which affected their production for the past few quarters. In fact, they are effectively rebuilding their inventory level and have resumed commercial activity, as shown in the image below, putting the business in a better position to combat today’s inflationary pressures.

K: Improving Brands (Source: Q2 2022 Investors Presentation)

Why does Kellogg want to spin off its North America Cereal and Plant Base Business if it is improving?

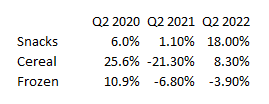

Looking at the image below, we can see that Kellogg’s North America’s Cereal and Frozen Business seems to fluctuate compared to its Snacks business.

K: North America Organic Growth Trend (Source: Company Filings. Prepared by InvestOhTrader)

The company’s Snacks business has shown consistent organic growth, with an impressive 18% growth in the most recent quarter, while its Cereal business shows an improving 8.3%, thanks to the effective price/mix implementation of the management. However, looking at the YTD figure provided by the management, the organic sales growth of its North America Cereal business incurred a -1.4% growth, its Frozen business a -3.0% growth, while its Snack business is the only one that has a positive growth of 11.4%.

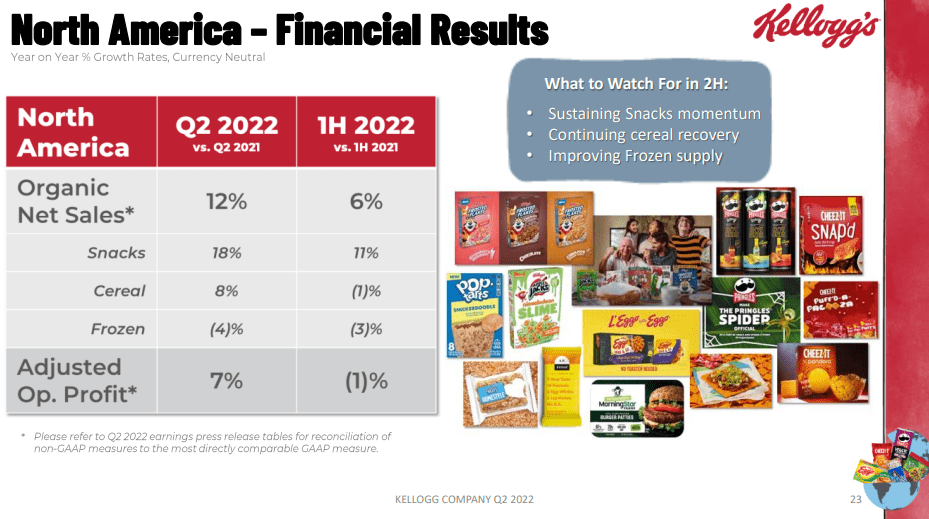

Kellogg: North America Financial Result (Source: Q2 2022 Investor Presentation)

Additionally, according to management, they incurred a negative operating profit on both of their cereal and frozen businesses, as shown in the image above. This puts pressure on the overall company’s operating profit.

Plant Co.

Looking at the image below, it appears that K’s peers in the plant-based food business are also struggling to turn a profit in this market, based on their recent financial results.

Plant Co.: Unprofitable Peers (Source: Data from SeekingAlpha. Prepared by InvestOhTrader. Amounts are in millions)

Steakholder Foods Ltd. (NASDAQ:STKH), Beyond Meat, Inc. (NASDAQ:BYND).

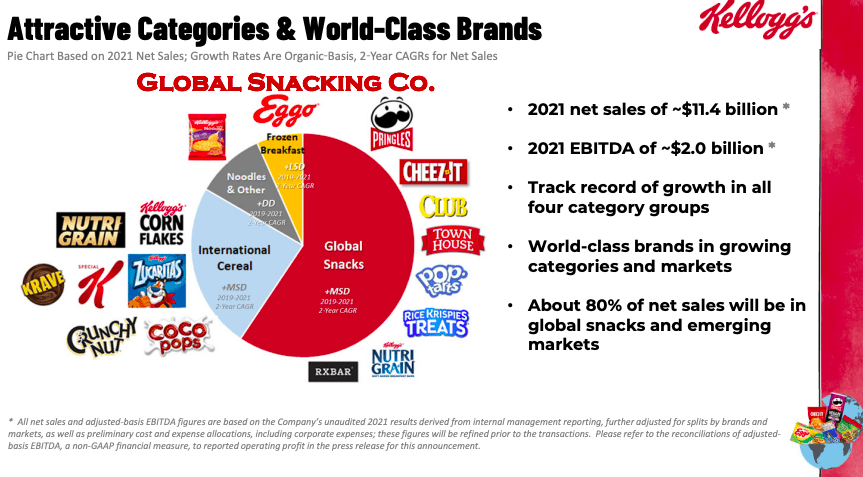

This leads me to the conclusion that their plan will be beneficial for the company, especially with their plan to keep 80% of its revenue-generating business as shown in the image below.

Kellogg: Portfolio Transformation (Source: Kellogg’s Portfolio Transition Presentation)

Lastly, this might promote profit margin expansion in the long run. However, this plan is still subject to final approval by the board. Hence, looking at the current inefficiency of the company makes it one of the profitability risks to monitor.

Kellogg Is a Cheaper Snack Company

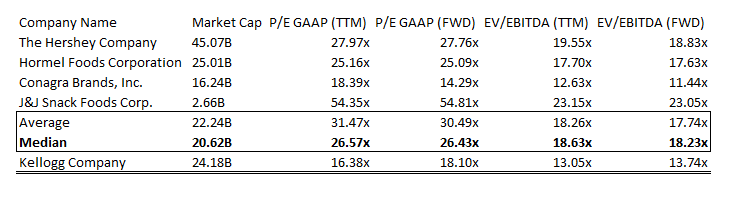

K: Relative Valuation (Source: Data from SeekingAlpha.com. Prepared by InvestOhTrader)

The Hershey Company (NYSE:HSY), Hormel Foods Corporation (NYSE:HRL), Conagra Brands, Inc. (NYSE:CAG), J&J Snack Foods Corp. (NASDAQ:JJSF)

Kellogg remains cheap compared to its peers, as shown in the image above. Looking at the company’s trailing P/E of 16.38x, we can see a premium compared to its forward P/E of 18.10x, but it seems that this figure considers a non-recurring separation cost as quoted below.

…the work continues towards the separation. As of now, we estimate that we’ll incur between $70 million to $80 million in upfront costs in 2022 related to readying for the transactions. Source: Q2 2022 Earnings Call Transcript

With the ongoing shortages and supply chain issues, I believe it is understandable why companies are having trouble managing their operating margins. Looking at the company’s multiples compared to its peers’ median, we can see a considerable discount. Using an implied 26.57x earnings, a forward EPS of $4.43, and a discount rate of 8%, we can arrive at a conservative fair price of ~$93, which can provide 32% upside potential as of this writing.

Trading Near Support

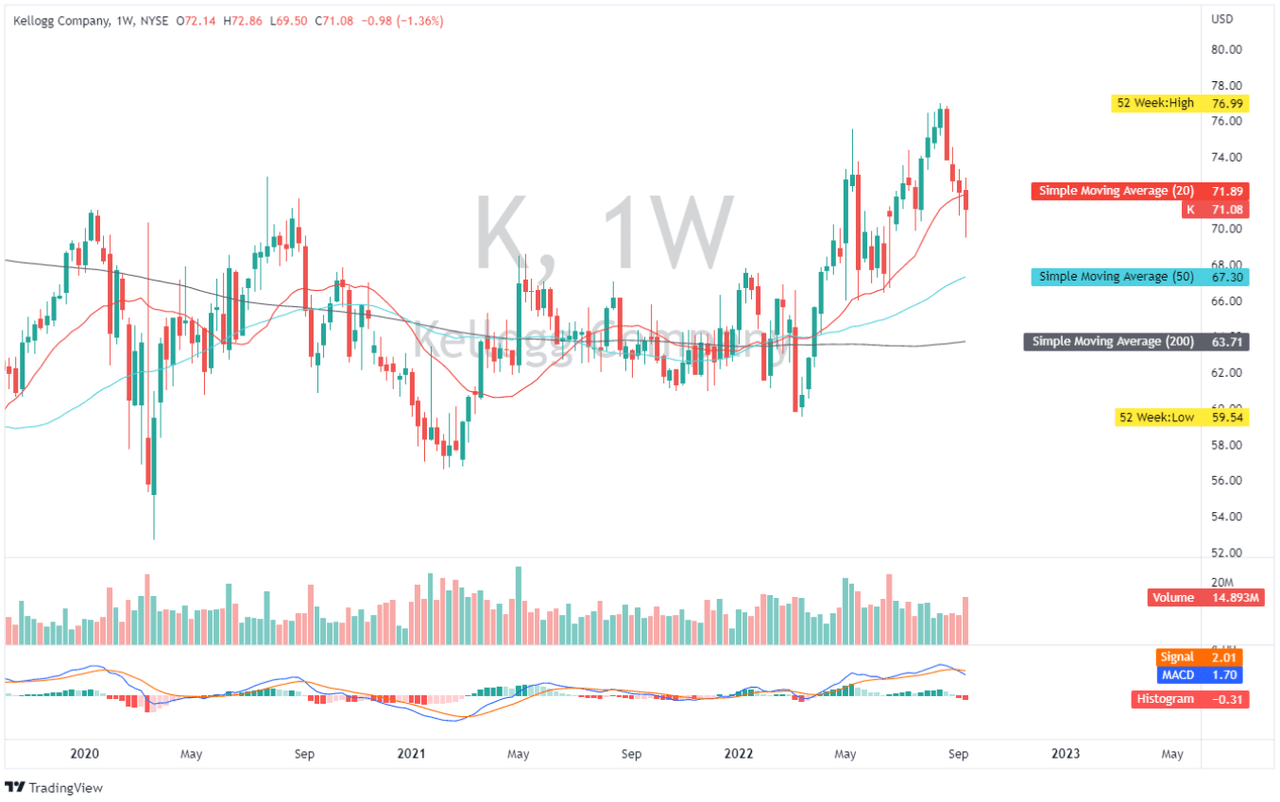

K: Weekly Chart (Source: TradingVIew.com)

Kellogg recently got denied by the market after breaching its multi-year resistance zone around $75 in August 2022. This opens a pullback opportunity, as the stock is currently trading near or below its 20-day simple moving average. Bullish momentum is currently challenged by the sentiment of its MACD indicator, where we can see a negative crossover as shown in the chart above. If initial support around $70 fails, I believe the next significant support will be around $67, providing another opportunity to get long this stock.

Risk

On top of its inefficiency in some of its business operations, as mentioned before, Kellogg remains under pressure due to today’s inflationary pressure. This showed in its slowing trailing gross margin of 30.96%, their lowest since FY2012. K’s profitability remains susceptible to another potential union strike risk, which may further slow its gross margin due to higher direct labor costs. Lastly, the company ended the quarter with a trailing declining operating margin of 13.56%, down from 14.26% recorded in FY2021, which makes this stock a bit risky as of this writing.

Conclusive Thoughts

Kellogg maintains a liquid balance sheet, with its declining long-term debt level amounting to $5,902 million, their lowest figure over the last five calendar years. This is reflected in the company’s improving debt-to-equity ratio of 1.87x than its 3.03x 5-year average. Additionally, the company has an improving trailing FCF margin of 8.92%, better than its 5-year average of 5.90%.

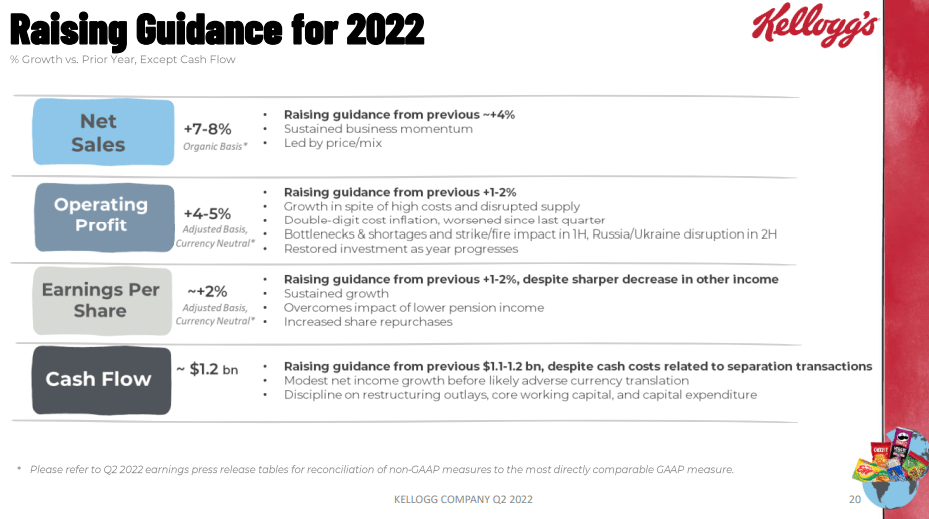

Kellogg: Rising Guidance for 2022 (Source: Q2 2022 Investor Presentation)

With its raised guidance for FY2022, I believe K remains investable, especially considering its growing cash flow from operations as shown in the image below. I believe K’s dividend yield of 3.32% remains safe and is getting more attractive in its potential drop. To sum it up, Kellogg remains investable and cheap compared to its peers, making it attractive at today’s correction.

Thank you for reading!

Be the first to comment