cemagraphics

It’s been a little over two months since I wrote my “avoid” piece about John Wiley & Sons, Inc. (NYSE:WLY), and in that time the shares have returned about 3.5% against a gain of 3.58% for the S&P 500. I’m apparently receiving a number of books for Christmas this year that I’ve been hoping for some time (most notably Toll’s “Twilight of the Gods”), and that put me in mind to write about this publishing leviathan. The company reported earnings since, so I thought I’d check in to see if it makes sense to buy or continue to avoid at the moment. I’ll make that determination by looking at the latest financial results, and by looking at the valuation. I’m also champing at the bit (horses don’t “chomp”) to write yet again about short put options. I’ve done well with these over the years, and I think it’s worth reminding investors of the risk-reducing, yield-enhancing potential of these instruments.

Welcome to the “thesis statement” portion of the article, where I offer up the highlights of my thinking. I do this so you won’t have to wade through all 1,780 words of my current screed, and it’s one of the many ways that I try to express my gratitude for your continued readership. You’re very welcome. Anyway, I think it would be prudent for investors to continue to avoid this name for a few reasons. This is not a growth company, as evidenced by the latest financial results. For that reason, we should treat it as a “cash cow” provider of consistent dividends. To continue the bovine simile for a bit, if this is like a cash cow, it doesn’t provide the purest milk in the world. The company has been on an acquisition spree typical of a growth company, and so far those haven’t moved the needle significantly. Additionally, a pile of debt is near maturity, which is inconvenient given what’s happening to rates. Lastly, I don’t like the “cash cow” qualities of this business at the moment because investors are receiving 100 basis points less than the risk-free rate while taking on significantly more risk. Thus, I think it would be prudent to continue to avoid the name.

Finally, this will be one of the, if not the final articles I will write this year. In spite of the fact that I’m awful at parties, I’ve been invited to many of them this year, so my time is short. I guess people have a “socially inept” quota system that they need to fill? Anyway, since this may be the last of 2022, I’d like to thank all of you for putting up with me for the past year, and to wish you and your loved ones the very best of the season, however, you celebrate it, and all the best of 2023 and beyond.

Financial Snapshot

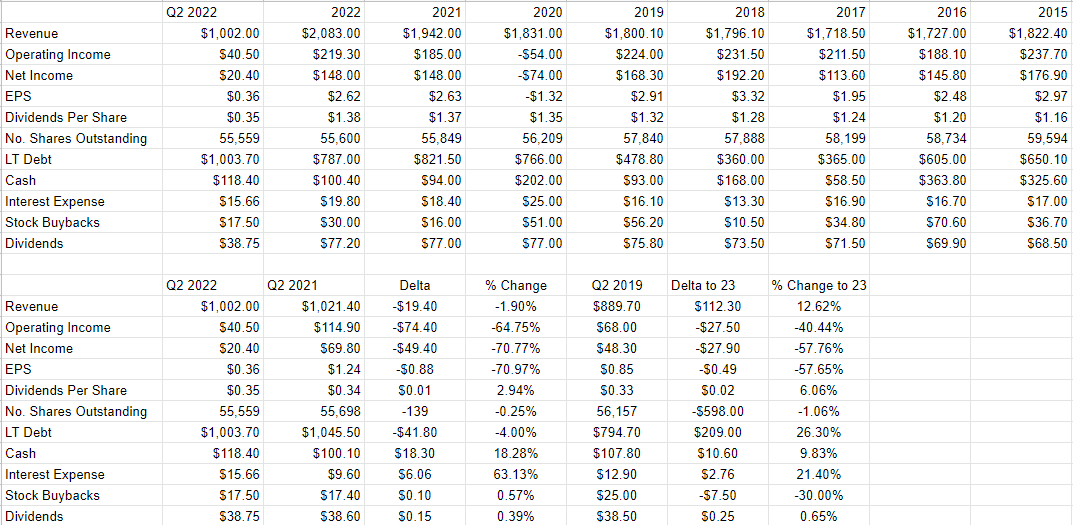

The latest financial results have “pulled it out of the fire” somewhat for John Wiley. The company went into the financial quarter looking “generally bad”, but revenue and net income have turned around somewhat. That written, the company has not returned to results from prior times, which is troubling. Compared to the same time last year, revenue and net income were lower today by 2% and 71% respectively. In case you’re worried that 2021 was a banner year, making any comparisons to it troublesome, fret no longer. When compared to 2019, the same pattern emerges. Specifically, net income during the first two quarters of 2022 was 58% lower than it was in 2019. This is not a “growth” company and should not be valued as such.

Although the capital structure has improved relative to 2021, current long-term debt is about $209 million, or 26% higher than it was in 2019. This is troublesome, in my view, because it has a direct impact on the sustainability of the dividend.

In my previous missive on this name, I expressed the view that this company can have a sustainable dividend, or it can have acquisitions, but it can’t have both. Feel free to peruse that screed for the specific reasons for this view. If the notion of being exposed to yet another Doyle article is just too much to take, I don’t blame you, and for that reason, I’ll offer the highlights. Over the recent past, the company has spent an average of $200 million on acquisitions. To put that in context, they have about $118 million in cash at the moment, and about 19% of net income is spent on interest payments. Additionally, there’s an incredible amount of debt coming due over the next year or two. Given where interest rates are, this may not be excellent timing. That’s the “gist” of my thoughts about John Wiley’s dividend. If you want a more fulsome review of the specifics, I’m afraid there’s nothing for it but to read my earlier work. My very insincere apologies in advance for any nausea this induces. The point is that I’d be willing to buy the stock only if the market price is reasonably cheap. I want to be compensated for the cash crunch risk here.

John Wiley Financials (John Wiley investor relations)

The Stock

If you subject yourself to my stuff on a regular basis, you know that I consider the stock and the business to be distinct from each other. The business licenses intellectual property, bundles it up, and sells the results. The stock is a speculative instrument that gets buffeted by a host of factors, some of which have nothing to do with those activities. One of the things that affects the performance of a given stock, for example, is the crowd’s ever-changing views about the desirability of “stocks” as an asset class. There’s no way to prove this definitively, as it’s an obvious counterfactual, but it’s possible to make the case that John Wiley has matched the market since I last wrote about it, because it was carried along for the ride as investors decided once again that they like stock.

So, this is why I consider the stock as a thing distinct from the business. The former is often a poor proxy for what’s going on at the company, and I think it’s possible to profitably exploit this disconnect. In my view, the only way to successfully trade stocks is to spot the discrepancies between what the crowd is assuming about a given company and subsequent results. What I want to see in this regard is a stock that the crowd is somewhat pessimistic about that goes on to exceed expectations. When the crowd is pessimistic, the shares are cheap, which is why I try to buy only cheap stocks. Now, I consider this to be a fine investment at the right price, and I want to work out whether we’re near that price or not today.

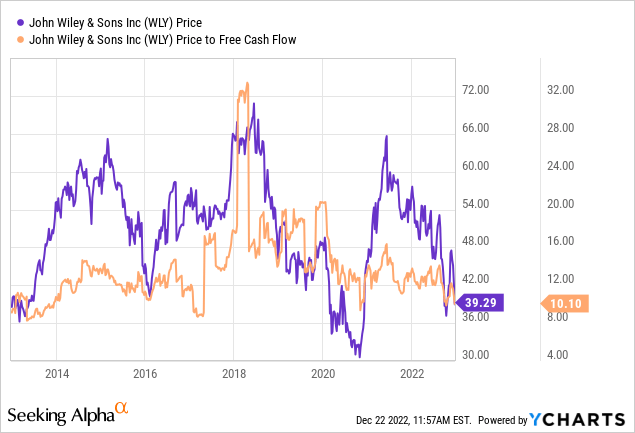

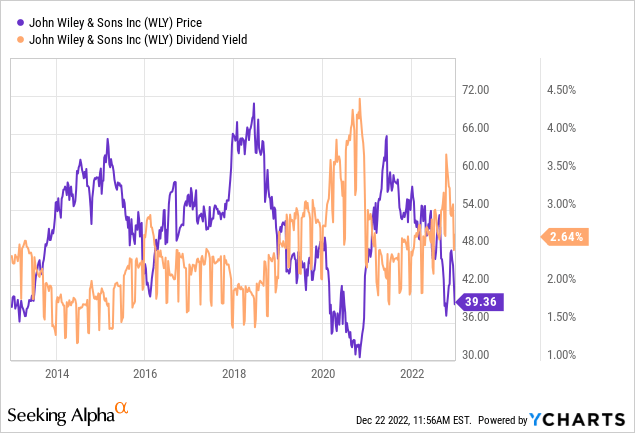

In my previous piece, in case you’ve forgotten, I remained cautious about this stock because the shares were trading at a price to free cash flow of about 10.3, and the dividend yield was only about 3.55%. Fast-forward to the present, and here’s the current lay of the land. The shares are actually about the same price today on a price to free cash flow basis, though the dividend yield is about 90 basis points lower than it was previously, per the following. I think it’s also relevant that at the moment, the yield on the 10-year Treasury Note is sitting around 3.66%. Thus, common stock investors in this, uh, “growth-light” business are taking on much more risk than they would if they simply lent their capital to Uncle Sam, and receiving about 100 basis points less cash for their trouble.

My regulars know that I think ratios can be instructive, but I also want to try to work out what the market is “thinking” about a given investment. If you read my stuff regularly, you know that the way I do this is by turning to the work of Professor Stephen Penman and his book “Accounting for Value.” In this book, Penman walks investors through how they can apply some pretty basic math to a standard finance formula in order to work out what the market is “thinking” about a given company’s future growth. This involves isolating the “g” (growth) variable in this formula. In case you find Penman’s writing a bit opaque, you might want to try “Expectations Investing” by Mauboussin and Rappaport. These two have also introduced the idea of using the stock price itself as a source of information, and we can infer what the market is currently “expecting” about the future. Applying this approach to John Wiley at the moment suggests the market is assuming that this company will grow earnings at a rate of ~1.2% in perpetuity. Although I consider that to be a nicely pessimistic forecast, I can’t get past the fact that the dividend yield is lower than the risk-free rate. If this were a growth dynamo, that wouldn’t be a problem. In this case, it very much is a problem in my view. Given the above, I’m going to continue to avoid this name.

Options Update

My regular readers know that I love selling deep out-of-the-money put options if I can generate a decent enough premium on them. I like this strategy because it creates a “win-win” trade. Either the shares remain above the strike price, and the options expire worthless, or I’m obliged to buy a company I like at a price I love. Both are very positive outcomes in my view. For that reason, I pound the virtual table, again, that if you’re not yet familiar with the yield-enhancing, risk-reducing potential of these instruments, I recommend you make yourself so in 2023. Having “learn about put options” is a much more fun, potentially profitable New Year’s resolution than some boring old “lose weight” nonsense, in my view.

Anyway, in terms of specifics, way back in January of this year, when these shares were trading just over $56, I sold June puts with a strike of $40. This sale of deep out-of-the-money puts has earned me about the same amount of cash that common shareholders have earned but at substantially lower risk.

While I normally like to try to repeat success, I can’t in this case as the premia on offer aren’t great in my view. That written, I think the shares will drop in price from current levels, and when that happens, I’ll likely sell puts again.

Be the first to comment