Antonio Masiello/Getty Images News

The iShares MSCI Italy ETF (NYSEARCA:EWI) is a ~$200m sized product that offers investors exposure to large and mid-cap Italian stocks. In this article, we’ll touch upon some notable factors for prospective investors to be mindful of.

The macro and political landscape isn’t great

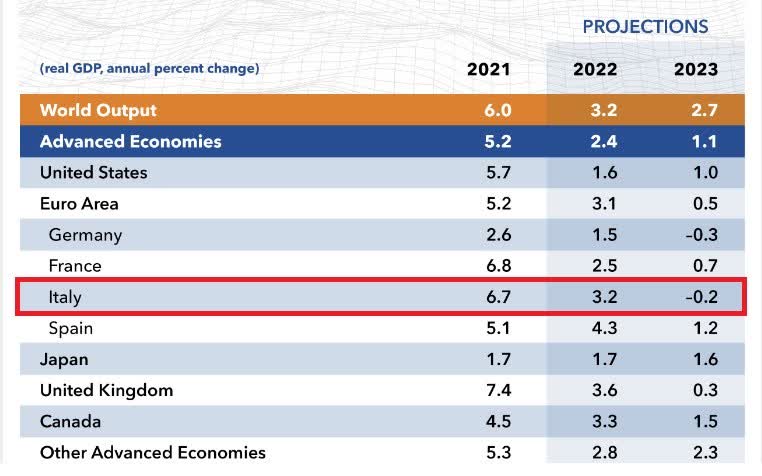

Italy’s growth outlook is one of the weakest in Europe (Real GDP is poised to decline by 0.2% in 2023), and amongst the major advanced economies, only Germany will likely see a more pronounced fall (-0.3%).

IMF

Meanwhile, over the last two months, inflation has been hovering at its highest point (11.8%) since the creation of the Euro back in 1999. Given the relatively low base effect in both December 2021 and Jan 2022, it is difficult to envisage a drastic YoY drop down from these steep levels; if anything, inflation may continue to trend well past the 12% levels. The economy minister of Italy has recently stated that he doesn’t believe energy prices will decline even by March. The heightened inflation levels are quite concerning as Italy has made a concerted effort to diversify its energy sourcing away from Russia to North Africa. Russia which used to previously contribute 40% of Italy’s gas imports now contributes less than 10%.

To help the economy tide over this environment of stagflation, it looks like the government will have to step in with even more fiscal support. Latest reports suggest that the Italian government will now plug in EUR21bn in tax breaks and bonuses to abet firms and households that have been ravaged by the energy crisis. This will naturally put pressure on the 2023 budget deficit which was previously estimated (in September) to come in at 3.4% of GDP; now it will likely be 90bps higher!

This isn’t the only issue that concerns me. The administration under Giorgia Meloni will also look to cap an increase in the retirement age which will only put further pressure on the pension bill which is already one of the highest in Europe. Since these pensions are index-linked, you can imagine what elevated inflation levels could do for the total bill. In the middle of last year, the treasury had suggested that the pension bill as a function of GDP would likely increase by 50bps in 2023 to hit 16.2% in 2023; I suspect this will need to be re-adjusted upwards by an even greater margin.

A profligate fiscal policy could undermine some of the reforms that were put in place by the erstwhile Draghi administration to procure EU recovery funds. If the Meloni administration undermines some of her predecessor’s work, it remains to be seen if the EU will be as magnanimous as before.

OECD

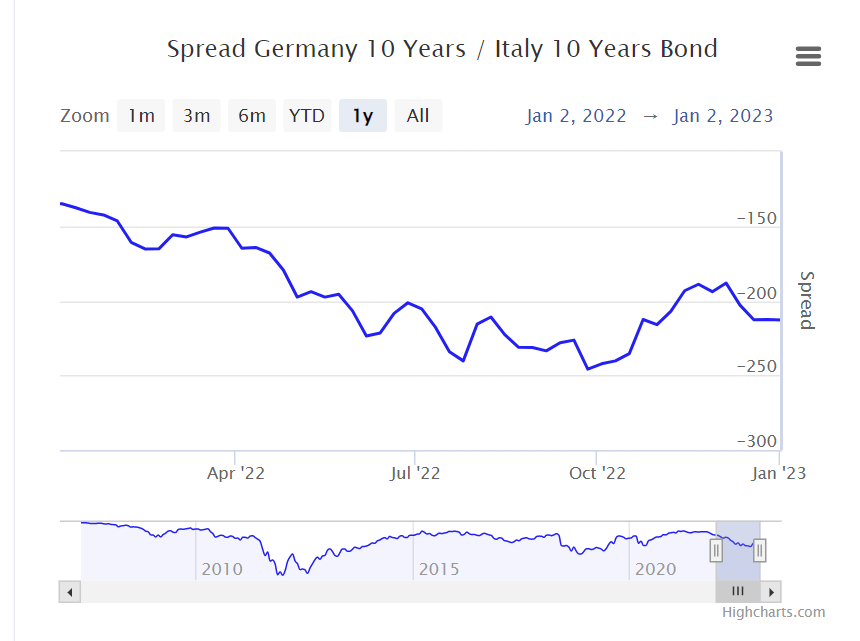

Besides Italy’s public debt levels are already at a rather precarious state (~150% of GDP), and the ECB’s aggressive stance with interest rates only compounds the debt servicing issue.

Highcharts

The wide spread between German and Italian 10-year bonds has pulled back slightly in recent months, but going forward it is still expected to be quite pronounced.

OECD

There are also question marks over the leadership and support that Meloni will likely receive. For instance, it is believed that the current economy minister – Giancarlo Giorgetti was not the preferred pick, and he has gone on record stating that he doubts his capacity to fulfill the role. It’s worth noting that he comes from Matteo Salvini’s league party (the coalition ally of Meloni’s Brothers of Italy party), someone who’s had to reluctantly accept that he wouldn’t be the PM. With a somewhat shaky coalition, it remains to be seen if Meloni will have the requisite support to push through her economic agenda. I don’t believe that investors should cast aside the prospect of political instability and what this could do for the volatility quotient of EWI.

Closing Thoughts

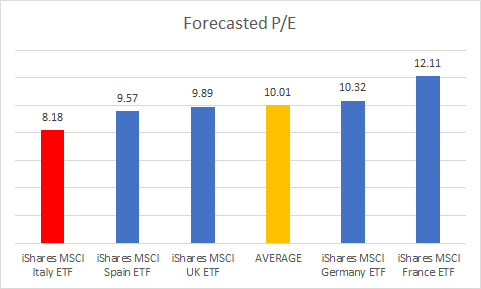

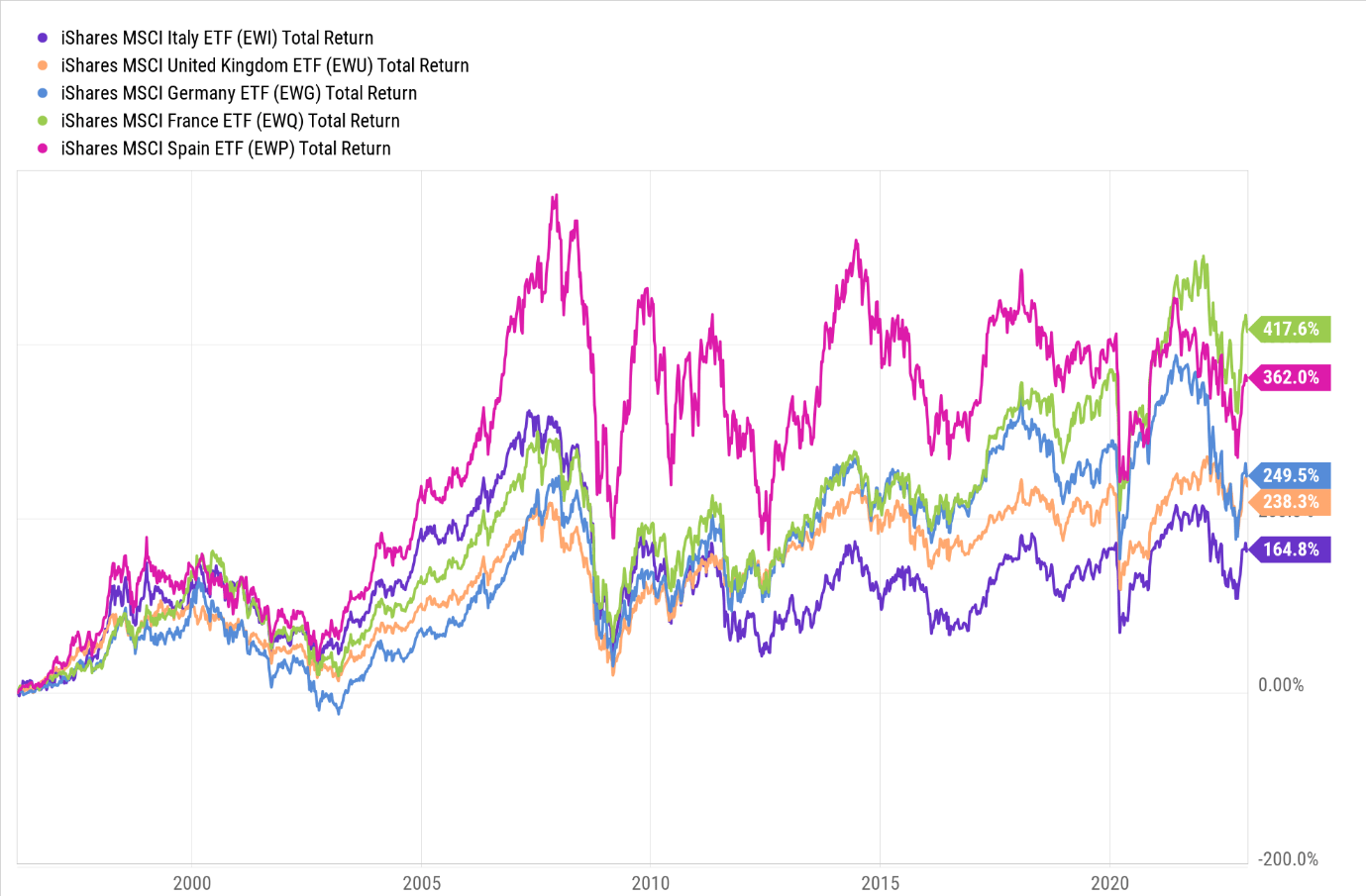

I wanted to conclude by focusing on how EWI looks relative to other options in this space. As far as forward valuations go, if you compare EWI relative to the ETF options of some of Europe’s largest economies, we can see that it is the most cheaply priced offering, trading at an ~18% discount relative to the peer set average (on a forward P/E basis, as per Morningstar data).

Morningstar

Before you get swayed by the dirt-cheap valuations, do consider what you’re getting into. For the uninitiated, the iShares MSCI Italy ETF has been the worst-performing ETF since its inception on the 12th of March 1996 (all these ETFs were listed on the same date), underperforming its peers by anything from 1.4-2.5x!

YCharts

Not only are you getting on board with a product with an underwhelming return track record, but you’re also looking at a product that hasn’t done a particularly good job in balancing its risk and delivering excess returns.

YCharts

The table above shows that EWI has a heightened risk profile, as exemplified by the highest standard deviation figure. This high SD figure means it needs to generate a lot more excess returns (over the risk-free rate) than its peers to come up with an acceptable Sharpe ratio, which it fails to do. We can also see that EWI doesn’t cope very well when faced with harmful volatility as it has the worst Sortino ratio amongst its peers. Going forward, I’m not suggesting that we will see the exact same dynamics pan out, but considering the consistency of these stats since its inception (over 26 years back), it’s difficult to envisage a drastic turnaround in the numbers.

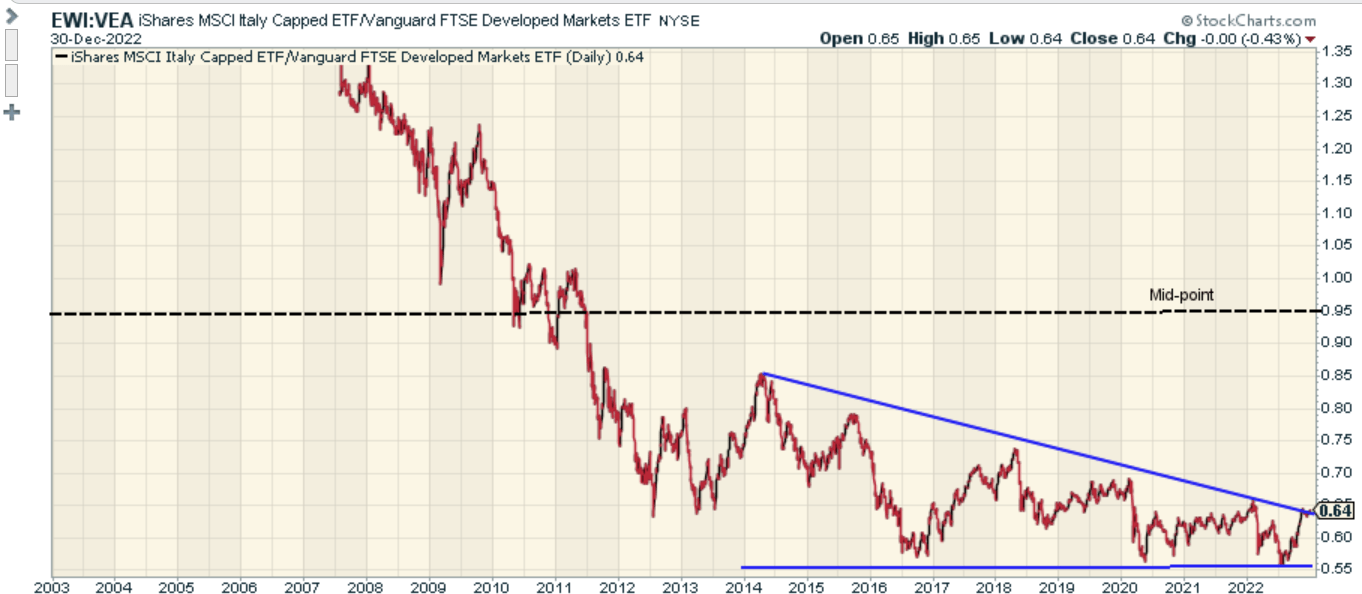

Then if I switch to the charts, and see how EWI is positioned relative to a diversified basket of developed market stocks (as represented by the Vanguard FTSE Developed Markets ETF), it looks like Italian equities look quite oversold as the current ratio is around 33% lower than the mid-point of its long-term range.

StockCharts

But then again, I’m not necessarily convinced that this is the best time to load up on EWI as the ratio has just hit its downward-sloping triangle resistance that has been in play since mid-2014.

Investing

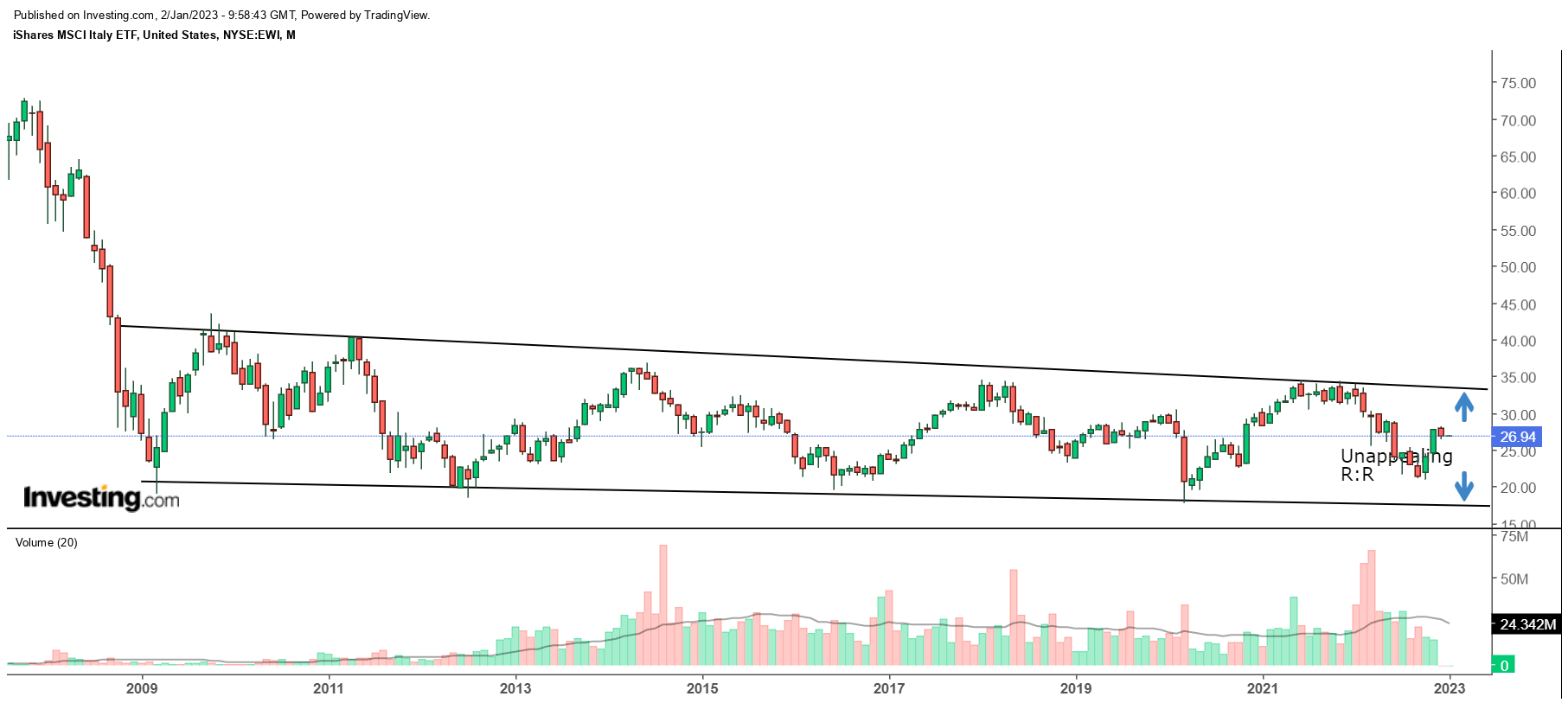

Finally, also note that since the GFC, EWI has been trading in the shape of a faint descending channel, and currently, if one were to go long, the risk-reward does not look great (less than 1, at 0.66x), as the stock is trading a lot closer to the upper boundary of this channel.

Be the first to comment