RiverNorthPhotography/iStock Unreleased via Getty Images

Bank of America Corporation (NYSE:BAC) has a decidedly checkered past. The acquisitions of Countrywide Financial and Merrill Lynch opened a floodgate for lawsuits.

A $2.4 billion suit related to Merrill Lynch was settled out of court in 2012. That was followed a year later by a federal lawsuit that resulted in BAC paying $6.3 billion to Fannie Mae and Freddie Mac.

In 2014, the bank and the U.S. Department of Justice agreed to a $16.65 billion payment related to the sale of risky, mortgage-backed securities. That marked the largest settlement in US history between a single company and the federal government. I’ll add that this is far from an exhaustive list of the troubles BAC investors endured

However, BAC emerged from this gauntlet as a more diversified and powerful financial institution. Largely due to the acquisition of Merrill Lynch, the firm is one of the largest online retail brokerages and a top wealth advisor.

Bank of America also ranks as the second largest U.S. money center bank by assets. The company is among the top two banks in terms of small business lending, retail mortgages, and home equity lines of credit. In an industry where size matters, Bank of America has one of the largest retail branch networks and ranks among the top four U.S. credit card issuers.

The bank’s robust increase in deposits of late represents a distinct positive; however, the company’s investment banking business has been hamstrung in 2022. More importantly, the Fed’s move to increase interest rates is a two-edged sword: higher rates drive bank’s profits, but an inverted yield curve often presages recessions.

Bank of America’s Metamorphosis

The enormous settlements listed above, combined with acquisition and integration costs, have weighed on Bank of America’s operating efficiency. However, the legal troubles are largely behind the firm, and in recent years, BAC has consolidated over 30% of its branches while reducing its employee headcount by a similar figure.

The bank’s scale provides a distinct competitive advantage. For example, credit card issuers have high fixed costs for their platforms. Consequently, there is a critical mass that is reached wherein additional consumers provide fatter margins. Additionally, by providing a full range of banking, asset management, investing, and other financial products and services, BAC has become a sort of one-stop-shop for consumers of all stripes.

This has resulted in a robust increase in the bank’s low-cost retail deposits. Over the last five quarters, BAC has increased deposits by roughly $600 billion. As of the end of FY 2021, it reported more than $2 trillion in deposits as opposed to roughly $945 billion in total loans. Since more than half of the bank’s deposits are from its consumer branch, this positions the company to take advantage of the upcoming rate hikes.

Rate Hikes: A Panacea Or Poison Pill?

Banks borrow money in the short term and gain revenue through long term loans.

Net Interest Margin (NIM) is a widely followed metric that provides insight into a bank’s profitability. NIM compares the net interest income (NII) a financial firm generates from credit products like loans and mortgages with the interest it pays holders of checking and savings accounts and certificates of deposit. Expressed as a percentage (the higher the better), it is akin to gross profit margin.

Conventional wisdom tells us that when the Federal Reserve raises interest rates, the NIM and NII expands, thereby increasing bank profits. Herein lies a strong tailwind that could provide robust revenue growth for Bank of America.

In this environment, Bank of America arguably has the advantage over many rivals. Due to its large number of commercial clients, BAC has a portfolio that includes a relatively high percentage of floating-rate loans. Those rates move higher along with the federal funds rate. Furthermore, with at least a trillion more in mostly low-cost retail deposits than it holds in outstanding loans, the company has a great deal of cash at its disposal.

Cyclically, BAC previously front-loaded costs to increase primary checking accounts and grow deposits at levels that far outpaced the industry, and it is now well positioned to better leverage these efforts. Indeed, the higher rate backdrop helps BAC more than peers given $2T of mostly sticky, low-cost deposits (half consumer) that should help fund higher yielding securities and loans, helping NIM [net interest margin] and NII.

In its most recent 10K, BAC projected the federal funds rate will land at 1% at the end of 2022. In the fourth quarter, BofA noted that a 100-basis-point shift in the interest rate yield curve should increase NII by $6.5 billion. Consequently, a 1% increase in interest rates by the Fed works out to roughly an $0.80 increase in BofA’s full-year EPS.

However, since the release of that annual report, investors now expect seven rate hikes in total this year, putting the rate at around 1.75% by 2023, thereby driving profits and revenues higher.

About two weeks ago, Betsy Graseck, an analyst for Morgan Stanley, upgraded BAC due to the Fed’s moves, citing a higher quality loan portfolio and above average sensitivity to higher interest rates.

We expect 6 rate hikes in 2022 and 4 in 2023 will drive a Net Interest Income CAGR of 16% over the next 2 years.

Unfortunately, there is a caveat attached to this scenario.

The yield curve plots the yield of Treasury securities and is seen by investors as a means to forecast U.S. growth and monetary policy.

The curve normally slopes upward as investors require compensation for the risk associated with increasing inflation and the toll it takes from owning longer-duration bonds. This generally results in 10-year notes yielding more than 2-year notes. However, on occasion the yield curve can invert, as it did earlier this month, and an inverted yield curve predicts recessions.

The following excerpt from a recent Barron’s article provides insights into the meaning and predictive ability of an inverted yield curve;

A bond-market anomaly called a yield curve inversion has shown up recently. Two-year Treasuries yielded more than 10-year notes at the end of trading Monday, closing at 2.42% and 2.4%, respectively. That’s unusual because investors usually demand more compensation for longer-dated Treasuries, to reflect the risk of tighter Fed policy and higher inflation.

The concern around this signal is understandable. In a recent study of yield curve inversions, BCA Research found that the gap between 2- and 10-year yields has inverted before seven of the past eight recessions, with no false signals. The gap between 3-month and 10-year yields has a better record, calling all 8 recessions without a false signal.

However, an inverted yield curve does not mean a recession is imminent. On average, it takes seventeen months after an inverted yield curve appears before a recession develops.

Moreover, there are analysts that believe the recent inversions are flashing a false positive. They believe the yield curve is artificially inverted by the prodigious sums of cash the Fed pumped into the economy. From this perspective, the long side of the curve has been driven down, resulting in an aberration.

This is in no way traditional Fed tightening—and there are no models that can even remotely give us the answers.

Knowledgeable investors are aware of the threat fintech presents to traditional financial institutions. There are few that would consider BofA a pioneer in that field. However, the company is adapting to the new environment well.

The bank ended FY21 with 41 million active digital customers. Three years ago, BAC had 5 million active digital users. In the last quarter, 49% of all sales were completed digitally. This marks a 31% increase from three years ago.

Aside from demonstrating that BofA is adapting to the times, digital transactions are less costly than in-person or phone based interactions.

A Second Potential Headwind

Investment banking revenue has slowed dramatically during the first few months of 2022. A boom in IPOs and SPACs resulted in a surge in investment banking fees in 2021. However, Financial Times recently reported that the combined equity market revenues of Goldman Sachs (GS), JPMorgan Chase (JPM), Bank of America (BAC), Morgan Stanley (MS), and Citigroup (C) in 2020 total $645 million.

Contrast that with $5.3 billion generated by those institutions in the same period in 2021. The fact that there wasn’t a single IPO in the US from February 17th through March 14th attests to the severity of the downturn.

Add to that predictions that deposits in major US banks will decline by 6% in 2022.

What To Expect From Q1 Earnings

Bank of America is scheduled to report its Q1 2022 earnings on March 18, 2022. Consumer and business banking is expected to help drive Q1 earnings while investment banking will lag badly relative to last year.

Results will likely reflect increased lending activity, including an uptick in commercial real estate, auto loan credit cards, and revolving consumer credit.

The consensus EPS estimate of the 20 analysts covering BAC, is $0.75. The high end of those forecasts is $0.83 while the lowest estimate is $0.69. This compares to $0.82 reported in Q4.

The consensus figure for revenue is $23.04 billion, a significant increase from the $22.063 billion reported last quarter.

Investors should anticipate a single-digit drop in deposits; however, this will likely have no effect on BAC. There should also be an uptick in NIM/NII, leading to increased revenue overall. On the downside, the investment banking revenue will drop markedly.

What Is Bank of America’s Forecast?

BAC currently trades for $39.59 a share. The average 12-month price target of the 19 analysts rating the company is $50.64. The average price target of the five analysts that rated the company following the last quarterly results is $50.10.

Bank of America’s forward P/E is 12.14x, roughly a half point below its average P/E over the last five years. The 5-year PEG is 1.69x. This compares to its historical average PEG of 1.50x.

Is BAC Stock A Buy, Sell, or Hold?

There is no doubt that rising interest rates are coming soon, and the Fed’s actions will push up NIM/NII. I also believe that if the economy remains on track, investment banking revenue will recover.

The conundrum I face is two fold: bank stocks moved sharply upward in 2021, likely due in part to investors’ anticipation of rate hikes. Furthermore, while I am not predicting that a recession is imminent, I’ll admit that even without an inverted yield curve, I would be somewhat wary of the economy.

I also view the current valuation metrics for the shares as representing a fairly valued stock, at best.

It is difficult for me to endorse an investment when BofA chief investment strategist Michael Hartnett views the US economy as standing on a precipice. According to a recent Fox article, Hartnett used, “Inflation shock’ worsening, ‘rates shock’ just beginning, ‘recession shock’ coming,” to describe the state of the current economy.

Now add this recent assessment by former Chase chief economist Anthony Chan when questioned regarding the likelihood of a recession in 2022:

Given everything that we know today, the probability is over 40%.

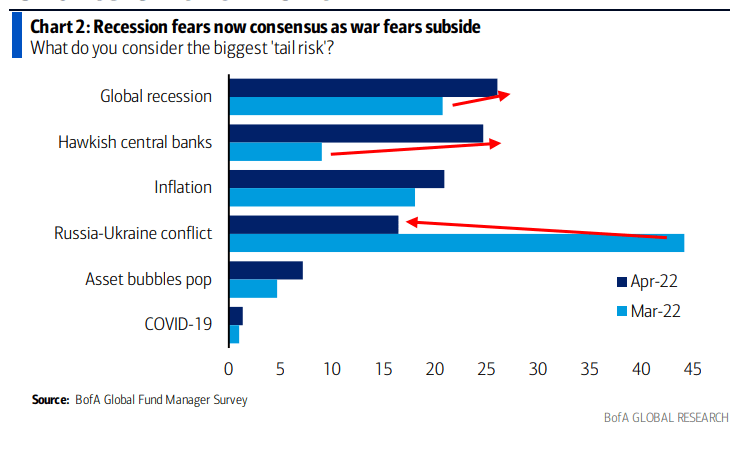

The following chart provides results from a survey of fund managers regarding their view of the greatest threat to the market

Seeking Alpha

Due to recession risk, and despite the potential for strong upside related to increasing interest rates, I view an investment in BofA as problematic. I would rather miss an opportunity for gains than risk locking in losses.

Please note that foreign exchange and other leveraged trading involves significant risk of loss. It is not suitable for all investors and you should make sure you understand the risks involved, seeking independent advice if necessary.

Be the first to comment