RiverNorthPhotography

Thesis

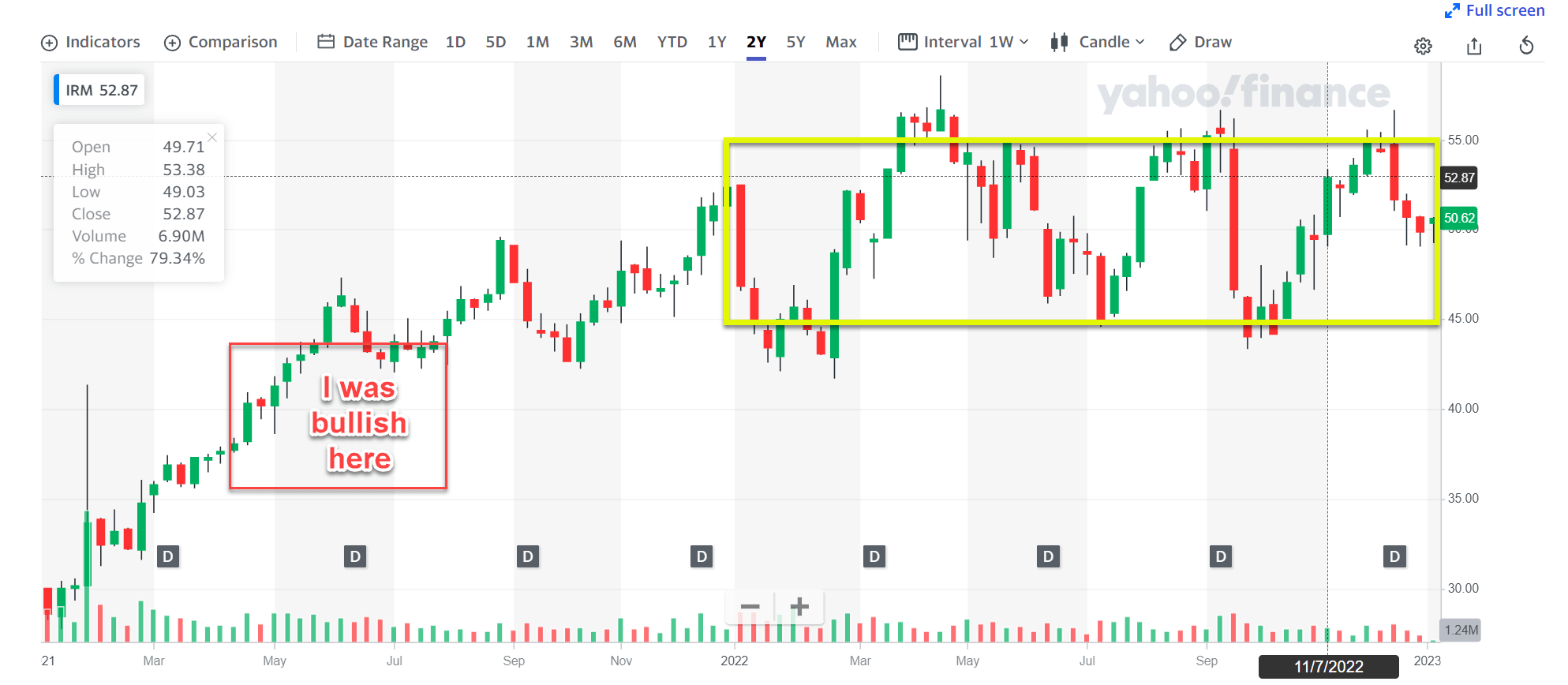

I wrote my first article on Iron Mountain (NYSE:IRM) more than a year ago (back in July 2021). At that time, I was quite bullish on the stock with its price hovered around a $40 per share and rated it as a “buy”. Fast forward to now, the stock price currently sits around $50, about 20% above the price when I first wrote about it. The stock has been trading in a consolidation window between $45 and $55 as you can see from the following chart (highlighted in the yellow box) for the past year or so.

And this leads me to the main thesis of this update article, which is twofold. First, I anticipate the stock price to be oscillating in this consolidation window in the near term. As to be detailed in the remainder of this article, I see multiple headwinds to keep both its earnings growth and also valuation multiple stagnated. And secondly, I’m seeing a mediocre return potential for any entry price between $45 and $55. And thus, I am updating my rating on the stock from “Buy” to “hold”.

Source: Yahoo! finance data

IRM’s headwinds ahead

I am seeing several strong headwinds facing the company’s business in the near term. The company’s core business is still paper document storage, which faces competition from cheaper digital storage. In the meantime, the business is also facing inflationary pressures and higher electricity costs for its relatively new data center business (just like the rest of economy). And finally, as a byproduct of inflation, higher interest rates will likely keep weighing on its bottom line. To fight inflation, the Fed has raised interest rates by almost 400 basis points in 2022 and more hikes are anticipated in 2023. About 21% of IRM’s $10 billion of debt has floating rates and will adjust to higher interest payments. Based on these numbers, a 200-basis point increase in its borrowing rate would translate into $40 million of higher payments, and further translating into almost 10% of its annual earnings.

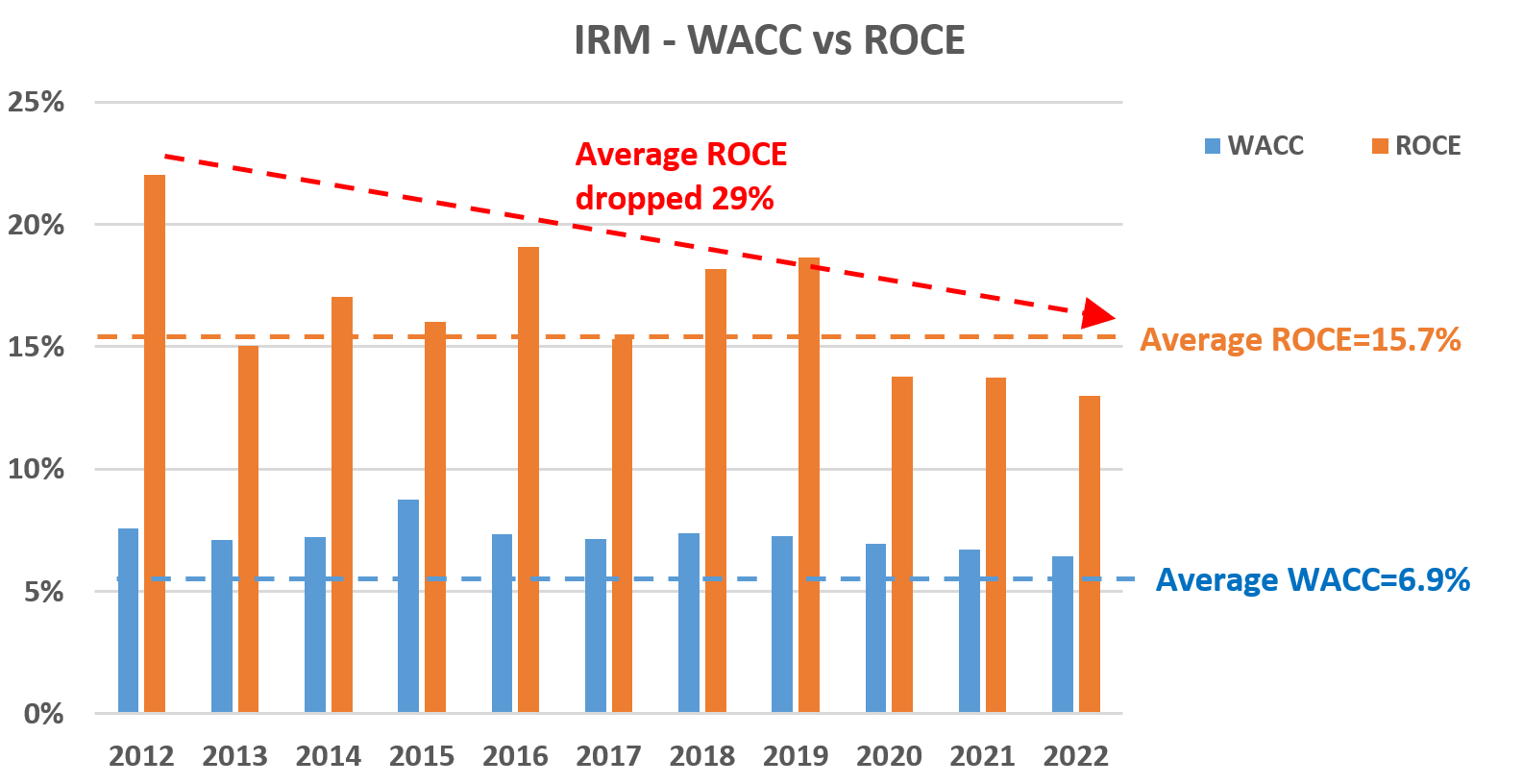

And these profit headwinds are reflected in its return on capital employed (“ROCE”) as shown in the chart below. As detailed in my earlier article:

To analyze the ROCE of businesses like IRM, I considered the following items in the calculation of ROCE: working capital (including payables and receivables) and the Total Real Estate Assets. I also analyzed its weighted average cost of capital (“WACC”). The WACC is the hurdle rate of return, or the minimum required return, that a business needs to make to overcome the cost of the capital.

As seen, its ROCE has declined quite a bit over years due to the above issues. To wit, its ROCE was above 22% in 2012 and has declined to the current level of 13%, not only a far cry from its good old days but also below its 10-year average of 15.7%.

Source: Author based on Seeking Alpha data

Valuation and return projections

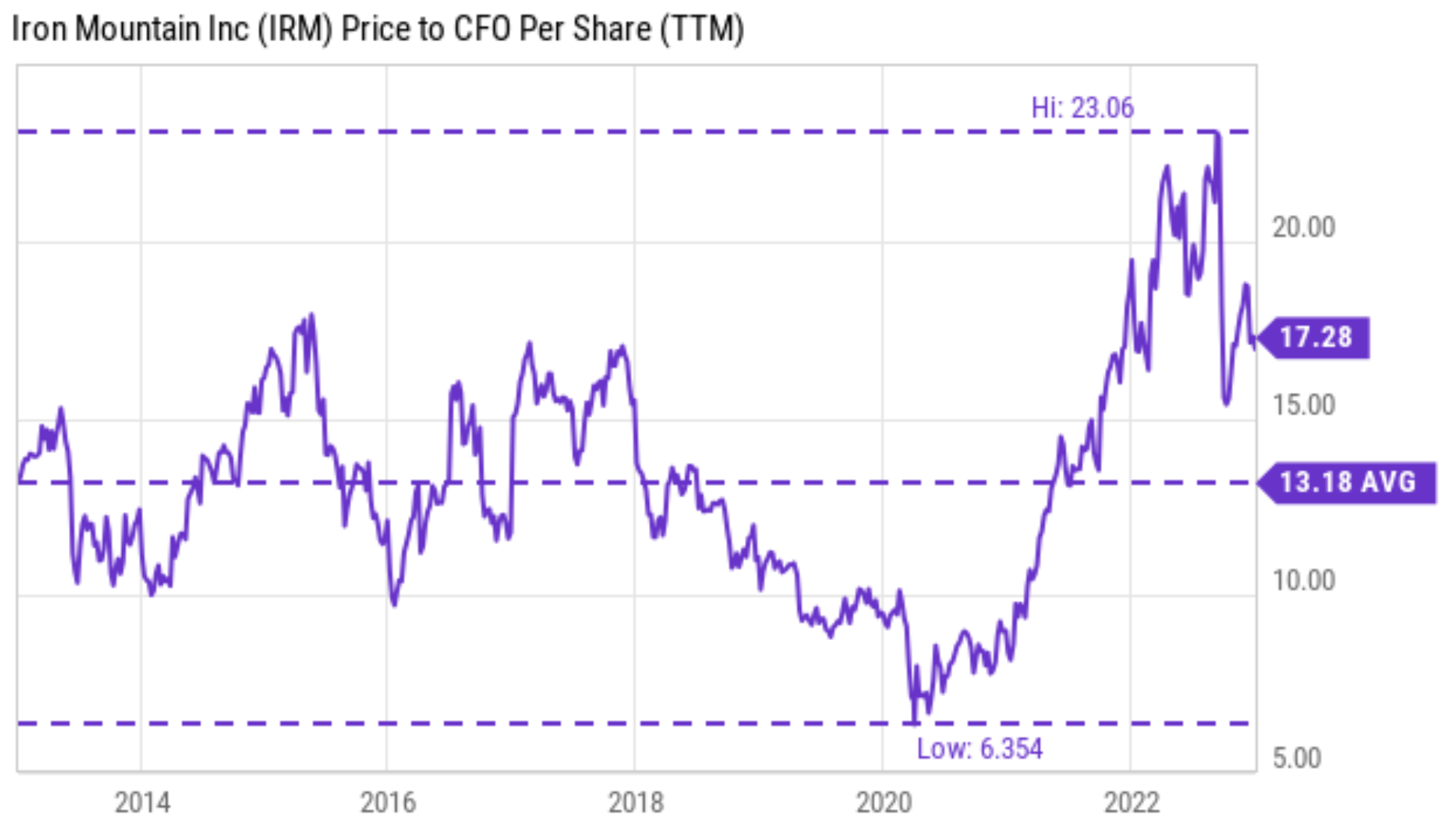

Onto valuation. Currently, the stock is valued at 17.3x of FFO as seen from the chart below. To put things under historical perspective, the P/FFO multiple for IRM has fluctuated in the past between 6.3x and 23.1x with an average of 13.2x. Therefore, its current valuation is actually on the more expensive end of the spectrum, above its historical average by a substantial 31%.

Source: Seeking Alpha data

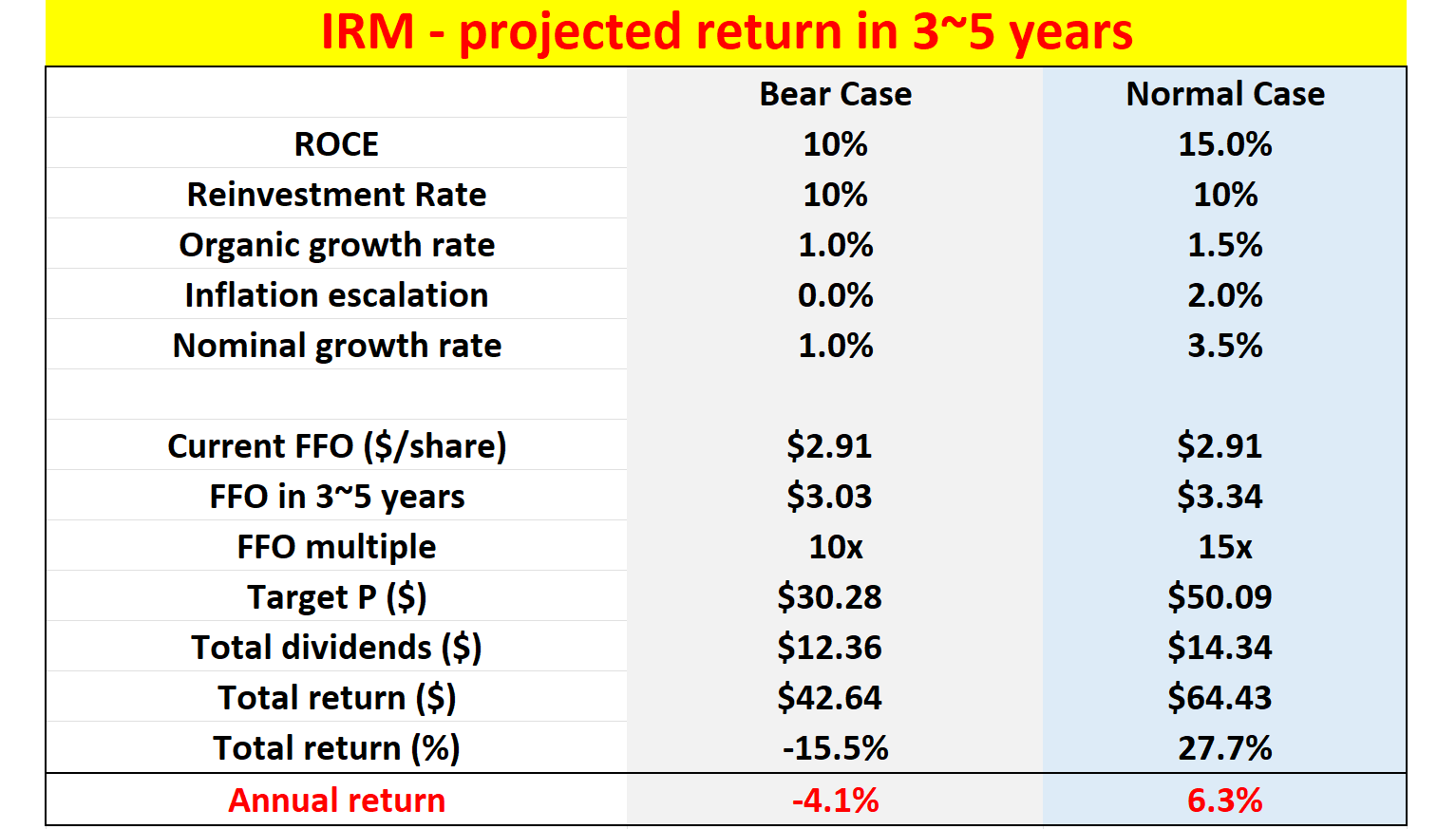

The combination of muted growth and high valuation lead to an unfavorable return profile as shown in the chart below. In these return projections, I am assuming that its dividends grow at the same pace as its FFO. And I am also assuming dividends are not reinvested to simplify things.

The bear case represents a further compressed ROCE of 10% from its current 13%. The 10% reinvestment rates (“RR”) are consistent with its actual level in recent years. Under this combination of ROCE and RR, its organic growth rate will be 1% per year (10% ROCE x 10% RR = 1%). In the bear case, I am also assuming that its pricing won’t be able to keep up with cheaper competitions and also the inflationary pressure as aforementioned. And lastly, I am assuming a compressed valuation multiple of 10x FFO.

The normal case assumes an expansion of ROCE back to its historical average of 15%. In this case, the organic growth rate would be about 1.5% (15% ROCE x 10% RR). At the same time, this case also assumes that management can successfully pass the inflationary pressure and electricity costs to customers. In this case, an inflation escalator of 2.0% is added to its growth rate as seen below. And finally, in this case, I am assuming a 15x FFO multiple, about 14% above its historical average.

And now as you can see what I mean by a mediocre return profile. The bear case projects a total loss of 15.5% in the next 3~5 years (translating into an annual loss of 4.1%). And the normal (or should I say bullish case) projects a total return of 27.7% in the next 3~5 years (translating into an annual return of 6.3%).

Source: Author

Other risks and final thoughts

To recap, I see multiple headwinds here, including competition from cheaper digital storage alternatives, inflationary pressure, higher energy cost, and also higher borrowing costs. Besides these, the business also faces currency pressure due to its global revenue streams. As an example, in the third quarter, its revenues went up 14% YoY, but the strong dollar cancelled off 4% of the growth. The major upside risk I see is its acquisitions. Its successful acquisition of IT Renew recently has opened the door for its entry into the information technology disposal business. Future similar acquisitions could add growth catalysts to supplement/replace its traditional paper storage business.

To conclude, I anticipate IRM’s stock price to be trapped in a consolidation window in the near term due to earnings headwinds and its current valuation premium. I’m seeing a mediocre return potential. For an entry price between the $45~$55 consolidation window, I am projecting a return potential somewhere between an annual loss of 4% to an annual gain of 6%. As such, I am updating my rating on the stock from “Buy” to “Hold”.

Be the first to comment