pong6400

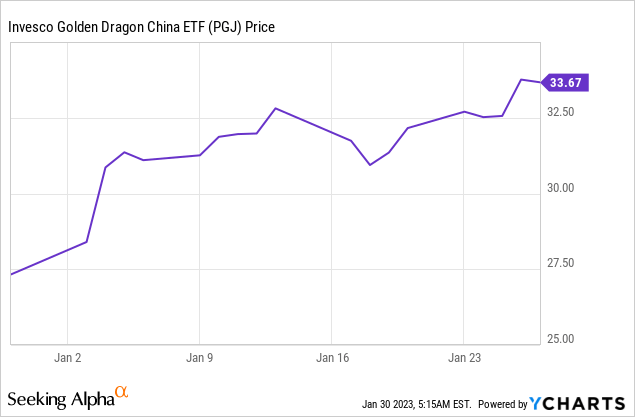

At some point last year, the debate on Chinese equities, and by extension, the Invesco Golden Dragon China ETF (NASDAQ:PGJ), was about their investability, coming off multi-year lows and harsh regulatory crackdowns across key internet companies. The investment narrative seems to have taken a ‘U-turn’ alongside the abrupt ending of China’s zero-COVID policy, with the rebound in Chinese stocks through November/December 2022 extending into this year as well, led by last year’s laggards (internet and property).

The economic data hasn’t yet caught up to the positive investor sentiment, but as we learned from the post-COVID rally in 2020/2021, equities are a forward-looking asset class and will trade ahead of a full reopening and the actual peak in COVID cases. With a full lifting of border restrictions (HK/Macau and international) yet to materialize and with current valuations below 2022 levels, the rally likely still has legs. Investors willing to stomach the (well-known) risks of China equity investing, including the regulatory shifts and opaque ownership structures, will find PGJ a worthy portfolio addition for low-cost exposure to the China recovery.

Fund Overview – Gain Cost-Effective Exposure to Chinese Equities

The Invesco Golden Dragon China ETF tracks, before fees, the performance of the NASDAQ Golden Dragon China Index. As the index comprises US exchange-listed equities of companies headquartered or incorporated in China, the fund holds strictly US-listed Chinese depositary receipts (‘ADRs’) and excludes any corresponding Hong Kong listings. Thus, it is important for investors to consider the risks associated with such ownership structures. The ETF had a market value of $273m at the time of writing and comes with a 0.7% expense ratio (0.5% management fee), making it a cost-effective option for US investors looking to access Chinese equities.

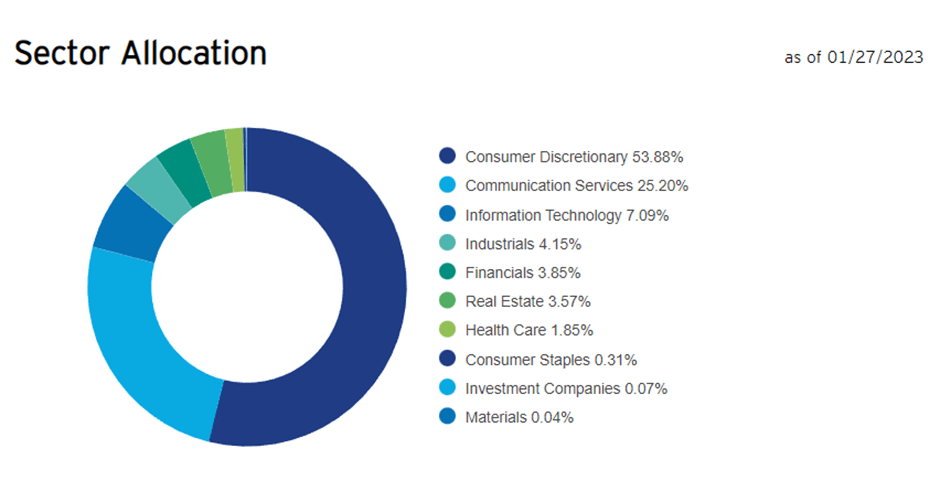

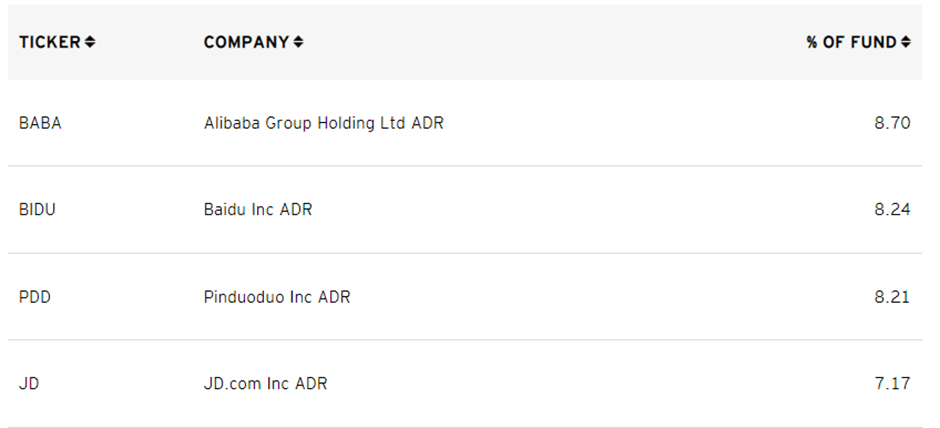

As reflected in the graphic below, the fund’s sector allocation skews toward the consumer discretionary (53.9%), communication services (25.2%), and information technology (7.1%) sectors, which accounted for a combined 86.2% of the total portfolio. The fund’s largest holdings are e-commerce leader Alibaba Group (BABA) (8.7%), Internet-related services and artificial intelligence company Baidu (BIDU) (8.2%), fast-growing e-commerce company Pinduoduo (PDD) (8.2%), and China’s other e-commerce leader JD.com (JD) (7.2%). The top ten holdings represent 32.3% of the portfolio, with single stock allocations maintained below 9% (note weighting restrictions mandate a maximum allocation of >8% only for five securities). Given the very high concentration in consumer discretionary/e-commerce names, this isn’t the most well-diversified ETF and will, thus, be very levered to Chinese consumer/economic cycles.

Invesco Invesco

Fund Performance Reflects the Volatility of Investing in China

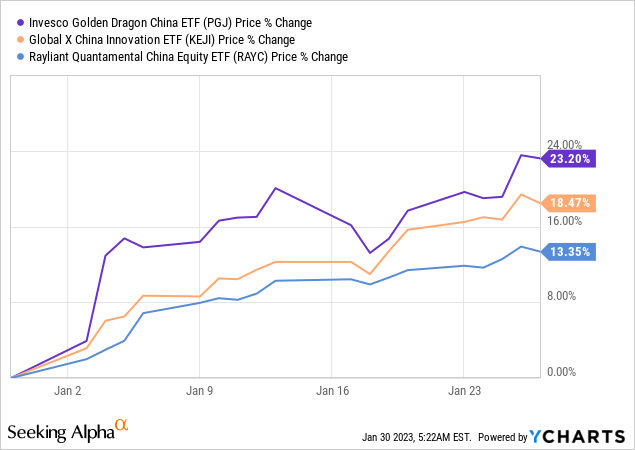

On a YTD basis, the ETF has returned 23.2% and has appreciated in value by a triple-digit % since its inception in 2014; though on an annualized basis, the fund has only compounded at a mid-single-digits % pace (in line with its benchmark index). Last year’s poor performance was a key drag across the space – alternative US-listed China funds like the Global X China Innovation ETF (KEJI) and Rayliant Quantamental China (RAYC) saw equally large double-digit drawdowns while maintaining non-ADR exposure (KEJI, for instance, holds HKSE-listed equities and RAYC holds Chinese A-shares). Of note, PGJ has led the YTD rally in Chinese equities, with KEJI and RAYC trailing at +18.5% and +13.4%, respectively, despite charging lower management fees.

Favorable Chinese Regime Shift Underway

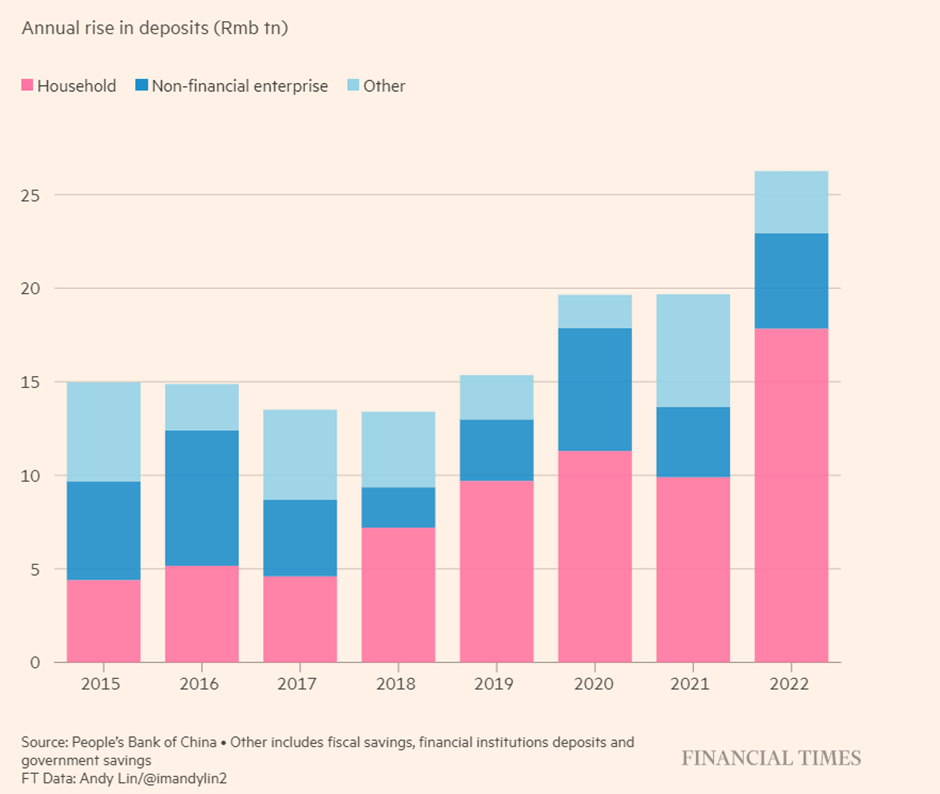

With zero-COVID now cleared, the growth impulse from the domestic economy will be the key focus in the coming months. In particular, the excess savings accumulated by Chinese households bodes well for a private consumption-led economic recovery – the ~$2.6tn of bank deposits held by households last year is almost double the prior year’s figure. While risk-off sentiment likely played a part following the drawdowns in equities last year, spending constraints amid zero-COVID restrictions have been cited as a key factor as well. With these constraints now lifted, expect a mobilization of these deposits into more consumption or perhaps even a reversal in investment flows back into equities. Either way, PGJ is poised to benefit – given its outsized e-commerce exposure, a consumption-led rebound should see the fund benefit from higher earnings revisions, while equity inflows will boost valuations.

FT

The shift in government policy can’t be ignored either – not only on the COVID front but also on fiscal policy loosening, as well as increasingly market-friendly commentary on the private sector (most notably in the beaten-down tech and housing areas). On the monetary policy side, China’s easing stance stands in stark contrast to the West, where central banks are more focused on fighting inflation over stimulating growth. Alongside a household consumption recovery in China, lower rates and higher money supply growth should add impetus to the future economic growth trajectory. In essence, exposure to China via PGJ provides investors a counter-cyclical offset to the largely correlated policy-driven slowdowns in the rest of the world.

Gain Low-Cost Exposure to the China Recovery

Sentiment has turned favorable on the once ‘uninvestable’ Chinese equities, and investors looking to participate in the rebound would do well to consider the Invesco Golden Dragon China ETF for low-cost exposure. In particular, the fund’s outsized exposure to consumer/internet names makes it an attractive option for investors looking to capitalize on the ongoing mean reversion trade – of note, beaten-down sectors in 2022, like tech, are already leading the outperformance this year.

All signs point to the rally still having legs as well. Border restrictions between China/HK/Macau and international have yet to be fully lifted, and following the post-COVID playbook in 2020/2021, equities, as a forward-looking asset class, should trade well ahead of economic data. Plus, the recovery is coming off a very low base in valuation terms; even at current levels, valuation multiples remain below 2022. Net, investors willing to stomach the regulatory risks associated with Chinese equity investments will find PGJ worth a look here.

Be the first to comment