MAGNIFIER

Some weeks ago, International Seaways (NYSE:INSW) released its results for the first nine months of 2022: financial and operating performances were aligned with expectations with a historical record EBITDA. In this article, I will review the key financial metrics and I will explain why I believe International Seaways is still worth a BUY recommendation even after the solid bullish rally of the last months.

If you have never heard of International Seaways, you can have a look at my previous article where I provide an overview of the company. In contrast, if you are looking for other stocks in the oil tanker market, I also cover Teekay Tankers (TNK).

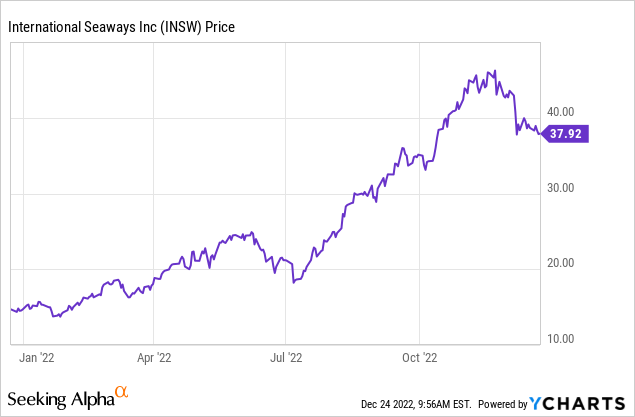

Stock performance

International Seaways is currently trading at $37.9/share, equivalent to a market cap of $1.86 billion. Throughout 2022, the stock had an incredible upward movement and it is now up 158% year-to-date and up 40% versus the price at my previous article publication. However, in the last 30 days, there was a slight downward movement that – from my point of view – represents a good entry point. The 52-week maximum is $46.2/share (November 22nd, 2022) while the 52-week minimum is $13.7/share, recorded almost one year ago, on January 26th, 2022. It should be mentioned that the stock is characterized by some volatility with the 52-week standard deviation being $9.6/share.

Financial results

Total revenues for Q3-2022 were at a record high of $234M, up 221% year-on-year ($73M in Q3-2021) and up 26% quarter-on-quarter ($185M in Q2-2022). About 67% of revenues were generated from the product tankers ($159M) while the remaining 33% came from crude tankers ($75M). The year-on-year growth was not homogenous across the two different tanker categories, with crude tanker revenues increasing by 114% and product tankers increasing by 318%. International Seaways generated most of its revenues (96%) in the spot market and the large revenue increase was mostly driven by the higher average daily rates earned across all the vessel categories (avg daily TCE rate in Q3-2022 was $33.9k vs $12.8k in Q3-2021).

International Seaways

Looking at the cost side, despite a large revenue increase, total operating expenses declined by 27% year-on-year, from $148M to $108M, mostly due to the lack of post-merger integration costs and vessel expenses remaining flat at $58M. Other relevant costs were G&A, up 35% from $8M to $11M and D&A, up 8% from $25M to $27M. Overall, International Seaways reported a historically high net income of $113M, up 64% quarter-on-quarter.

During the first nine months of 2022, cash flow from operations was positive at $106M, mostly driven by the high net income. Cash flow from investing activities was $52M and was the result of several initiatives including:

- Capital expenditure for vessels improvement (-$87M)

- Divestment of vessels (+$79M)

- Sale of the 50% share in the FSO JV that owned 2 vessels offshore of Qatar (+140M)

- Investment in short-term time deposits with maturities between 90 and 180 days (-$80M)

Cash flow from financing activities was negative at -$81M due to some restructuring activities:

- A new $750M secured credit facility was obtained from a pool of banks with a 5-year maturity

- Repayment of debt for $744M from three different credit facilities.

At the end of September 2022, the total outstanding debt was $1.1bn while the cash available was $174M, resulting in a net debt of about $0.9 bn or 48% of the market cap.

Market outlook

International Seaways, and its competitors such as Teekay Tankers, have already largely benefited from the high tanker rates seen in the last months, however, the business context is still far from getting back to the pre-Covid and pre-Russia/Ukraine war dynamics. Indeed, I believe that tanker rates will remain at high levels for the next months helping tanker companies generate profits and sustained cash flows.

On December 5th, the EU ban on Russian crude entered into force with roughly 1 million barrels per day of Russian crude that is now being redirected to other countries (mostly in Asia) with longer average voyage duration. From February 2023, the EU will also ban all the other petroleum products being imported from Russia with the consequence that another 1 million barrels per day of petroleum products will need to be delivered to markets further away.

In addition, oil demand is expected to increase in the next quarters, reaching 102 million bbl/d in 2023 and, with inventories at very low levels, oil delivery from net suppliers to net consumers will become even more important.

However, the increasing demand for tankers driven by the above-mentioned dynamics is not supported by an increase in oil tankers supply with new orders still being at an all-time minimum and the global net fleet growing only 1.5% from September 2021. Overall, I believe that the market dynamics look very good for companies operating in the tanker industry.

Wall Street Analysts’ Ratings

International Seaways is currently covered by 7 analysts with 6 of them suggesting a “strong buy” recommendation and one giving “buy” advice. The average target price is $53.5/per share, which would imply a 41% upside from the current stock price.

Conclusion

International Seaways has achieved another positive quarter with a record-high EBITDA and net income. The company is well positioned to gain the upside provided by the pressure exerted by commodity market dynamics on tanker day rates. Overall, I believe that the current trading price represents an interesting entry point that could still provide a significant upside despite the strong bullish rally of the last months.

Be the first to comment