AscentXmedia/E+ via Getty Images

International Petroleum Corporation (TSX:IPCO:CA, OTCPK:IPCFF), an intermediate Canadian E&P company that is part of the Lundin group, has just released its 2022 year-end financial results. More importantly, on February 7, it held its Capital Markets Day, during which it announced the sanctioning of Phase 1 of its greenfield Blackrod project, an oil sands field located in Alberta, Canada. I have already covered International Petroleum in a series of previous articles, so here I will focus exclusively on the implications of the new project in the context of the company’s overall strategy.

On the one hand, the development of the Blackrod project has the potential to significantly transform the company, adding production of around 30 thousand boepd (for comparison, total production for 2022 was around 48.6 thousand boepd). On the other hand, first oil will flow only in 2026, the capital requirements are significant, and the company is not going to generate almost any free cash flow in 2023, in the current pricing environment.

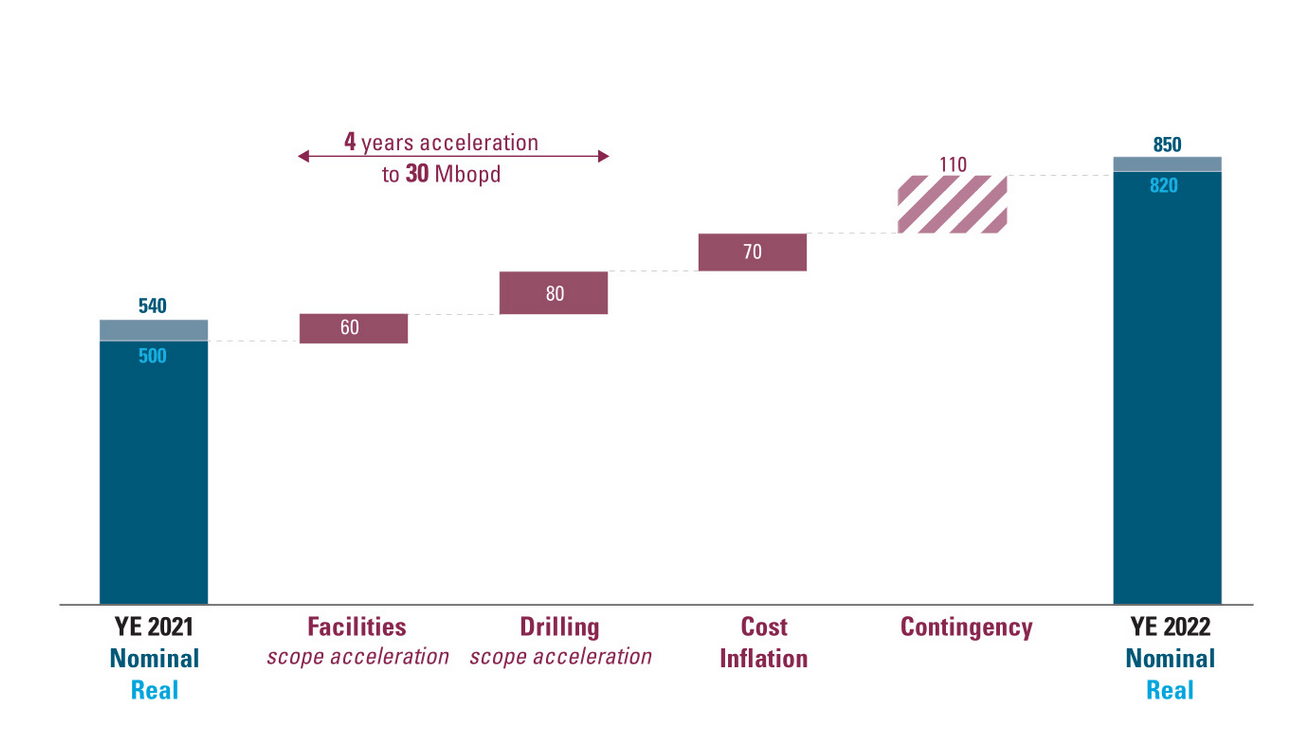

Crucially, the capital costs have come out significantly higher than previously anticipated. The original capex for the Blackrod project was estimated at around $500 million in 2021; now, it has been increased by 70%, to around $850 million. I believe this is the main reason behind the heavy sell-off that has seen the share price in Stockholm plunge almost 15% on Thursday, to a low of around 90 SEK per share, before recovering some ground on Friday. Incidentally, the Stockholm listing has the best liquidity, and most of the selling pressure seems to have originated there, since the Canadian listing did not dip as much. I strongly believe this sell-off offered an excellent entry-point for new investors, as well as an opportunity to accumulate more shares for old investors. In fact, any further pullback to the 90 SEK per share level represents, in my opinion, a buying opportunity.

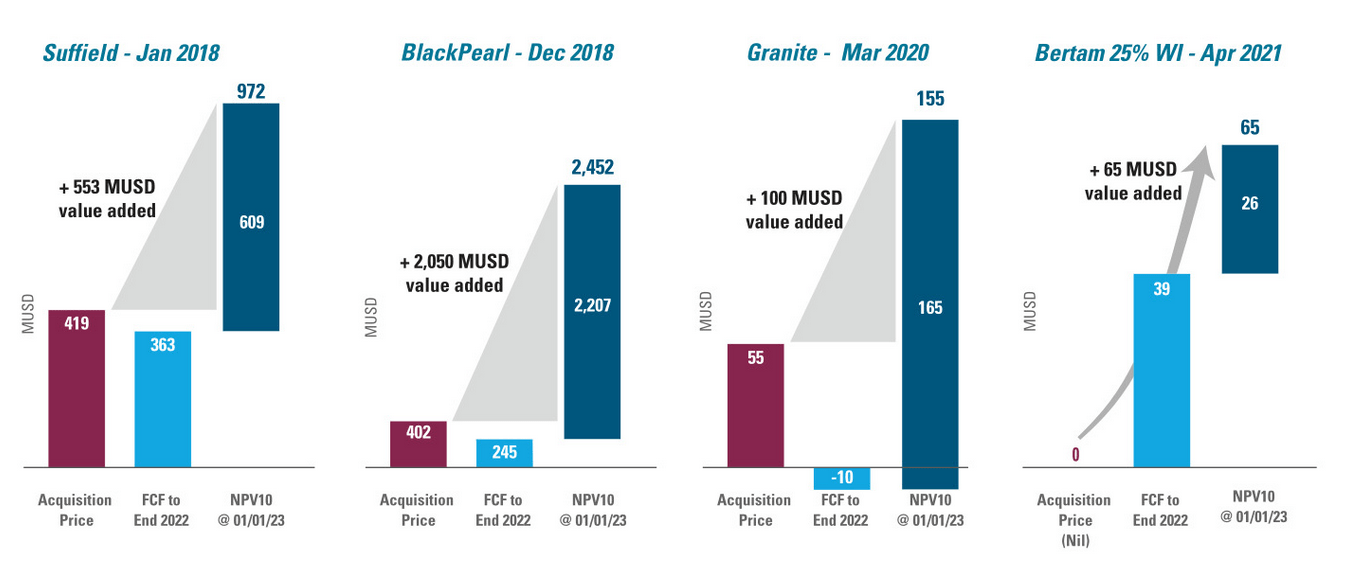

The current management has a remarkable track record of value creation. During the last six years, it has consistently pursued a strategy aimed at both opportunistic growth and capital returns. International Petroleum started in 2016 as a small company with 2P reserves of only 29 million boe. Since then, it has managed to increase its reserves by more than 16 times and add 19 years to its reserve life index. Crucially, it has achieved all this with minimal dilution along the way. The company has generally traded at a large discount to its NAV, so the management has found it efficient to reinvest part of its free cash flow in share buybacks. It has also engaged in well-timed acquisitions, that have added more than $3 billion to its NAV.

Company’s main acquisitions (Company’s Presentation)

The current strategy represents a continuation of the old one. On the one hand, International Petroleum has just added 4 thousand boe via the acquisition of Cor4 Oil Corp for asset consideration of approximately $62 million. Why has management decided to buy Cor4? After all, International Petroleum already has several options on the table to increase its production organically. Is management splurging money on M&A, pursuing growth for growth’s sake? As a matter of fact, this is not the case. The explanation is simply that, in the current inflationary environment, it was cheaper, from a perspective of total costs per flowing barrel of oil, to buy some immediately available, already existing production, rather than to develop its own.

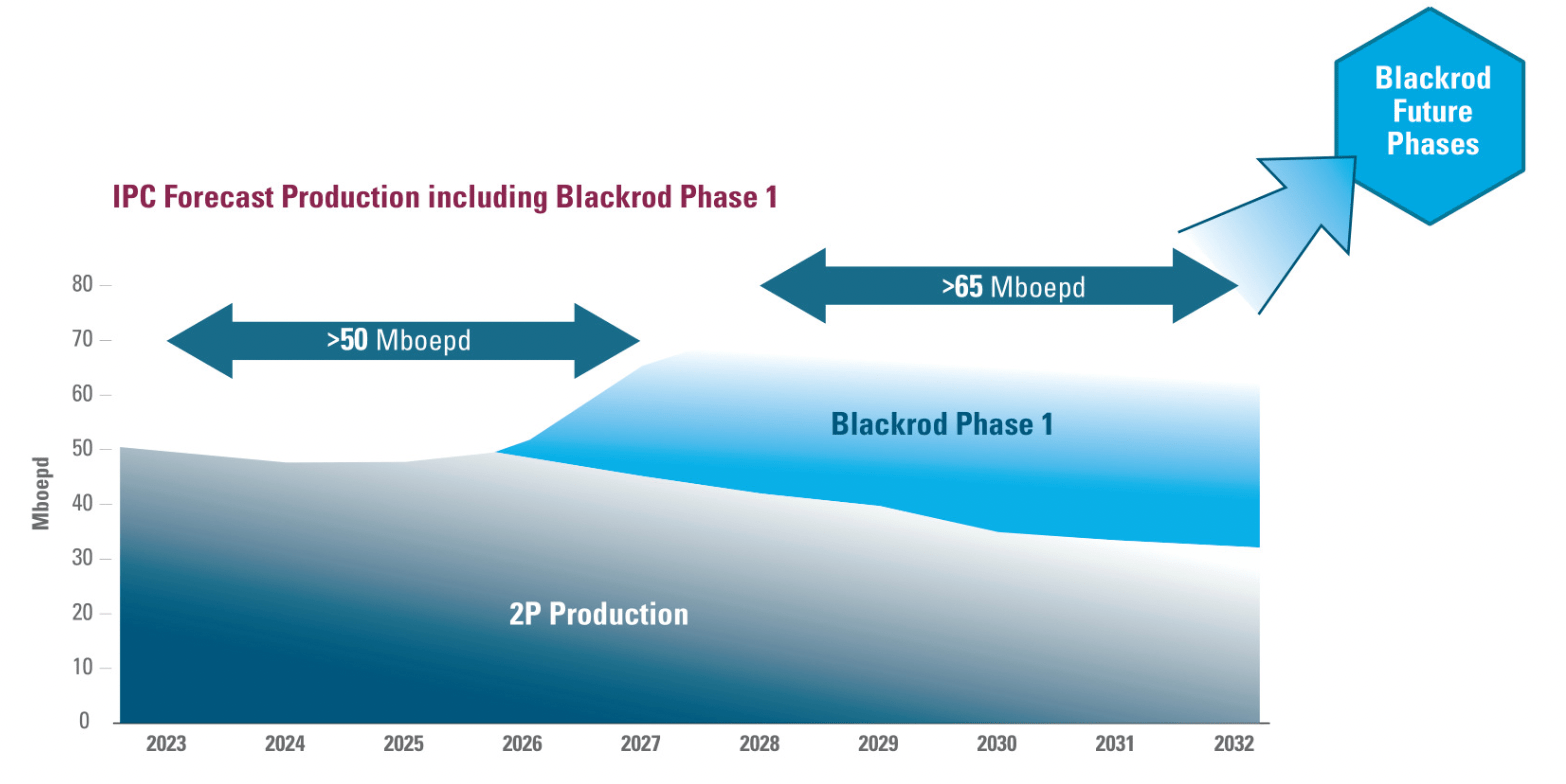

So, in the short term, the company is adding some new production, and it is doing so at a price that is more convenient than the alternatives at its disposal. The intention is clearly to keep the production profile stable, while Blackrod is ramping up. In fact, the company is forecasting stable production of around 50 thousand boepd over the next 5 years. In the same period, it will complete Phase 1 of the already mentioned Blackrod project. Crucially, Phase 1 is going to develop less than 20% of Blackrod’s resources, or around 218 million barrels out of an estimated total of 1.2 billion barrels. In terms of production, Phase 1 will add around 30 thousand boepd, but International Petroleum already has obtained regulatory approval for around 80 thousand boepd. Therefore, there is still significant optionality going forward, even after Phase 1.

Forecast production (Company’s Presentation)

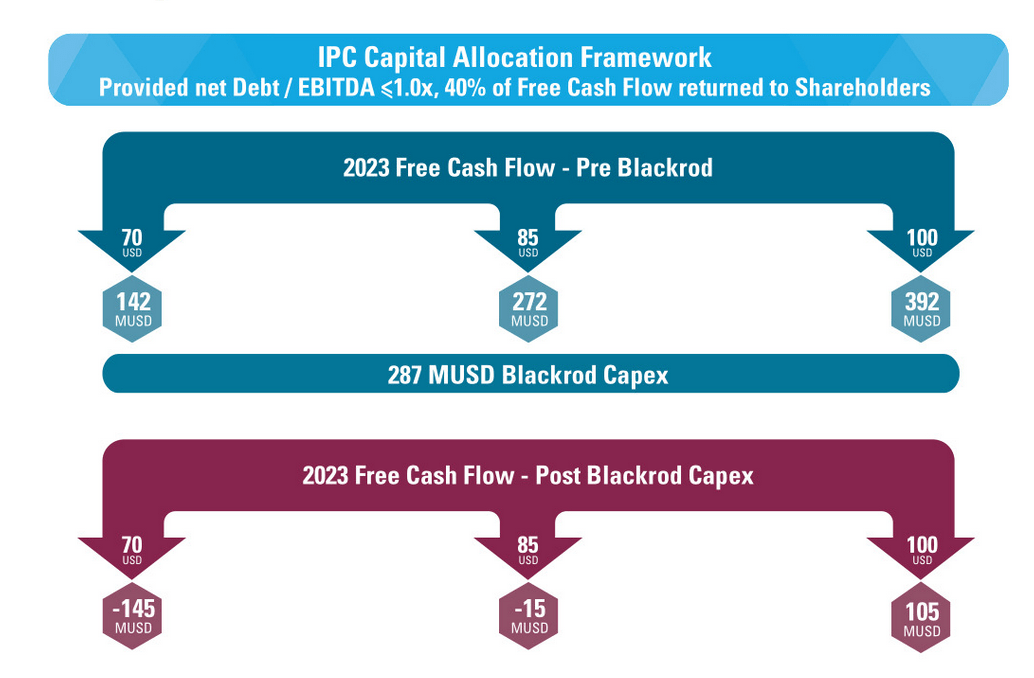

How is the company going to finance the project? The good news is that International Petroleum has a robust balance sheet, with a net cash position of $175 million, and gross cash of $487 million. Pre-production capital expenditures are forecasted to be in the range $800-850 million, of which $287 million during 2023. So, clearly the company already has the resources to get the project started and no dilution is needed. As a matter of fact, it could fund the project in its entirety via its internal free cash flow generation, and still have excess free cash flow to redistribute to shareholders.

Free cash flow will be negligible for 2023, since this year is the most heavily impacted by the capex requirements for Blackrod. Under the company’s base scenario (Brent trading at an average of $85 per barrel, WTI at $80 per barrel, and WCS at $60 per barrel), free cash flow is expected to be around $272 million, before taking into account the Blackrod capex. However, over the 2023-2027 period, International Petroleum is still going to generate significant excess free cash flow. Even after taking into account the impact of Blackrod, cumulative free cash flow will be between $700 million and $1.4 billion (depending on different oil price assumptions, from Brent trading at $75 per barrel in the low scenario, to $95 in the high scenario). The current market capitalization is around $1.3 billion. If the company were to use all the excess free cash flow to buy back shares, then, at current prices, it could buy back between 54% and 107% of its current market capitalization, which is equivalent to an annual yield between 11% and 21%. The company’s policy requires it to distribute only 40% of free cash flow; this would still imply a minimum annual yield between 4.3% and 8.6%.

Company’s forecasted free cash flow for 2023 (Company’s Presentation)

In the meantime, the company will be developing Blackrod. First oil is expected in 2026. Production will ramp-up progressively over the following years, to a total of around 30 thousand boepd. Over the 2028-2032 period, the company’s total production is expected to average around 65 thousand boepd. In terms of free cash flow, this means between $1.9 billion and $3 billion, which is equivalent to a yearly average yield between 29% and 46% (assuming all free cash flow is returned to shareholders).

I believe the value proposition in International Petroleum is quite obvious. If Brent were to average $95 per barrel over the next 5 years, which does not sound like an unrealistic assumption, the company could buy back its entire market capitalization. In fact, even in 2023, it intends to continue its buyback program (at least via its NCIB facility, possibly in excess of it, depending on oil prices). More importantly, while continuing to generously reward its shareholders, the company will also be developing the Blackrod project. This is a truly transformative project that, after Phase 1, will raise total company’s production by 30%, and still offer plenty of future growth opportunities.

Unfortunately, the market is reacting instinctively to the surface of the announcement, without digging deeper into its implications. For instance, the apparent 70% increase in capex is explained by the fact that Phase 1 originally targeted production of only 20 thousand barrels. More careful planning aimed at achieving economy of scale convinced management to immediately go for 30 thousand barrels. In addition, the capex guidance contains a provision of $110 million for contingent expenses, that is meant to allow for future known unknowns. Management has let it be known that the estimate is meant to be conservative.

Capex for the Blackrod project, 2023-2027 (Company’s Presentation)

There is, however, a reason for caution. The project has a relatively high breakeven of WTI $57 per barrel. With WTI trading at $80 per barrel, the NPV 8% would be around $1128 million. The expected annual rate of return would be around 10%. This is of course a function of oil prices. If oil prices were to fall significantly, the margin of safety would not be huge. On the other hand, the project has significant torque in case oil prices rise again above the $100 mark.

Summing up, I continue to see International Petroleum as a value opportunity. The company is pursuing a consistent strategy that combines capital returns via buybacks with opportunistic growth. While Blackrod has not the most attractive economics, it is robust and offers significant leverage to oil prices. Even after Phase 1, it will still have around 80% of its 2P reserves undeveloped, offering options for future growth to capitalize on a renewed oil bull market.

Crucially, even after taking into account the capital costs for developing Blackrod, International Petroleum Corporation remains a cash flow machine at current oil prices. Over the next 10 years, the company could easily generate free cash flow equal to 2–3 times its entire market capitalization.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment