da-kuk

Interactive Brokers (NASDAQ:IBKR) is one of the most popular online stock brokerages in the world. The company is highly rated as a go to service for the average person and professionals. Its platform is less “gamified” than a broker such as Robinhood. In addition, Interactive Brokers offers advanced features such as options and futures trading, which isn’t always available on a range of very simple “free trading” apps. Recently the company has reported strong financial results for the fourth quarter of 2022, as it beat both top and bottom line growth estimates, despite a tough macroeconomic environment. In this post I’m going to break down its financials and valuation, let’s dive in.

Fourth Quarter Financials

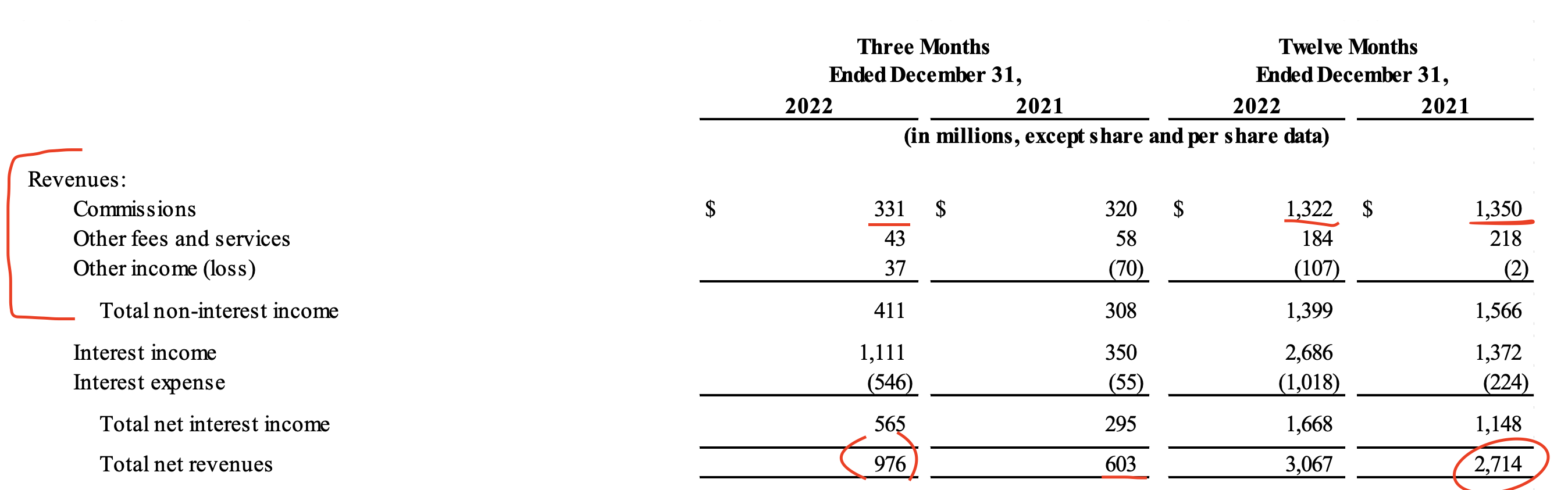

Interactive Brokers reported strong financial results for the fourth quarter of 2022. The company reported revenue of $976 million, which increased by a blistering 61.9% year over year. This main seem like a really fast growth rate for the tough economic environment, but brokerages benefit from interest rate payments on certain funds. In the fourth quarter of 2022, the company reported Net Interest income of $565 million, up from $295 million in the same quarter last year. This was driven by the large increase in interest rates, as the Fed has raised rates in order to combat inflation. Interactive brokers therefore generated higher interest on its margin loans and segregated cash portfolio.

Revenue (Q4,22 report)

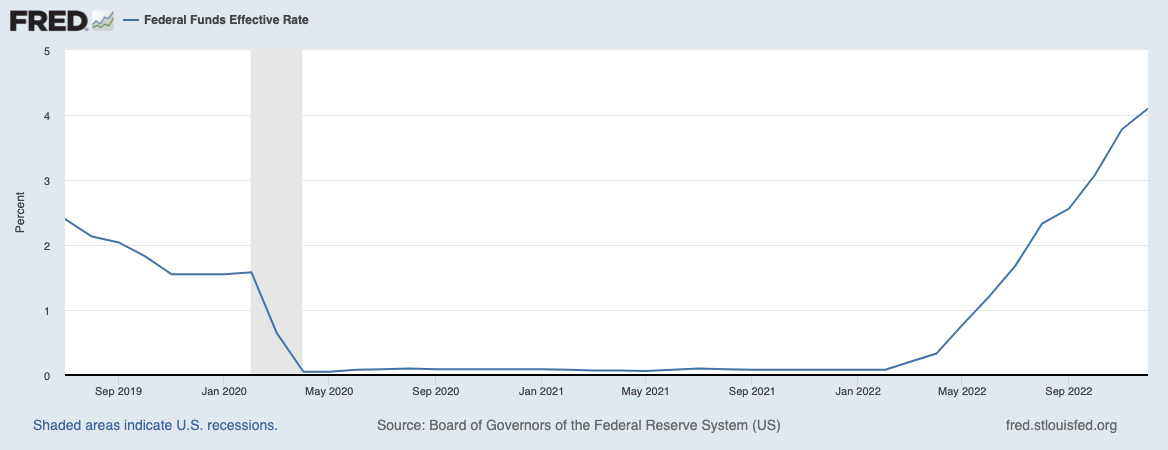

CPI Inflation is on a downward trend from its 9.1% high in June 2022, to approximately 6.5% in December 2022. This is still above the Feds 2% target. Fed chairman Jerome Powell is cautious about lowering rates too fast due to fears that inflation could come back as it did during the 1970’s. Therefore I expect interest rates to remain elevated for at least another 12 months, which means Interactive Brokers should continue to benefit. In its Q4 earnings call, Management even laid out estimates for the net interest income benefit based on Federal fund rate hikes, I have outlined these estimates below.

- At 25 basis points, an increase of $49 million.

- At 50 basis points, an increase of $97 million.

- At 75 basis points, an increase of $146 million.

- At 100 basis points, an increase of $195 million.

Federal Funds Rate (FRED Economic data)

Moving onto Interactive Brokers “normal” revenue, the company generated $331 million in commissions, which increased by 3% year over year. For the full year, this commission revenue was $1.3 billion, which was only down slightly from the “meme stock bubble” of 2021. In general, the macroeconomic environment has caused valuation multiples to compress and the stock market to plummet. The S&P 500 is down 18% from its all-time highs in December 2021. In addition, many big technology and “growth” stocks have had their share price decimated. For example, I have discussed this in depth in my reports on Amazon, Google, Meta, etc. Surprisingly, low stock prices actually result in less trading activity, as many investors get “scared” out of the market. Ironically, low stock prices are usually the best time to buy, but having the “dry powder” on hand can be a challenge as many investors have funds trapped in downtrodden stocks.

For Interactive Brokers overall trading volume was down (as expected), with its Daily Active Revenue Trades (DARTs) declining by 22% year over year to 1.69 million. A positive is the company did report pockets of engagement in areas such as its Futures and options trading which is likely done by more sophisticated investors. Its Industry-listed U.S. options average daily trading volume was over 41 million contracts in 2022, this increased from just under 40 million in the prior year. The business also surprisingly increased its number of customer accounts by 25% year over year to 2.09 million. Interactive Brokers did report a solid increase in “other income” to $107 million, up $37 million year over year. This metric mainly consists of proceeds from a strategic investment into Tiger Brokers (Fintech Holding Limited) and $34 million from its currency hedge strategy. Tiger Brokers has over 1.8 million customers and is popular in countries such as China and Singapore, as well as having a U.S presence. I believe this was a great investment by Interactive Brokers as it helps them gain more exposure to emerging markets.

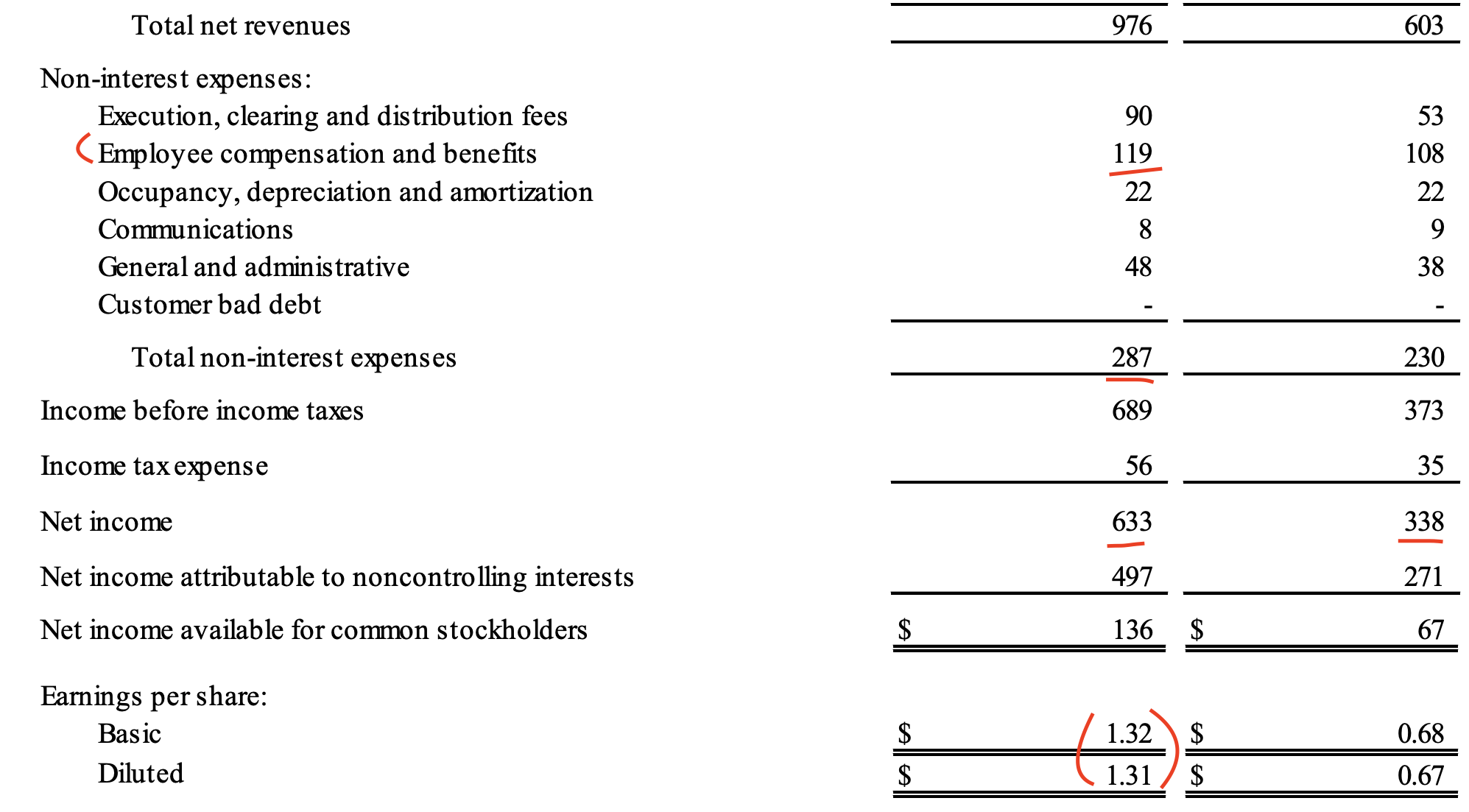

Moving onto profitability, Interactive Brokers reported earnings per share [EPS] of $1.31, which beat analyst expectations by $0.14. This was driven by the aforementioned increase in “interest income” and options trading momentum. IBKR reported a solid pretax profit margin of 71%, which was up substantially from the 62% margin reported in the prior year. This margin is also the “highest in the industry” according to management on its earnings call. This increase in profitability was despite an increase in employee compensation from $108 million in Q4,21 to $119 million in Q4,22. Its execution, clearing and distribution fee expenses also increased from $53 million to $90 million.

Income and expenses (Q4,22 report)

Interactive Brokers has also been investing in continual product improvement and recently launched “GlobalTrader”, which is a streamlined version of its platform for smart phone. New features include rollover options tools, strategy builders and even a “Probability lab”.

The business also continues to expand internationally and has recently received a banking license in Hungary. The company plans to launch in this market in 2023. Although Hungary is a small country it is part of the European Union and an EU banking license is very valuable. This is because there are different rules about how margin trades can be financed in Europe versus the U.S, with banks needing to be involved in Europe.

Interactive Brokers has a solid balance sheet with total assets of $115 billion, which includes customer cash balances. As customer cash/securities should be segregated from the business funds (FTX?), I will analyze the company’s specific cash and debt position. Interactive Brokers has $3.4 billion in cash and cash equivalents. In addition to a solid $25.2 billion in cash segregated for regulatory purposes. The company also has virtually no long term debt, which management confirmed in its Q4 earnings call. It should be noted that some external financial providers such as Yahoo Finance and Seeking Alpha show debt on their financial calculations, but I believe this is not accurate.

Advanced Valuation

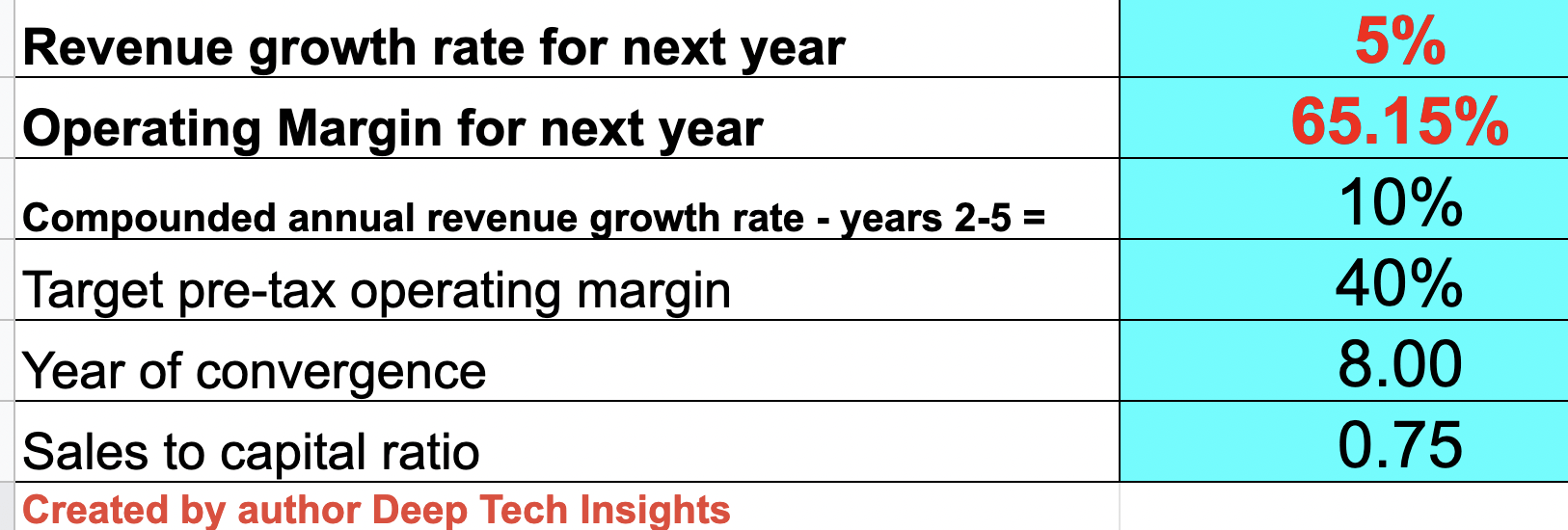

In order to value Interactive Brokers I have plugged its latest financials into my discounted cash flow valuation model. I have forecast 5% revenue growth for “next year”, which is fairly conservative as I expect low commissions revenue growth due to the macroeconomic environment. However, as the Fed will likely continue to raise rates, it could also increase by a much greater degree. In years 2 to 5, I have forecasted 10% revenue growth per year as I expect macroeconomic conditions to improve and stock trading to increase in popularity again.

Interactive Brokers stock valuation 1 (created by author Deep Tech Insights)

For the operating margin, I am expecting a continual high level of ~65%. However, over the next 8 years I have actually conservatively forecast a decline to 40%, as I believe interest rates will decline (thus profitability from interest rates) will over time. This is still not a “bad” margin given the average operating margin for the software industry is 23%.

Interactive Brokers stock valuation 1 (Created by author Deep Tech Insights)

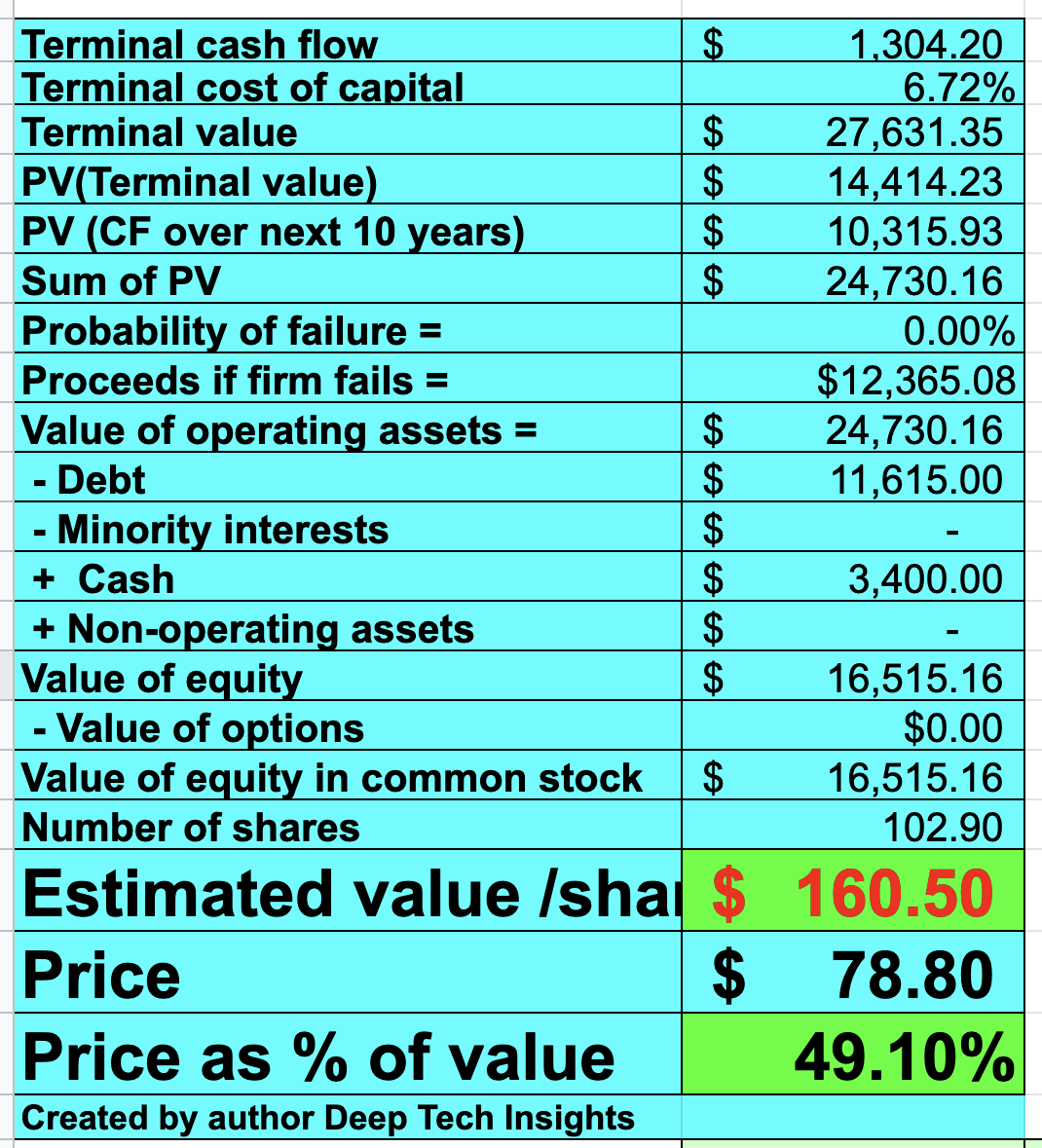

Given these factors I get a fair value of $160 per share, the stock is trading at ~$78/share at the time of writing and thus is over 50% undervalued. As mentioned prior this is with conservative expectations.

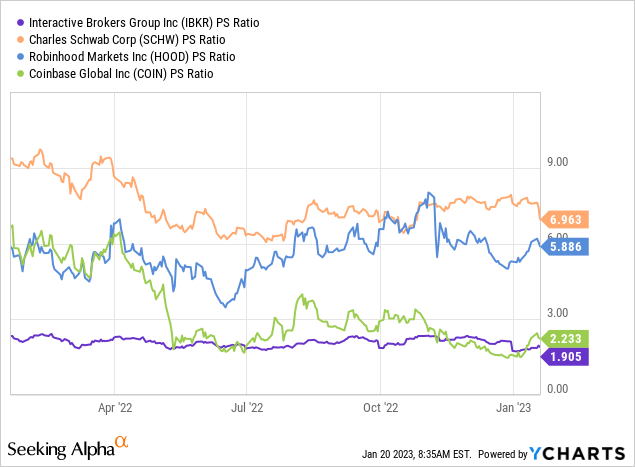

As an extra datapoint its forward price to earnings ratio = 14.5, which is 36.7% cheaper than its 5 year average. Interactive Brokers also trades at a much cheaper price to sales ratio than many other brokers. IBKR trades at a PS ratio = 1.9. Whereas Charles Schwab (SCHW) trades at a PS ratio = 6.96 and Robinhood (HOOD), at PS = 5.886.

Risks

Recession/lower trading volume

Many analysts have forecast a recession for 2023 and thus it seems like that stock prices will be impacted for some time. As mentioned prior, we are currently in a “bear market”, which has resulted in lower trading volume.

Final Thoughts

Interactive Brokers is one of the most popular brokerage companies in the world. The business has continued to produce solid financial results despite a tough economic backdrop. Interestingly, the company has been one of the few businesses to benefit from rising interest rates and is thus technically an inflation or interest rate “hedge” to some extent. As economic conditions are likely to improve in the future I forecast a rebound in its traditional trading business. Its stock is undervalued intrinsically at the time of writing, thus it looks to be a great long term investment.

Be the first to comment