JasonDoiy

Intel Corporation (NASDAQ:INTC) is one of the greatest names in the chip industry, yet its stock has been dead money for years. The company has lost significant market share to Advanced Micro Devices (AMD) in the CPU market recently. Perhaps more importantly, Intel fell behind its competition technology-wise. Shamefully, in 2020, the company had to announce to the whole world that its next major manufacturing milestone needed to be pushed back several years.

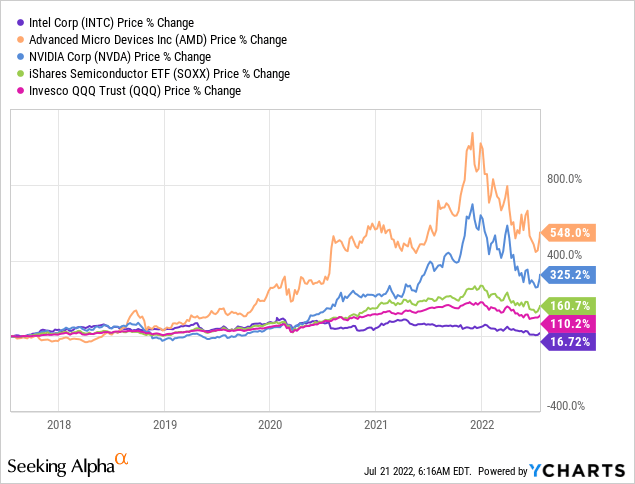

Intel has certainly seen its share of problems in recent years, and stockholders have paid for it, as the company’s stock appreciated by only 17% over the last five years. In comparison, AMD has appreciated by 550%, Nvidia (NVDA) by 325%, iShares Semiconductor ETF (SOXX) by 160%, and the Nasdaq 100 ETF (QQQ) by 110% in the same time frame.

However, despite its recent mishaps, Intel remains a dominant force in the CPU and GPU markets. Moreover, Intel has made some crucial changes and increased R&D spending, leading to improvements in technology and better products. Therefore, Intel will probably regain some lost market share from AMD, leading to improving growth and profitability. Additionally, the company’s CEO said that Intel will reach its crucial manufacturing milestone sooner than anticipated (late 2024), implying that Intel is on the right track to regain its leadership role in the chip sector.

Intel’s earnings expectations have decreased considerably since 2020, and the company’s earnings are likely around a low point now. Future earnings could surpass analysts’ ultra-low estimates, and we should see upward earnings revisions as we advance. Intel is trading at around 16 times forward EPS (consensus estimates) now. This valuation is inexpensive, and the company should increase earnings significantly, enabling its stock price to appreciate considerably as the company advances in the coming years.

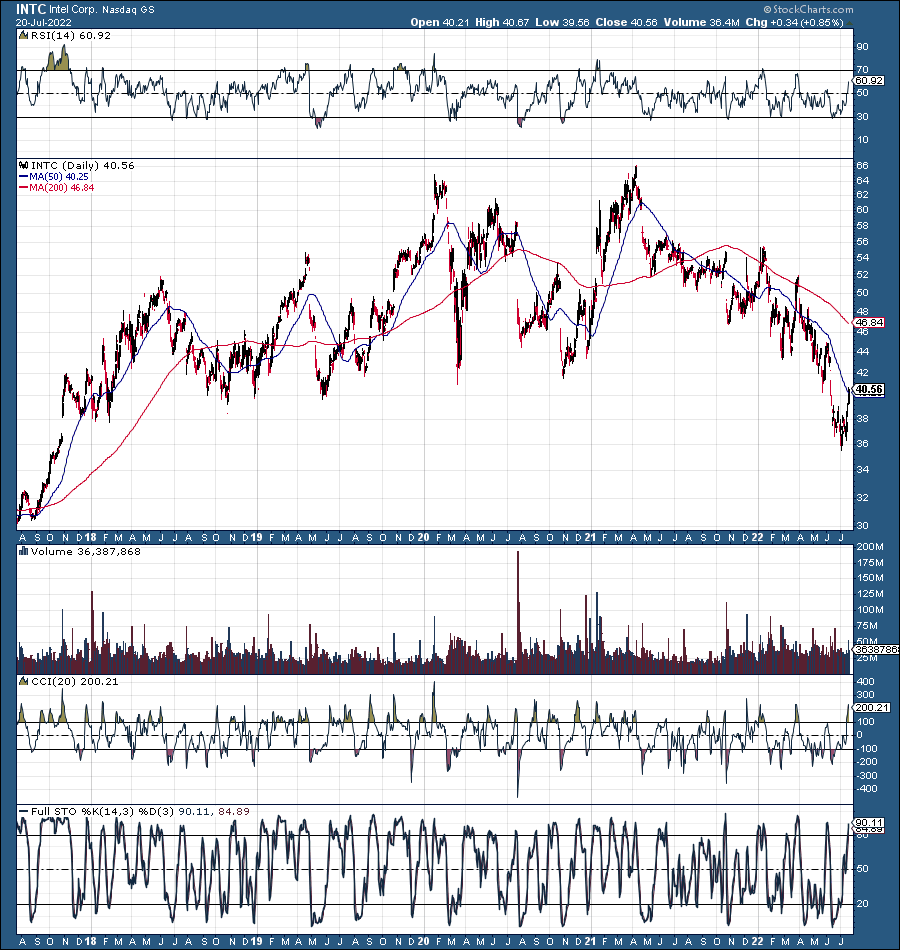

INTC – 5-Year Chart

INTC (StockCharts.com)

Intel has been up and down, but the stock has essentially gone nowhere over the last five years. Now, if we compare Intel to several other prominent chip makers, we see how deep the disconnect and the underperformance have been.

Intel vs. The Competition

If you’re wondering about a longer time frame, like the last ten years, the results aren’t much different. Intel is only up by around 60%, while Nvidia and AMD have appreciated by several thousand. The SOXX and index and the QQQ ETF are up by several hundred percent each. Thus, we see Intel’s significant underperformance going back at least ten years.

So, why would you want to own a stock that has done so poorly and has underperformed its peers in recent years?

Well, things are changing. Intel is going through a crucial turnaround and will likely claw back lost market share. Moreover, Intel’s stock is dirt cheap, and as the company begins improving earnings in the coming years, the stock should appreciate considerably.

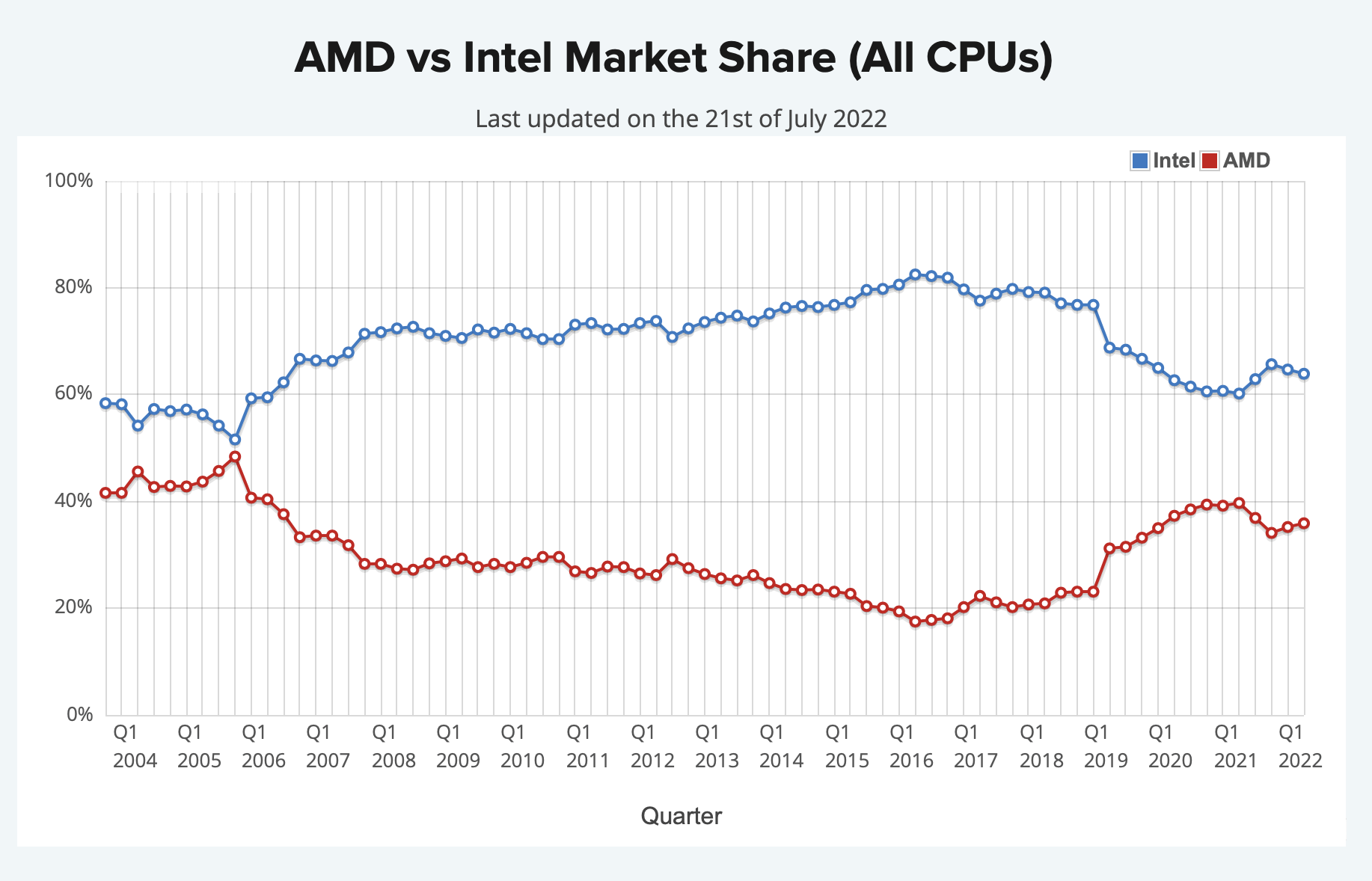

Intel – Likely to Regain Market Share from AMD

CPU Market (All CPUs) (cpubenchmark.net )

Intel’s CPU dominance peaked at around 80% in early 2016. Then, Intel’s market share started to slip, essentially crashing down to just 60% in the 2019/2020 era. However, we’ve seen a rebound in recent quarters, and with the company’s new lineup, we should see Intel’s CPU market share continue to improve. We see a positive trend recently where Intel’s market share has rebounded to around 64-66% in recent quarters, and we may see a continued rise to roughly 70% by this time next year.

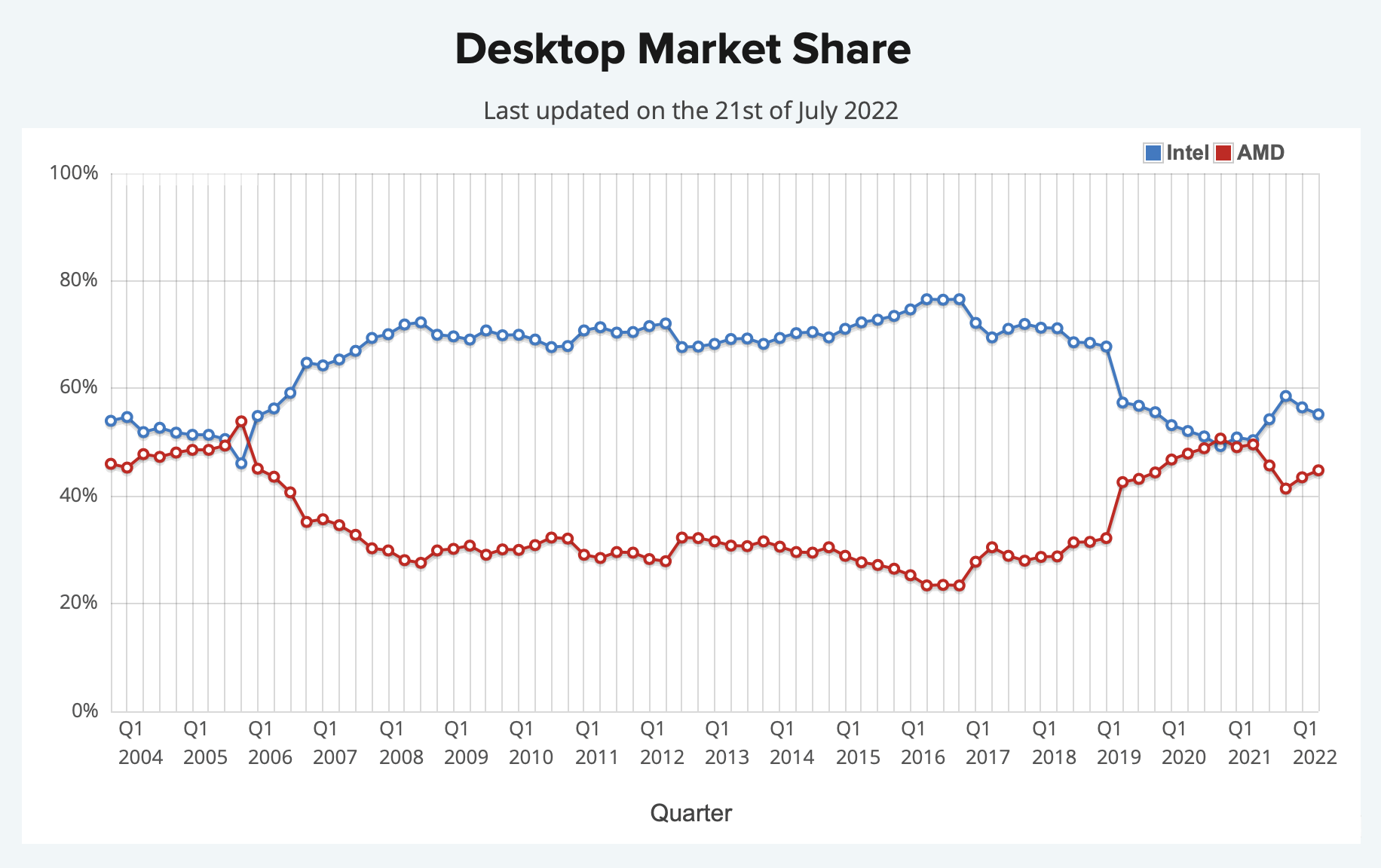

CPU Market (Desktop) (cpubenchmark.net )

Intel’s desktop CPU market share cratered from nearly 80% to just 50% with the recent setbacks. In other words, AMD has been able to eat Intel’s lunch. However, Intel has begun to make gains in the desktop CPU market, reaching a market share of about 60% in early 2022. As intel continues improving its technology and lineup, the company should continue seeing improvements in market share and sales.

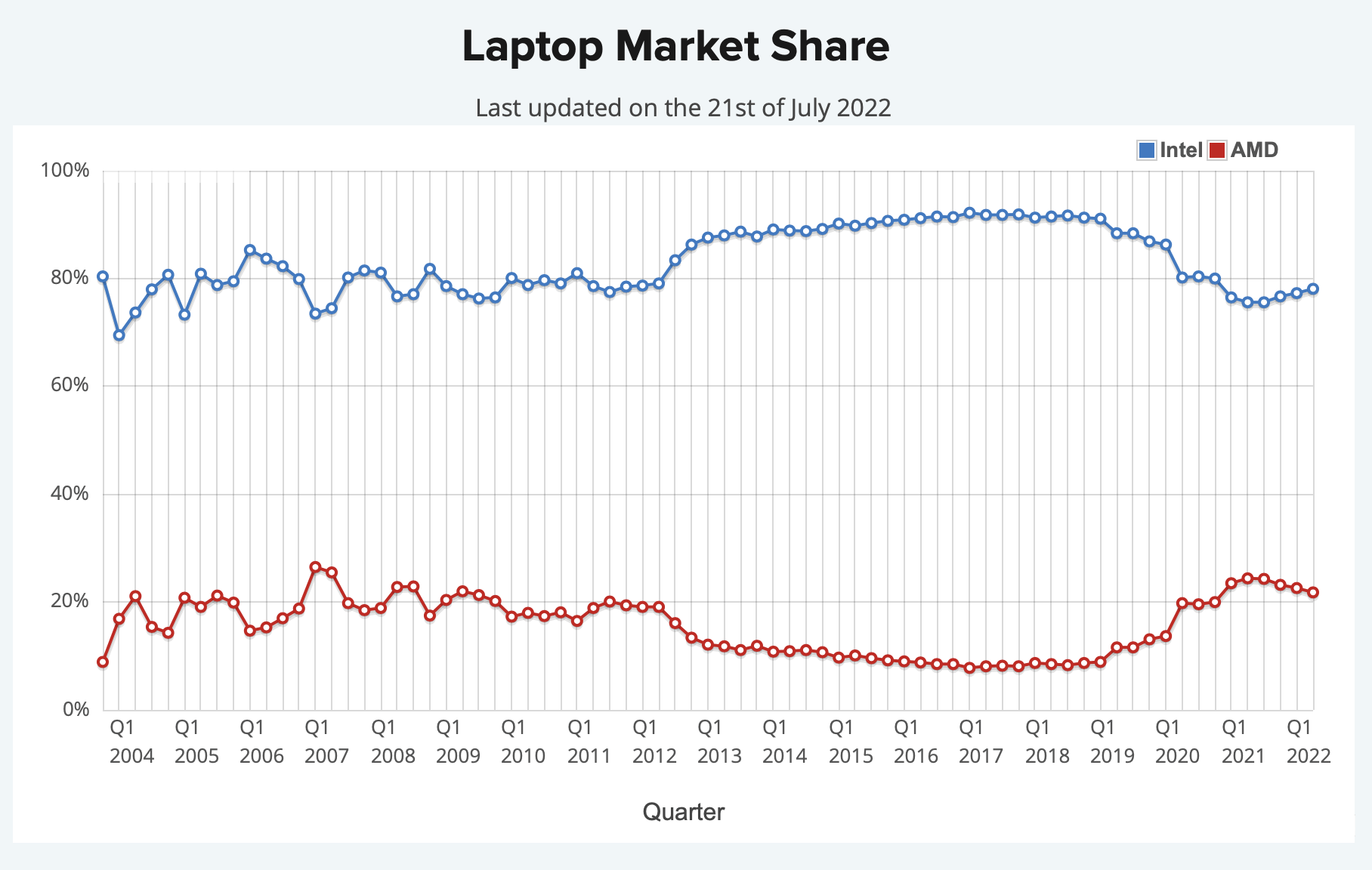

CPU Market (Laptop) (cpubenchmark.com )

The laptop market is where Intel’s CPUs shine, and the company’s market share remained around 80-90% for a long time. However, Intel’s market share slipped into the 70s recently but has also begun to make gains again. The company’s 12th-gen Core CPUs (Alder Lake) could power Intel’s market share back up to 90%.

Now, Let’s Look at the GPU Market

GPU Market (Statista.com)

While Nvidia and AMD dominate the discrete graphic cards market, Intel is the dominant force in integrated GPUs. Despite dropping from more than 70% market share to just 60% in recent years, Intel remains the leading force in the GPU space. Integrated GPUs account for approximately 76% of all GPU sales, and AMD’s Radeon accounts for only around 14% of those sales. While Intel should continue dominating the integrated GPU landscape, it’s also entering the discrete GPU space. Intel’s Arc Alchemist could compete well with AMD and Nvidia in the lucrative dedicated GPU market, leading to higher market share, higher sales, and more profits for Intel as we advance.

Intel’s Investments Should Pay Off

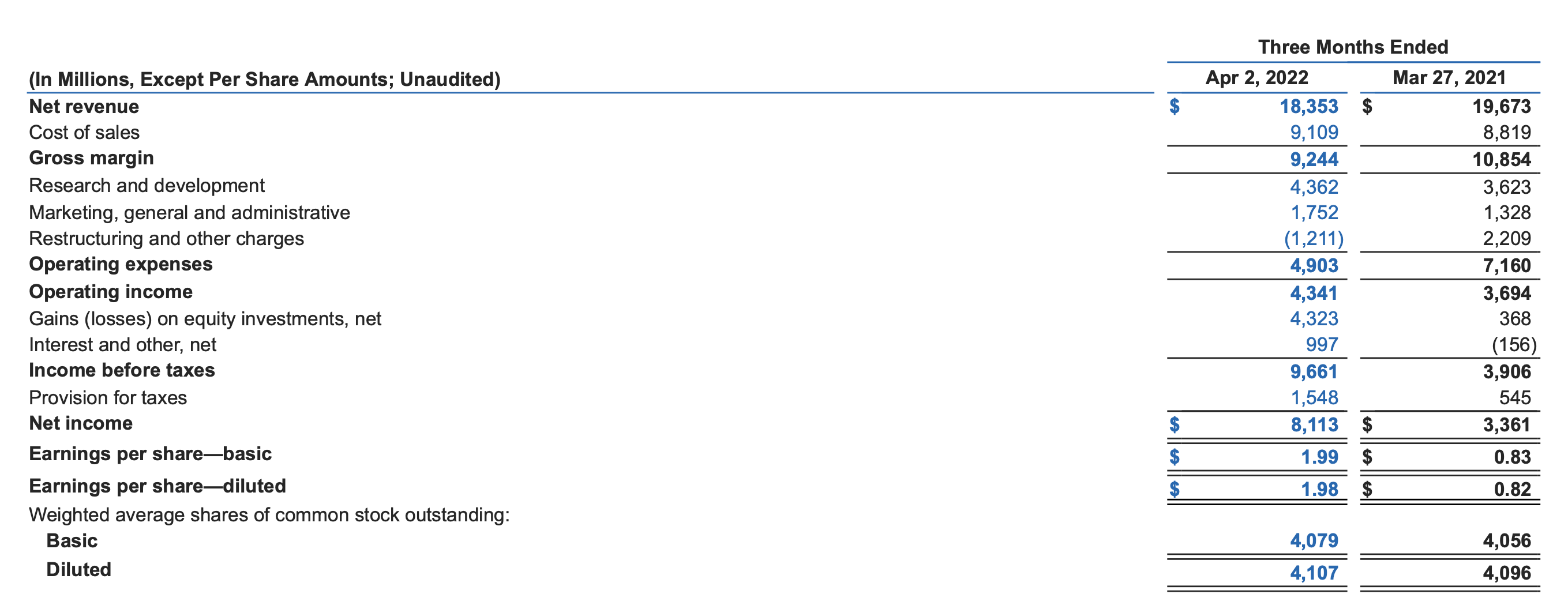

Income Statement

Income statement (intc.com)

We see that Intel’s recent income statement shows a YoY revenue drop of 6.7%. However, despite the significant revenue decline, Intel’s R&D was up by 20% YoY. Additionally, Intel’s marketing, general, and administrative costs increased by 32% YoY last quarter. Last quarter, Intel spent a whopping record $4.36 billion on R&D and nearly $16 billion in R&D spending in its TTM. Therefore, we see that Intel’s priority isn’t maximizing profits right now. On the contrary, Intel is spending massively to regain its technological edge. In comparison, AMD spent about $1 billion on R&D last quarter and has spent roughly $3.3 billion in the TTM.

Now, let’s consider that AMD provided about $5.9 billion in revenues in Q1 while dishing out approximately $1 billion in R&D, roughly 17%. Intel’s R&D budget was about 24% of revenues ($18.35 billion) for the same quarter. Therefore, we see Intel more than quadrupling AMD’s R&D spending, and the company has impressive chip lineups that should recapture some lost market share as we advance.

Intel’s Valuation – Too Cheap to Ignore

Intel’s market cap is about $165 billion, and AMD’s is around $147 billion. Intel’s 2021 revenue was $79 billion, putting the company’s P/S valuation at roughly two times sales. AMD’s 2021 revenue was $16.4 billion, putting AMD’s P/S valuation at nine times sales. Now, I understand that AMD is a growth company with significant earnings momentum, and I own AMD’s stock as well. However, we should not overlook how cheap Intel has become, as the stock represents a remarkable buying opportunity now.

AMD should earn about $4.38 in EPS this year (consensus estimate), putting its P/E ratio at about 20.5. Intel should earn approximately $3.90 in EPS this year, putting its P/E ratio at only around 10. So, we see that Intel is incredibly cheap right now, but we should also consider that earnings and earnings expectations are probably at a low point here.

Therefore, if we look forward:

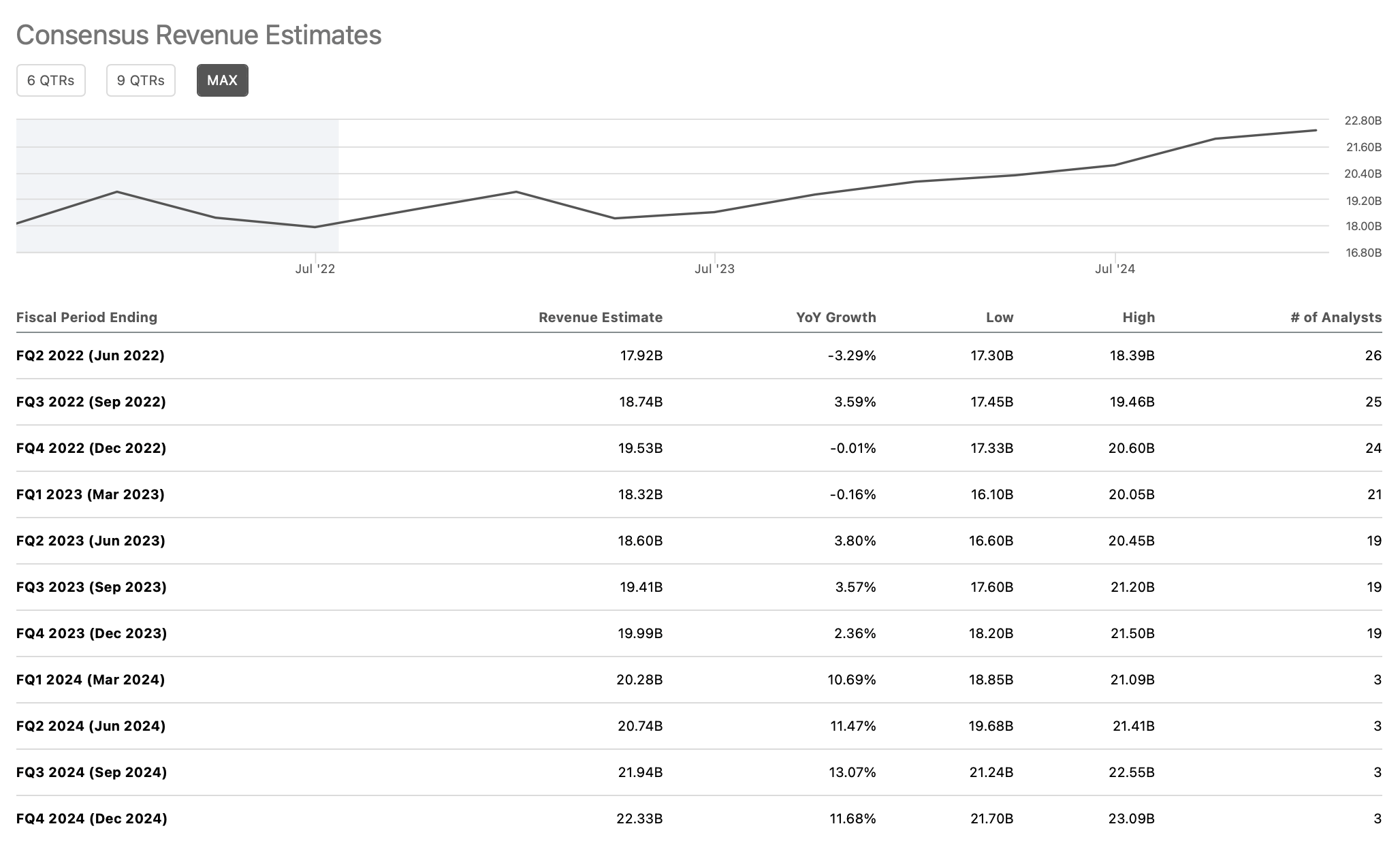

Revenue estimates (seekingalpha.com )

2022 and 2023 should be the rock bottom years for Intel, and 2024 revenues should start growing at double-digits again. Intel should provide about $86 billion in revenues in 2024, but the company could generate closer to $90 billion in revenues, as higher-end estimates suggest.

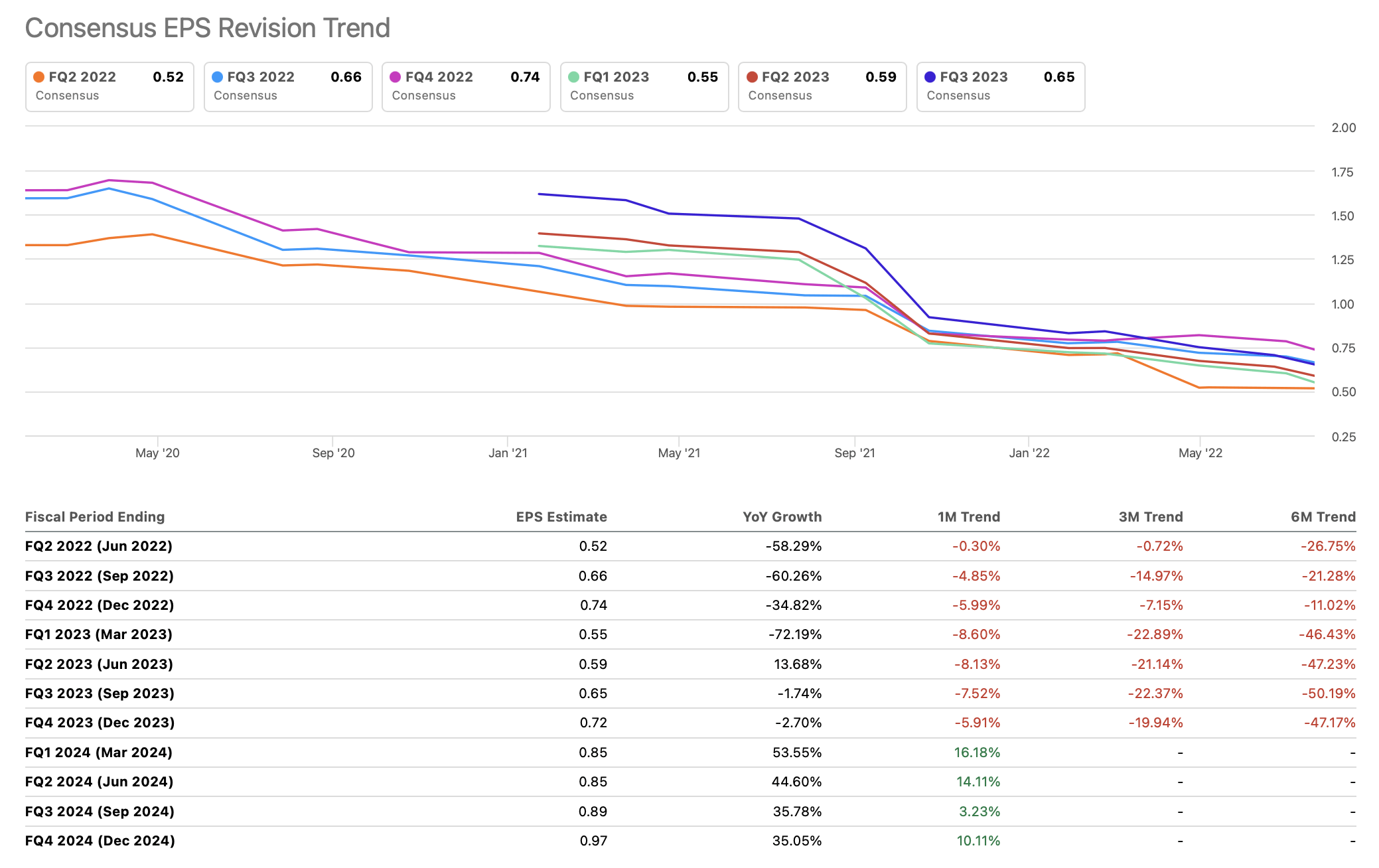

Revisions Tell An Interesting Tale

Revisions (seekingAlpha.com)

In 2020, consensus analysts’ forecasts for 2022 were for more than $6 in EPS. However, current estimates are for fewer than $4 now. We’ve seen EPS estimates drop off by 40-50% in some cases. However, just as EPS projections got lowered in recent years, they should start to rise again. We’re seeing 2024 EPS estimates get a lift, and this constructive trend of upward EPS revisions should continue as the company continues to implement its turnaround plan in the coming years.

This is what Intel’s financials could look like in the future:

| Year | 2022 | 2023 | 2024 | 2025 | 2026 | 2027 | 2028 |

| Revenue Bs | $74.5 | $76.3 | $86 | $96 | $107 | $118 | $129 |

| Revenue growth | 3% | 2.5% | 13% | 12% | 11% | 10% | 9% |

| EPS $ | 3.90 | 2.75 | 4.10 | 4.92 | 6.05 | 7.20 | 8.80 |

| Forward P/E | 14.5 | 15 | 16 | 16 | 15 | 15 | 14 |

| Price | $40 | $62 | $79 | $97 | $108 | $132 | $150 |

Source: The Financial Prophet

As Intel regains its technological advantage, the company should return to low double-digit revenue growth in future years. Additionally, the company’s forward P/E ratio should rise as the stock goes through a period of multiple expansion. Now we’re seeing a low point in the company’s earnings curve, and future years’ EPS could be substantially higher. Therefore, we could see the company’s stock price appreciate considerably as its earnings increase, and the forward P/E multiple expands. Intel could reach $100-150 by 2025-2028, making the stock a strong buy at current levels.

Risks to Intel

While I am bullish on Intel’s turnaround, there are some risks to consider. There is a possibility that Intel won’t make the technological progress envisioned in the coming years. Competition could remain several steps ahead of Intel, leading to more lost market share and lower revenue. Intel may not be as profitable as projected as the company advances. Additionally, Intel could continue experiencing difficulties as it has been in past years. There is also the possibility that the upcoming recession could cause the stock price to drop more before a lasting recovery occurs. Market participants should carefully consider these and other risks before committing capital to an investment in Intel.

Be the first to comment