natatravel/iStock via Getty Images

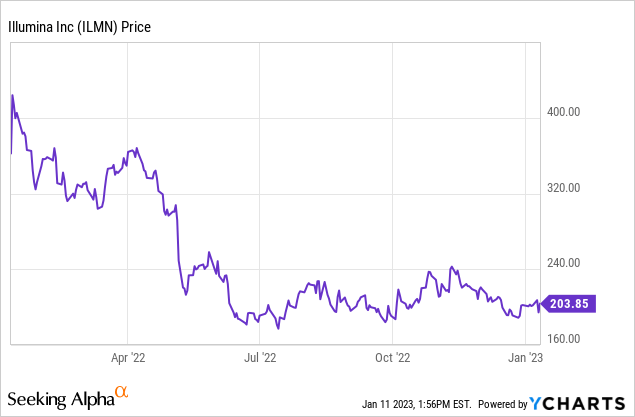

Illumina (NASDAQ:ILMN), the world’s largest maker of DNA sequencing equipment, is recovering somewhat today from a plunge on January 10, 2023. On that day it fell $12.86 per share or 6.2% to $194.45. It had fallen as much as 10% in pre-market trading. It remained above the 52-week low of $173.45 hit on July 14, 2022. While the stock price is more reasonable today than it has been for over a decade, I believe Illumina is still overvalued. In this article I will start with the announcement that sent the stock price down. Then I will show how that confirms the earlier thesis I wrote about in August in Illumina Needs GRAIL, But May Lose It. I will also recap Q3 2022 results, which provide a factual basis for my thesis. I remind everyone that Illumina is still a very successful company that brings a lot of value to the world. The problem is not so much the company itself, as past over-enthusiasm led to failed analysis by investors and most analysts.

Illumina Guidance Disappoints

Illumina made a presentation on January 10, 2023, at the JPMorgan Healthcare Conference. On Slide 10 you can see it estimates 2023 revenue between $4.9 and $5.03 billion, representing annual growth of 7% to 10%. Non-GAAP EPS is expected between $1.25 and $1.50. Revenue is expected to be aided by growth in the GRAIL division of $90 to $110 million, but GRAIL will hurt earnings by generating a non-GAAP operating loss of $670 million. Keep in mind that Illumina could be forced to divest GRAIL, given that it acquired the company (which it had earlier spun off) without EU permission.

Prior to the announcement, the Wall Street consensus for 2023 had been for $5.05 billion in revenue or 11% y/y growth. Worse still, analysts had estimated EPS at $3.10. However, preliminary results for 2022 were about in line with the analyst consensus.

Q3 Results Pointed to the Problem: Slower Growth

We will not get Q4 or 2022 full results until the release and analyst conference scheduled for February 7, 2023. Going back to Q3 2022 results, revenue was up just 1% y/y to $1.12 billion. The CEO blamed challenging macroeconomics, including foreign exchange rates. A goodwill impairment charge for GRAIL hit GAAP net income, leaving a loss of $3.8 billion or loss of $24.26 per share. By eliminating the usual trouble spots, Illumina declared its non-GAAP net income squeezed into the plus column with $54 million, for a diluted non-GAAP EPS of $0.34. Compare that to negative free cash flow of $119 million.

Lining up the stock price with the new guidance

Investors should view even the new guidance with a cold eye. Revenue was up just 1% in Q3 2022 over Q3 2021. What gives us confidence that it can hit the new guidance of 7% to 10%? A price increase? FX tailwinds? In this market where payers are resisting even the old prices, when they can, not everyone wants a full generic sequence. GRAIL growth is the only possible positive I can see in 2023 and it is not guaranteed. Illumina may be a good company with good products, but that is not a magic wand. There is only so much demand in the real world, despite the Addressable Market projections you can find on Slide 5 of the presentation, if you want to argue yourself into assigning a Hold to the stock, even at the current price.

I’m not saying the king of gene sequences has no clothes. I am saying the clothing looks more like a pair of jeans and a jean jacket, not ermine and a diamond-studded gold crown. The stock should be priced accordingly. Gene sequencing is great. But as sequencers become more powerful, the cost per analysis will continue to fall and competition will increase. If at some point GRAIL returns Illumina to an extraordinary growth rate, the stock price should then reflect that. Right now we have a modestly growing company, for which my rule-of-thumb PE is 20-ish. So top guidance of $1.50 for 2023, the implication is Illumina would be attractive at $30 per share. It is not, as far as I can tell, the next Microsoft in the biotech space. It has been around long enough that it is an established company with a large revenue base that is not that easy to grow. Even if you want to bend reality quite a bit and expect it to grow EPS to $3.00 per share sometime soon, and assign a PE of 30 to it, you only get to $90 per share. Anything above that is selling to greater fools.

Be the first to comment