mattjeacock

Author’s note: This article was released to CEF/ETF Income Laboratory members on November 9th, 2021.

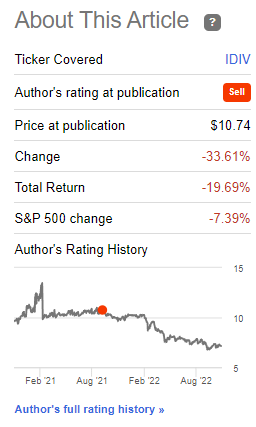

I last wrote about the US Equity Cumulative Dividends Fund-Series 2027 (NYSEARCA:IDIV), a complicated dividend futures ETF, close to one year ago. In that article, I explained in detail how the fund works, and argued that its low long-term expected returns made it a sell. Since then, the fund has posted significant losses, underperforming relative to the S&P 500. IDIV somewhat underperformed expectations, but these were quite low regardless.

IDIV Previous Article

I thought an article explaining why the fund underperformed, and trying to estimate future potential returns, might be of use to readers and investors.

IDIV’s long-term expected returns closely track S&P 500 dividend growth rates, minus expenses. As per historical S&P 500 dividend growth rates and IDIV expenses, investors should expect long-term returns of around 5.0% per year moving forward.

IDIV’s short-term returns are dependent on the market value of its dividend futures, which fluctuate for varied reasons. These have seen rapidly declining prices YTD, due to bearish market sentiment, and due to rising interest rates. Dividend futures with 5.0% in expected long-term returns simply don’t make a ton of sense when T-bills are yielding 4.0%, and investors are pricing these securities accordingly.

IDIV’s long-term expected returns remain quite low, so the fund remains a sell, in my opinion at least.

IDIV – Long-Term Expected Returns Analysis

IDIV invests in dividend futures, derivative contracts with clearly specified characteristics, parameters, coupon, and capital payments. I went through some of the details concerning these securities here, but will include a shorter overview in this article as well.

IDIV’s dividend futures are derivatives contracts linked to the value of the S&P 500 Dividend Points Index (Annual). Said index measures the dividends paid by S&P 500 constituents YTD for the specified date. As an example, as of November 23rd 2022, S&P 500 constituents have paid $61.28 in dividends, and so the index has a value of $61.28.

S&P

IDIV’s dividend futures entitle the fund to all S&P 500 dividend payments during a year, at the end of said year. As an example, the S&P 500 paid $61.28 in dividends during 2021, and so the fund received $61.28 in dividends in late 2021. If the S&P 500 had paid more in dividends, the fund would have received more from its dividend futures, and vice versa.

IDIV currently holds dividends futures for every year until 2027.

IDIV

IDIV buys these dividends futures from a counterparty, and they tend to be quite costly.

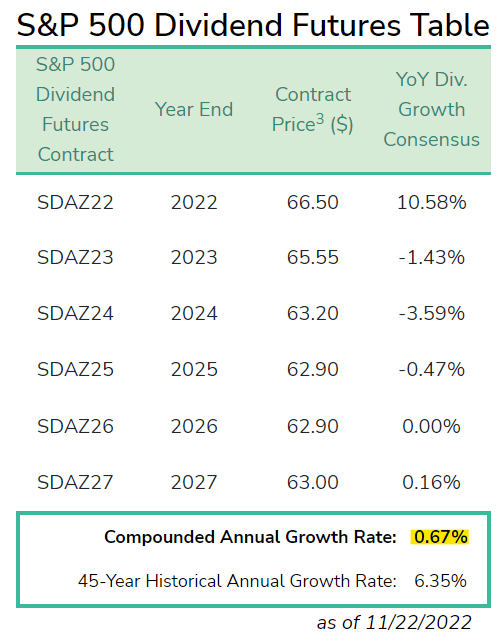

Net profitability depends on the relative magnitude of dividends paid and dividend futures costs. Dividend futures are profitable when S&P 500 dividends are high and futures costs are low, and vice versa. The math behind this is quite complicated, but IDIV provides investors with break-even dividend growth rates. These currently stand at 0.67%, in bold above.

In simple terms, IDIV has said that its dividend futures are profitable if S&P 500 dividends grow by more than 0.67% moving forward, unprofitable otherwise. S&P 500 dividends tend to grow at a 6.35% annual rate, see above, so these futures will almost certainly be profitable long-term. Dividend futures profits would equal 6.35% – 0.67% = 5.68%, assuming S&P 500 dividends grow at the same pace they have done in the past. IDIV’s shareholders would receive around 4.8% in returns, accounting for the fund’s 0.87% expense ratio.

The actual expected returns are a bit more complicated than described above, see here, but not significantly so.

IDIV – Recent Performance Analysis

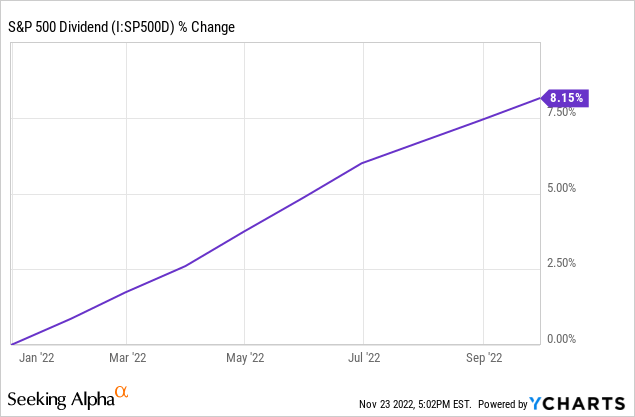

S&P 500 dividends have seen very healthy growth all year, and have grown 8.2% YTD.

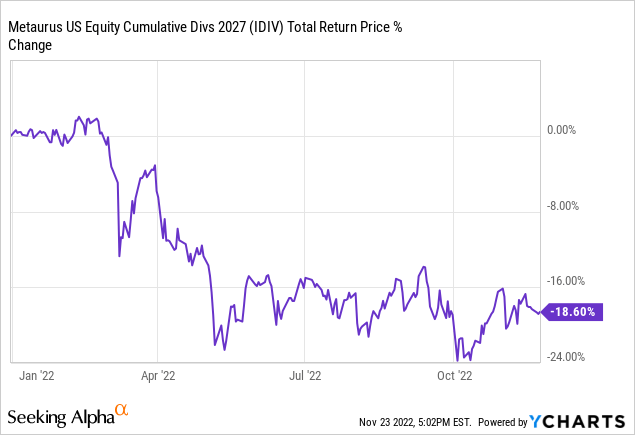

IDIV’s dividend futures should have seen positive returns, but they mostly did not, and so the fund is down for the year, and by a lot.

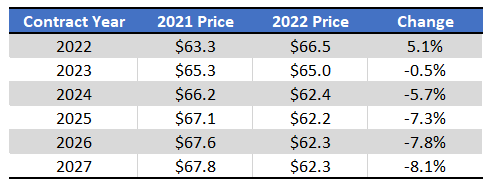

To understand why the fund has underperformed expectations, it might be useful to take a closer look at how specific dividend future prices have evolved these past few months. The following table compares the prices of these securities in late 2021 and late 2022.

IDIV – Chart by Author

As can be seen above, dividend future prices for 2022 increased, a year in which S&P 500 dividends grew, as expected.

Dividend futures for other years, however, decreased instead. The reason why is simple enough: demand for these securities have dropped, leading to lower market prices. Demand decreased for two main reasons.

First, is simply bearish market sentiment. Worsening economic fundamentals, elevated inflation, and rising interest rates, have caused asset prices to plummet, including dividend future prices. In this particular case, some investors are concerned that the Federal Reserve might be forced to engineer a recession to combat inflation, which would almost certainly result in significantly reduced corporate profits, and hence S&P 500 dividends. IDIV’s dividend futures would experience sizable losses if S&P 500 dividends are cut, a distinct possibility under current market conditions. Dividends for 2022 have not decreased, and will almost certainly not decrease, too late in the year for that, so dividend futures for 2022 did not decrease either.

Second, are increased interest rates. Some context first. Looking at my previous article on IDIV, it seems that at the time, dividend futures were expected to yield around 3.7% per year. At the time, that seemed quite low. High-yield corporate bonds were yielding more, as were some equities and other niche asset classes. Dividend futures are not incredibly risky securities, but they aren’t incredibly safe either, so a sub 4.0% yield seemed too low. Today, a 3.7% yield seems absurd: more or less everything yields more, including T-bills, short-term bonds, I Bonds, and investment-grade bonds. There is simply no demand for a 3.7% yielding security under current market conditions, leading to plummeting prices for the same.

Importantly, the issues above are a purely short-term phenomenon, and do not impact the long-term expected returns of these securities, or of the fund. If S&P 500 dividends grow in 2023, then 2023 dividend futures should see strong returns, in 2023. The same is true for other years. IDIV has dividend futures for every year until 2027, so long term should be understood as lasting until 2027.

As a final point, I mentioned some of the issues above in my previous article. Specifically, I said that IDIV’s short-term returns and prices are strongly correlated investor sentiment, and that future prices are in part determined by prevailing interest rates, an important risk to consider. These risks and issues remain, which might result in further short-term losses for the fund and its shareholders. IDIV’s low long-term expected returns do not adequately compensate investors for these risks, in my opinion at least.

Conclusion

IDIV is a dividend futures ETF, whose long-term returns are strongly dependent on S&P 500 dividend growth rates. IDIV’s expected long-term returns are quite low, so I would not be investing in the fund at the present time.

Be the first to comment