Montes-Bradley/E+ via Getty Images

Thesis

The iShares iBonds Dec 2023 Term Treasury ETF (NASDAQ:IBTD) is an exchange traded fund investing in treasuries. The fund falls in the potential cash parking vehicles we are analyzing but falls short when looking at the vehicle from the lens of a retail investor. IBTD contains solely treasury bonds, hence it is risk-free. What is particular about this fund is its defined maturity date in December 2023. As per the fund literature:

IBTD is designed to mature like a bond, trade like a stock. Combine the defined maturity and regular income distribution characteristics of a bond with the transparency and tradability of a stock.

So unlike other instruments that invest in short-term treasuries which are continuously rolled, such as (GBIL) which we analyzed here, or (SCHO) which we looked at here, IBTD has a defined maturity. At the end of 2023, all underlying bonds in IBTD would have matured, and the cash will be returned to investors. So, purchasing IBTD is akin to buying a 1-year treasury bond. There is a difference in duration and yield, though. The fund does not contain just one bond maturing in one year, but a ladder of treasury bonds, giving it a weighted average maturity of 0.56 years. For a rolling fund (i.e., not a defined maturity one) this would make somewhat of a difference because it would reduce duration. For a December 2023 maturing vehicle, in our mind, this doesn’t really matter from a retail investor lens.

The most disappointing part of the equation, though, is the yield:

Holdings (Fund Website)

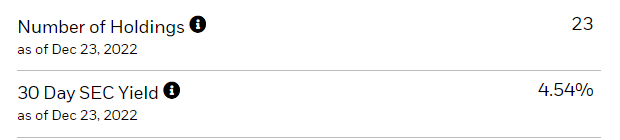

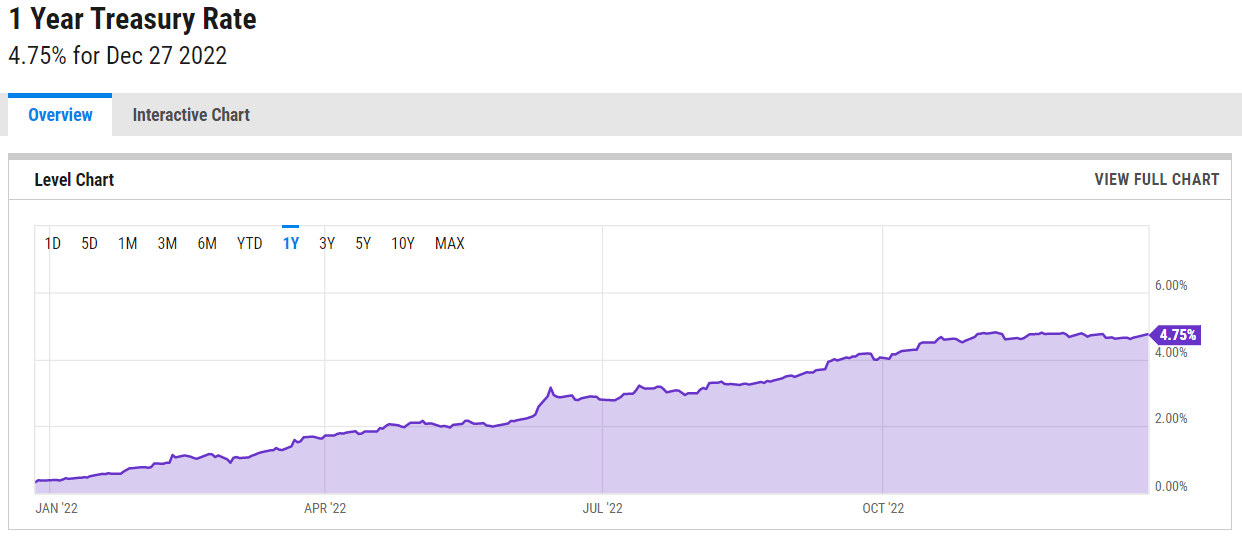

The fund has a 30-day SEC yield of 4.54%, which would seem attractive at the first glance. However, 1-year outright treasury bonds yield substantially more:

1-Year Treasury Rate (YCharts)

If a retail investor just purchases a 1-year treasury outright, the obtained yield is 4.75%. We understand why a large, institutional investor would want the liquidity associated with an ETF and the ability to enter in size without specific name concentration issues, but for a retail individual, IBTD just does not make much sense. At this point, a retail investor wanting to park cash for very short periods of time can just roll 1-month Bills, while said investor looking to lock in a 1-year rate is much better served by just purchasing a 1-year treasury bond outright.

IBTD has no risk from a credit perspective and a very small interest rate sensitivity. Given its defined maturity profile, however, makes it unappealing from a retail investor side given its inferior yield.

IBTD Holdings

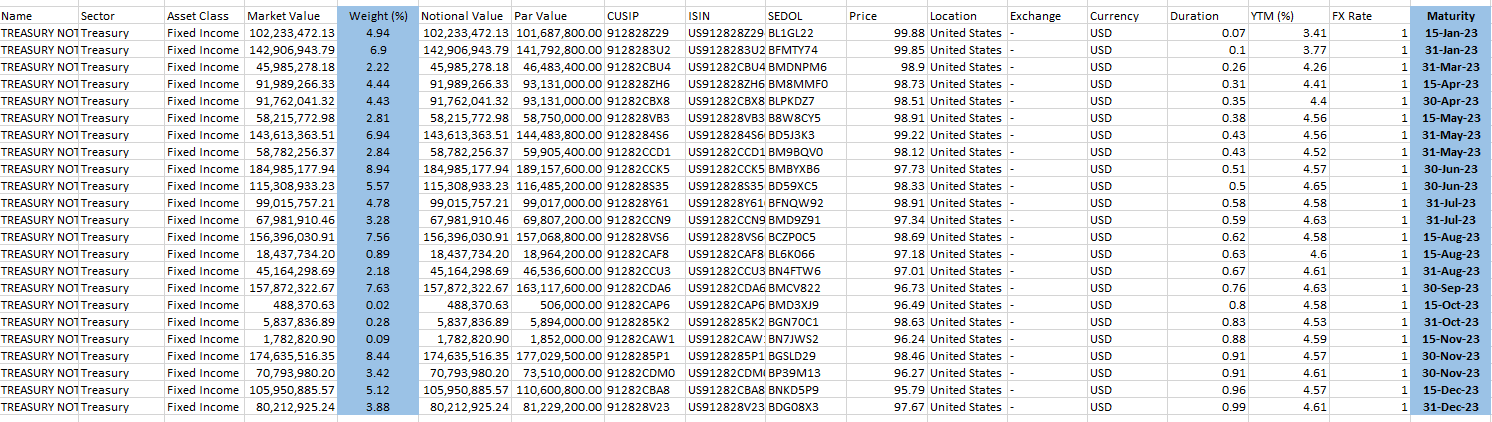

The fund holds a portfolio of laddered treasury securities:

Collateral (Fund Website)

When we drill in the fund holdings, we can see that IBTD holds 23 securities. The held treasury bonds have a staggered maturity, starting in January 2023. The laddered approach gives the fund a shorter duration and weighted average life than a pure 1-year bond.

Treasuries are obligations of the U.S. government, hence they are credit risk-free. The only impact to this portfolio can come from higher rates, but its extremely short duration gives it a very small sensitivity overall.

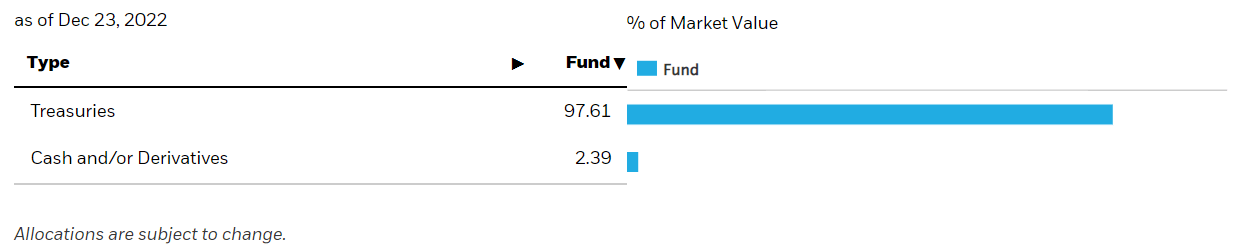

We can see the fund holding some cash as well for redemptions:

Holdings (Fund Website)

IBTD Performance

An investor needs to keep in mind that when purchasing term funds with matched maturity collateral, it is akin to purchasing the respective underlying instrument yield on the traded date. This fund was started in February 2020:

Fund Inception (Fund Website)

At the beginning of the vehicle’s life, ultimately an investor should have expected to receive a total return close to the 3-year treasury rate on the respective date, which was somewhere close to 1.5%. From a total return perspective, we are getting there:

Total Return Since Inception (Seeking Alpha)

Conclusion

IBTD is an exchange traded fund investing in treasuries. The fund has a defined maturity date in December 2023, and its collateral has a matched tenor profile. The fund contains 23 treasury securities with maturity dates staggered throughout 2023. The vehicle currently has a 30-day SEC yield of 4.54%, which is below what a 1-year treasury bond pays (the current yield on a 1-year treasury bond is 4.75%). IBTD’s only advantage versus a 1-year treasury is its lower duration, given its staggered collateral maturity profile. However, for a retail investor looking to lock in higher risk-free rates, IBTD just doesn’t offer any advantages. Conversely, investors looking to park cash short term can just roll 1-month treasuries or purchase (GBIL) or (BIL). At this stage, we do not feel IBTD is very useful for a retail investor.

Be the first to comment