Andres Victorero

The iShares iBoxx USD High Yield Corporate Bond ETF (NYSEARCA:NYSEARCA:HYG) offers a highly attractive yield to maturity of 8.6%, which is high for a fund with a low maturity of 5.2 years and a duration of just 4.0 years. This high yield reflects the elevated yield on 5-year U.S. Treasuries, which is back above 4.0%, and elevated expectations of credit risk. While the ETF is susceptible to intensifying economic weakness, any rise in spreads would likely be accompanied by falling UST yields, supporting returns.

HYG Total Return Performance (Bloomberg)

The HYG ETF

The HYG ETF tracks the performance of the Markit iBoxx USD Liquid High Yield Index and offers a yield to maturity of 8.6%, with a weighted average maturity of 5.2 years. HYG was the first mover in the high-yield corporate bond market and is one of the largest and most liquid junk bond ETFs, with USD15.5bn under management, which compares to USD7.6bn and USD1.1bn for its rival, the SPDR Bloomberg Barclays High Yield Bond ETF (JNK).In terms of the HYG’s holdings, it is highly diversified, with 1,220 holdings and with no single bond comprising more than 1% of the index. Over 80% of the bonds held are in U.S. corporations, the majority of which are rated BB. Industry exposure is also highly diversified, with Media, Telecommunications, and Healthcare Services are the three main industries. The expense fee of 0.48% is on the high side.

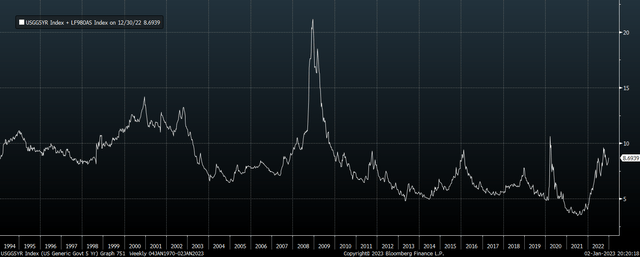

8.5% Yield Is High In The Context Of Current Default Rate

The chart below shows the yield on the Bloomberg U.S. High Yield Corporate bond index (a proxy for the yield on the HYG) going back to 1994. The current yield is above the long-term average of 8.3%, which is not something that can be said for most bond funds.

U.S. Corporate High Yield Bond Yield (Bloomberg)

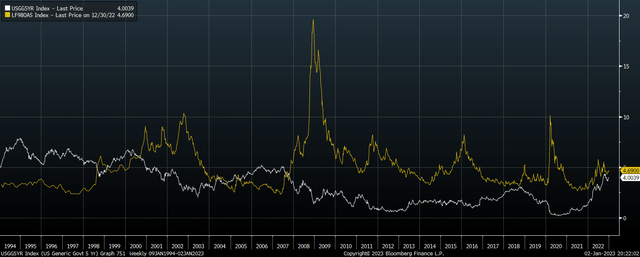

If we break down the yield into the risk-free rate and the spread over Treasuries, we can see that the main reason yields are higher than average is the risk-free rate is higher.

5-Year UST Vs High Yield Bond Spread (Bloomberg)

It could be argued then that investors may be better off holding risk-free USTs instead of high yield corporate bonds, and this may be the case for risk-averse investors. However, the HYG is still likely to perform well over the coming years. As a recent article by Bloomberg noted, junk bond default rates remain extremely low, averaging just 1.2% in 2022, 3.4 percentage points below the HYG’s current spread over Treasuries. Bloomberg quoted Goldman Sachs Group Inc. strategist Spencer Rogers who noted in his latest research that interest coverage ratios and net margins are still hovering near all-time highs for the median HY issuer, while net leverage hovers near multi-decade lows. Goldman is forecasting that the 12-month trailing default rate will move to 2.8% by the end of 2023.

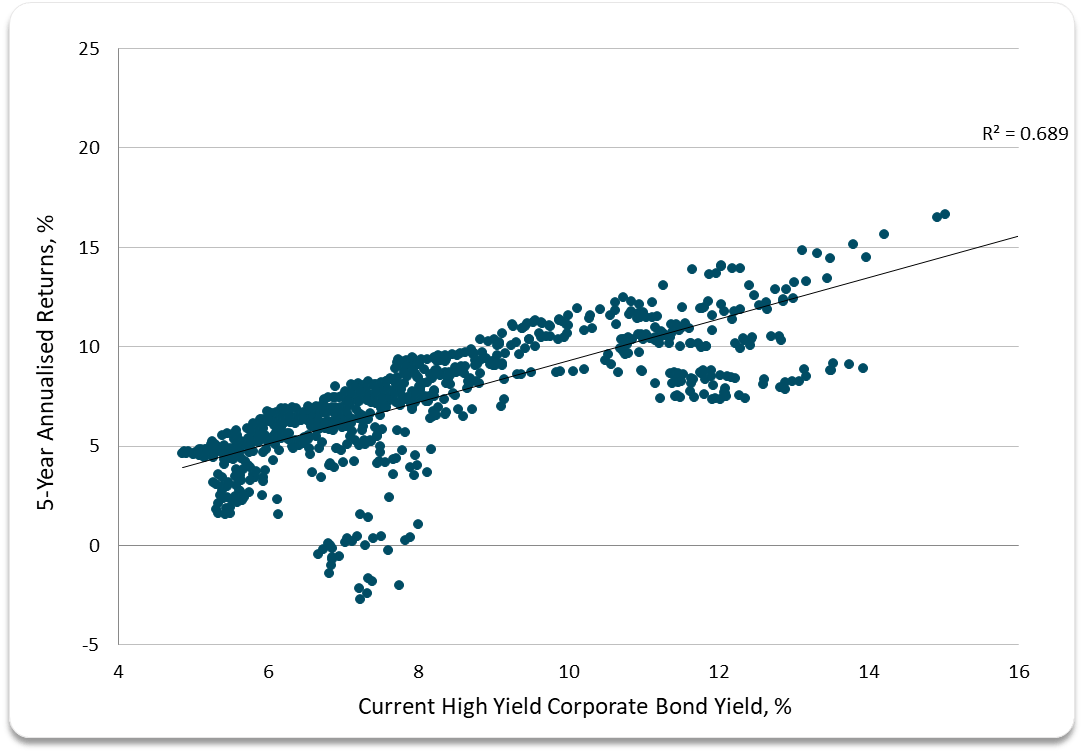

To be sure, default rates tend to peak only after a recession, and we could see a surge in defaults if the economy enters a deep recession. As S&P noted in November, default rates could rise as high as 6% by end-2023 in the event of a deep recession. However, while the rise in UST yields over the course of 2022 has raised interest costs for corporates, it has also improved return prospects for USTs themselves. There is now significant room for Treasury yields to decline in the event of rising default risk. As we have seen during previous spikes in default risk, Treasury yields have fallen, supporting junk bond returns, and this is highly likely to happen again. As seen in the chart below, junk bond yields are very strongly correlated with subsequent 5-year total returns, and current yields imply around 7-8% annual returns.

High Yield Bond Yield Vs 5-Year Annualised Returns (Bloomberg, Author’s calculations)

Summary

The HYG high yield bond ETF is likely to deliver strong returns over the coming years thanks largely elevated UST yields. The HYG is appropriate for fixed income investors looking for higher returns relative to Treasuries, and willing to accept higher volatility. Unless we see a spike in default rates, the HYG is highly likely to outperform Treasuries, while any default spike should be expected to drive down Treasury yields, supporting the HYG.

Be the first to comment