VioletaStoimenova

Hudson Global (NASDAQ:HSON) is an RPO or recruitment process outsourcing company.

The company was previously more diversified in the HR services industry but after an activist campaign it concentrated on RPO alone. Since then, HSON has been growing revenues and profits, and improving cost efficiencies.

HSON has also engaged in small but accretive acquisitions, and has a very strong balance sheet.

Today, the company is facing the risks of a recession, which coupled to operating leverage, generate significant volatility in forward earnings. Using an average of a positive and a negative scenario yields an interesting P/E ratio at current prices. Further, I like the quality of the company’s management.

Note: Unless otherwise stated, all information has been obtained from HSON’s filings with the SEC.

Business development

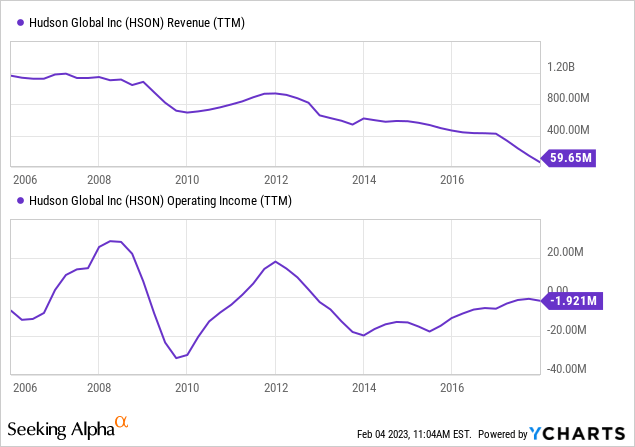

An activist intervened company: Before 2018, HSON was a diversified HR company involved in temporary staff, headhunting, RPO, and other areas. The company had been losing revenues and profitability.

Then, an activist grouped leaded by the company’s current CEO invested in the company and started gaining positions in the BoD and then in management. The first strategic change was to divest most businesses to concentrate on the RPO segment.

The RPO market: The thesis behind the activists was that the RPO business has better competitive characteristics than other HR segments like temporary staffing. According the company’s investor presentation, an RPO provider outsources most of the recruitment function from a company, and therefore becomes a partner of that company. This provides for a more recurrent, less transactional, and higher margin business model.

Indeed, the company did not suffer a significant fall in revenues during the global pandemic in 2020. This provides evidence that the business is not highly transactional and intermittent.

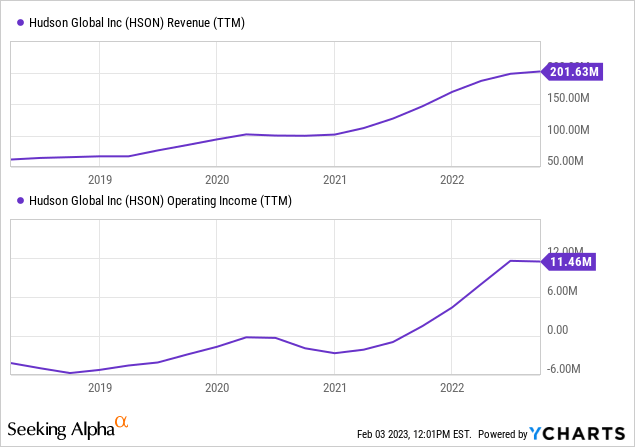

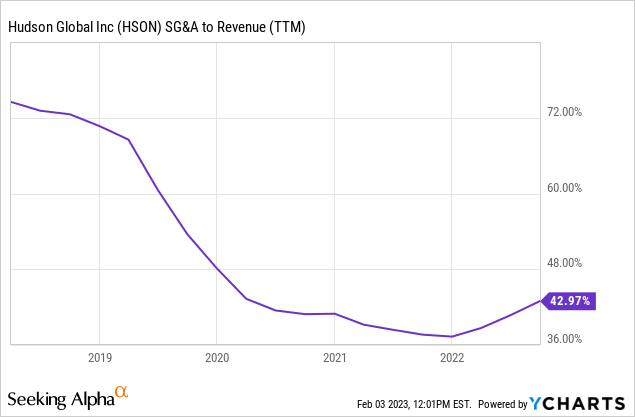

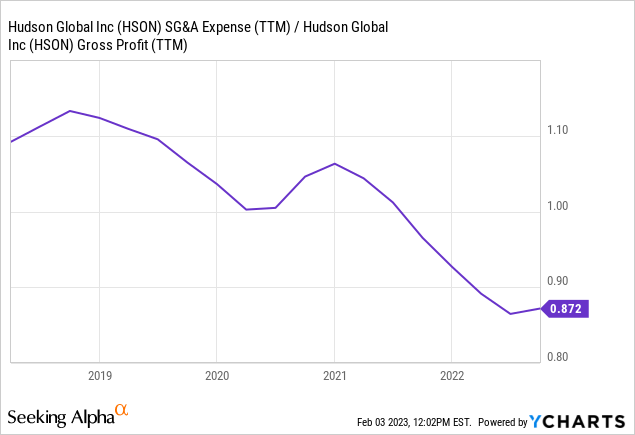

The strategy works: Since the company completed its strategic shift in 2018, revenues and profitability have grown substantially. Particularly important for these companies is the control of SG&A expenses, so that they do not eat all of the profits generated by new business.

Possibly accretive and conservative acquisitions: With a managerial team that comes from investment management, HSON has engaged in acquisitions that seem accretive and conservative. These have been directed toward smaller and localized RPO operations.

In 2020, the company acquired Coit Staffing, an RPO provider in the San Francisco area, related to the IT vertical. HSON paid $4 million for the company in 2020, and generated $11 million in sales from it in FY21.

In 2021, the company acquired Karani, an RPO provider from India with clients in the U.S. The company was acquired for $8 million, and generated $800 thousand in net income in the 9M22 period.

In the 3Q22, the company also acquired HnB, another Indian RPO, this time with local customers, for $1 million.

Although these acquisitions are still young, their sales and earnings multiples seem accretive. They have been conservative because of their size compared with HSON’s size and cash reserves, and because they have been financed internally.

Geographically diversified: More than 90% of HSON’s revenues are generated in Australia, the U.S. and the U.K., in that order. In FY21, Australia represented almost 65% of revenues.

A strong balance sheet: HSON has $1.3 million in debts against cash reserves of $22.5 million. The company is very well positioned to resist a downturn in business, and also to engage in opportunistic acquisitions.

Massive NOLs: HSON has carried enormous NOLs from its previous business operations, as much as $360 million, which could eventually represent as much as $70 million in income tax savings.

Antitakeover rights: Supposedly in order to protect the NOLs from expiring under a change of control, HSON has issued rights that are traded with the common shares and that allow shareholders to purchase one preferred unit for $3.5 per right, with the same rights as common shares.

Further, an investor with more than 5% of shares who tries to double his stake in the company without authorization from the Board, would automatically lose these rights and trigger the rights activation. The effect would be to almost automatically dilute the incumbent shareholder, while more or less leaving the rest of the shareholders in the same situation as before the rights activation.

These clauses have the effect of blocking any attempt to take over the company without Board authorization. The rights will eventually be cancelled if the company either uses up or decides not to use its NOLs.

Customer concentration: HSON claims to work for mid and large cap multinational corporations. The company has significant customer concentration, with three customers accounting for 66% of revenues in FY21, and two of them accounting for 65% of revenues in FY20.

High managerial compensation: For a company of HSON’s size, its managerial team is compensated excessively, in my opinion. The CEO made $1.25 million in FY21, with another $750 thousand for the CFO.

Recent developments

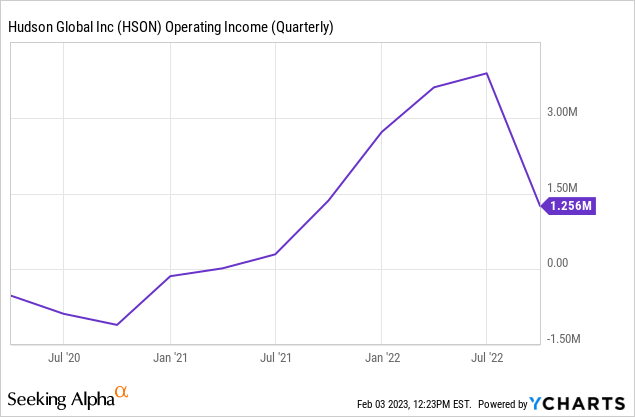

The dark side of operating leverage: The company was able to generate record revenues of more than $50 million in 1Q22 and 2Q22. These translated into operating income above the $3 million mark, per quarter.

However, a relatively small fall of revenue to the $48 million level more than halved operating income in 3Q22. According to the company, the fall was caused by a decrease in hiring in the IT vertical. This relatively small revenue setback showed the company’s operational leverage dark side.

The effects of a strong dollar: With only 25% of revenues coming from the U.S., HSON is exposed to foreign exchange rate volatility. For most of FY22, the dollar strengthened against the currencies of other developed markets, like the British pound or the Australian dollar. On a constant currency basis, HSON revenues are growing at twice the speed of its non adjusted revenues.

Valuation

Positive scenario: If the company is able to return to the previous revenue levels, it could generate more than $12 million in operating income. Without meaningful interest expenses, and lower taxes in the U.S. because of NOLs, this could easily translate into at least $9 million in net income.

Negative scenario: HSON showed revenue resilience even during the pandemic (the Coit Staffing acquisition was carried in October, so FY20 revenue was organically stable). If HSON operated at the level of 3Q22, HSON could generate some $6 million in operating income, and close to $5 million in net income.

Quality business premium: I believe HSON deserves a premium on quality over average earnings generation capacity. This premium is predicated on revenue resilience, consistent bottom line growth, control over costs, significant cash reserves, a managerial team with capital allocation experience, and geographic diversification.

Conclusions

Trading at a market cap of $70 million, HSON offers a low P/E ratio of 7.5x to a positive scenario, and a higher ratio of 14x to the more negative scenario.

Although I generally do not like ratios as high as 14x, and do not count on revenues growing significantly, I believe HSON justifies a quality premium, and that its revenues have shown to be resilient.

For those reasons, I believe HSON is an opportunity at current prices.

Editor’s Note: This article covers one or more microcap stocks. Please be aware of the risks associated with these stocks.

Be the first to comment