Justin Sullivan/Getty Images News

HP Inc. (NYSE:HPQ) returned -17.4% (including dividends) over the last 12 months, slightly outperforming the computer hardware industry as a whole (total return of -19.0%, as tracked by Morningstar). The COVID years, with people working from home and many children having online school, saw a surge in sales of personal computers. The market for PCs is returning to more normal conditions, putting downward pressure on HPQ’s sales. HPQ had a 29% decline in the worldwide number of PC shipments in Q4 of 2022 vs. Q4 of 2021. The outlook for PC sales in 2023 indicates further declines across the industry.

Thanks in large part to the earnings windfall in the past several years, HPQ’s trailing 3-year total return is 12.1% per year, much higher than that of the computer hardware industry (4.7% per year), the S&P 500 (SPY, 8.5% per year), and the NASDAQ 100 (QQQ, 9.7% per year) over the same period.

Seeking Alpha

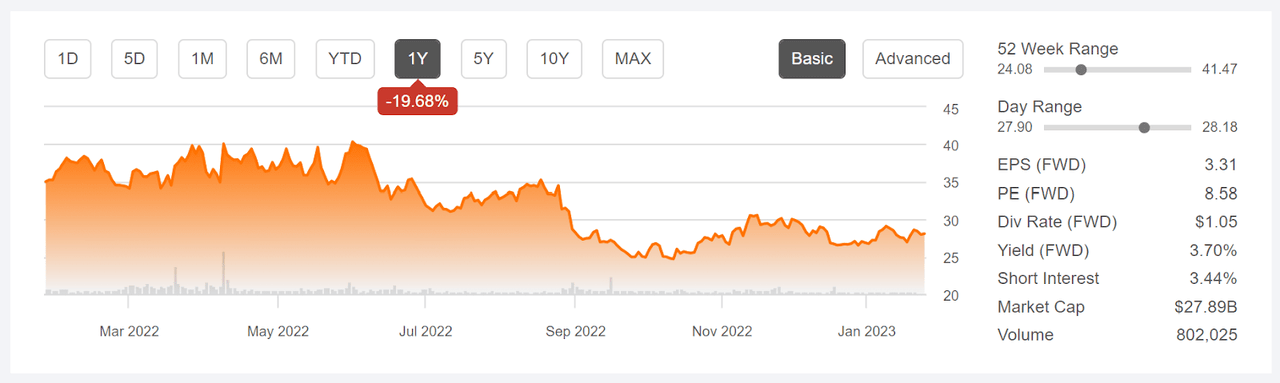

12-Month price history and basic statistics for HPQ (Source: Seeking Alpha)

HPQ reported Q4 FY 2022 results on November 23, 2022. Net revenue for the quarter was down 11.2% YoY (down 8% in constant currency). Net revenue for the full year was down 0.8% (up 0.7% in constant currency). For 2022, the company had $44.1 Billion in net revenue from the Personal Systems side of the business (PC’s, laptops, handheld devices) and $18.9 Billion from printing. Total net revenue for the year was $63 Billion. The company spent $5.3 Billion on share buybacks and dividends for FY 2022 (all values are in the Q4 slide deck).

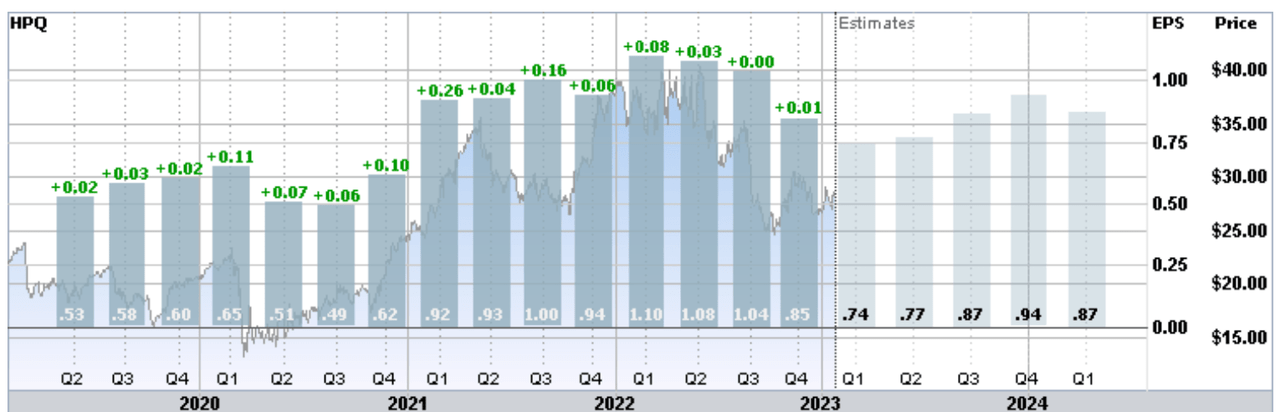

HPQ has grown earnings substantially over the past 4 years, although much of this growth has been a temporary phenomenon due to the COVID-driven spike in PC sales. According to ETrade, the consensus expected EPS for 2023 is $3.31 per share, as compared to $4.08 in 2022. The expected EPS growth rate over the next 3 to 5 years is 0.75% per year.

ETrade

Trailing (4 years) and estimated future quarterly EPS for HPQ. Green (red) values are amounts by which EPS beat (missed) the consensus expected value

HPQ has trailing 3-, 5-, and 10-year dividend growth rates of 15.5%, 13.5%, and 15.8% per year, respectively. The payout ratio is 24.6%. With the current valuation (forward P/E of 8.6 and TTM P/E of 7.0) and the low payout ratio, there is no reason to think that the company will slow down on the rate of dividend growth going forward. It is worth noting that the forward P/E is not especially low compared with historical levels, however, so the shares don’t look undervalued.

I last wrote about HPQ on May 17, 2022, more than 8 months ago, when I assigned a hold / neutral rating. At that time, the Wall Street consensus rating was a hold, and Seeking Alpha calculated a consensus 12-month price target that was 5% below the share price. The basic narrative was largely the same as it is today, with the market trying to price in the expected drop in earnings after the COVID run up. The market-implied outlook, a probabilistic price forecast that represents the consensus view from the options market, was neutral with some signs of a slight bearish tilt. The expected volatility was somewhat high, at 40% (annualized).

Seeking Alpha

Previous post on HPQ and subsequent performance vs. the S&P 500 (Source: Seeking Alpha)

I noted that selling covered calls could provide a high level of income and I executed a covered call position on the day that I submitted the post. I purchased HPQ for $39.16 and sold call options with a strike price of $40, expiring on January 20, 2023, for $4.43. Now that these options have expired, we can look at how things turned out. On January 20, HPQ was trading at around $27, so the options expired worthless. HPQ’s total return (including dividends) from the close on May 17th to the close on January 20, 2023 was -27.8%. The total return for the covered call position (long the shares, short the call) was -16.4%. Selling the call options partly offset the losses from owning HPQ over this period.

For readers who are unfamiliar with the market-implied outlook, a brief explanation is needed. The price of an option on a stock reflects the market’s consensus estimate of the probability that the stock price will rise above (call option) or fall below (put option) a specific level (the option strike price) between now and when the option expires. By analyzing the prices of call and put options at a range of strike prices, all with the same expiration date, it is possible to calculate the probable price forecast that reconciles the options prices. This is the market-implied outlook. For a deeper discussion than is provided here and in the previous link, I recommend this outstanding monograph published by the CFA Institute.

I have calculated updated market-implied outlooks for HPQ and I’ve compared these with the current Wall Street consensus outlook in revisiting my rating.

Wall Street Consensus Outlook for HPQ

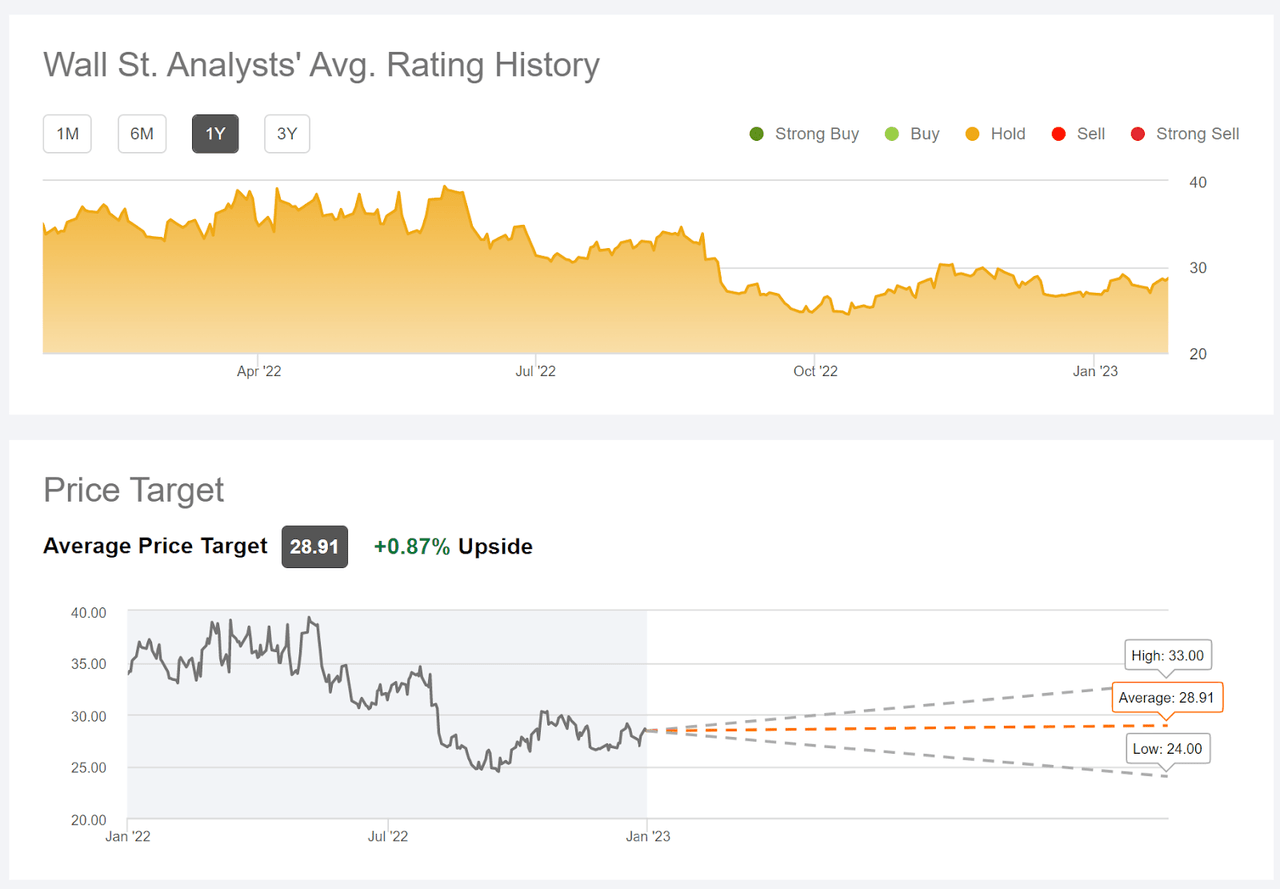

Seeking Alpha calculates the Wall Street consensus outlook for HPQ by aggregating the views of 17 analysts who have published price targets and ratings in the last 90 days. The consensus rating continues to be a hold, as it has been for all of the past year. The consensus 12-month price target is 0.87% above the current share price. The highest analyst price target from this sample is 14% above the current share price.

Seeking Alpha

Wall Street analyst consensus rating and 12-month price target for HPQ (Source: Seeking Alpha)

The consensus price target for HPQ was between $36 and $37 from the start of 2022 through most of August, but declined following the Q3 earnings report on August 30th. The reduced price target reflects the accumulating data in 2022 that showed a major slowdown in global PC sales, as well as falling quarter-on-quarter earnings for HPQ.

Market-Implied Outlook for HPQ

I have calculated the market-implied outlook for HPQ for the 4.6-month period from now until June 16, 2023 and for the 11.7-month period from now until January 16, 2024, using the prices of put and call options that expire on these dates. I selected these specific expiration dates to provide a view to the middle of 2023 and through the entire year.

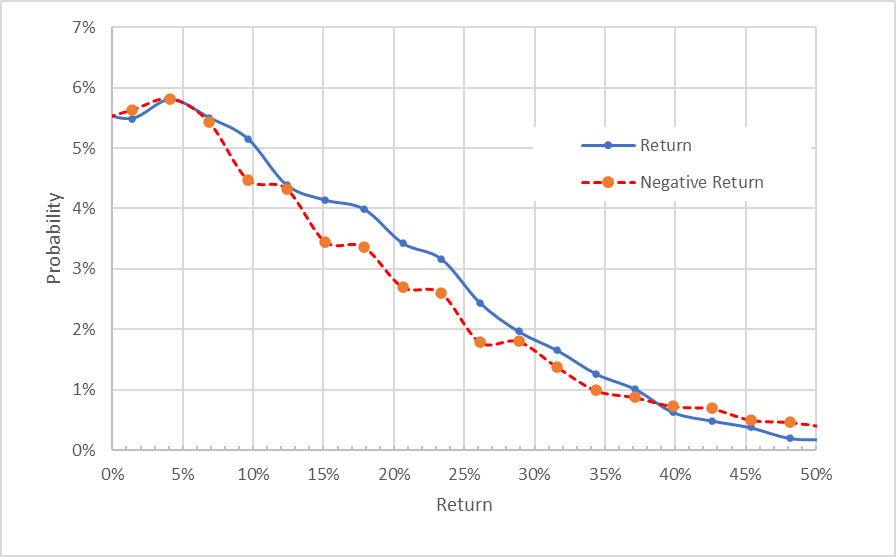

The standard presentation of the market-implied outlook is a probability distribution of price return, with probability on the vertical axis and return on the horizontal.

Geoff Considine

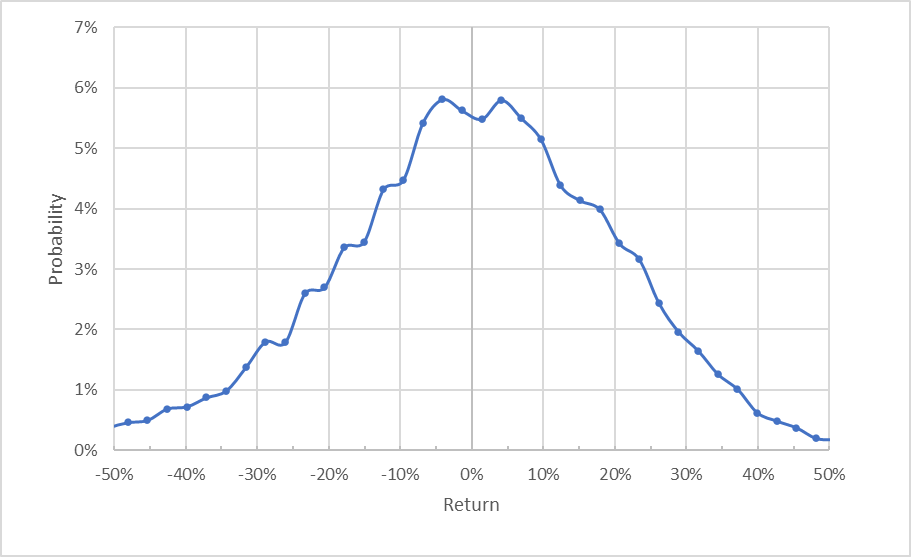

Market-implied price return probabilities for HPQ for the 4.6-month period from now until June 16, 2023 (Source: Author’s calculations using options quotes from ETrade)

The market-implied outlook to the middle of 2023 is generally symmetric, with comparable probabilities of positive and negative returns of the same magnitude. The expected volatility calculated from this distribution is 32.7% (annualized), much lower than the value in May (40%).

To make it easier to compare the relative probabilities of positive and negative returns, I rotate the negative return side of the distribution about the vertical axis (see chart below).

Geoff Considine

Market-implied price return probabilities for HPQ for the 4.6-month period from now until June 16, 2023. The negative return side of the distribution has been rotated about the vertical axis (Source: Author’s calculations using options quotes from ETrade)

This view shows that the probabilities of positive returns are consistently at or above those of negative returns of the same size, across a wide range of the most-probable outcomes (the solid blue line is on or above the dashed red line over almost all of the left ⅘ of the chart above). This tilt in probabilities suggests a moderately bullish view from the options market.

Theory indicates that the market-implied outlook is expected to have a negative bias because investors, in aggregate, are risk averse and thus tend to pay more than fair value for downside protection. There is no way to measure the magnitude of this bias, or whether it is even present, however. The expectation of a negative bias reinforces the bullishness of the market-implied outlook to the middle of 2023.

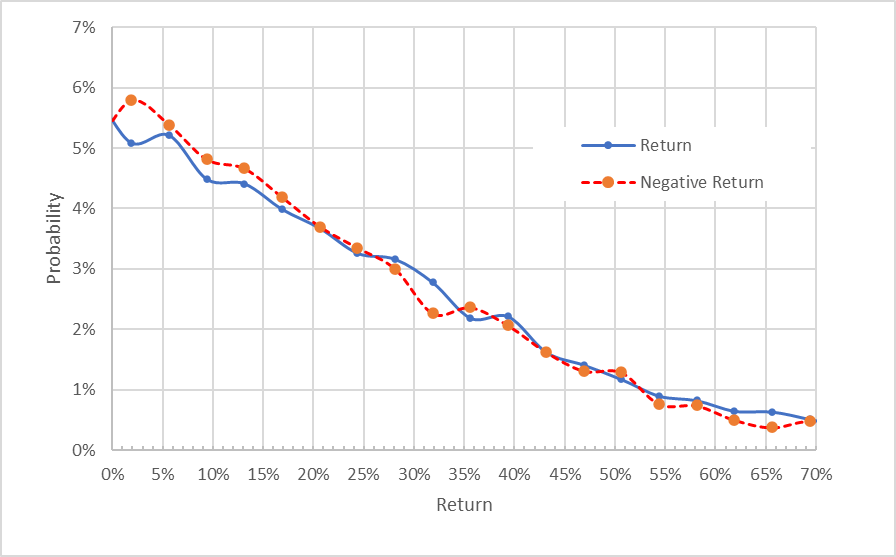

The outlook to January 19, 2024, calculated using options that expire on this date, exhibits a very close match between the probabilities of positive and negative returns (the solid blue line and the dashed red line are almost on top of one another). If there was no negative bias, this chart would indicate a neutral view. With the expectation of a negative bias, this market-implied outlook is slightly bullish. The expected volatility calculated from this distribution is 31.9% (annualized).

Geoff Considine

Market-implied price return probabilities for HPQ for the 11.7-month period from now until January 19, 2024. The negative return side of the distribution has been rotated about the vertical axis (Source: Author’s calculations using options quotes from ETrade)

The market-implied outlook to the middle of 2023 is moderately bullish, and the outlook into January of 2024 is slightly bullish.

At the time that I pulled options quotes today, HPQ was trading at $28.47 and the bid price of a call option with a strike of $30, expiring on January 19, 2024, was $2.91. Adding this option premium to the $1.05 in expected dividends over this period, the total income yield is 13.9% over the next 11.7 months. This net position sacrifices all but 5.4% of the potential upside from price gains over this period. For investors who believe that HPQ is fundamentally sound but agree with the consensus outlook for stagnant earnings, this covered call position looks very reasonable.

Summary

HP Inc. is coping with a global decline in PC demand that is expected to continue. On the positive side, the valuation is quite low, the dividend yield and growth rates are quite high, the payout ratio is modest, and management continues to favor share repurchases. Until demand for PCs rebounds, earnings will be stagnant or lower. The Wall Street consensus rating is a hold, with a 12-month consensus price target that corresponds to a total return of 4.57% over the next year. The market-implied outlook is moderately bullish to the middle of 2023 and slightly bullish for the full year, with expected volatility of about 32%. Taking all of this together, I am maintaining a neutral/hold rating on HPQ. For those who own HPQ, selling covered calls is worth considering as a way to buffer potential share price declines.

Be the first to comment