marchmeena29/iStock via Getty Images

Waste Management, Inc. (NYSE:WM) is a large, publicly traded waste management conglomerate that is focused on providing environmental solutions to meet the growing demand for sustainable waste management services. As a leader in the industry, WM provides a wide range of services from waste collection and disposal to recycling and sustainability programs. In its most recent financial quarter, WMI posted strong financial results and has continued to demonstrate growth and profitability in the years leading up to this quarter. But a range of headwinds may finally result in a correction in the fourth quarter, and the current trading patterns confirm as much.

A Strong Quarter Despite Inflationary Headwinds

The most recent quarter for WM was especially noteworthy, as the company reported a net income of $639 million, up from $587 million in the quarter before. This represents a 1.08% increase in net income, which is a testament to the company’s ability to effectively manage its operations. Additionally, Waste Management reported a to-this-month (TTM) revenue of $19.4 billion, up from $17.9 billion in the same period one year ago, which represents an increase of 9%, and is an impressive achievement considering the broader economic headwinds, and the industry being relatively old. Looking ahead to the next financial quarter, Waste Management is expected to see some headwinds. In order to manage the headwinds, the company is expected to focus on expanding its services and offerings, while maintaining cost control. Commercial price strength continued to be a key driver of revenue in 2022, increasing by 9-11% depending on the segment, and this allowed the company to offset some of the increasing costs. But questions surrounding costs stemming from an impairment, and other tax liabilities bring into question whether the stock will remain at the current levels.

WM Investor Presentation

Fourth Quarter Issues

Adding to the woes, things could be challenging due to the rising cost of raw materials, labor, and energy, which have been affected due to increasingly stubborn inflation. Inflation is the primary concern that management has outlined, and despite Waste Management’s history of strong execution and cost control, margins for the company are under pressure once again. Having said that, despite the headwinds, EBITDA grew by 12% for the latest quarter and margins grew by 60 basis points. Inflation in the waste management industry tends to be more stubborn and has a higher propensity to affect operational costs, due to the importance of both capital and labor costs. Part of the reason that the company is not facing rising costs is that it is on track to reduce headcount by 7,000 personnel for the fiscal year. This allows for margins to continue to expand at a time when salaries are expected to rise by around 9%. Annual EBITDA was around $5.4 billion to this month. In order to mitigate some of the issues that will carry over from 2022, in 2023 Waste Management is increasing the use of automation and robotics. Many waste processing facilities now employ robots to sort through trash, separating recyclable materials from non-recyclable items. This not only increases the efficiency of the waste sorting process but also reduces the need for manual labor, improving working conditions for employees.

In addition to cost control, WM is also looking to expand its services and offerings in order to remain competitive and grow its customer base. The company is currently investing in new technologies and services such as waste-to-energy solutions, recycling programs, and other green initiatives. These investments will help WM stay ahead of its competitors and continue to meet the changing needs of its customers. The company continues to invest in its $1.65 billion sustainability program, out of which it will invest 550 million in 2022. Furthermore, the company is expected to bring online 17 new RNG projects and five new automated material recovery facilities during the fourth quarter. Management has projected that the renewable gas projects will add another $400 million in EBITDA by 2026, and these are conservative estimates.

Finally, WM is also looking to improve its customer service. The company has recently announced plans to invest in new customer services initiatives, such as online customer support and mobile applications. This will help the company better engage with its customers and ensure that its services are meeting the needs of its customers. Overall, Waste Management Inc. is well-positioned to continue its successful trend of growth and profitability in the next financial year. The company is making significant investments in new services and technologies, while also maintaining cost control and improving customer service. These strategies should enable WM to remain competitive and remain a leader in the waste management industry.

Management has outlined that a number of headwinds could bring the final year EBITDA to around $5.5-5.6 billion for the fiscal year, and would mean that forward P/E currently stands at around 25-26x. Investors will look to the company with a lot of scrutiny despite being in an industry that is relatively recession resistant. The current dividend, which stands at 1.6%, and with the prospects for growth in 2023 being relatively flat, and estimates of revenue growth ranging anywhere from 6-8%, the company is not likely to see any major benefit from bottom-line expansion during the fourth quarter. In turn, this means the stock could also remain relatively flat for the foreseeable future, that is if the results don’t cause a correction. Cash flow has also come down slowly during the year to $1.7 billion down from $2.4 billion in the previous year, additionally, the total cash on books continues to be relatively low at close to $200 million, and although there are no expected working capital problems, the company is not likely to increase dividends anytime soon. Therefore, investors may not be as forgiving of low dividends, as they were historically.

Technicals Are Showing Headwinds

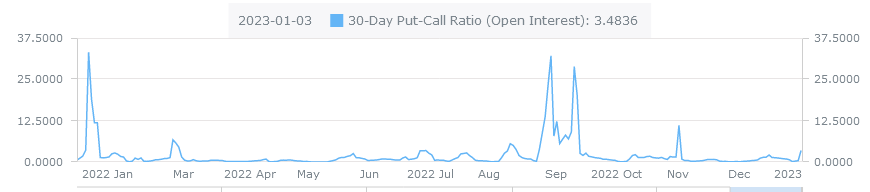

Technicals currently show that investors are firmly bullish on the stock with a put-to-call ratio of 0.38, and firmly on the side of bulls, but recently large bets were placed that sent the put-call ratio to above 3 showing that an investor might be betting on a 4th quarter impairment, which sends the stock lower. The large bet when combined with relatively low implied volatility, and low beta means that someone is clearly expecting the stock to decline to the lower end of the support channels.

Alpha Query

Finally, the fourth quarter could be a bit of a blip in terms of results and how the stock trades, while Waste Management has not seen any significant headwinds in terms of revenue, the market is clearly indicating that it believes things will slow down, so if the thesis pans out, the stock could correct 10%. But if things continue according to the current trend, then the stock is likely to remain mostly flat, making for an interesting short-term trading outlook.

Be the first to comment