jfmdesign/iStock Unreleased via Getty Images

Hormel Foods Corporation (NYSE:HRL) develops, processes, and distributes various meat, nuts, and other food products to retail, foodservice, deli, and commercial customers in the United States and internationally. The firm has released its latest quarterly results on the 30th of May, and for this reason, the aim of our article today is to give an updated view on the business, its financial performance and our expectations about the near/mid term.

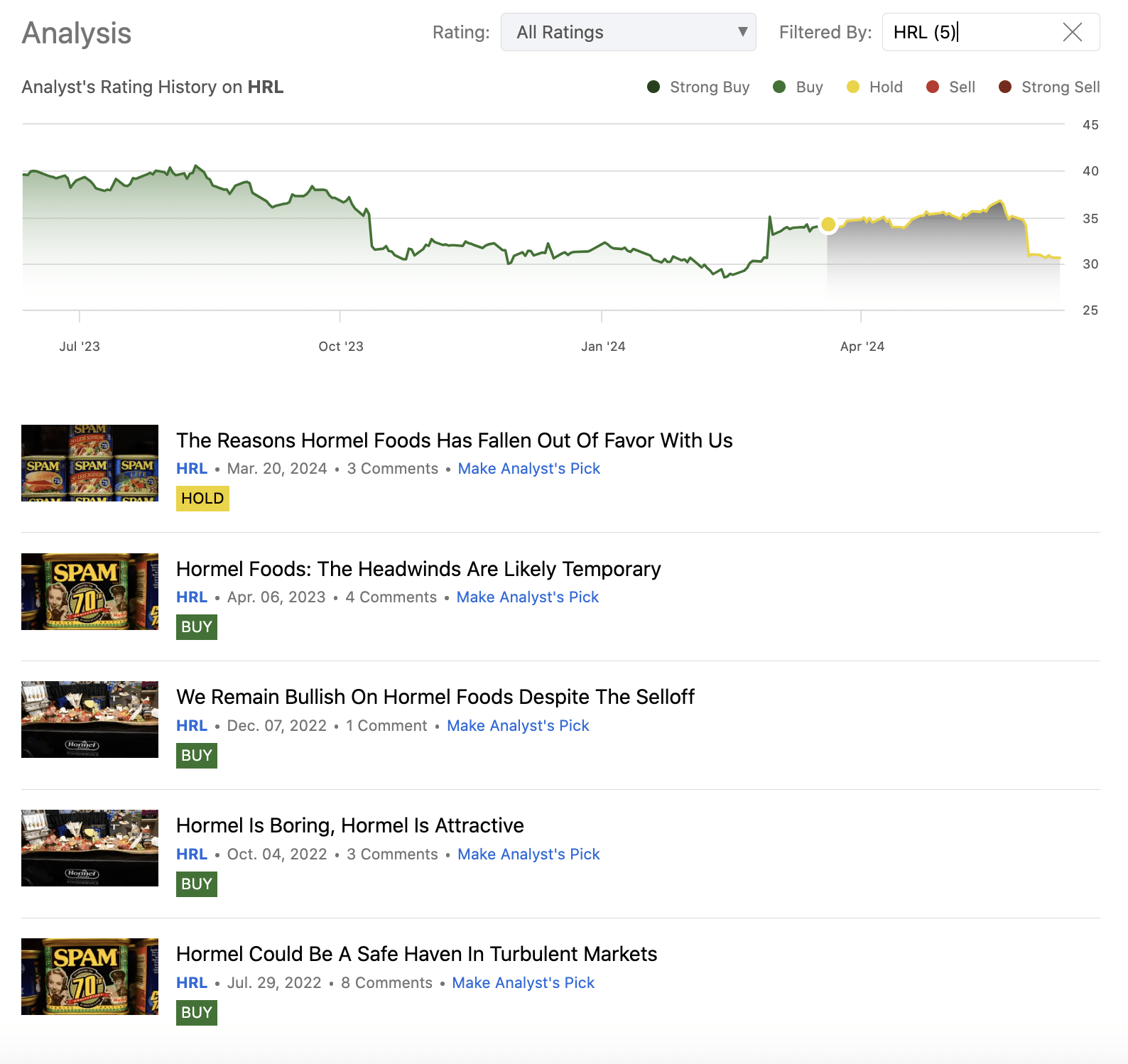

We have started cover of the firm with a “buy” rating in July 2022, citing the company’s relative independence from consumer sentiment, as well as its steadily growing dividends as attractive factors. We have kept/reiterated this rating several times, up until March 2024, when we have turned slightly more bearish and assigned the company a “hold” rating. The reason for our downgrade has been the gradual decrease in profitability over the past five years and the valuation metrics – a set of traditional price multiples – indicated limited upside potential.

Analysis history (Author)

Year-to-date, the stock price performance has also not been particularly outstanding, significantly underperforming the broader market.

Let us look at the firm’s quarterly earnings results and try to assess, whether this underperformance is likely to last in the coming months/quarters or not.

Earnings highlights

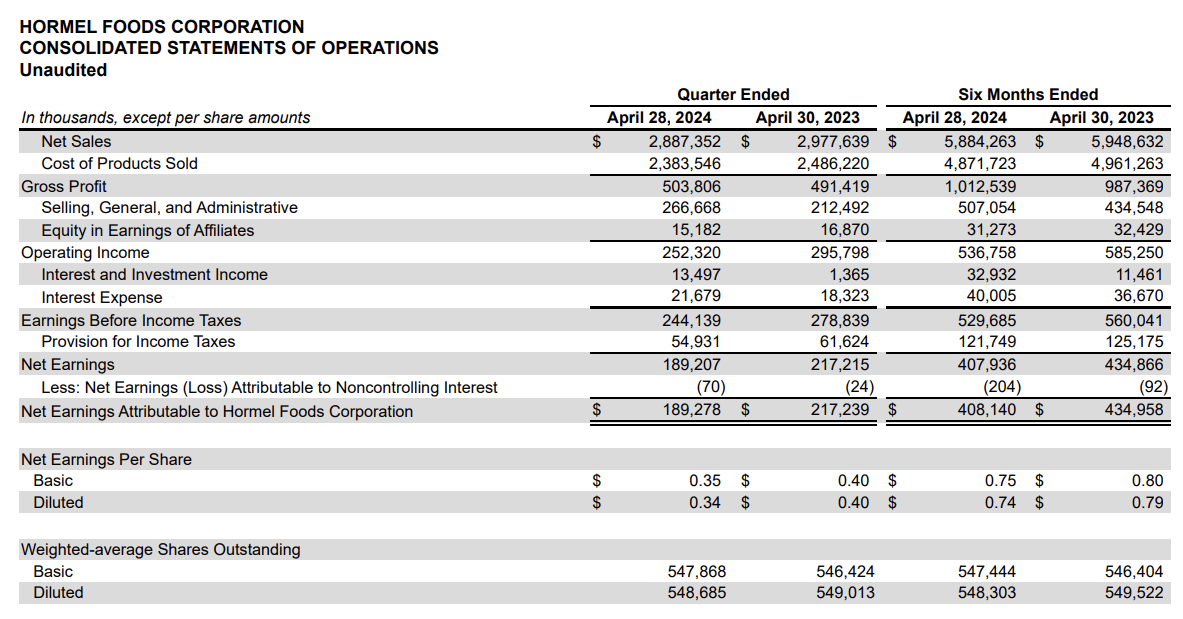

HRL has managed to beat EPS estimates in the previous quarter by as much as $0.02 per share, while revenue has come in $80 million below the $2.89 billion analyst estimate. While it may appear positive at first that the firm has beaten the EPS estimates, we believe that the results are not so rosy when we look closer. Volumes as well as net sales have declined, not just in the past quarter, but in the first six months too.

Income statement (HRL)

The operating income has fallen by roughly 15% from $296 million to $252 million, year over year. The development of the operating margin is also not too appealing. It has contracted by 120 bps from 9.9% to 8.7%. Last, but not least, EPS has also decreased by as much as 15%, compared to the same period in the prior year.

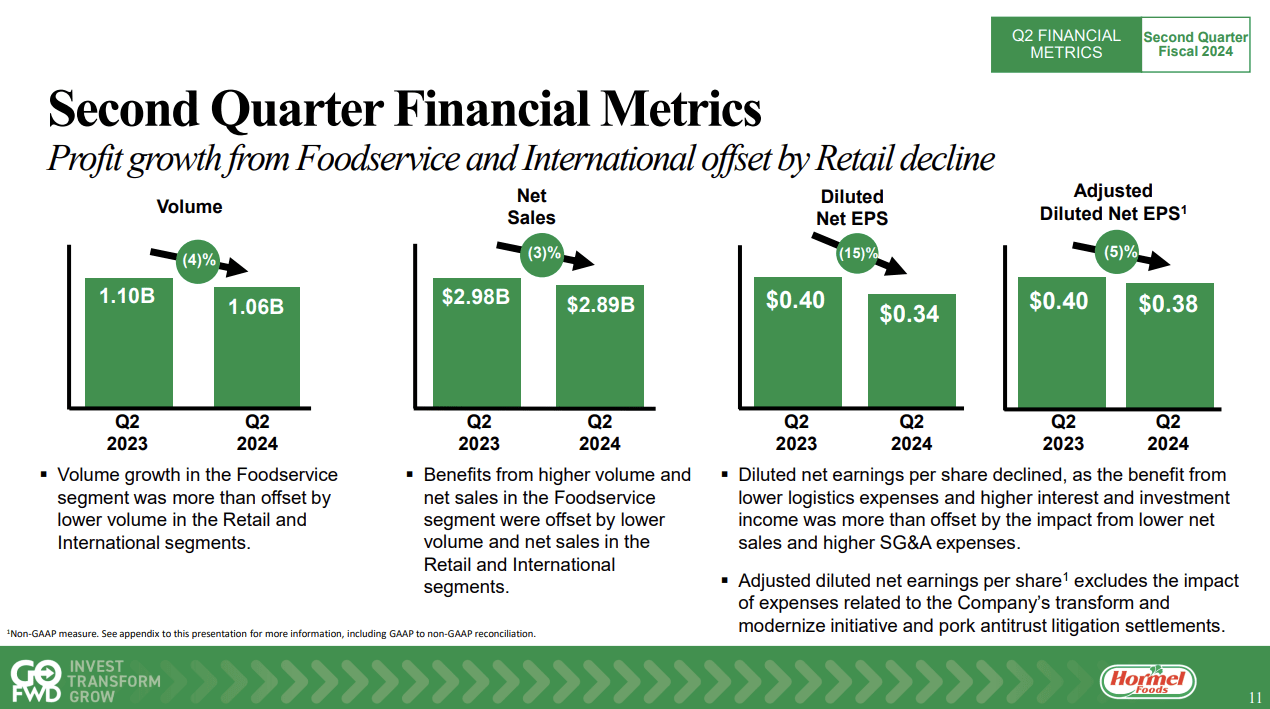

Let us now look at the segment results to understand, what exactly has been driving the firm’s performance lower.

Financial Metrics (HRL)

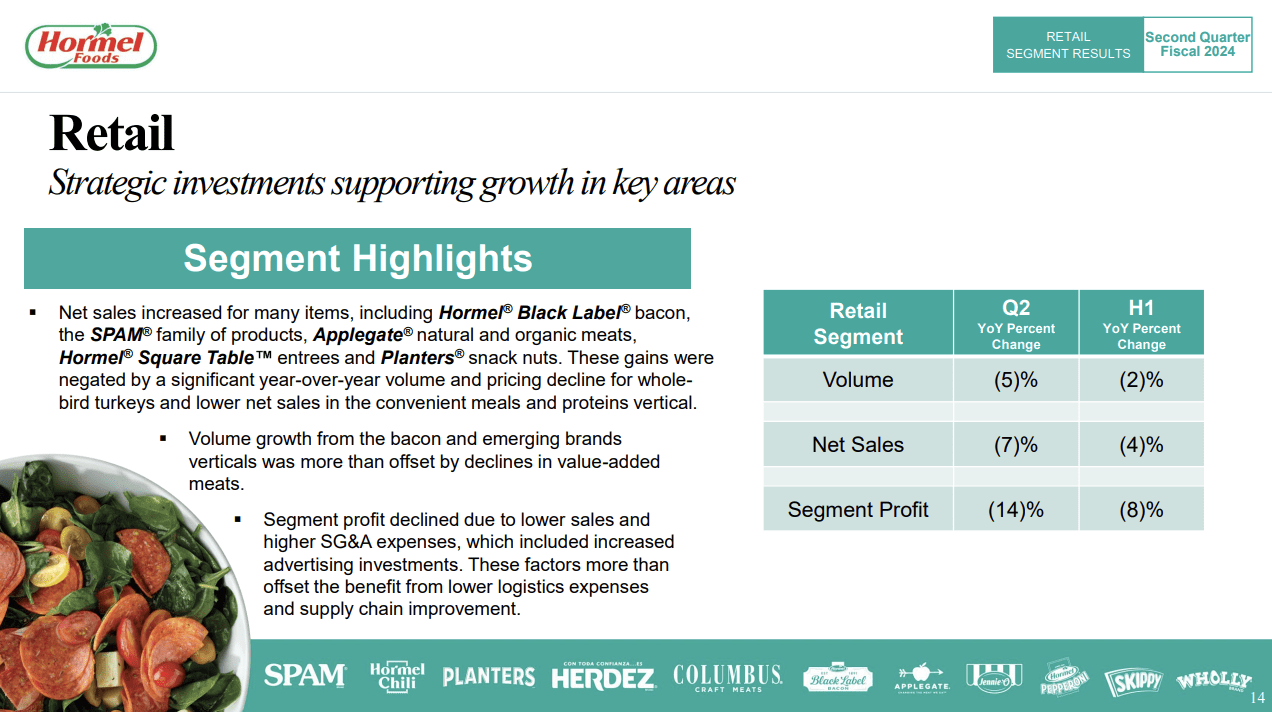

Retail

The firm’s retail segment has been one of the key drivers of the poor performance. Both volume and net sales have declined by 5% and 7%, respectively. Segment profit has fallen by as much as 14%. Important to mention that several items have contributed positively to the sector performance, including the increased net sales of Hormel Black Label bacon, the SPAM family of products, Applegate natural and organic meats, Hormel Square Table entrees and Planters snack nuts. Unfortunately, these have been more than offset by the poor performance of the value-added meats, including the declining price and sales of whole-bird turkeys and the lower net sales in the convenient meals. On the expense side of the equation, the picture is also not brighter. While logistics cost have decreased and supply chain has improved due to the improving macroeconomic environment, higher SG&A expenses have more than offset these benefits.

Retail (HRL)

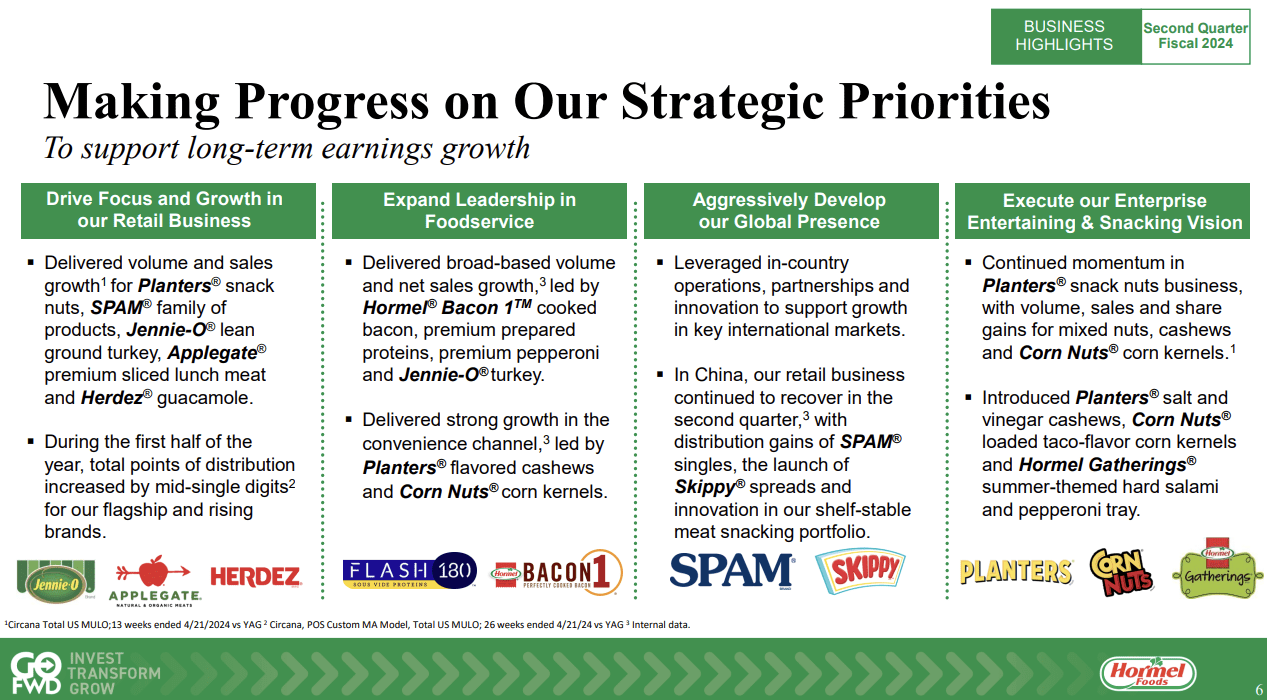

These results, however, indicate one important thing. Hormel is delivering on its long term strategic initiatives. They are aiming to focus on certain brands in their retail portfolio and these brands have actually showed increased sales volume. We cannot forget, however, that it has been potentially driven by the heavy advertising and the main question is, will this momentum last after the advertising spending is lowered?

Strategic priorities (HRL)

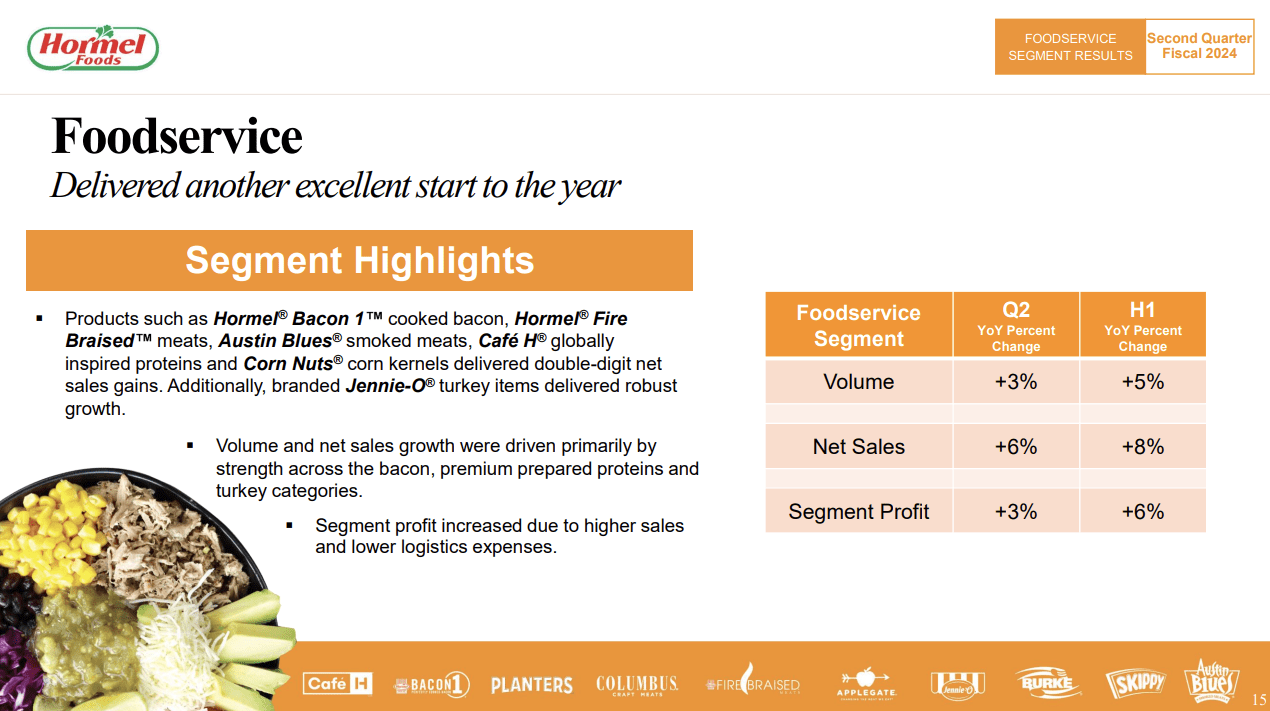

Foodservice

The Foodservice segment has been the strongest segment in the past quarter. Both net sales and volumes have increased by 6% and 3%, respectively. Segment profit has also improved by 3% compared to the same period in the prior year. The growth drivers have been the bacon, premium prepared proteins and turkey categories, in which some products have even exhibited double-digit sales growth. In this segment, the sales growth and the lower logistics expenses have been high enough to offset the higher advertisement expenses.

Food service (HRL)

Just like in the Retail segment, also in the Foodservice segment HRL is delivering on its long term strategic initiatives.

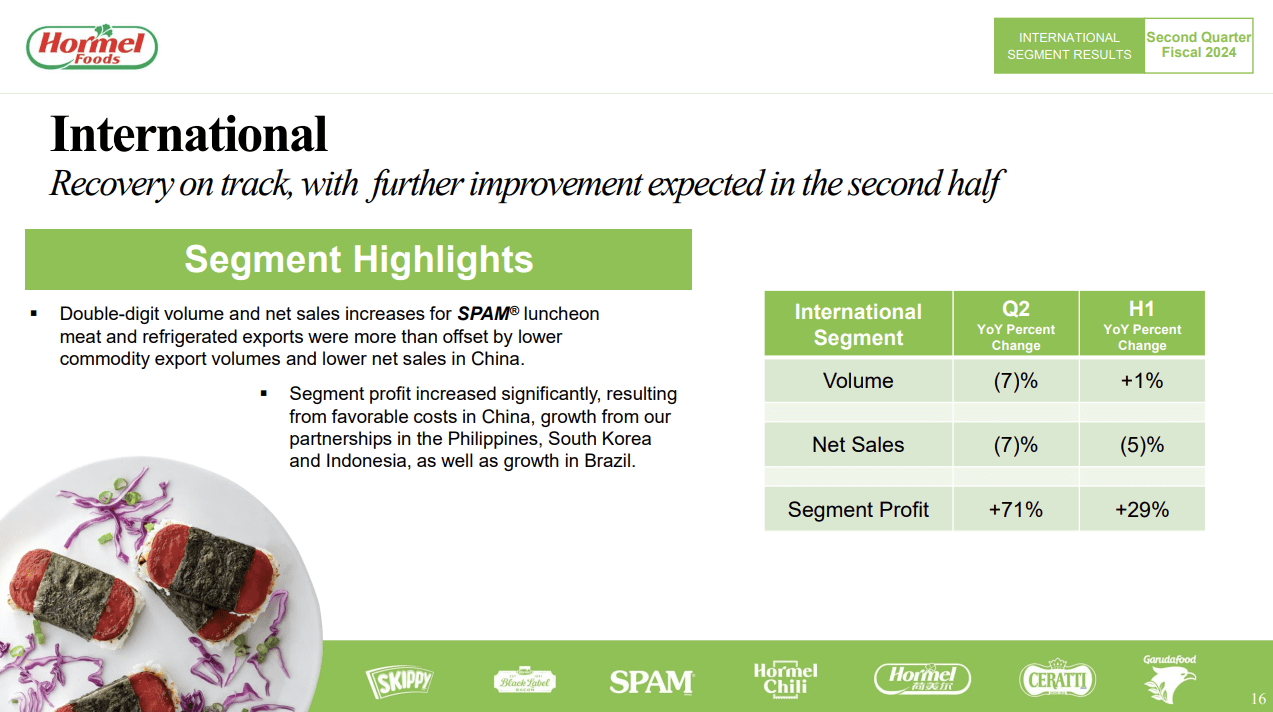

International

The International segment has shown significant decline in both volume and sales, 7% in each case. While the net sales of SPAM has been trending upwards, the lower sales in China and the lower commodity export volumes have more than offset the benefits. Despite the negative volume and sales trend, the firm has managed to increase its profit in the segment by a whopping 71%, driven by partnership growth in the Philippines, South Korea, Indonesia and Brazil.

International (HRL)

On top of the poor sales metric, in this segment, we are also not particularly satisfied with the progress of the firm’s strategic plan. While partnerships do appear to work based on the increased profit metric, the sales in China keep disappointing. We would like to see this trend change, before we could get bullish on this segment.

All in all, we believe that these results are not too appealing. Broad sales and volume declines indicate that the demand for the firm’s products is relatively weak and may be highly price sensitive. The lack of pricing power likely comes hand-in-hand with the lack of brand loyalty, which may explain why the firm needed to spend significantly higher sums on advertising in this quarter. For these reasons, we are not convinced that an investment in HRL’s business is an attractive one, based on the business performance.

Outlook

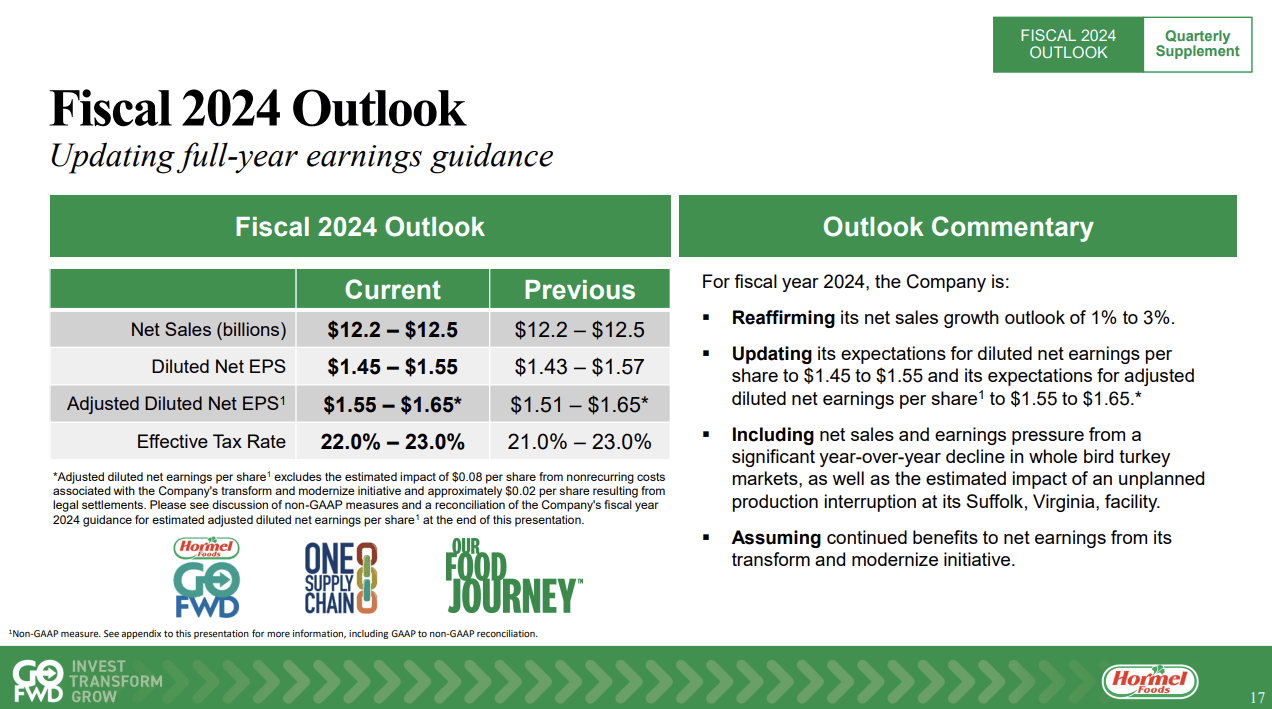

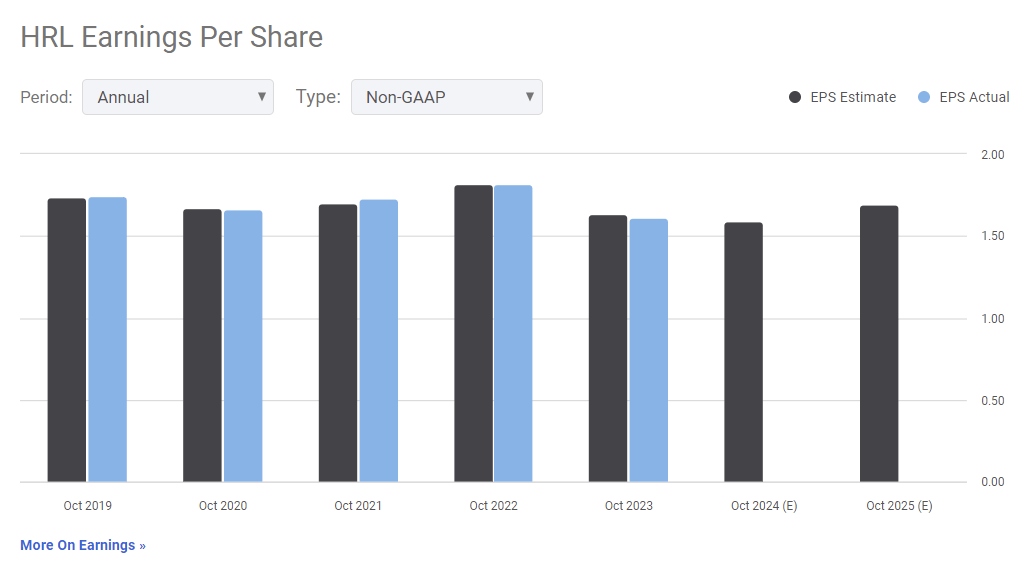

Looking forward, there is also not much to be optimistic about in the near term. The firm has largely left its outlook unchanged, although it slightly narrowed EPS and diluted EPS estimates. Regardless, EPS is still expected to decline in 2024, compared to the prior year.

Outlook (HRL) Estimates (SA)

Return to shareholders

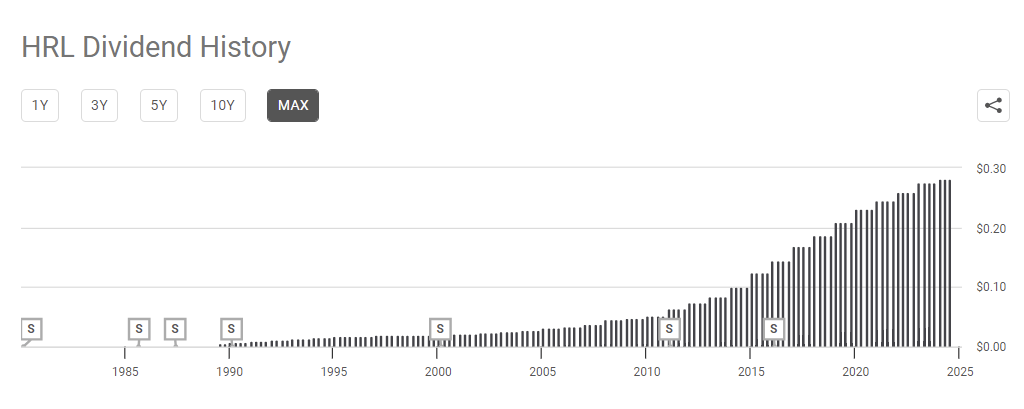

Last, but not least, we have to take a brief look at the return to shareholders, as one of our key arguments for our earlier bullish ratings have been the growing dividends.

Dividend history (HRL)

As of now, the firm remains a reliable dividend payer with consistently growing quarterly dividends. The firm’s payout ratio and cash flow from operations indicate that these payments are sustainable in the near term.

Conclusions

While HRL has topped EPS estimates in the prior quarter, the declining sales, volumes and earnings shed a negative light on the firm.

The execution of the firm’s strategic initiatives appear to be on track in the Retail and Foodservice segments, in which certain products have shown significant increases in both volume and sales. The International segment, however, has shown significant weakness in both sales and volume.

Increased advertisement spending has been necessary to achieve generate higher interest for certain product categories and the main risk at this point is that once the advertisement campaign runs out, the demand may start to diminish for these products.

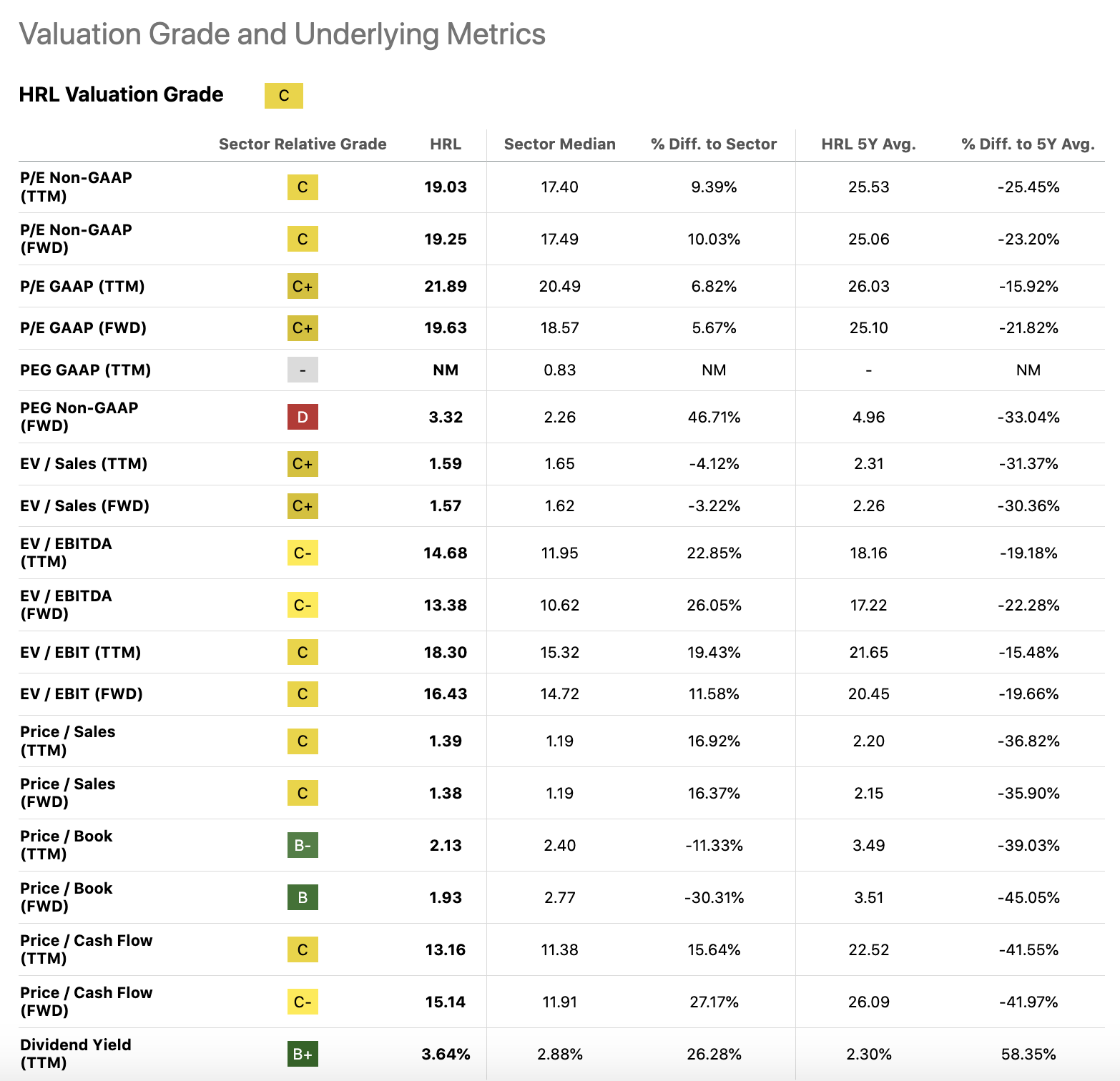

From a valuation point of view, we still see limited upside potential. The following multiples compare HRL’s valuation to its own historic valuation and also to the consumer staples sector median. While the firm appears to be selling at a discount to its own historic valuation, it is selling at a significant premium compared to the sector median. In our view, based on the firm’s financial performance, including shrinking margins, declining sales and declining EPS, the discounted compared to the historic valuation is justified.

Valuation (SA)

For these reasons, we maintain our “hold” rating.

Be the first to comment