RelaxFoto.de

Dear readers/subscribers,

I’ve invested plenty in Scandinavian forestry and paper/pulp over the past decade – and done so profitably. Companies I’ve looked at are typically among the larger ones in Sweden, Norway, Finland, and other countries. Holmen AB (OTCPK:HLMMF) isn’t the largest, but it’s a solid one with plenty of things to like about it.

In this article, which I frankly don’t expect many of you to read given how small and niche of a company we have here, I’m going to present you with a thesis for this company.

What is Holmen?

Holmen is a Swedish forest, timber, and paper/pulp company. It was previously known as Mo och Domsjö AB, which can trace its roots all the way back to 1873, meaning the company has a close-to 150-year history. It’s a company where 90% of the business is done in Europe through its own paper and product sales companies and subsidiaries.

The company is majority-controlled by the Swedish magnate Fredrik Lundberg, and his investment company L E Lundbergföretagen AB (OTCPK:LBGUF), which like the Wallenbergs, is a Swedish power company, albeit smaller than the Wallenbergs.

Holmen AB is a fully vertically-integrated forestry and paper products company.

It has over 3,000 employees, annual revenues of around 17B SEK, and assets of over 20B SEK. It’s small on a global basis, and on an American perspective, but large when we look at it from a Swedish perspective. The company has subsidiaries working in the energy sector, the timber sector, the paper sector, and the forest sector, in addition to specific subsidiaries such as Iggesund Paperboard AB, which is world-leading in the very high-end premium carton for luxury products, which was acquired by Holmen 2 years back.

The company is one of Sweden’s largest forest owners. Its current ownership comes to 1.3 million hectares of forest, with around 1 million of productive forest – so the company is self-sufficient in terms of raw materials for its input.

Holmen IR (Holmen IR)

The company, specifically, is in the following sectors:

- Forest, including ownership of forests, with annual net sales of over 6.5B SEK.

- Renewables, where it produces Hydropower. Holmen owns 21 hydropower plants in Sweden and is building wind power on the company’s own land, in addition to developing opportunities like real estate and quarries. The renewable segments have annual net sales of half a billion SEK and can produce 1,230 GWh on an annual basis.

- Wood Products, where the company refines wood for net sales figures of 4.8B on an annual basis. The company owns facilities and plants in Sweden, but also in England/UK.

- The Paperboard segment is the aforementioned Iggesund, which focuses on premium packaging for electronics, pharma, food, and cosmetics, with net sales of 6.6B per year.

- The company also has a traditional Paper segment, focusing on the production of legacy paper in its mills with annual sales of 5.4B SEK.

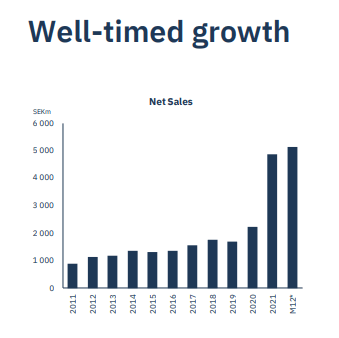

As you can see, the company is one of those “does-it-all” sorts of companies. If you’re thinking to yourself “This doesn’t sound bad”, you’re not alone. This is a very attractive mix of capabilities. While there is undoubtedly cyclicality to many of these business segments, the high-level returns over time for this company have been amazing. Holmen has been a great investment that for the past 18 years has delivered TSR of nearly 300%.

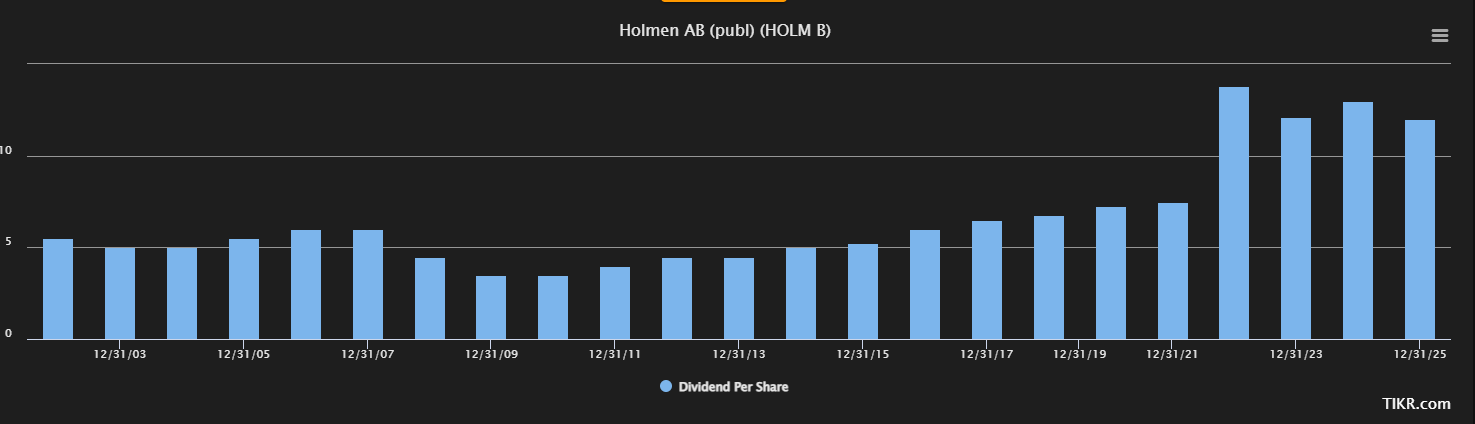

It’s not the highest yielder – only 1-3% traditionally, around 1.8% at today’s share price, but there’s some stability to it. It hasn’t been cut to zero at the very least.

Holmen Dividend (TIKR.com)

As a company with international businesses, Holmen has actually paid for an S&P Credit rating, and you may be surprised to learn that Holmen is actually BBB+ rated, which makes it the highest-rated paper/forest company that I cover. Even Finnish UPM (OTCQX:UPMKY) is at BBB, not at BBB+.

Holmen never rises above a 25% debt/equity ratio and the company has access to credit facilities of over 5BSEK for the foreseeable future.

So, it’s safe.

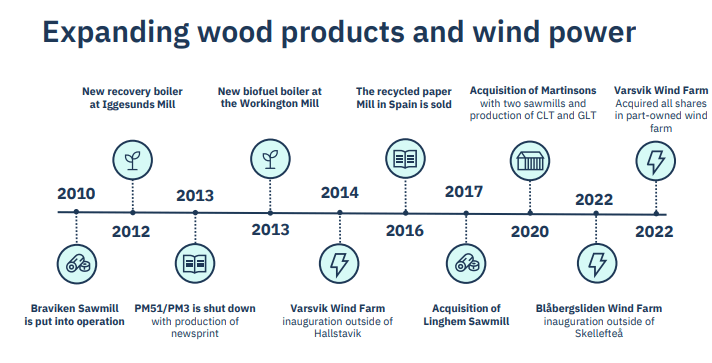

The company’s recent history is impressive…

Holmen IR (Holmen IR)

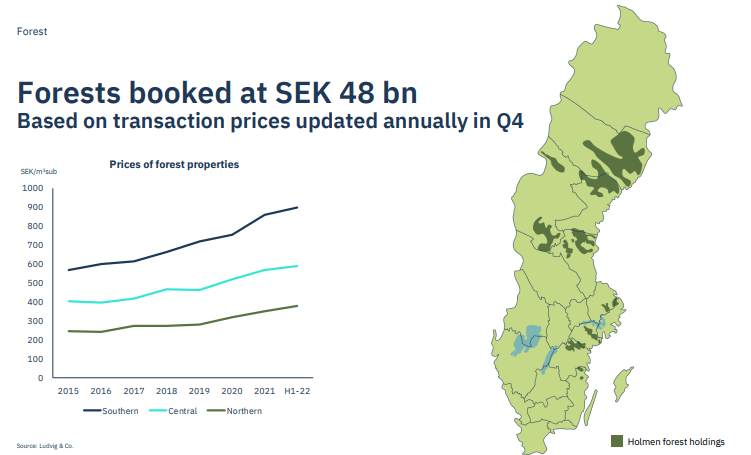

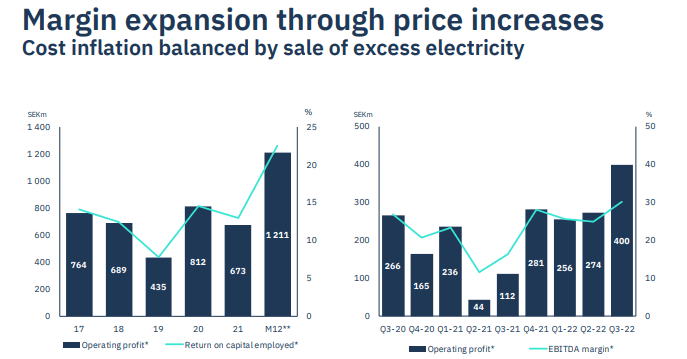

…and the company has been buying more and more land and forests over the past 10 years to secure its supply and reserves. Companies like this are in large part a play on timber pricing, and these prices have been rising as of late in line with inflation. Price increases in timber support ongoing profitability, and the company has been able to post operating profit of well over 1BSEK since 2017, with over 1.5B for the 2022E period. The company’s forests are worth around 48B SEK, and they are located in relatively attractive areas.

Holmen IR (Holmen IR)

The paperboard segment alone is a 550,000 tonne business on an annual basis, which already owns contracts with many high-end premium brands in the areas of liquors and luxury products – and the prices here have been increasing steeply due to inflation, supporting even margin expansion, and underbuilt by the fact that the company is mostly self-sufficient in terms of energy.

Holmen IR (Holmen IR)

As for the paper segment, you know that I am not a big fan of pure paper plays given the declining nature of the industry – but Holmen is managing the dial-down here fairly well, with deliveries at stable levels for the last 5 years.

Holmen is actually in a very good position, all things considered. Its own power supply means that its mostly insulated from the energy crunch – even profits from it due to the sale of surplus, and the paper shortage is pressing paper prices up, which is an advantage to a company like Holmen.

However, forget paper and paperboard for sales explosions – that’s where we find wood products.

Holmen IR (Holmen IR)

Even though this is likely to slow down given the construction cyclicality, there are plenty of positives in this segment, despite profit coming off its highs. Holmen is even considering capacity expansion – an entirely new sawmill at Rundvik in a JV with Swedish SCA (OTCPK:SVCBF). Housing accounts for 35% of the EU energy needs and building in wood stores carbon, which is an argument for the company and the company’s products.

With the Russian market closed off to most of the world, most of the wood in the world has to come from one of 3 areas – Sweden, Finland, and Canada. Oh, there’s wood in other regions – but these are the exporters of wood if we exclude Russia.

The company, as of the latest quarter, has a debt/Equity ratio of close to 5%, which makes Holmen one of the least indebted companies in this sector that’s publicly traded – in the world.

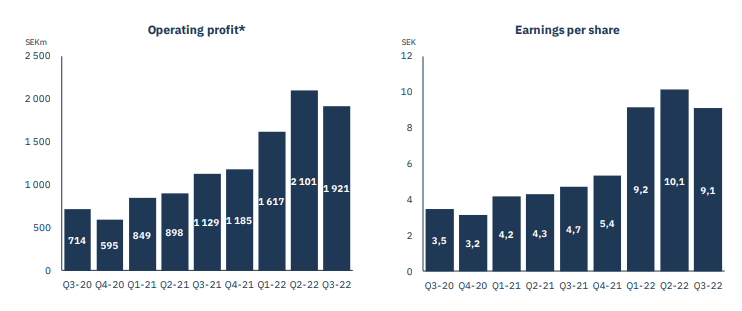

3Q22 results were great. Profits remain at absolutely record levels, arising from pricing power coupled with extreme cost control.

Holmen IR (Holmen IR)

I forecast, and analysts agree, similar trends as this cycle peaks, and I expect the company to remain absolutely solid going into the next downcycle for this segment, weighed up by the non-cyclical segments in the company, such as carton and paperboard (or at the very least less cyclical).

Why do I think this – let’s look at the company valuation here.

Holmen AB – The Valuation

I hope I have made a case for why Holmen is a company you may want to consider owning. It’s led by an extremely motivated and experienced majority shareholder who through his investment vehicle owns no less than 34.1% of the capital and 62.3% of the voting power.

It’s a trailblazer, mixing energy, with forests, with wood products, with paper, with carton, and high-end premium products, with its own sales subsidiaries. It’s the entire value chain.

Heck, if it owned its own shipping arm and used biofuel from its own trees, we could consider it more or less completely independent.

This also explains why the company tends to command a decent premium on the market, with a 10-year average P/E of 18.77x, which is significantly above the sector. At times, you could have picked it up under 10x, but the “right” time is around 15x or below, I’d say. That’s when you could start seeing double-digit upsides based on growth estimates of about 4-5% per year while taking into consideration the very solid foundation here.

The same pattern is true for other multiples – such as asset-based P/B, sales multiples, and the like. I would say that the company currently commands too high of a premium to be interesting here or to offer double-digit returns at a conservative level.

Street targets are high here. 6 companies follow the company, 2 of which are at a “BUY”, with ranges starting at 380 up to 520 SEK, and the average coming to around 448 SEK. Now, most of the analysts are admirably stable in their recommendations and targets on this company, but it’s been frequent that this business, based on these targets, has been overvalued by about 10-12% – which is exactly the sort of discount I apply to make sure we get it at an attractive level.

I wouldn’t “BUY” Holmen at above 380 SEK/share.

That’s also exactly why I sold the puts that I currently hold with February expirations at 380 SEK, which when including the premium, comes to a very attractive ~375 SEK investment level if the company drops down.

If it does not – well, I’ll get my 9.8% annualized yield, and I’ll likely try again – and I’ll have outperformed the yield by about 4x at least in the meantime.

It’s one of those companies I consider pretty easy to put valuations on – both when to “BUY”, and when to “SELL”.

At under 380 SEK, this company is to my mind a “Must-buy” for its stellar assets and upside as well as fundamentals. Once it hits 500 and above, it becomes “too hot”, and once it hits 550 SEK, you better run for the doors, because chances are high it’ll drop from here, barring something non-recurring.

At least, the way the company looks today.

So, my current thesis for the company looks like this.

Thesis

- Holmen is perhaps one of the best paper/forest/wood companies out there. Stellar credit, superb fundamentals, a good basis for value creation with everything pretty much covered. However, it commands the excepted premium.

- That makes the company a “HOLD” with a PT of around 385 SEK per share, with a 5 SEK margin of error to the 380 level, where I would start “BUY” on the common share.

- The way I invest in Holmen is by writing puts. I go for the 380s or below where possible and secure yields of 7-11% annualized, waiting for the company to drop and collect premiums in the meantime. I have several contracts currently OTM (out of the money), but I wouldn’t be at all sad to see those “filled”.

Remember, I’m all about:

1. Buying undervalued – even if that undervaluation is slight, and not mind-numbingly massive – companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

2. If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

3. If the company doesn’t go into overvaluation, but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

4. I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them (italicized):

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside based on earnings growth or multiple expansion/reversion.

The company does not have an attractive upside due to valuation issues – I give it a “HOLD” Here, but I’m busy writing attractive put options when the company sees a decline in share price.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment