bunhill

Introduction

When last reviewing Helmerich & Payne (NYSE:HP) back in early 2022, their future was looking increasingly questionable, as my previous article discussed one year ago. Fast forward to the present day and they ended up seeing a surprisingly strong year, although this was largely due to the unforeseen Russia-Ukraine war and looking ahead, I feel it is now time to take profits, as it is quite difficult to see significantly better days ahead.

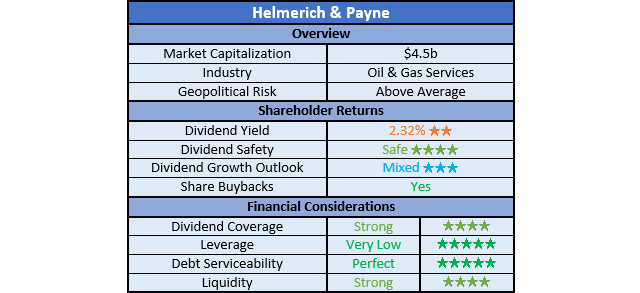

Coverage Summary & Ratings

Since many readers are likely short on time, the table below provides a brief summary and ratings for the primary criteria assessed. If interested, this Google Document provides information regarding my rating system and importantly, links to my library of equivalent analyses that share a comparable approach to enhance cross-investment comparability.

Author

Detailed Analysis

Author

The Covid-19 pandemic brought about a very severe downturn for many industries, although those in oil and gas services industry suffered immensely and worse, they also endured a slow recovery. When conducting the previous analysis one year ago, their cash flow performance was still struggling to gain traction with scant signs of consecutive improvements that often saw negative operating cash flow in some fiscal quarters.

Fast forward to the present day and ultimately, their fiscal year 2022 proved surprisingly strong with their operating cash flow landing at $233.9m, which represents a massive improvement of about 71% year-on-year versus their previous result of $136.4m during their fiscal year 2021. Whilst a positive surprise, it was largely helped by the otherwise tragic Russia-Ukraine war that sent oil and gas prices booming and thus provided an abnormally large incentive for drilling in the United States, which is not necessarily ever going to be repeated once again in the future.

Even though oil and gas prices eased as months passed, the natural lag between prices, drilling activity and finally, their cash flow performance meant their recent results for the first quarter of their fiscal year 2023 were even stronger. As a result, their operating cash flow climbed to $185.4m, which ultimately left $79.9m of free cash flow that provided strong coverage of 154.29% to their accompanying dividend payments of $51.8m.

Author

When viewed on a quarterly basis, their operating cash flow saw consecutive improvements during every fiscal quarter since the beginning of their fiscal year 2022. At the time, their reported operating cash flow was negative $3.7m, which is a far cry beneath the aforementioned most recent result. The same story is shared once excluding working capital movements with their underlying operating cash flow also seeing consecutive improvements, thereby rising from a result of $30.8m during the first quarter of their fiscal year 2022 to most recently, a very impressive $224.5m during the first quarter of their fiscal year 2023.

To put the magnitude of this latest result into context, it equals just shy of $1b if annualized, which if maintained for an entire year, would represent their highest operating cash flow since their fiscal years 2014 and 2015 given their historical cash flow performance. Whilst this initially sounds like a reason to rejoice, there is an issue lurking beneath the surface that foretells concerns on the horizon.

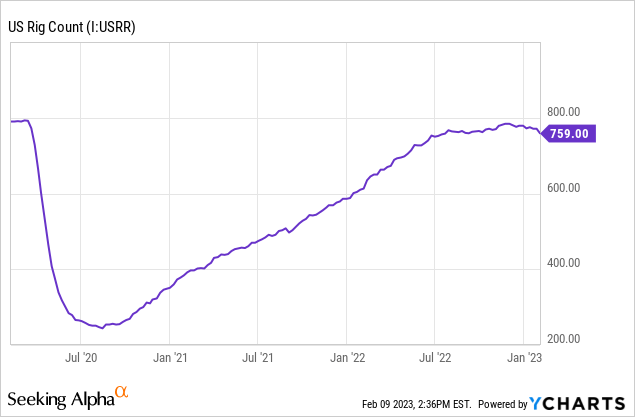

Y-Chart

When conducting the previous analysis one year ago, it was concerning to see the oil and gas rig count in the United seemingly slowing the pace of increases after initially seeing a strong bounce from the depths of the Covid-19 pandemic downturn. Following more time elapsing, the numbers ended up getting very close to their levels before the Covid-19 pandemic wreaked havoc, largely due to the Russia-Ukraine war. Disappointingly, this merely delayed my concerns from one year ago because as clearly evident in the above graph, the oil and gas rig count is now declining and thus the demand for their drilling services is also declining.

Since their recent cash flow performance is already near its historical best, the declining oil and gas rig count makes it quite difficult to see significantly better days laying ahead, at least barring another geopolitical shock. Plus, if looking further afield into the long-term, the clean energy transition hinders growth potential for oil and gas production and thus by extension, demand for their services.

Author

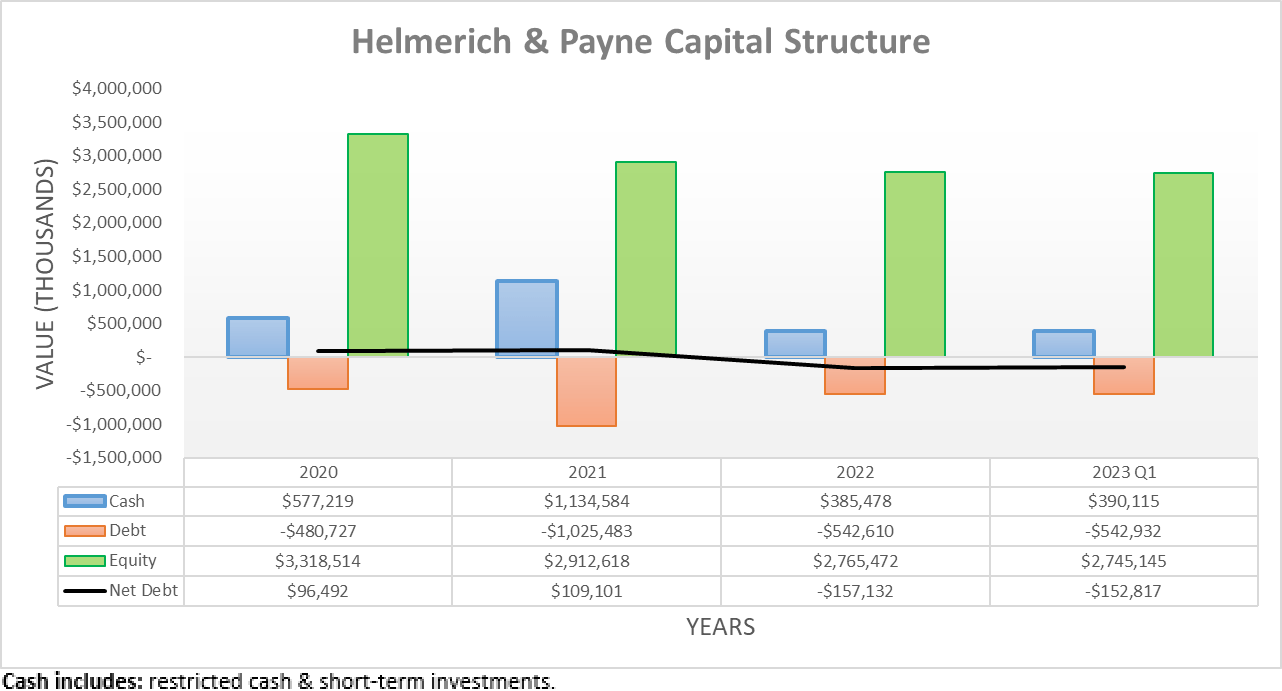

After running with a net cash position for many years, this ended during their fiscal year 2022 with their net debt emerging and subsequently climbing to $157.1m by the end of the year, before tracking broadly sideways to $152.8m following the first quarter of their fiscal year 2023. This was partly due to their negative free cash flow during their fiscal year 2022, although it was also significantly influenced by their strange choice to also conduct share buybacks in the magnitude of $77m with a further $39.1m during the first quarter of their fiscal year 2023.

Author

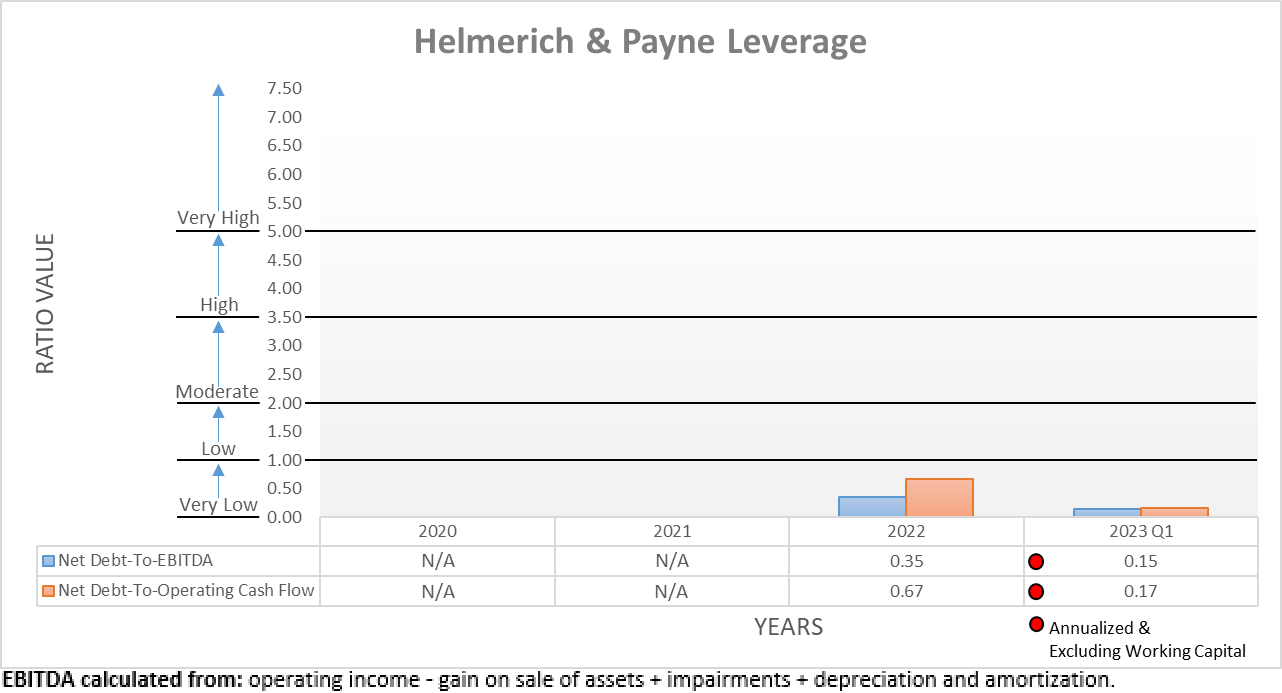

Despite net debt emerging, thankfully their leverage remains very low with barely a visible net debt-to-EBITDA of 0.15 and an accompanying net debt-to-operating cash flow of 0.17, which are both beneath the applicable threshold of 1.00. Admittedly, this is partly helped along by their very strong financial performance during the first quarter of their fiscal year 2023 and if this were to subside once again on the back of lower oil and gas drilling, it would push their leverage higher.

Since they are starting from a very low base, this is not really concerning but at the same time, it will nevertheless be important to monitor their net debt going forwards to ensure it does not become unruly, potentially fuelled by share buybacks. Otherwise, they risk damaging the one attribute that was historically their main strength and ultimately afforded the luxury of simply waiting out downturns.

Author

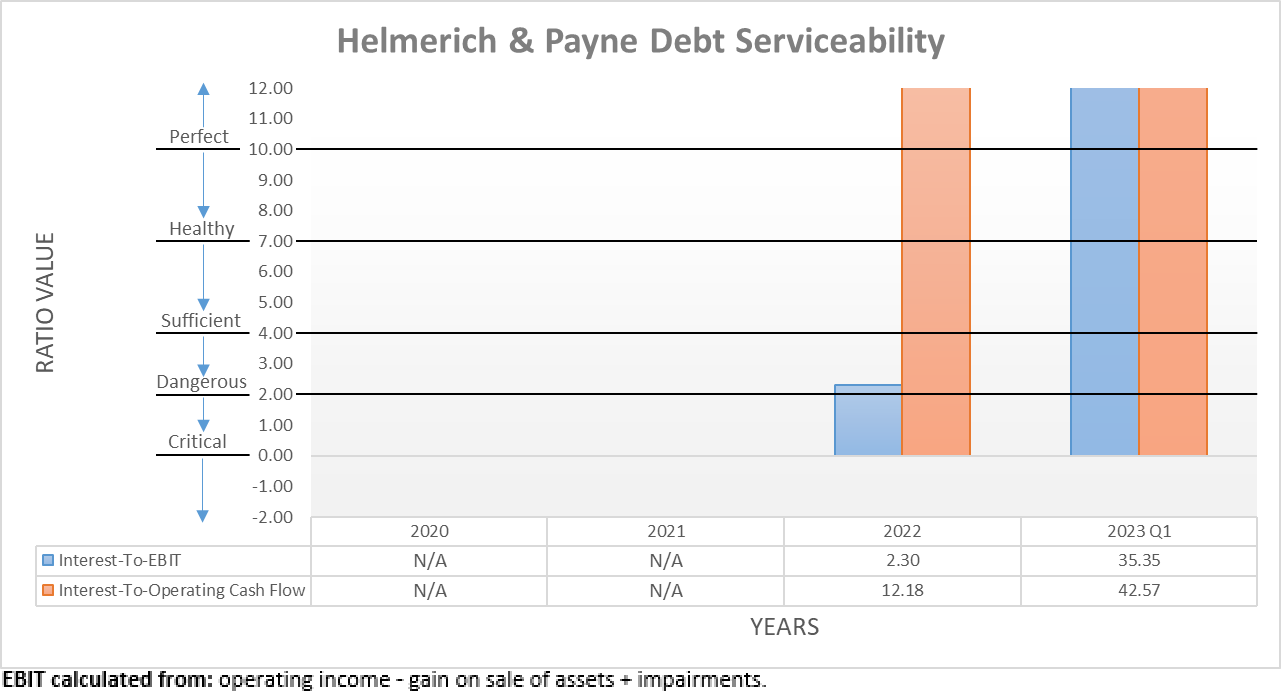

Since they still sport very low leverage, it is not too surprising this is accompanied by perfect debt serviceability with their interest coverage at 35.35 and 42.57 when compared against their EBIT and operating cash flow, respectively. Whilst positive, their recently emerging net debt did not stem from issuing new debt, rather they actually repaid debt via running down their once massive cash balance that was $1.135b at the end of their fiscal year 2020 and now sits at $390.1m following the first quarter of their fiscal year 2023.

Due to this choice, they have actually been shielded from the higher interest rates on the back of rapidly tightening monetary policy. That said, if they were to push their net debt higher going forwards, they would have to eventually start issuing new debt that would expose them to higher interest rates and thereby, hurt their debt serviceability as well as hinder their free cash flow given the larger interest expense.

Author

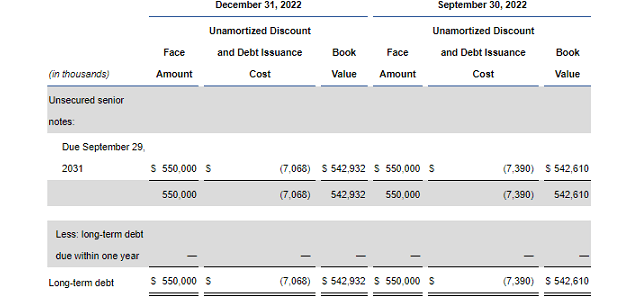

Despite running down their cash balance, thankfully their liquidity remains strong with a current ratio of 2.29 and a cash ratio of 0.83. Unless they keep running down their cash balance, this should persist well into the future but similar to their leverage, this will be important to monitor going forwards. At least they face no debt maturities until as far into the future as September 2031 when the entirety of their debt matures, which provides plenty of breathing room.

Helmerich & Payne Q1 2023 10-Q

Conclusion

Whilst it is very positive to see their cash flow performance fully recovering, it is counteracted by oil and gas drilling in the United States not just slowing down but worse, it is actually decreasing after having nearly reached the same levels as before the Covid-19 pandemic wreaked havoc. This makes it quite difficult to see significantly better days on the horizon and unlike back during 2019 when their share price was also around its present circa $40 levels, they no longer sport a net cash position. Even though this does not necessarily endanger their solvency, its loss still hinders this comparison. After wrapping everything together, I believe that downgrading to a sell rating is appropriate since I feel it is now time to take profits.

Notes: Unless specified otherwise, all figures in this article were taken from Helmerich & Payne’s SEC filings, all calculated figures were performed by the author.

Be the first to comment