Cristian Borrego Sala/iStock via Getty Images

One mustn’t dream of one’s future; one must earn it.“― Carlos Ruiz Zafón.

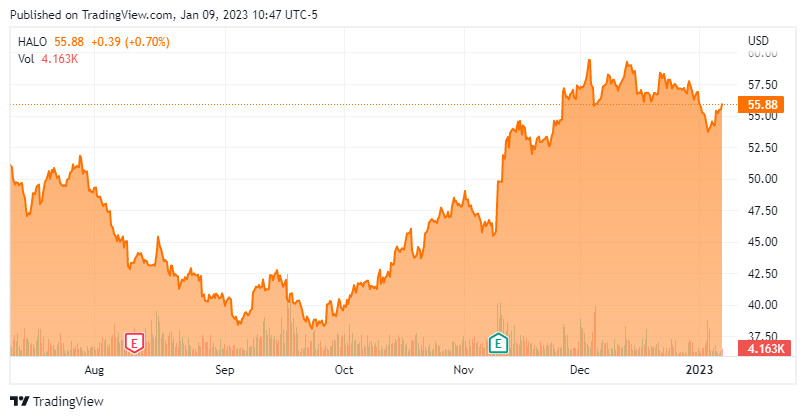

I posted an article on Halozyme Therapeutics, Inc. (NASDAQ:HALO) for the first time in many years in early August of last year. The conclusion around this unique healthcare play is that it was worthy of a small allocation should the shares drop below the $45 level.

Seeking Alpha

Investors did not have long to wait for that correction as the stock dropped briefly under $40 in early September. I picked up some shares via covered call orders during that time. That timing turned out to be prescient, as Halozyme Therapeutics shares have climbed some 30% on solid third quarter numbers and other developments. So what should Halozyme Therapeutics shareholders do now? An updated analysis follows below.

Company Overview:

This midcap healthcare concern is based in San Diego, California. Its stock has crested above the $55.00 share level and boasts an approximate $7.5 billion market capitalization.

November Company Presentation

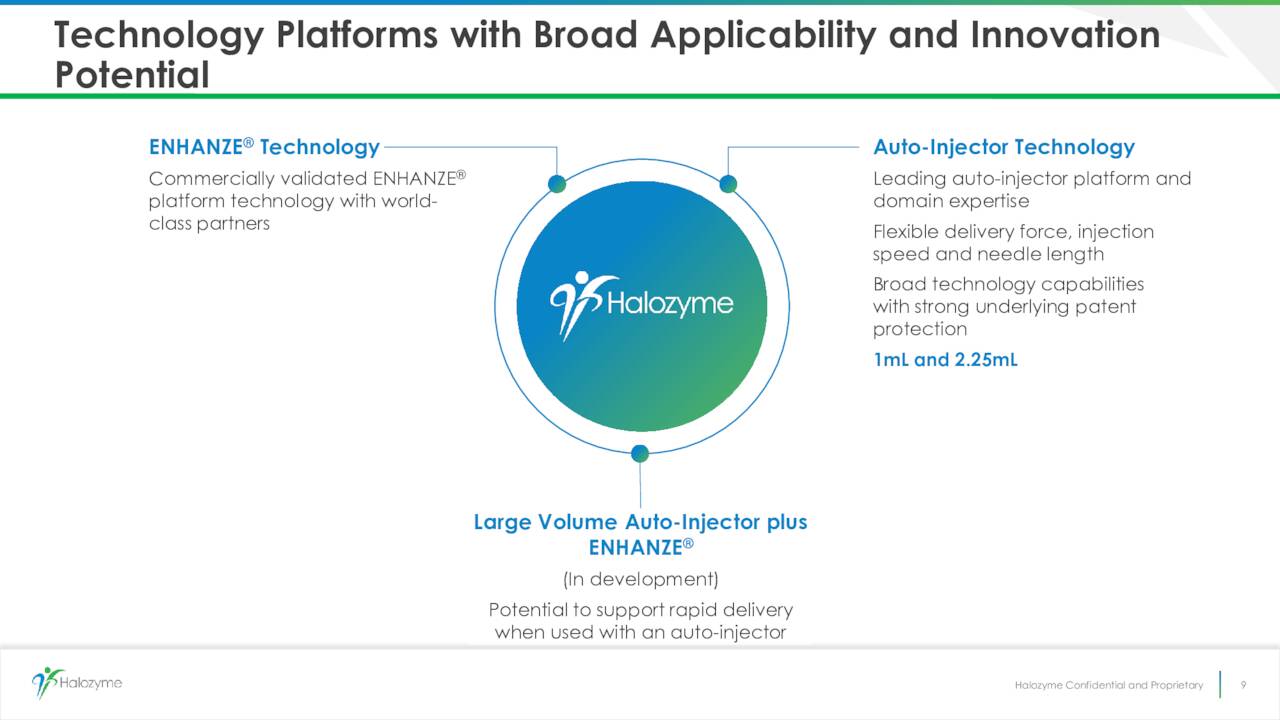

Halozyme enhances the delivery of other approved injected drugs via an advantageous subcutaneous formulation that improves infusion times. This improves the performance of many well-selling compounds, including those from Johnson & Johnson (JNJ) and other drug giants like Roche Holding AG (OTCQX:RHHBY). Halozyme does this by utilizing its ENHANZE drug delivery platform. This technology consists of a patented recombinant human hyaluronidase enzyme (rHuPH20) that enables the subcutaneous delivery of injectable biologics, such as monoclonal antibodies and other therapeutic molecules, as well as small molecules and fluids. Halozyme earns a living via royalties and milestone payouts from major drug makers for these enhanced products.

November Company Presentation

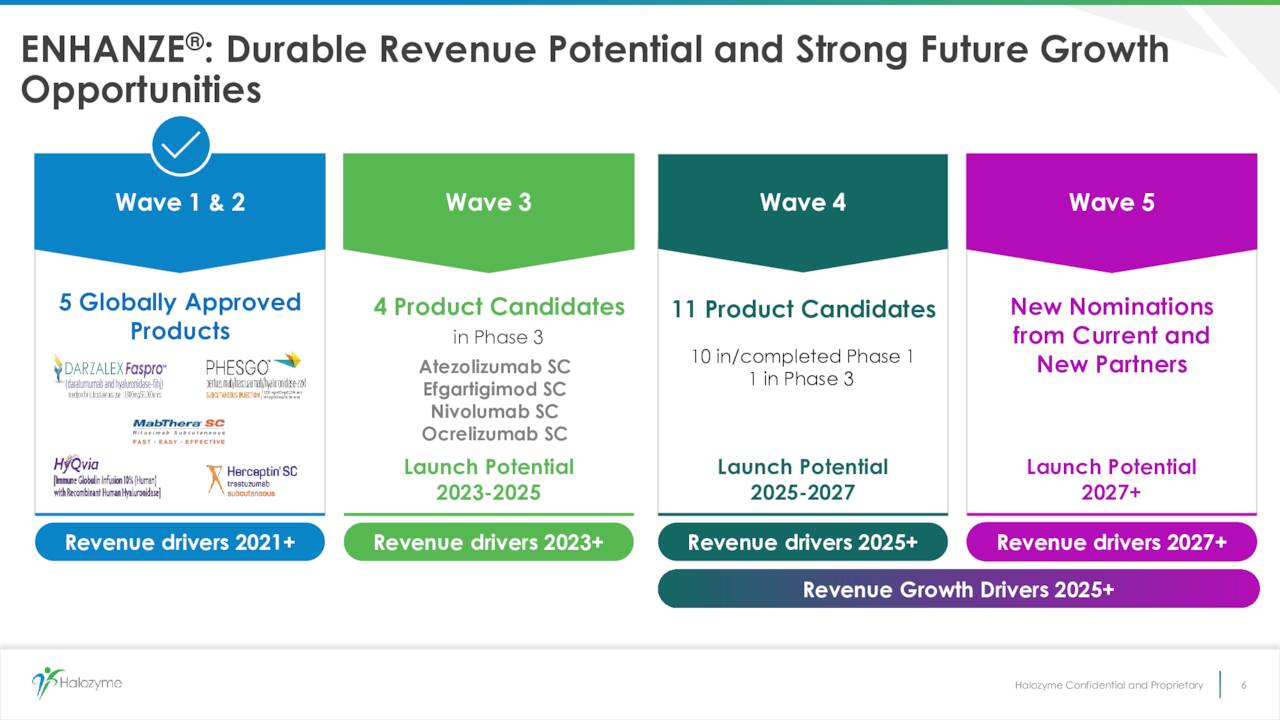

The company’s technology has resulted in five approved “reformulated” products on the market, with many more projected to follow in coming years. In late November the FDA granted priority review to argenx’s (ARGX) application seeking approval of subcutaneous efgartigimod to treat adult patients with generalized myasthenia gravis (gMG), which utilizes Halozyme’s ENHANZE technology. The final FDA decision is scheduled for the back half of March.

Third Quarter Results:

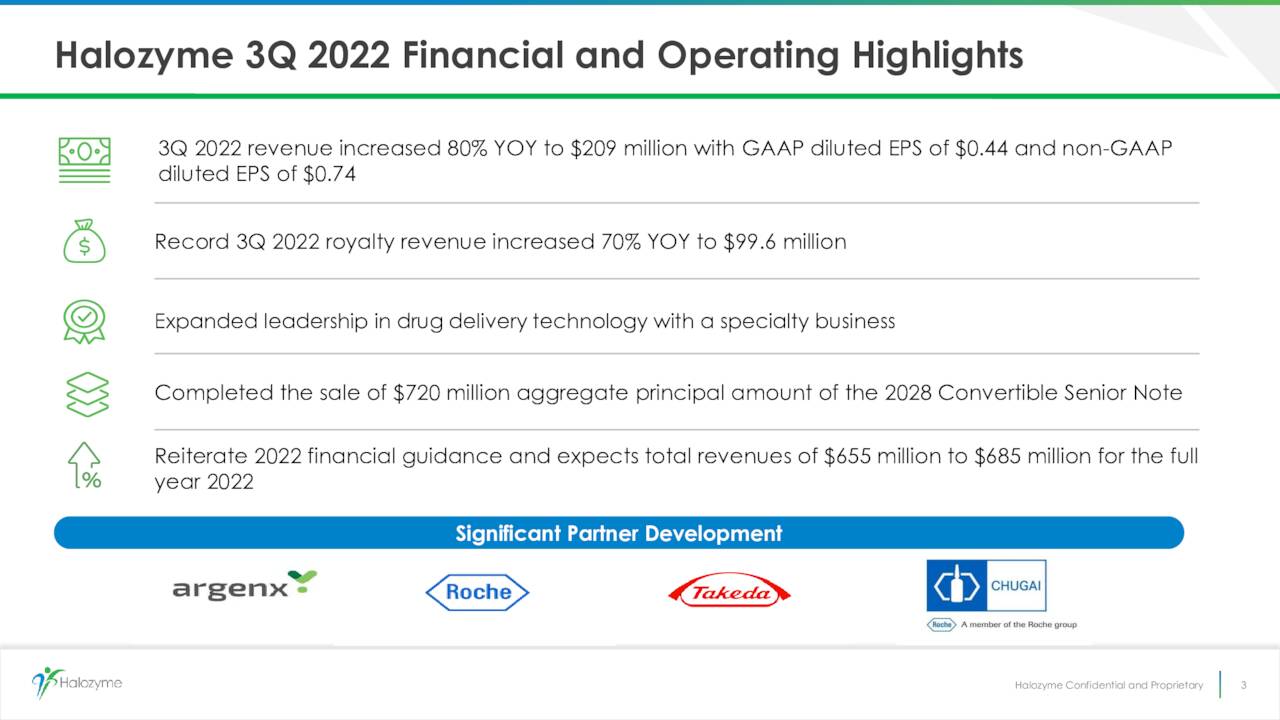

On November 8th, the company posted its third quarter numbers. The company had Non-GAAP earnings of 74 cents a share, nearly a quarter above the consensus. Revenues grew 80% on a year-over-year basis to $209 million, nearly $18 million above expectations.

November Company Presentation

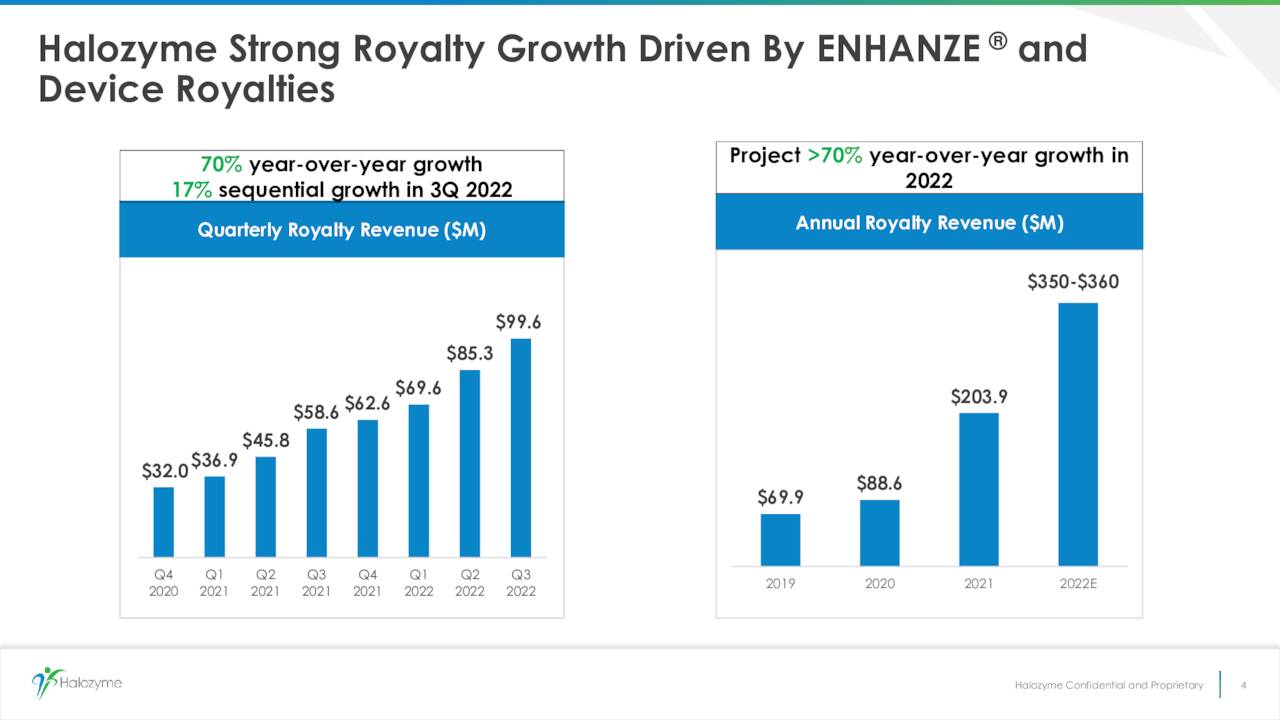

Royalty revenue was up 70% from the same period ago to $99.6 million. Management noted the overall sales increase was due primarily to:

November Company Presentation

“The robust and rapid adoption of DARZALEX Subcutaneous (daratumumab) in the U.S. and Europe, the addition of product sales as a result of the Antares Pharma acquisition and an increase in revenues under collaborative agreements due to milestone recognitions from BMS and Roche.“

November Company Presentation

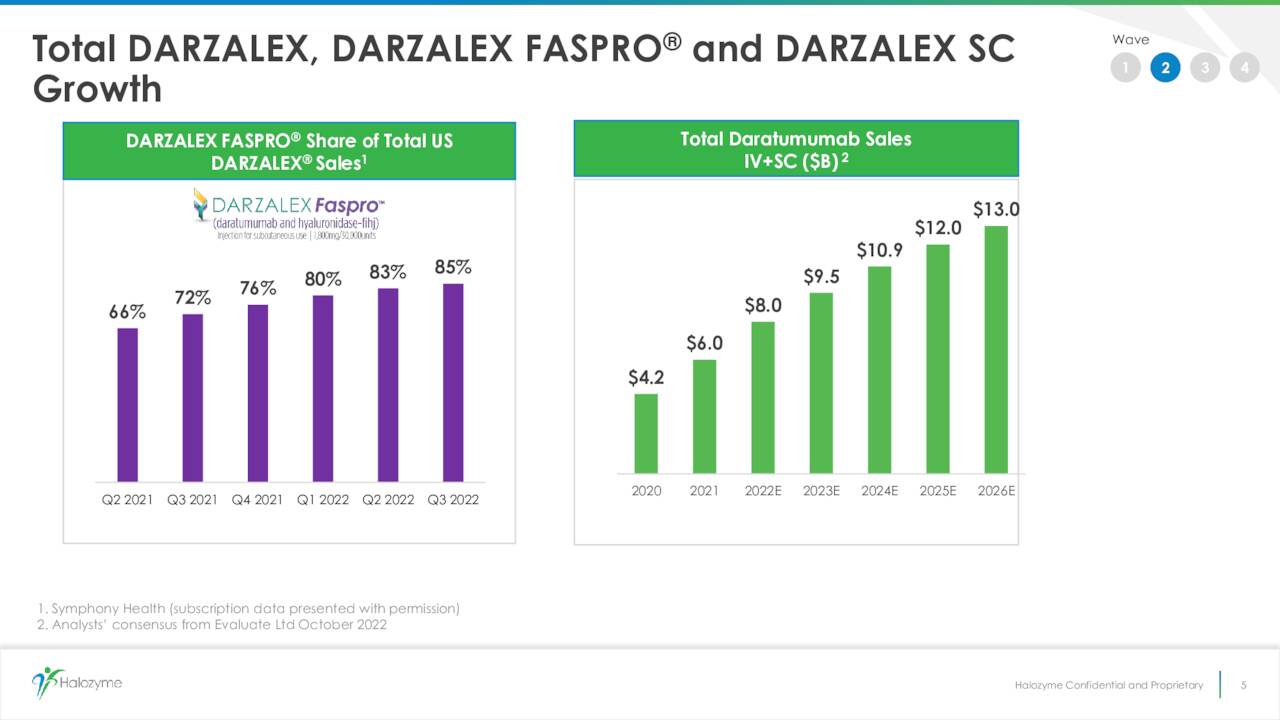

Halozyme’s subcutaneous version of DARZALEX now has 85% of the approximate $8 billion annual DARZALEX market. Leadership stated:

“It is now predicted the overall DARZALEX market will achieve $12 billion in sales in 2025 with strong continued growth driven by increased penetration into the earlier lines of treatment.”

The company also closed the purchase of Antares Pharma in early August of this year.

November Company Presentation

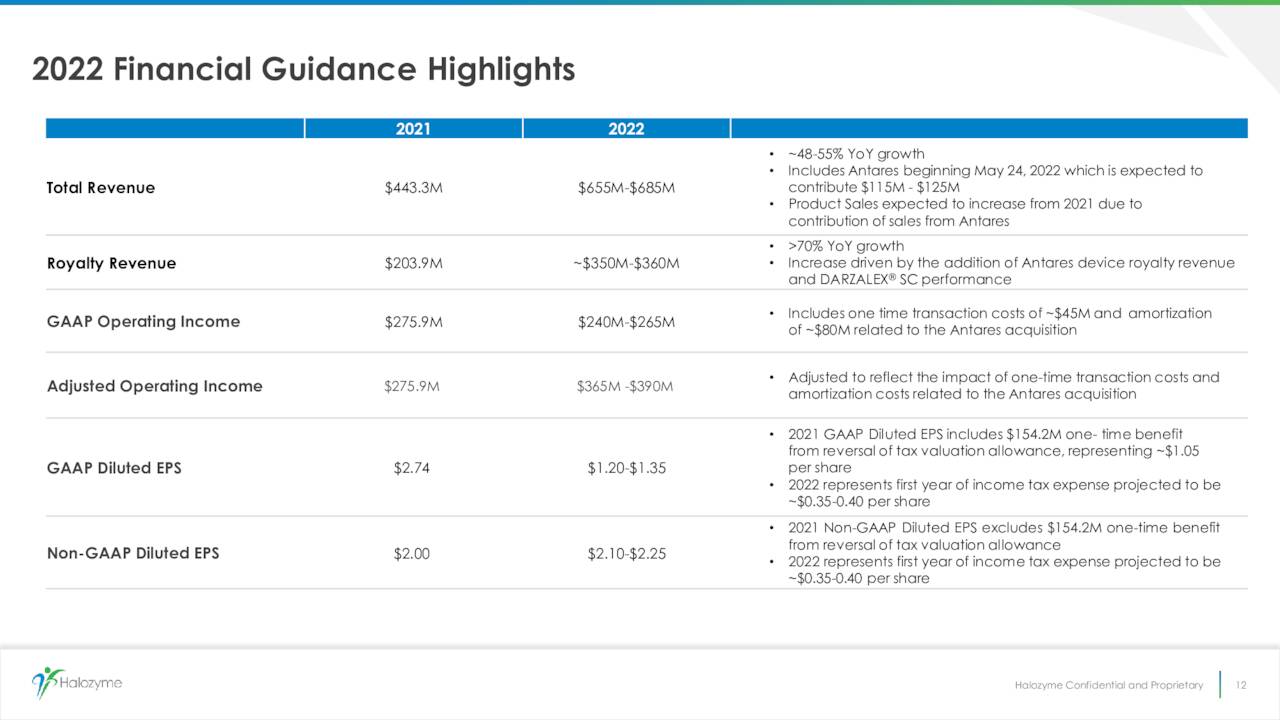

Management gave full-year revenue guidance of $655 million to $680 million for FY2022 and provided a Non-GAAP earnings range of $2.10 to $2.25 a share for the year. The consensus was looking for just under $2.05 a share at the time of the revised guidance. Royalty sales are projected to be in the $350 million to $360 million range for FY2022.

Analyst Commentary & Balance Sheet:

Since third quarter results posted, a half dozen analyst firms including J.P. Morgan and Morgan Stanley have reissued Buy/Outperform ratings on the stock. Price targets proffered range from $54 to $68 a share. In late November, Wells Fargo initiated coverage on HALO with an Overweight rating and $65 price target, noting Halozyme was a “profitable, high-growth company with earnings power to grow at 21% CAGR through the end of the decade.”

Approximately seven percent of the outstanding float is currently held short. After no insider transactions for just over a year, insider selling started to pick up noticeably in mid-November of last year. Since then, numerous insiders have disposed of more than $6 million worth of the equity in aggregate.

The company ended the third quarter of this year with $265 million in cash and marketable securities on its balance sheet against nearly $1.5 billion in long term debt. In 2022, management announced a three-year $750 million stock buyback program, which it intended to use $350 million on which in FY2022.

November Company Presentation

Verdict:

The analyst firm consensus has Halozyme Therapeutics, Inc. earning $2.20 a share in FY2022 as revenues soar just over 50% to approximately $675 million. Growth is projected to slow to just north of 30% in FY2023, with profits moving up to $2.90 a share.

Halozyme Therapeutics, Inc. does not appear expensive at just under 20 times forward earnings given its growth outlook, at least on an earnings basis. However, the stock sells for north of 11 times revenues and 13 times enterprise value/revenues taking the company’s net debt into consideration. Insiders sales have noticeably picked up over the past two months at these trading levels, and Halozyme Therapeutics, Inc. stock is bumping up against the low end of analyst firm price targets.

I am happy to let my position in HALO expire in the money when options expiration rolls around on January 20th. If the shares dip below the $50 level in the months ahead, I will probably reinitiate a covered call holding in a ‘rinse, wash and repeat‘ trade around Halozyme Therapeutics.

It is difficult to say what is impossible, for the dream of yesterday is the hope of today and the reality of tomorrow.”― Robert H. Goddard

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment