ArtistGNDphotography

Introduction

Guess (NYSE:GES) shares have risen 2.5% YTD. Since my publication on October 21, 2022, the stock is up 36%, outperforming the S&P index, which posted an 8.7% gain. Due to rising stocks, continued pressure from inflation, macro data updates and a change in my expectations for the future cash flows of the business, I have decided to amend my forecasts and update my recommendation.

The survey of current trends

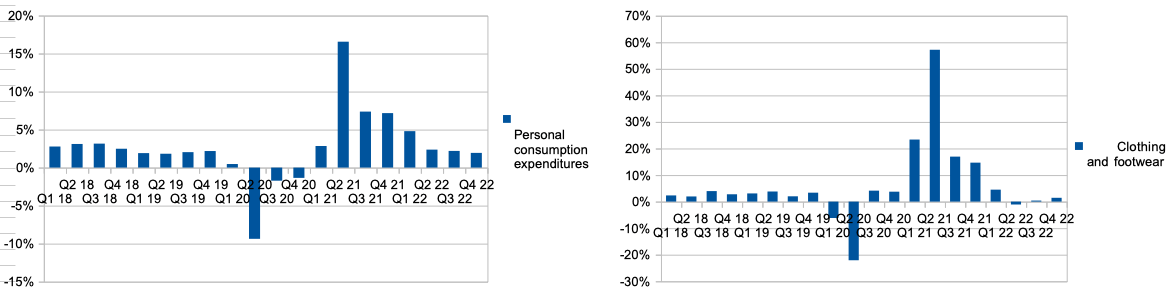

I believe that the decrease in consumer spending may have an impact on the company’s revenue dynamics in future periods. At the end of 2022, overall consumer spending continued to be under pressure due to rising macro and geopolitical uncertainties, higher interest rates, lower real incomes and consumer confidence. Spending in the Clothing and footwear segment continues to be under pressure too. According to the results of the 4th quarter, the growth in expenses in the segment amounted to a little more than 1% YoY. In my personal opinion, I expect continued pressure on consumer spending in the Clothing and Footwear segment in 2023, which could have a negative impact on revenue growth and the operating margin of the business. You can see the details in the charts below.

bea.gov (Personal expenditures)

Projections

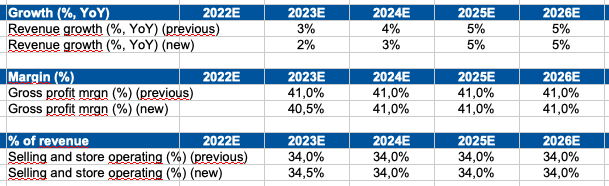

After the company’s Q3 2022 report and the pressure on consumer spending, I decided to make some changes to my model. As such, I lowered my 2023 revenue growth forecast from 3% to 2%. In addition, I lowered my expectations for the gross margin from 41% to 40.5% in 2023 due to pressure on sales and reduced economies of scale. In addition, I raised my SGA (% of revenue) spending forecast from 34% to 34.5% in 2023. You can see the details in the chart below.

Forecasts (Personal calculations)

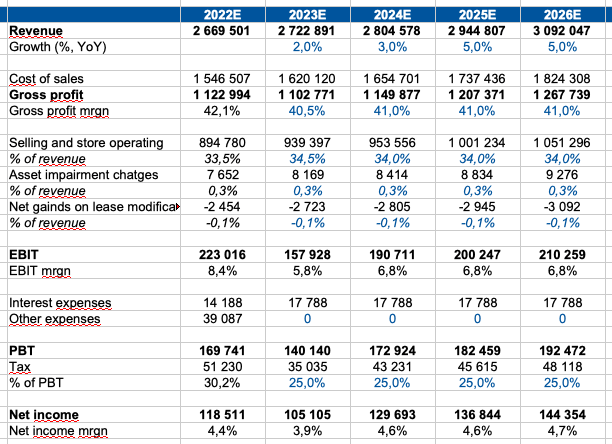

Thus, when forecasting future cash flows, I rely on the following inputs:

Revenue growth: I believe that the revenue growth rate will decrease to 2% in 2023, then I predict revenue recovery to 5% by 2026 with the normalization of consumer behavior, consumer spending and the recovery of real incomes of the population.

Gross margin: I expect pressure on the gross margin, so I predict a decline to 40.5% in 2023, then I predict a recovery to 41% by 2026.

SGA: I expect a decrease in (% of revenue) from 34.5% to 34% by 2026.

Yearly projections

Forecasts (Personal calculations)

Valuation

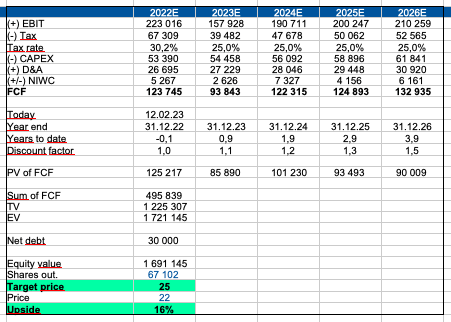

I use the DCF approach to value a company. In my personal opinion, the use of the DCF model for valuation is the most preferable for a company that operates in a stable and predictable market. In addition, the use of DCF allows me to make assumptions about future revenue growth and operating margin trends. Also, when forecasting, I can rely on a long period of historical observations and macro data.

Basic inputs for my model:

WACC: 10.6%

Terminal growth rate: 3%

DCF model (Personal calculations)

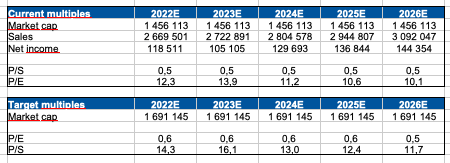

Multiples

In addition, I calculated current and future P/E and P/S multiples based on my sales and net income projections for the company. You can see the details of my calculations in the chart below.

Multiples (Personal calculations)

Risks

Macro: declining real incomes, high inflation and declining consumer confidence could lead to lower consumer spending on clothing, which could have a negative impact on the company’s bottom line.

Revenue growth: a decrease in the average check or a decrease in traffic in stores as a result of cost reduction can lead to a decrease in revenue and a decrease in economies of scale.

Margin: decreasing economies of scale, rising operating costs and the inability to raise prices for weakening customers can lead to lower operating margins.

Drivers

Macro: a recovery in real incomes and lower inflation could lead to a normalization of consumer patterns and an increase in consumer confidence, which could support equities in the coming periods.

Margin: it is possible to raise prices for the end consumer, the growth of economies of scale and effective management of operating costs can have a positive impact on the level of operating profitability in the future.

Conclusion

Despite the presence of fundamental potential, in my personal opinion, now is not the best time to open long positions. I believe that a decline in real income and therefore consumer spending in the apparel segment could have a negative impact on business growth rates in the first half of 2023, which could lead to a post-growth share price decline. So I decided to lower my price target for the stock from $30 to $25 and change my recommendation from Buy to Hold.

Be the first to comment