CHUNYIP WONG

I would like to add to our position in Essex Property Trust (NYSE:ESS) again. We picked up some shares in November, and I still like the valuation.

NAV Expectations

I’m expecting NAV estimates to continue trending lower across apartment REITs. That’s a mix of pressures on apartment values in the private real estate market with less attractive financing and analysts being late to update their estimates as they try to build out their models.

It’s worth mentioning that analyst models often have significant flaws, but using the consensus estimate for larger REITs can often get us reasonably close so long as we remember the lag time impact. It also helps to remember that analysts will try to reach NAV estimates by plugging in NOI estimates and cap rates. Consequently, if NOI goes up or down without real estate values changing, analysts will incorrectly estimate a change because they may be slow to adjust the cap rate.

Guidance

ESS gave weaker guidance for 2023 than the other apartment REITs. Some investors believe that means the situation in California is hopeless. I don’t see it that way.

ESS builds their guidance, leaning heavily on macroeconomic forecasts. When those forecasts are bearish, they will give weaker guidance than REITs that build their guidance using other techniques.

Buybacks

I’d like to see ESS using this opportunity to focus on share buybacks. Not taking on extensive leverage but unloading a couple of buildings and using proceeds to repurchase shares. It has a small positive impact on growth, but it also sends a strong signal to the market.

Previously, ESS has repurchased shares when trading at a material discount. That has happened as recently as Q3 2022. On the Q3 2022 earnings call, management stated:

Turning to our stock repurchase and investments. Consistent with last quarter, investing in our own portfolio and select preferred equity investments offers the best risk-adjusted returns in today’s market. In the third quarter, we repurchased $97 million of common stock at a significant discount to our internal NAV, which we plan to match fund on a leverage-neutral basis with proceeds from a disposition expected to close in the fourth quarter.

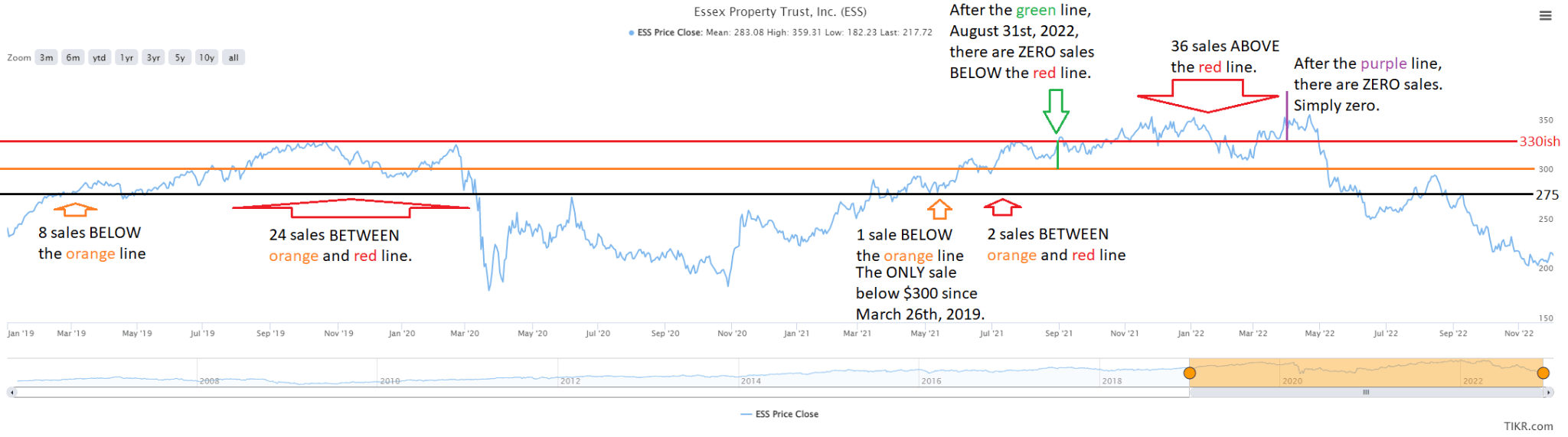

Management Transaction History

Some investors focus on insider trading. There are times when it can be a useful signal, but I find it helps to look for patterns. ESS hasn’t had much insider buying in a very long time. There was only one insider buy since June 2013. So, we probably shouldn’t read into a lack of insider buying. However, we could analyze the information in a different way.

There have been several insider sales across the last decade. We could look at the price for those transactions to see if we can find a trend. After we copy the data into Excel, we can start running filters. The method I found most useful was filtering for transactions since the start of 2019 to meet the following criteria:

- Price below $275.00. Insider Sales: 0.

- Price below $300.00. Insider Sales: 9. Out of 9, 8 were in Q1 2019.

- Price below $330. Insider Sales: 26. Out of 26, 24 were before Q2 2020.

- Price above $330. Insider Sales: 36. All were between Aug. 31, 2021, and March 31, 2022.

I think the chart enhances the message. You’ll need to zoom in on this image for decent resolution:

TIKR.com

Dividends and NAV

The fact remains that ESS trades at a substantial discount to the net value of its assets (consensus estimate of $284.57 in early December per TIKR.com). Further, their dividend of $8.80 per share (annualized) provides an attractive 4.2% dividend yield. That dividend is thoroughly covered with consensus AFFO per share over the next year at $13.46.

In my opinion, those factors easily outweigh the near-term headwinds.

That dividend has been exceptionally stable. ESS is a dividend champion with 27 consecutive years of dividend growth.

Conclusion

There are still plenty of challenges facing apartment REITs. The biggest one is the rapid deceleration in rent growth. In some markets, month-over-month asking rent growth is negative. In simpler terms, that means in some markets, landlords are asking for lower rents in November and December than they were for the same units in August through October. Clearly, that’s a material headwind.

Further, apartment rents are still pressured by a large volume of projects being completed in late 2022 through 2023. This is a temporary headwind. It’s an increase in supply, but supply won’t be growing that fast for long. The amount of new projects starting today is dramatically lower. This is simply the lag time that occurs between when projects were started (with a better economy and lower interest rates) and today.

We don’t buy apartment REITs when everything looks great. We were fiercely bearish on the sector earlier this year, with the argument that rental rate growth was going to plunge and trigger negative headlines. Now that we have that environment, prices are very attractive again.

Alternatives

AVB and CPT: I’ve thought about starting a position in Camden (CPT) or growing our position in AvalonBay (AVB), but the weakness in ESS made it the most attractive choice.

SUI: Still a good choice, but we already have a large position in Sun Communities (SUI) and increased our allocation in October. Still on the radar as a potential choice, especially if it underperforms. Shares are deep in our target range.

Ratings: Bullish on ESS, AVB, CPT, ESS

Be the first to comment