400tmax

Alphabet (NASDAQ:GOOG) (NASDAQ:GOOGL), also known as Google, reported Q2 earnings recently. While the company’s EPS and revenues came in slightly below forecasts, the general tone of the report was strong. Google’s stock is down by about 30% from its ATH this year as concerns of an economic slowdown and a slowdown in ad spending linger. Yet, the recent earnings report illustrates Google’s resilience and implies that the company should weather the storm better than anticipated. Moreover, Google should continue growing revenues and expanding EPS in future years, and the stock is relatively cheap here. Therefore, Google’s stock represents a compelling long-term buying opportunity at current levels, and its share price should appreciate considerably as we advance.

Google Isn’t Snap

Snap Inc. (SNAP) experienced another epic drop recently after providing a horrible earnings report. Snap also relies heavily on ad spending, and the company reported top and bottom line misses along with weak guidance. However, Google isn’t Snap, and not all companies that rely on ad sending are created equal. Snap’s been delivering worsening results for several quarters now, and the company warned of deteriorating economic conditions in prior reports. Snap’s stock is down from a high of around $85 to just about $9 a share as the company’s revenue growth has decelerated significantly. However, Google is much different, and the company is posting very different results.

Google’s Q2 Earnings Report

Google reported GAAP EPS of $1.21, missing consensus estimates by 6 cents. The company reported revenues of $69.69 billion, missing the estimated figure by $110 million. However, despite the slightly lower-than-expected numbers, investors were pleased with the results. There were fears of a more significant miss, and it’s constructive to see that Google’s earnings are not deteriorating. Moreover, the company’s revenues increased by 12.6% YoY, illustrating continued robust growth for the tech giant.

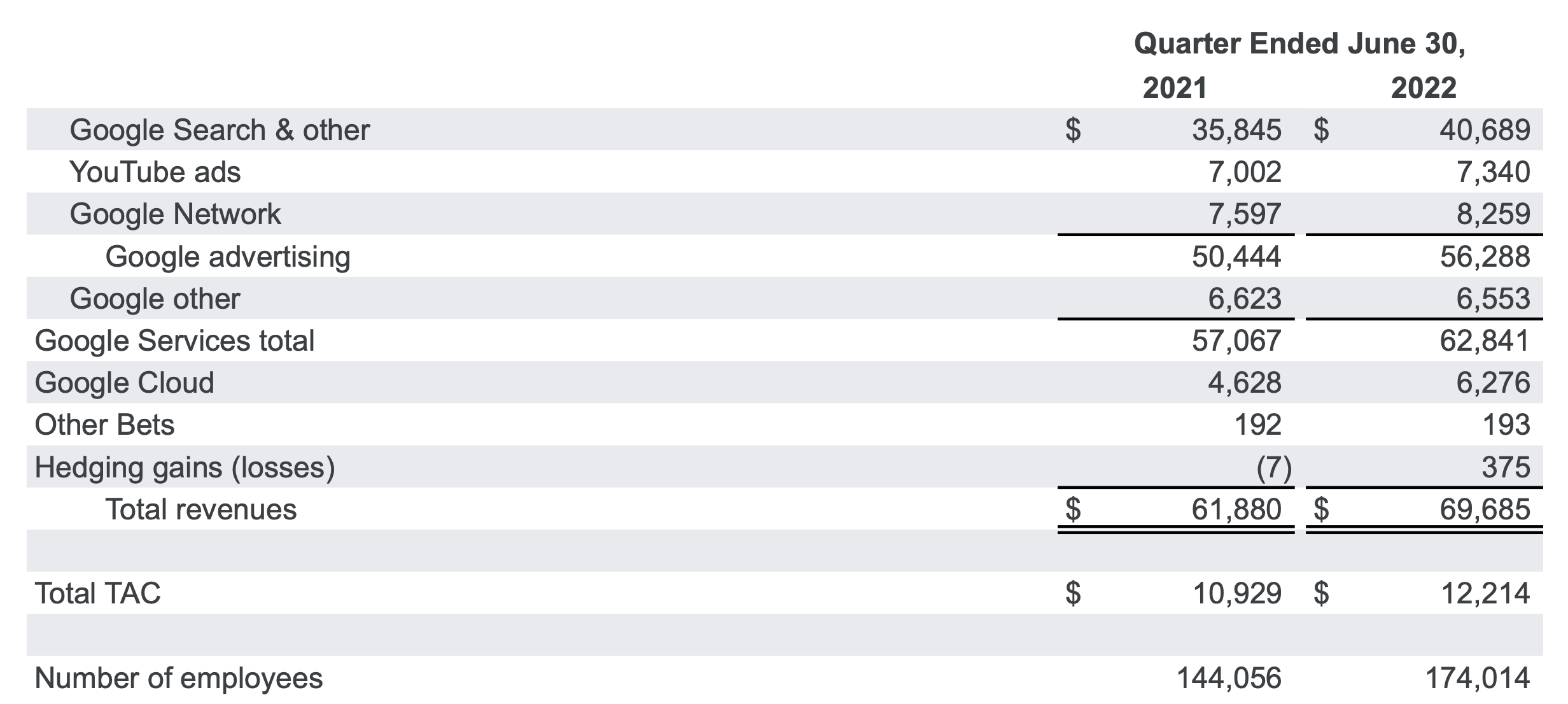

Statement of Operations

Operating statement (abc.xyz)

Google Search and “other” delivered about $40.7 billion in revenues last quarter, a 13.7% YoY gain. This figure illustrates that despite the slowing economic conditions, Google’s core Search segment continues firing on all cylinders, providing significant growth for the company. YouTube ads revenues came in at $7.34 billion, illustrating modest growth. Google advertising provided approximately $56.3 billion in revenues, roughly 12% YoY growth. Cloud revenues came in at nearly $6.3 billion, illustrating a significant 36% YoY growth in Google’s cloud segment.

Google Can Improve Efficiency

Google’s employee count increased significantly by almost 21% to more than 174,000 YoY. The company said it would “slow” the hiring rate through 2023, as even Google is not immune to economic headwinds. Therefore, Google will probably focus on increasing efficiency, which should translate into improving margins and higher profitability in the coming quarters. The increased efficiency should offset some of the impacts from slower growth and inflation, softening the overall blow from the economic slowdown.

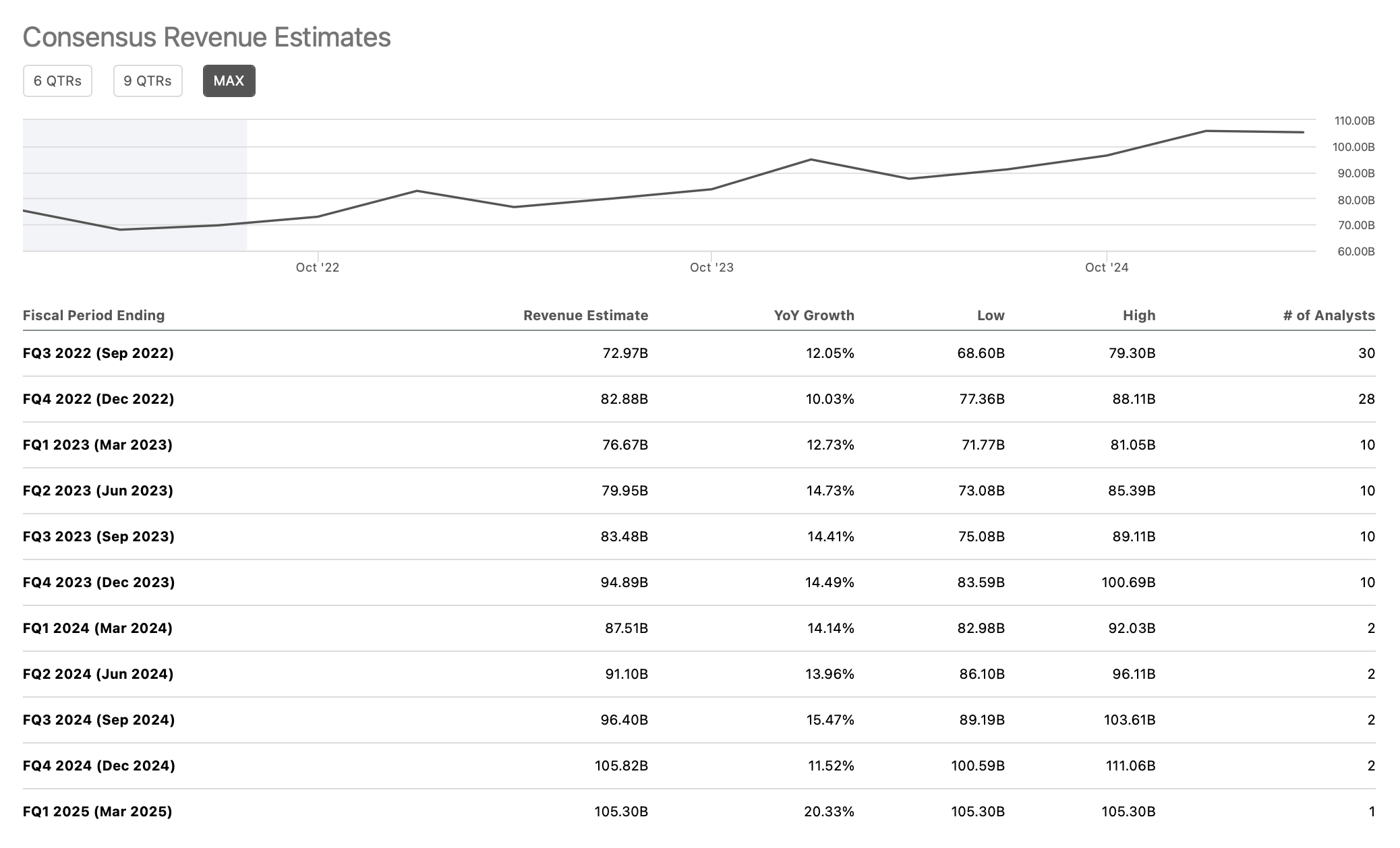

Google – On Its Way to Making $100 Billion Per Quarter

Revenue Projections

Revenue growth (SeekingAlpha.com )

Remarkably, Google will probably make more than $100 billion per quarter soon. The company’s double-digit revenue growth should continue through 2025 and probably longer. Therefore, the company could provide more than $400 billion in sales by 2025. With booming sales, Google should deliver substantially more profits for shareholders simultaneously.

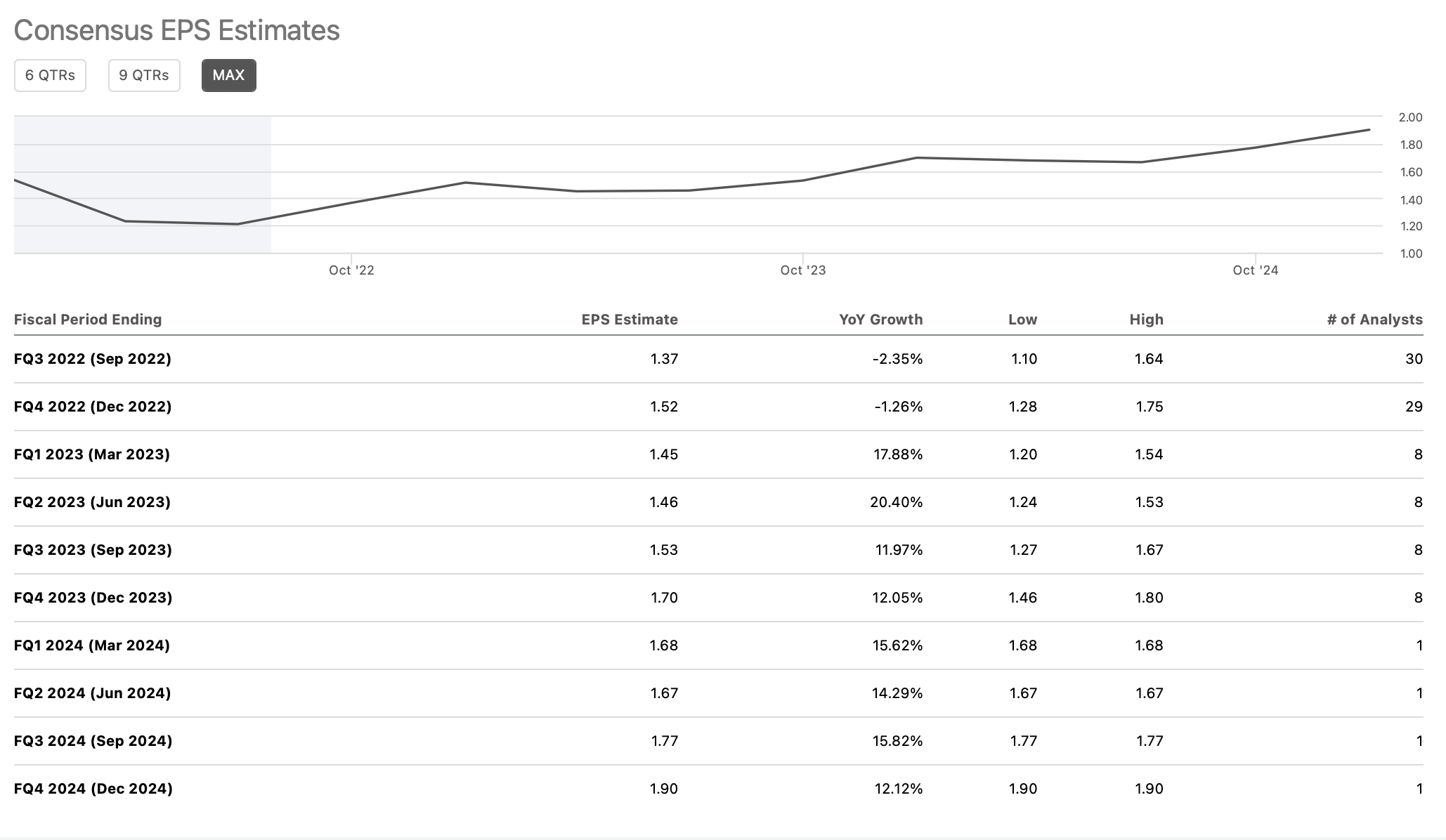

EPS Estimates

EPS estimates (SeekingAlpha.com )

Despite a slight decline this year, Google should return to robust EPS growth as the company advances. Consensus EPS estimates are for $6.14 in 2023. Therefore, Google is trading at only 17 times forward earnings estimates. In 2024, Google should earn around $7 in EPS, placing its forward 2024 P/E multiple at just 15. Given Google’s significant long-term growth prospects and exceptional earnings potential, the company’s stock is relatively cheap and should appreciate considerably in the coming years.

Here is what Google’s financials could look like in future years:

| Year | 2022 | 2023 | 2024 | 2025 | 2026 | 2027 | 2028 |

| Revenue Bs | $294 | $345 | $392 | $445 | $503 | $565 | $634 |

| Revenue growth | 21% | 17% | 14% | 13.5% | 13% | 12.5% | 12% |

| EPS | $5.13 | $6.15 | $7.05 | $8.30 | $9.80 | $11.60 | $13.30 |

| Forward P/E ratio | 17 | 18 | 19 | 20 | 20 | 19 | 18 |

| Price | $105 | $127 | $156 | $196 | $232 | $252 | $275 |

Source: The Financial Prophet

I’m using relatively modest projections of low double-digit revenue growth and EPS growth of approximately 15-18% in the coming years. Also, I am just using a slightly higher forward P/E multiple, keeping it around or below 20 as the company advances. Nevertheless, we see that Google’s stock is likely heading higher and should be approximately $300 by the decade’s end, possibly sooner. Furthermore, the company could achieve higher growth, become more profitable, or experience more significant multiple expansion, resulting in a higher stock price than my projections predict.

Be the first to comment