monsitj

Gold prices are up 15% since the triple bottom was triggered in early November, and the metal’s rally shows no sign of ending. Another run at the USD2,000 area looks likely from a technical perspective. However, gold’s strength over the past two months has contrasted greatly with the fundamentals, which now suggests the metal is overvalued. I believe that a covered call position is now an appropriate strategy to protect against a downside reversal.

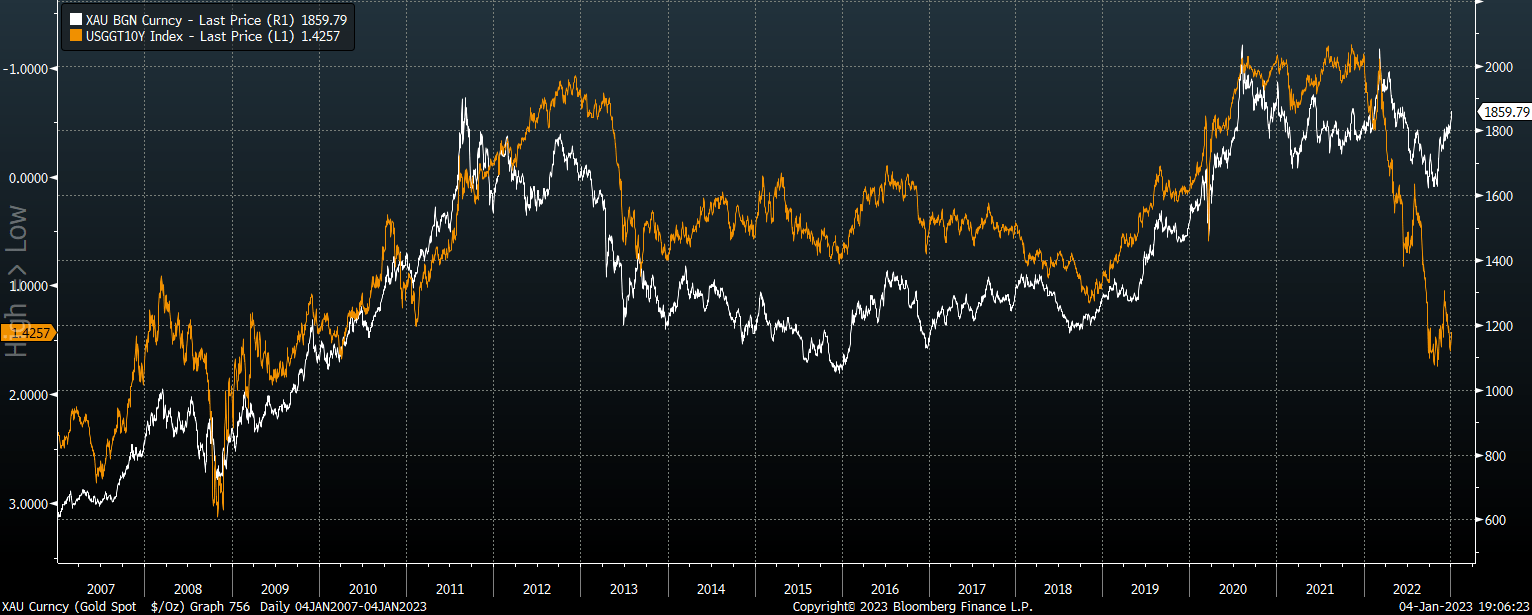

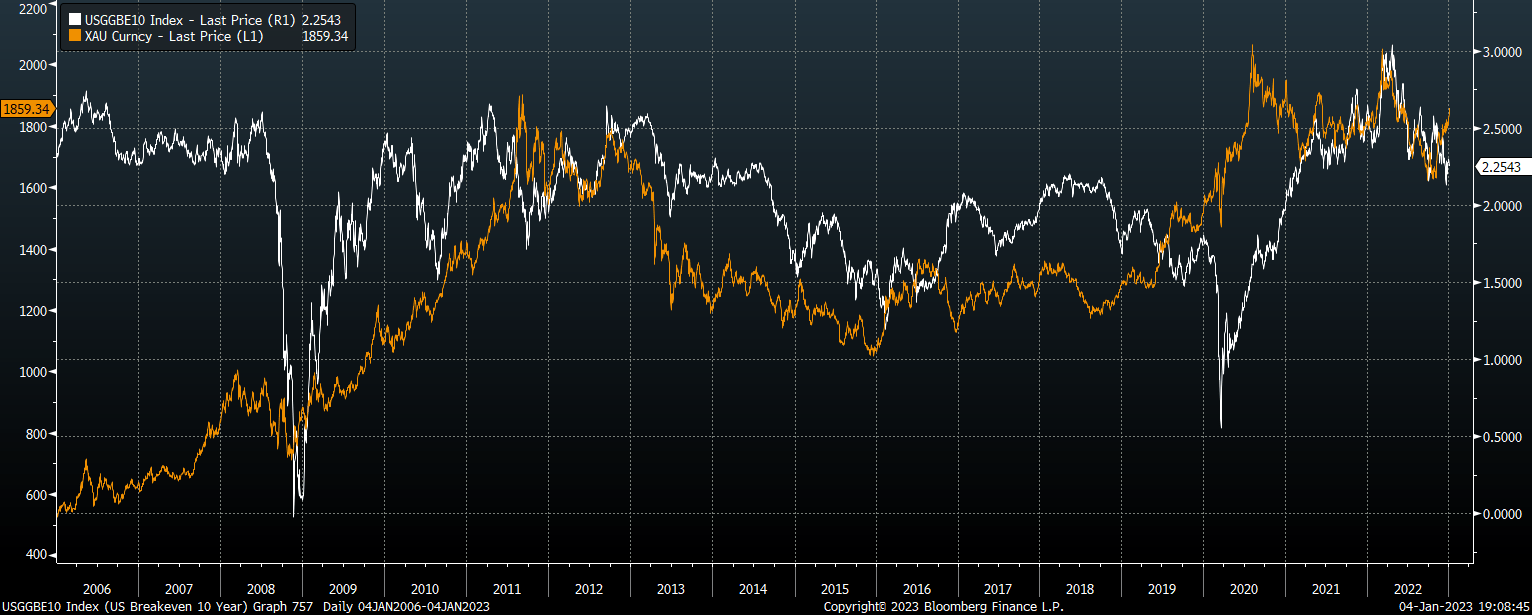

Real Yields Are No Longer Supportive For Gold

The single most important factor driving short-term gold prices over the past two decades has been real bond yields, specifically the yield on long-term U.S. inflation-linked bonds. When real bond yields are high and rising, this raises the opportunity cost of holding gold, which of course does not pay any interest. While real bond yields and gold prices were closely inversely correlated for most of last-year’s selloff, gold has risen since November even as real yields have remained near cycle highs.

Gold Vs 10-Year Inflation-Linked Bond Yield (Bloomberg)

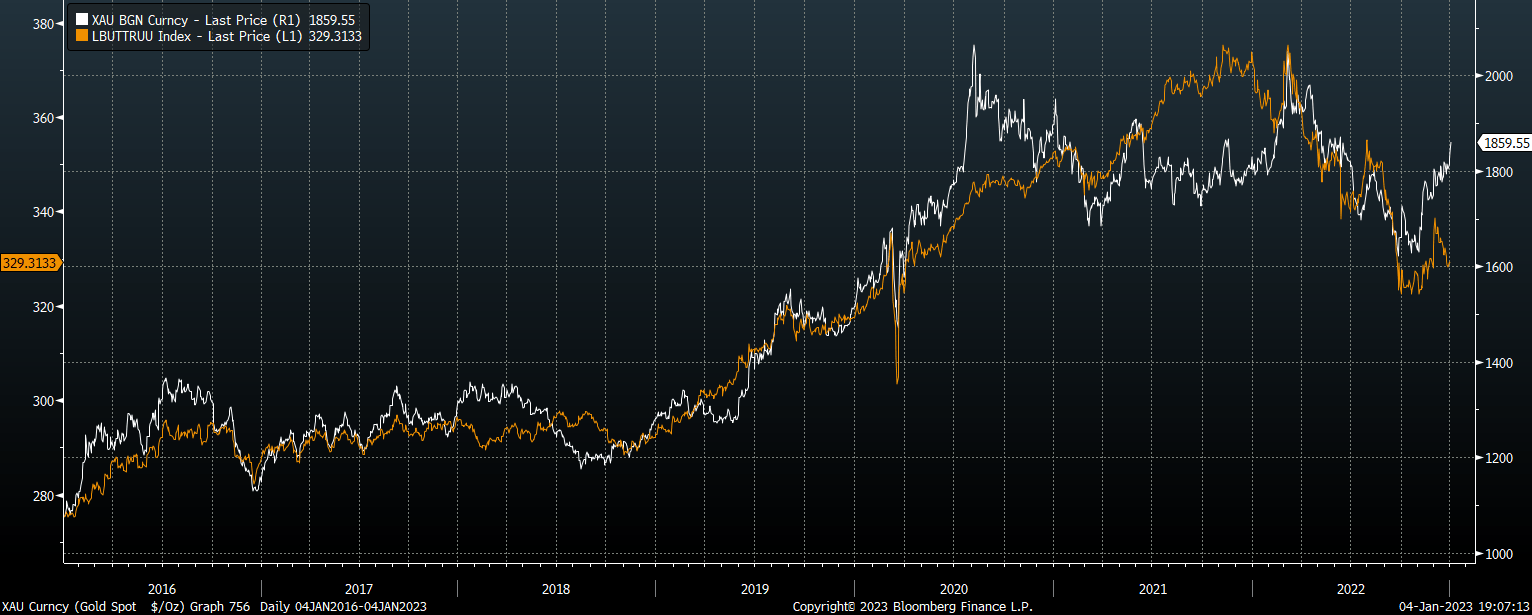

As U.S. inflation-linked bond yields do not capture the steady upward pressure on gold caused by inflation, we can also compare gold to the total return performance of U.S. inflation-linked bonds. Even when the impact of inflation is taken into account, the rally in gold still seems excessive.

Gold Vs 10-Year Inflation-Linked Bond Total Return (Bloomberg)

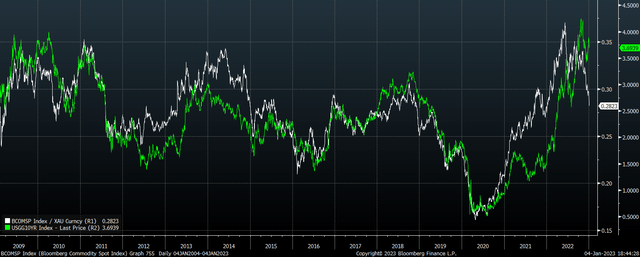

Gold’s Rise Has Bucked The Global Commodity Trend

Over the long term, gold prices tend to track the price of the broader commodity complex, as both are driven in part by global inflation pressures. Here again, the rally in gold prices seems out of line with the fundamentals, with the metal’s 15% rally since November occurring alongside a fall in commodity prices.

U.S. 10-Year Bond Yield Vs Ratio Of Commodity Complex Over Gold (Bloomberg)

It is not unusual for gold prices to disconnect with the broader commodity complex during times of falling bond yields, but gold’s recent outperformance has come even as nominal yields have risen significantly.

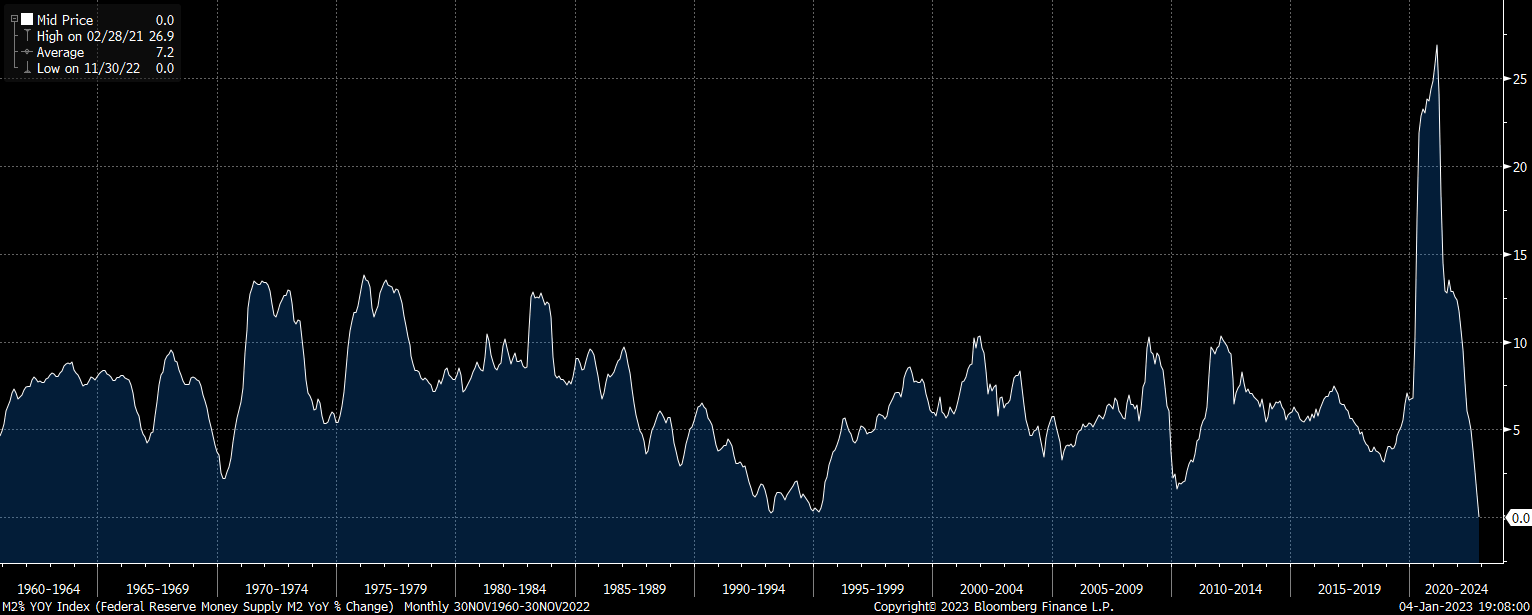

The Risk Of A Deflation Shock Is Growing

As I argued in ‘VGLT: Bonds Look Good As Deflation Scare Increasingly Likely‘ there is a growing threat of another episode of cash hoarding as U.S. money supply contracts and risk assets face another leg down. M2 growth is current at zero in year-on-year terms and is highly likely to turn negative over the coming months for the first time on record. This, combined with increasingly austere real borrowing costs, suggests we are now in one of the tightest periods of monetary policy on record. It would likely only take a spike in U.S. corporate credit spreads for investors to scramble for dollars in a self-reinforcing shock.

U.S. M2 Money Supply Growth (Bloomberg, Federal Reserve)

While I have noted in previous gold articles that any such deflationary shock would be met with further rounds of monetary and fiscal easing, which would actually improve the long-term outlook for gold, in previous such deflationary shocks, gold has still suffered a large initial selloff. In 2008 the metal lost 30% from peak to trough, while it lost 15% in 2020.

U.S. Breakeven Inflation Expectations Vs Gold Price (Bloomberg)

Selling Call Options Is The Way To Go

One option for benefitting from the overdone rally in gold prices would be to enter a short position, but with the technical picture still looking strong and the long-term outlook for the metal still bright, this is not a strategy I would recommend. A more attractive idea is to sell calls options. At the money call options for expiry on May 25 are currently trading at USD95, which translates to an annualized return of almost 13%. For anyone holding gold and looking to hedge against short-term weakness, this high option premium means that investors are unlikely to lose unless we see a large drop in gold prices, in which case losses will still be cushioned. For anyone not long the metal, selling naked call options is preferable to shorting in my view as losses are capped in the event of a continued rally.

Be the first to comment