Alex Potemkin

In recent months, I’ve changed my preferred stock focus to issues that get on the dividend elevator by converting from fixed to floating payments.

I’ve written about Wells Fargo Series R (WFC.PR) and Annaly Capital Management Series F (NLY.PF), and set up a spreadsheet comparing some of the converting issues.

| Ticker | Coupon | Dividend |

Recent Price |

Yield | Call/conversion date | Terms | ||

| C-K | 6.88% | 1.719 | 25.03 | 6.87% | 11/15/2023 | Fixed to floating LIBOR+4.130% | ||

| C-J | 7.12% | 1.78 | 25.16 | 7.07% | 9/30/2023 | Fixed to floating LIBOR+4.04% | ||

| GS-J | 5.50% | 1.38 | 24.65 | 5.60% | 5/10/2023 | Fixed to floating LIBOR+3.64% | ||

| GS-K | 6.38% | 1.59 | 24.77 | 6.42% | 5/10/2024 | Fixed to floating LIBOR+3.55% | ||

| MS-E | 7.13% | 1.78 | 25.15 | 7.08% | 10/15/2023 | Fixed to floating LIBOR+4.32% | ||

| MS-F | 6.88% | 1.72 | 24.98 | 6.89% | 1/15/2024 | Fixed to floating LIBOR+3.94% | ||

| MS-I | 6.38% | 1.59 | 24.26 | 6.55% | 10/15/2024 | Fixed to floating LIBOR+3.708% | ||

| NLY-F* | 6.95% | 2.16 | 24.38 | 8.86% | Now | Converted 9/30/22 LIBOR+4.993% | ||

| WFC-Q | 5.85% | 1.46 | 23.01 | 6.35% | 9/15/2023 | Fixed to floating LIBOR+3.09% | ||

| WFC-R | 6.63% | 1.66 | 24.73 | 6.71% | 3/15/2024 | Fixed to floating LIBOR+3.69% | ||

* Dec. 22 payment x 4

Source: Author’s spreadsheet

In doing this research, I found a candidate where the conversion will come almost a year sooner than for the Wells issue.

Goldman Sachs Preferred Series J (GS.PJ) (Quantum description) has been paying a fixed coupon of 5.5%, the lowest among the issues on the chart. As a result, it is trading slightly below its $25 liquidation preference price (chart) for a current yield of 5.6%.

Goldman Sachs is the world’s second largest investment bank, with assets of $1.56 trillion. Its Tier 1 capital ratio is strong at 13.26%.

Its preferred issues are rated one step below investment grade at BB+. Dividends are non-cumulative and qualify for the preferential tax rates of 15% and 20%.

Big Rise In Yield Coming

On May 10, dividends will change to the three-month LIBOR rate plus 3.64%. At the current LIBOR rate of 4.75%, GS.PJ would yield 8.39% if it sold at the $25 base price– a 289 basis point increase.

Forward curves show short-term rates rising, so the actual first payment under the new system is likely to be even higher.

Of the three main risk factors, two aren’t high.

GS.PJ can be called at $25 starting in May, but as long as it’s trading below that price, a call would add to total return.

Credit risk seems acceptable since Goldman kept paying preferred dividends even through the 2008 financial crisis. At that time, it sold $5 billion in preferred shares to Warren Buffett, which were redeemed three years later.

That leaves the third risk, interest rates.

What happens if the Fed funds rate goes back to zero, where it hovered most of the time in 2009-15 and 2020-21? The excess yield would disappear, so the price would decline well below 25. Nimble investors will have to be prepared to sell.

My guess though, is that the Fed won’t go back to capping rates near zero anytime soon. Right now, it is having a hard time engineering any kind of landing, soft or hard, as the labor shortage keeps wages growing and unemployment low.

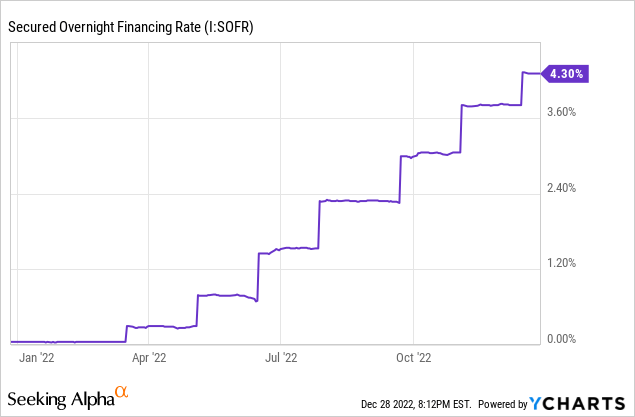

Effect Of LIBOR Shutdown

A complicating factor is that the Bank of England is sending LIBOR to the big piggybank in the sky in June, killing it off because it was subject to manipulation. The Fed has ruled that LIBOR will be replaced in financial contracts by the Secured Overnight Financing Rate.

SOFR should lag LIBOR both on the way up and the way down for technical reasons, and in neutral environments is likely to be slightly lower because it represents secured rather than unsecured borrowing. Still, it should follow the same pattern.

The forward curve shows SOFR is expected to be at about 4.9% in the spring. The curve remains above 3% as far as it goes, through 2033. That would mean a yield of at least 6.64% for GS.PJ–comparable or better than fixed-rate preferreds of high-quality banks usually yield.

So the most likely outcome isn’t a sharp decline. It’s more probable these fixed-to-floating issues eventually will be called as CFO’s decide they can refinance more cheaply with fixed rates. In that case, anyone who bought below $25 would get out with a small capital gain.

Another Goldman preferred (GS.PK), converts to floating a year later, in May 2024. Even though its terms will be slightly less generous, its price is still higher than GS.PJ because its expiring fixed coupon is greater. Expect the relative prices of the two to reverse in 2023.

Conclusion: GS.PJ is an excellent buy below $25 and remains buyable slightly above it.

Be the first to comment