ozgurdonmaz

As the most prominent American investment bank, Goldman Sachs (NYSE:GS) has been plagued by broader market headwinds. Yet, due to its involvement in various assets and markets and its unique ability to acquire and deploy capital, Goldman Sachs establishes itself for long-term success.

Investment Thesis

While I believe that Goldman Sachs is intrinsically undervalued, my long-term bullish view on the company is more contingent upon its capacity to strengthen its core businesses, scale its Wealth and Asset Management segments, and capture significant growth in digitalized products.

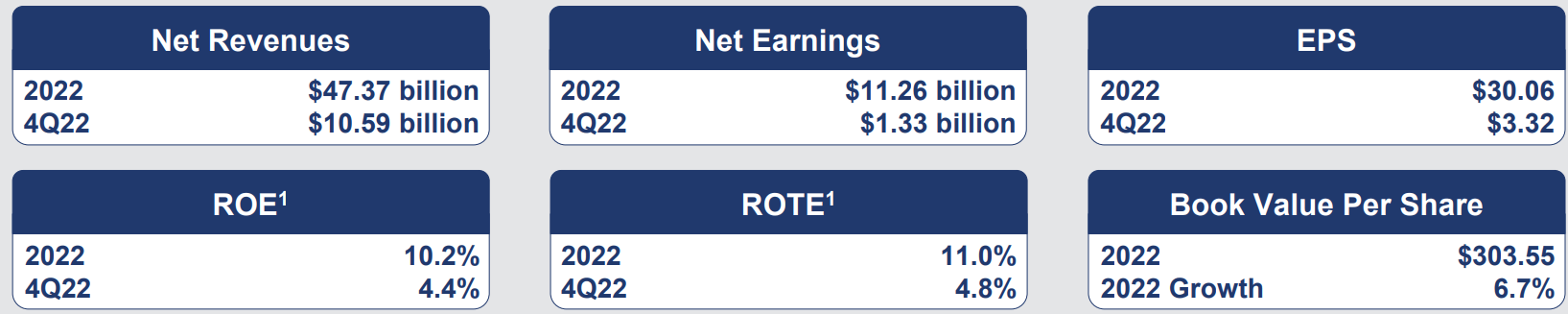

In the short to medium-term, I still hold a positive view of the bank, as its underperformance in Q4 2022 has led to an 8% drop in its stock price over the past 5 days. With Goldman Sachs’ fundamentals still solid, a reversion to the mean would yet be expected. Their Q4 earnings yet contained promising updates; the company experienced a 6.7% growth in their book value per share, increased FICC revenues, and elevated private banking deposits.

Goldman Sachs Q4 Report

Much of these results can be attributed to the macroeconomic backdrop Goldman Sachs is operating against- particularly rising interest rates.

And the company’s propensity to withstand said macro pressures, in combination with its laser focus on its core segments, ability to scale, and organic expansion into long-term opportunities is why I rate this company a buy.

Introduction

Goldman Sachs is a global financial services company, with a specific focus on investment banking- being the second largest in the world by net revenues. The company additionally operates across retail, commercial, and corporate banking, as well as wealth management, asset management, securities, and FICC intermediation and financing.

Goldman Sachs Investor Presentation

The bank’s $47.37bn and $11.26bn in respective 2022 revenues and net earnings can be divided among its three principal segments; Global Banking & Markets ($32.49bn in annual revenues), which includes investment banking and FICC/Equities intermediation and financing; Asset & Wealth Management ($13.38bn); and Platform Solutions ($1.50bn), which encompasses consumer platforms, such as credit cards, and transaction banking.

Valuation & Financials

General Overview

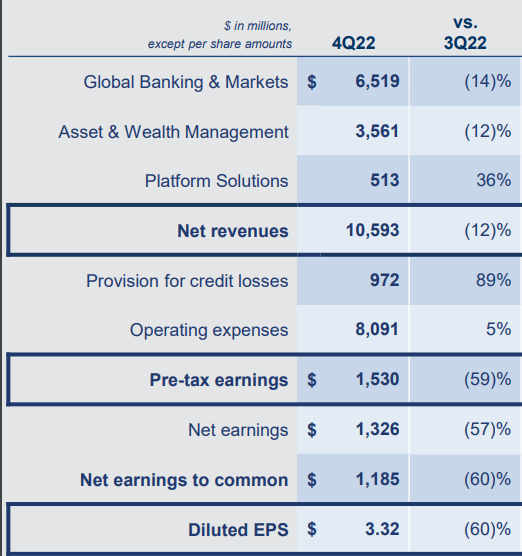

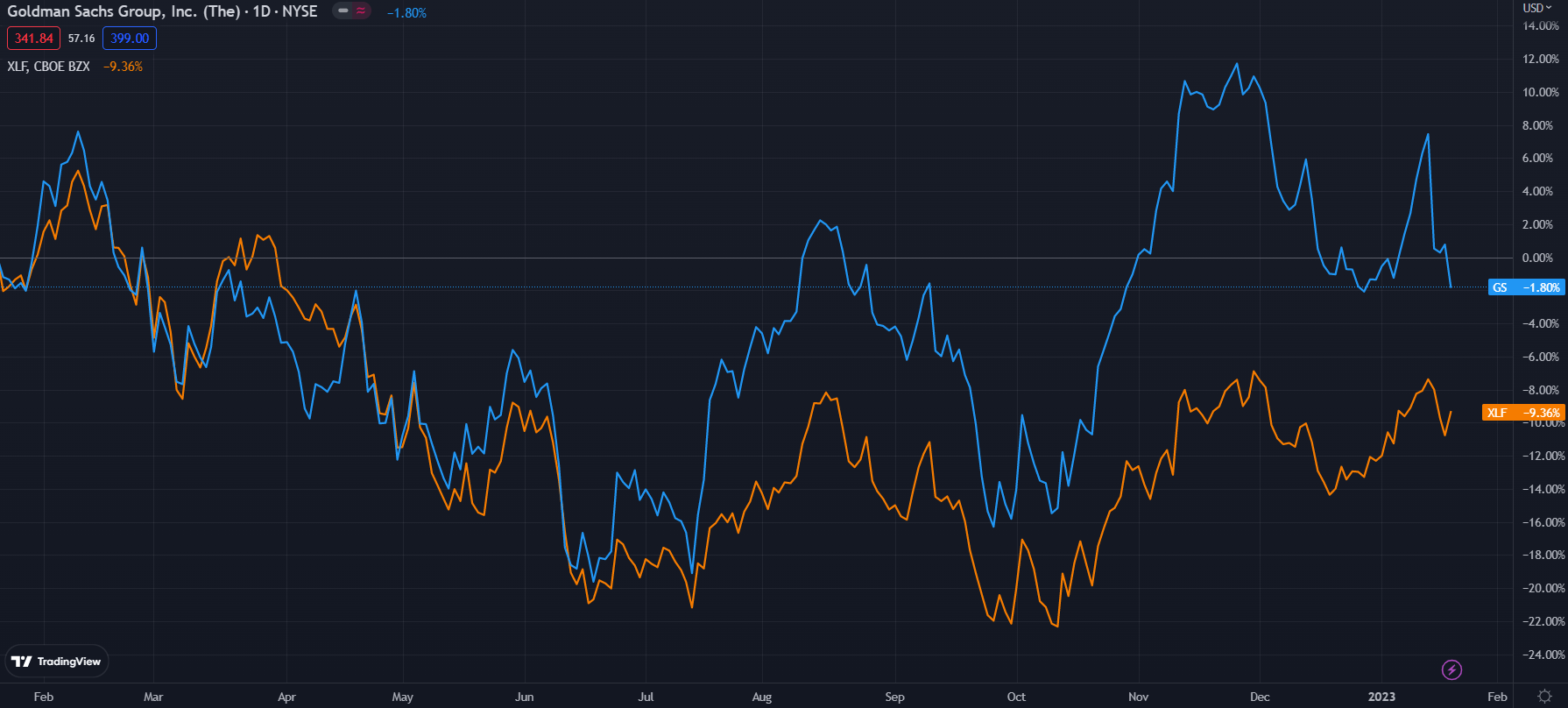

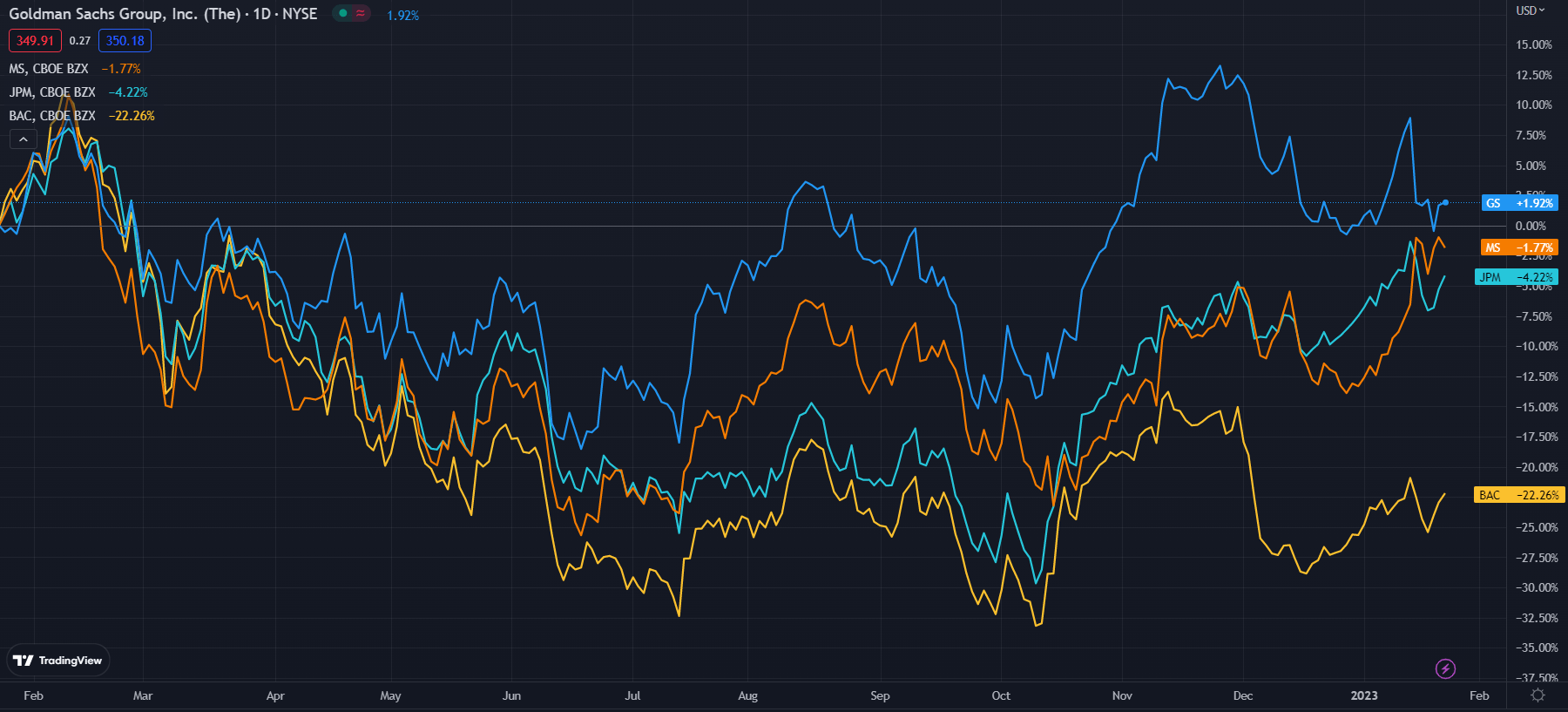

Coming off a poor Q4 performance due to macro conditions, Goldman Sachs has seen annual revenues decline ~20% YoY and pre-tax earnings down 50%. Although this trend has been reflected by a decline in their 1Y stock price (-1.80%), the bank is still performing better than the financial services index, XLF (-9.36%).

GS (Dark Blue) Performance versus Fin Services Industry (TradingView)

The dependence of universal banks, such as JPMorgan (JPM) or Bank of America (BAC), on credit spreads and traditional products such as mortgage-backed securities, which carry an inverse convexity to interest rates, have had greater material impacts on their respective balance sheets than that of Goldman Sachs or Morgan Stanley (MS), which tend to abstain from holding such products.

These measures continue to support Goldman Sachs’ core revenue streams; the bank sustains a price/cash flow ratio of 2.47- that too alongside a 2.63% dividend.

Comparable Companies

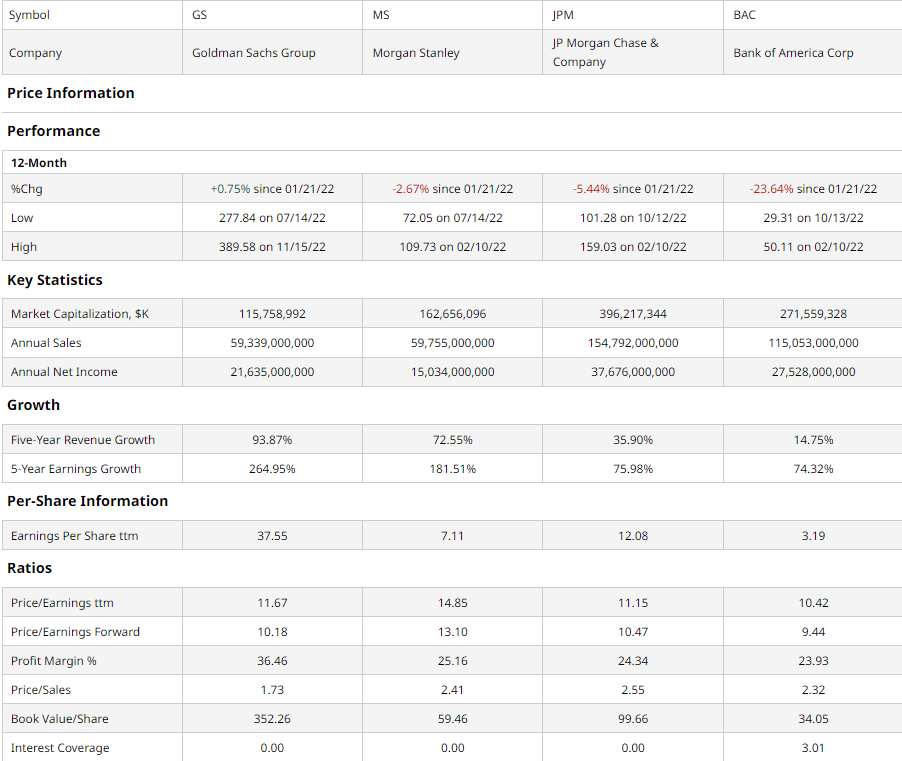

The relatively conservative landscape of the financial services industry has created a level of consistency in terms of industry competitors. Morgan Stanley, JP Morgan Chase, and Bank of America, as the companies with the greatest investment banking transaction volume asides from Goldman Sachs, comprise the company’s core competitors.

barchart.com

As I have demonstrated above, Goldman Sachs presupposes a superior value proposition to its peers, particularly considering its stronger revenue growth and organic margin expansion over the past 5-years. Subsequently, through all the headwinds I detailed earlier, Goldman Sachs maintains a greater profit margin than all its peers.

That margin comes in spite of $2.72bn set aside for provisions for credit losses- up $357mn from FY2021.

And evaluating the companies from a multiples basis, Goldman Sachs has a lower trailing and forward P/E, an undervalued P/S, and manifests greater book value per share.

GS (Dark Blue) Performance versus Competitors (TradingView)

Valuation

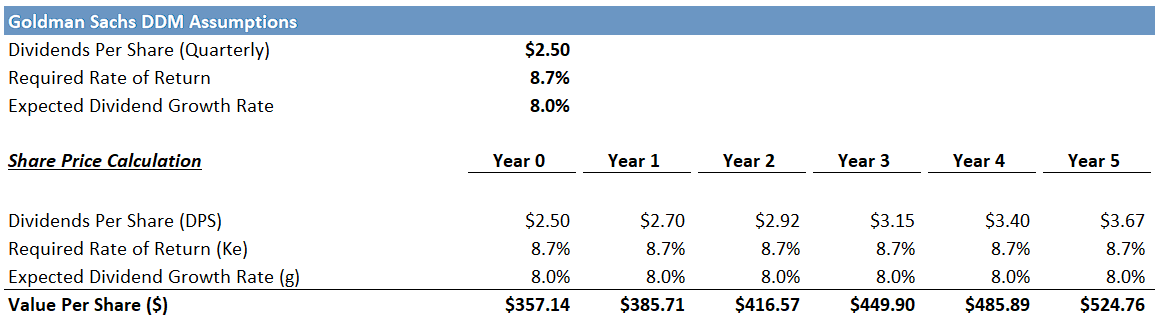

Due to the nature of Goldman Sachs as a financial services company, a discounted cash flow would misconstrue the true value of the company. Additionally, since the company has a limited number of direct competitors, both are attributed to the scale and universality of peer banks. As such, I will apply a dividend discount model/Gordon Growth Model to discern the fair value of Goldman Sachs.

Goldman Sachs Gordon Growth Model (Goldman Sachs Earnings)

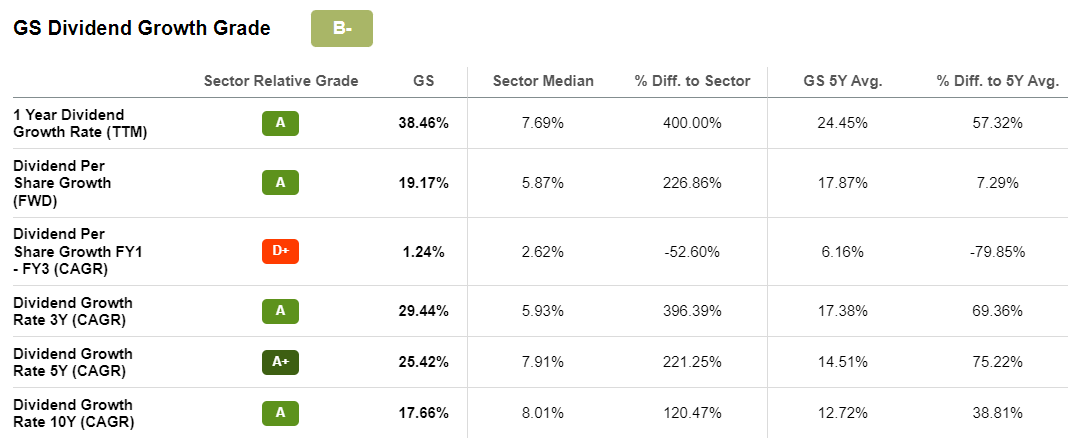

Walking through my model, it assumes a required rate of return of 8.7%, this is a reflective weighted mean of both the expected growth of financial services companies of similar sizes, as well as the capital cost structure of Goldman Sachs- taking into account their 8.3% WACC. Additionally, the dividend growth rate is extremely conservative- as you can see below, the bank has aggressively moved towards returning shareholder value through dividends.

Seeking Alpha

However, I find this conservative estimate adequate, with the RRR being similarly muted, thus only potentially undervaluing the bank rather than anything else.

Therefore I see Goldman Sachs as fundamentally undervalued by a minimum of 2.1%. However, this does not account for Goldman Sachs’ future strategy, as well as the expected 8.5% CAGR according to this model. Additionally, the assumptions within this model are perhaps overly prudent and the Gordon Growth Model is limited by its failure to account for shifts to dividends in the context of black swan events.

Corporate Strategy

Streamlined Business Practices

Goldman Sachs has zeroed in on their most successful business practices to accelerate margin expansion and sustain an edge of specialization and lead their industry. The company has recently divested from their ‘Marcus’ retail banking branch, reducing labour overhead and restricting personal loans on the platform.

By then focusing on and integrating its investment banking divisions, the company has achieved a level of synergetic growth and enhanced ROE of 15% on the back of interactions in merger advisory, acquisition bridge financing, and derivatives, amongst other actions. This strategy has been replicated across the company; Goldman Sachs’ wealth management and asset management have integrated their active management and fee structures, leading to growth in AUM and alternative assets offerings.

Expansion into High-Growth Opportunities

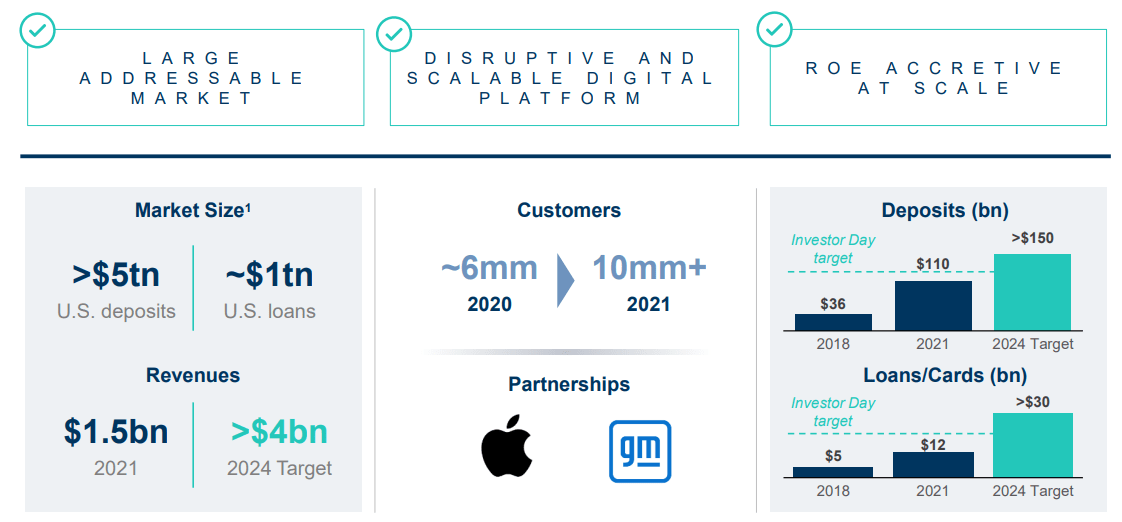

The company has further expanded into cyclical cash flow opportunities that both complement their core businesses while developing their revenue base. Labelled ‘Platform Solutions’, this segment of Goldman Sachs has experienced YoY net revenue growth of 177%.

The products encompassed by this segment include the company’s transaction banking and consumer solutions platforms. With the two markets containing over $5.2tn in potential deposit sizes, Goldman Sachs can foster growth in their AUM size and consequently support their fee structure.

Goldman Sachs Investor Presentation

The company has already secured deals with the likes of American Express, Visa, Apple Pay, and General Motors, essentially offering banking-as-a-service and handling the back-end of financing operations to support their core operations.

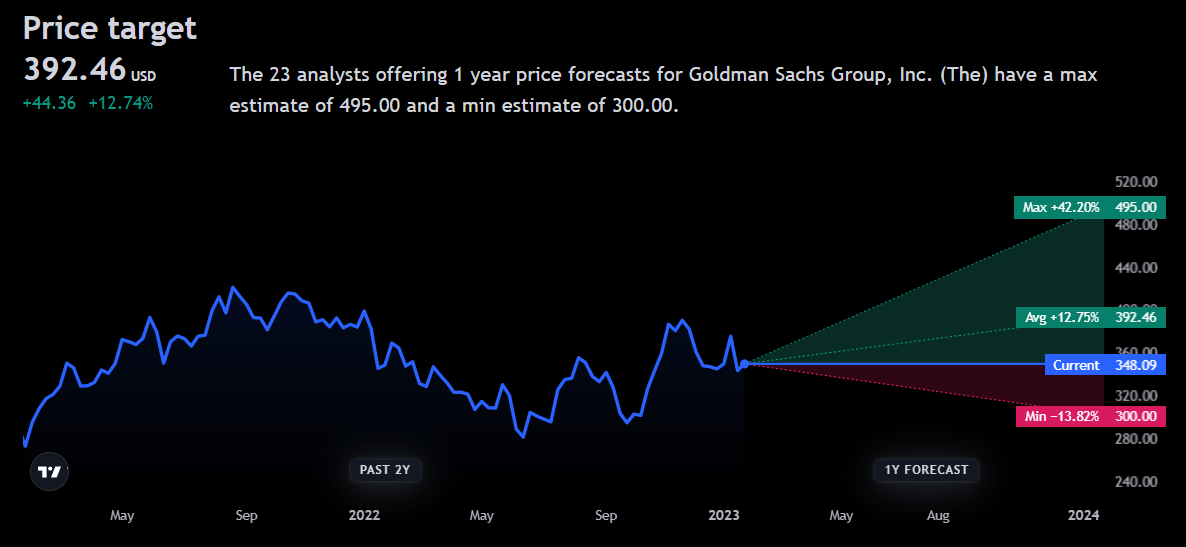

Wall Street Consensus

Analysts echo my positive outlook on Goldman Sachs, predicting an average price increase of 12.75% in the coming year, leading to a price of $392.46.

Goldman Sachs Earnings Forecast (TradingView)

However, analysts are cautious and thus price in potential volatility or continued recessionary pressures, with the minimum base price of the company predicted to be a -13.82% decline to $300.00.

Risks

Market & Liquidity-Based Financial Risks:

As a market-centric institution, Goldman Sachs is more vulnerable than other banks and companies to broad market impacts and uncertainties. Additionally, declining asset values and volatility can materially influence Goldman Sachs ability to acquire and execute IPO and M&A deals and generate profits through their asset and wealth management portfolios.

Rising Interest Rates:

As demonstrated by the compressed margins of the previous few quarters, interest rates are central to the general performance of the company; the ability to acquire credit and the demand for credit services and securities have faced a steep decline and can lead to levels of illiquidity in the general market.

Third-Party Interconnectivity:

Particularly in the intermediation of FICC and equities, Goldman Sachs plays a key role in connecting clients with capital. As such, they sustain significant exposure to third-party risk. The financial crisis of 2008 reflects the company’s connection to the broader financial markets well.

Conclusion

In the short term, Goldman Sachs presents a value play, being significantly cheaper relative to peer companies and able to sustain higher margins in spite of highly recessionary pressures.

In the long term, my analysis of their future strategy regarding Platform Solutions, AUM growth, partnerships with industry leaders, and ability to concentrate on securities, derivatives, and banking will lead to accretive growth and price appreciation.

Be the first to comment