lindsay_imagery

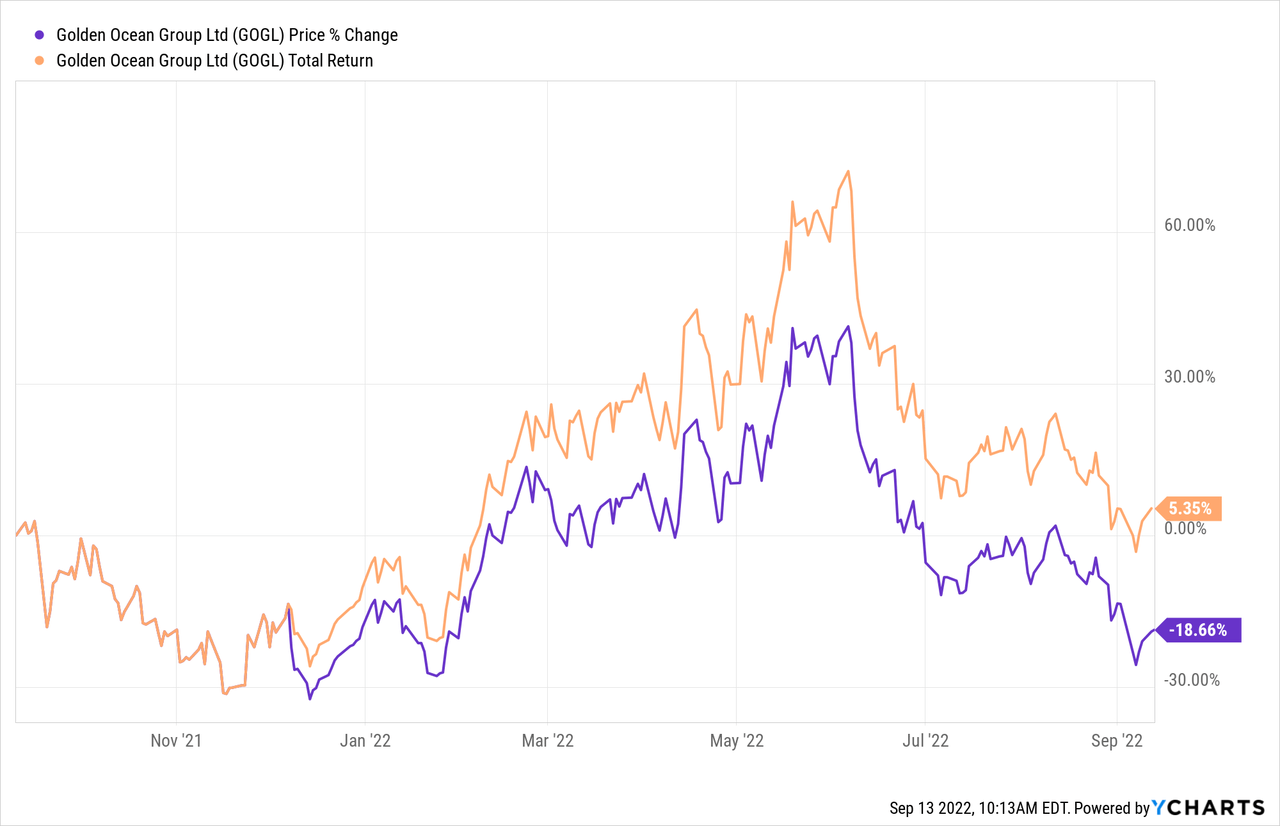

In our previous analysis of Golden Ocean (NASDAQ:NASDAQ:GOGL) we assigned a buy rating to the stock based on the premise of its excellent operational results. In this follow-up article, we assign another buy rating as we believe the stock’s general profile is conducive to the current market environment.

Furthermore, Golden Ocean’s second-quarter results reveal a trajectory that could coalesce with sustained dry bulk demand, resulting in continuous bottom-line growth for the company.

We assume a 6-month horizon and will revisit our rating in due course.

Factor Grades

I’d like to start proceedings by discussing the stock market’s year-over-year factor performances. Unsurprisingly, high-dividend yield stocks have outperformed amid global risk aversion.

The ongoing uncertainty among financial market participants means that high-dividend paying, highly profitable, and deep-value assets will likely outperform the broader stock universe for the time being. Therefore, we tout Golden Ocean as one of the frontrunners during the next six months as it’s one of the highest dividend-paying stocks on the market, with a forward dividend yield of approximately 26.09%.

Seeking Alpha

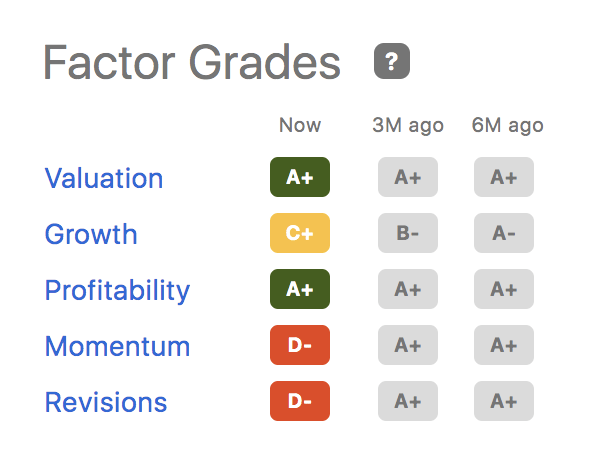

I wanted to incorporate a holistic factor analysis on Golden Ocean stock. According to Seeking Alpha’s factor grades, the stock exhibits sound value and profitability, which is exactly what you should be looking for in today’s shady market environment.

Golden Ocean’s Factor Grades (Seeking Alpha)

Looking ahead, I believe investors will favor high-dividend, deep value, and quality stocks. As mentioned before, it’s common for the market to seek out the mentioned characteristics during uncertainty as investors are unwilling to bear risks on unprofitable companies whenever the economic climate is gloomy.

Golden Ocean’s Operational Prospects

Commodities As An Influencing Factor

It’s critical to understand that Golden Ocean’s fair value is driven by the commodities sphere; the reason for this is twofold.

Firstly, the firm’s demand is very much reliant on the demand from commodity producers & traders. Therefore, wider profits in the primary sector equate to stronger demand for Golden Ocean’s vessels.

The second reason why the company’s value is linked to commodity prices is due to the fact that its assets are a culmination of metals. Industrial goods such as ships rise and fall in value relative to input costs. As such, Golden Ocean’s book value is likely to fluctuate parallel to the “built-up value” of its acquired vessels.

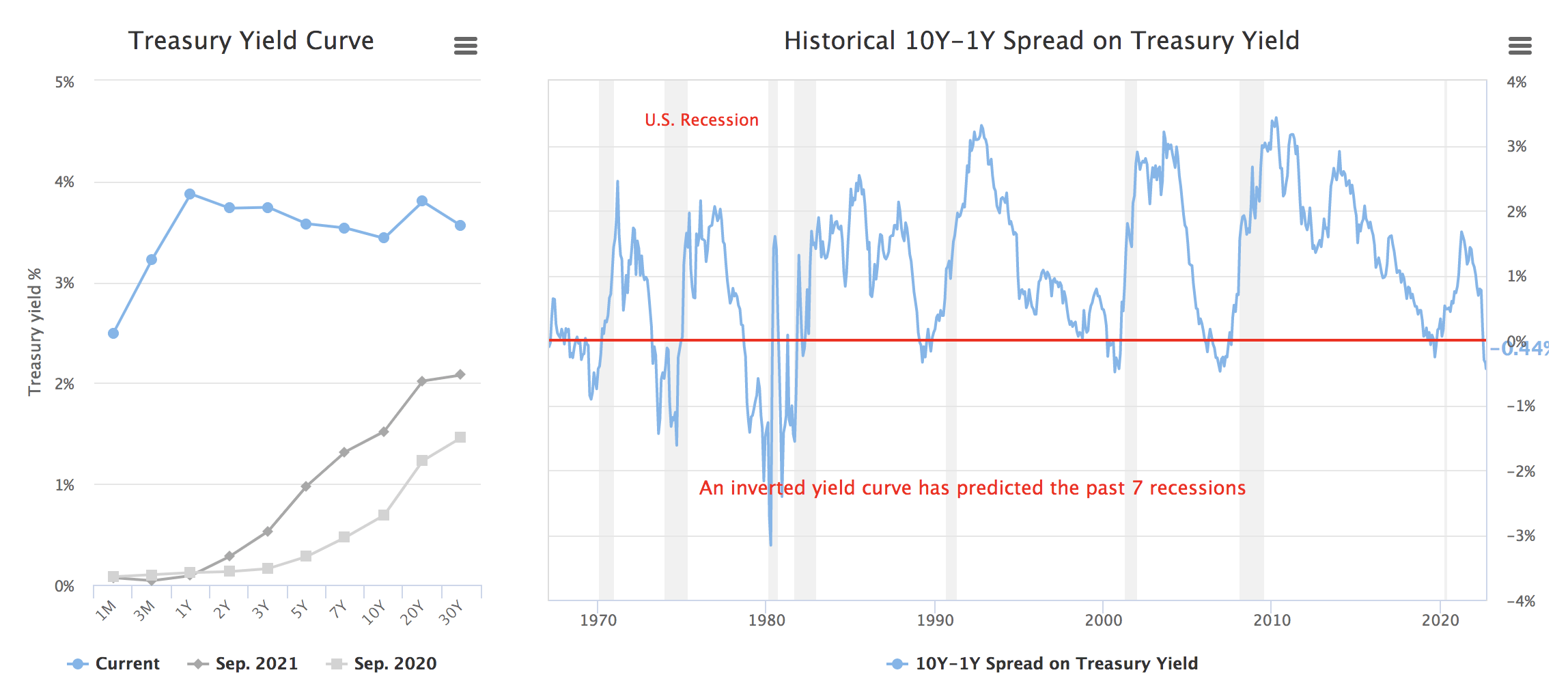

So, where do I think commodity prices will go from here on in?

It’s apparent that we’re in the late stage of an economic cycle amid slow global growth and high inflation. Commodity prices usually peak at late-stage inflation and subsequently recede as demand wanes. Based on the yield curve’s bearish flattening, it’s likely that commodity prices might plummet over the coming years before expansionary monetary & expansionary fiscal policies get implemented again.

So, in summary, I believe commodity prices will recede over the next few years.

GuruFocus

Company Idiosyncrasies

Everything about Golden Ocean suggests that it’s a “best in class” shipping stock. For instance, upon releasing its second-quarter earnings report, the company recognized the economic challenges ahead. However, it’s also anticipated that Golden Ocean’s capacity utilization will improve towards the back end of the year, which could see it rack up tremendous profits.

Additionally, in its previous financial quarter, Golden Ocean experienced exponential success with both its Capesize and Panamax vessels, which produced TCE rates (per day) of $30 661 and $27 581, respectively.

Golden Ocean

Much of Golden Ocean’s recent success derives from a global shift in dry bulk supply. Due to the European energy crisis (and reversion to coal), various Southern Hemisphere nations, namely Australia and South Africa have been responsible for supplying coal. Capesize vessels are the ideal vessels for long-distance transport of dry bulk, which I could see being a common trend over the following years.

On the flip side, I revert back to my earlier argument that global trade, and especially commodities trade, might slow down amid decelerating economic growth. Therefore, investors should bear in mind that Golden Ocean’s earnings growth remains on a knife’s edge.

Justified Valuation

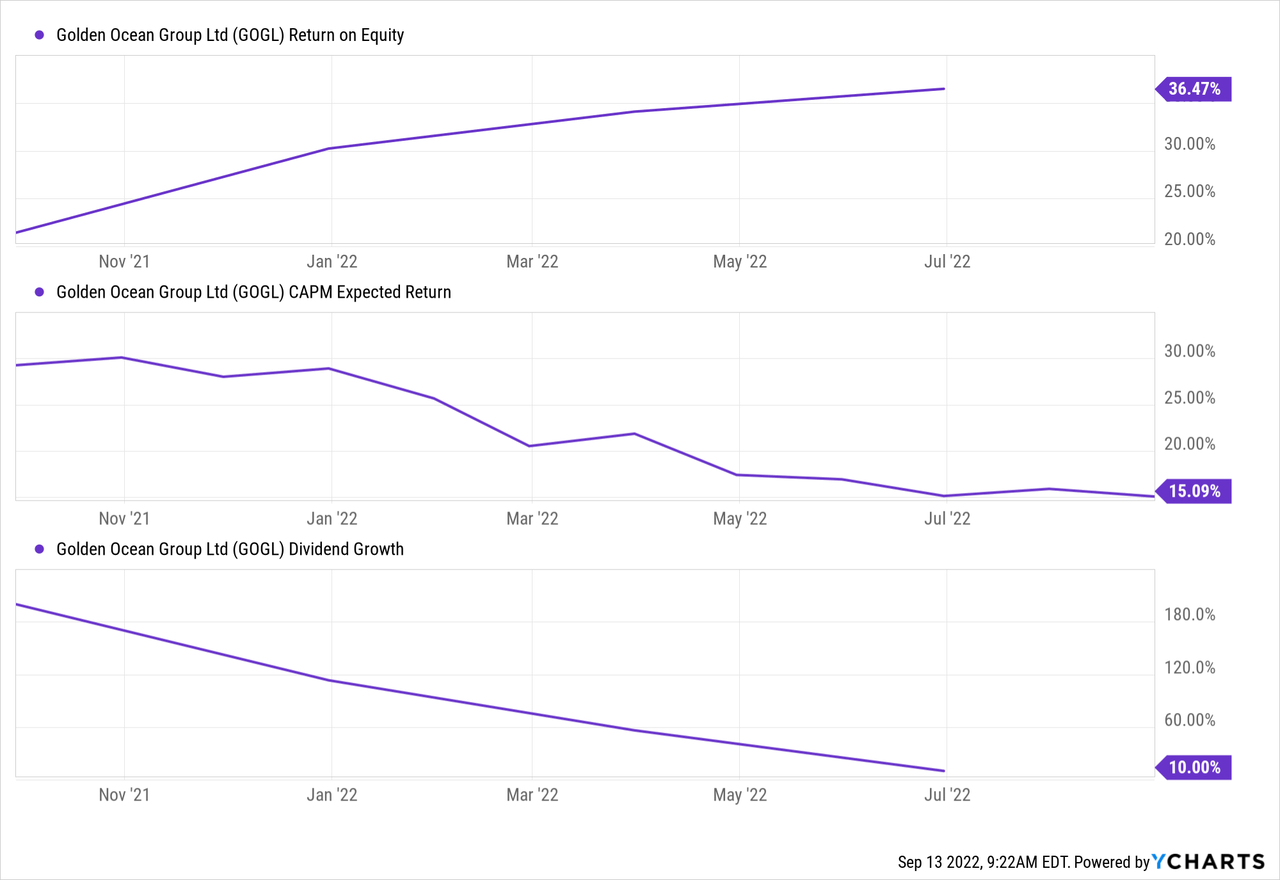

I used justified valuation metrics to value Golden Ocean’s stock. As a rule of thumb, the stock’s undervalued if your justified price multiple exceeds the financial statement price multiple.

I used the formulas below.

- Justified Price-to-Book = (Return on Equity – CAPM)/(CAPM – Dividend Growth Rate)

- Justified Price-to-Earnings = (Dividend Payout Ratio)/(CAPM-Dividend Growth Rate)

Apart from the company’s latest dividend payout ratio, of 90.10%, the diagram below conveys the plug-ins to the formulas above. Note that CAPM is an alternative term for investors’ required return on equity.

Based on my calculations, Golden Ocean’s justified price-to-book and price-to-earnings ratios exceed its market-based price multiples. As such, I declare the stock undervalued on a fundamental basis.

| Market Price-Earnings | 2.91x |

| Justified Price-Earnings | 17.7x |

| Market Price-Book | 0.95x |

| Justified Price-Book | 5.2x |

Source: Seeking Alpha & Author’s Calculations

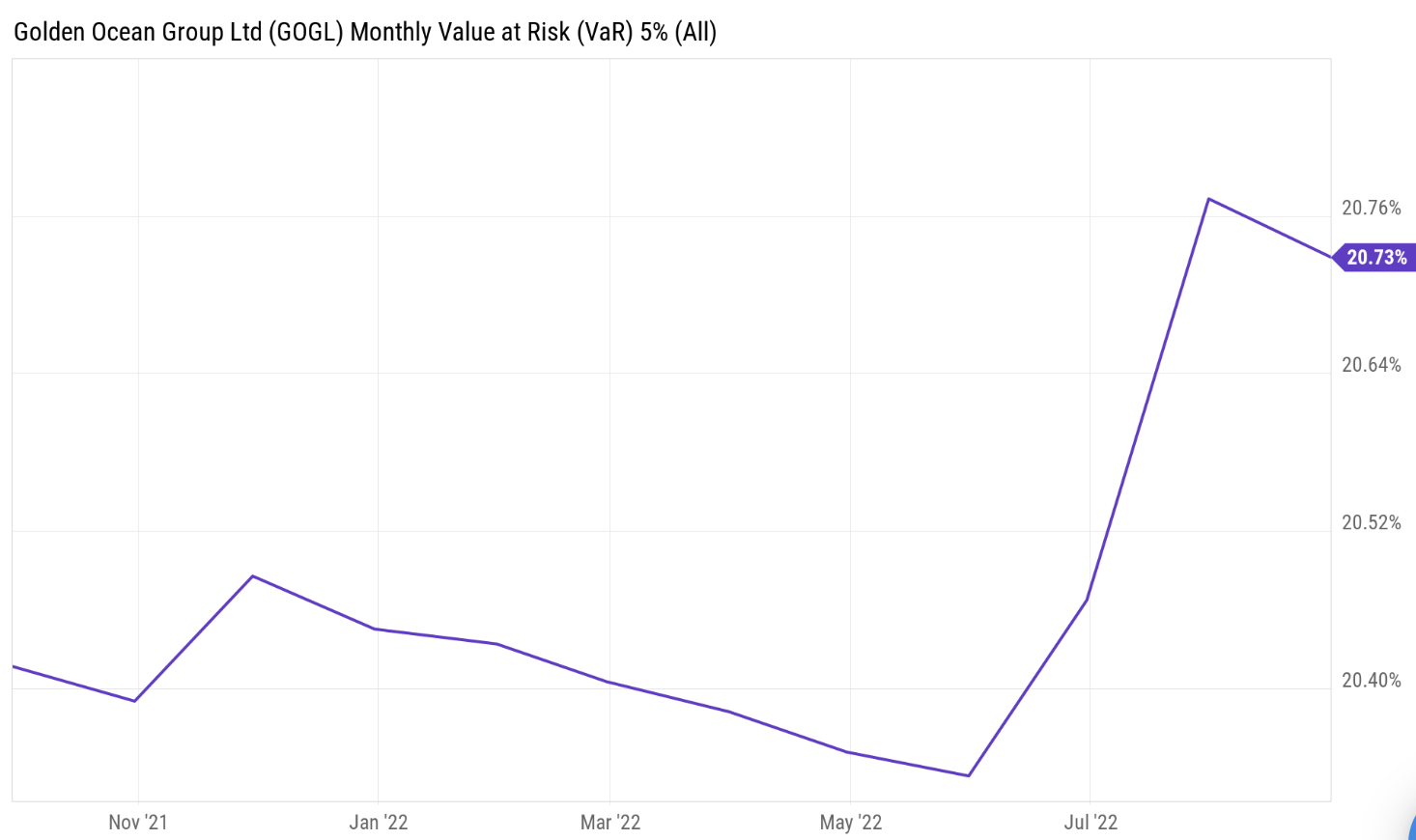

Although the stock is theoretically undervalued, investors should note that a prolonged bear market could mean my valuation metrics are in vain as the stock will likely turn into a value trap (if the bear market sustains for much longer). Additionally, Golden Ocean’s Value-at-Risk suggests that it can be an extremely volatile asset whenever systemic shocks occur.

Seeking Alpha

Concluding Thoughts

Although receding commodity prices could add downward pressure to Golden Ocean’s valuation, the stock is severely oversold. Justified valuation metrics, asset pricing tools, and an operational overview suggest that this is one of the best tactical buys on the market.

Be the first to comment