Pgiam/iStock via Getty Images

Introduction

“Global despise of wealth inequality is worse than poverty itself.”

The millennial old Chinese proverb above reflects today’s distress. The record stock market and global total debts are symptoms of extreme wealth inequalities closing on breaking points. The rich have never been richer, and the poor have never been poorer. To moderate this trend means to correct many past excesses of capital dominance. Prosperity for all people is the goal of humankind and a responsible government.

People prefer gold to preserve purchasing power

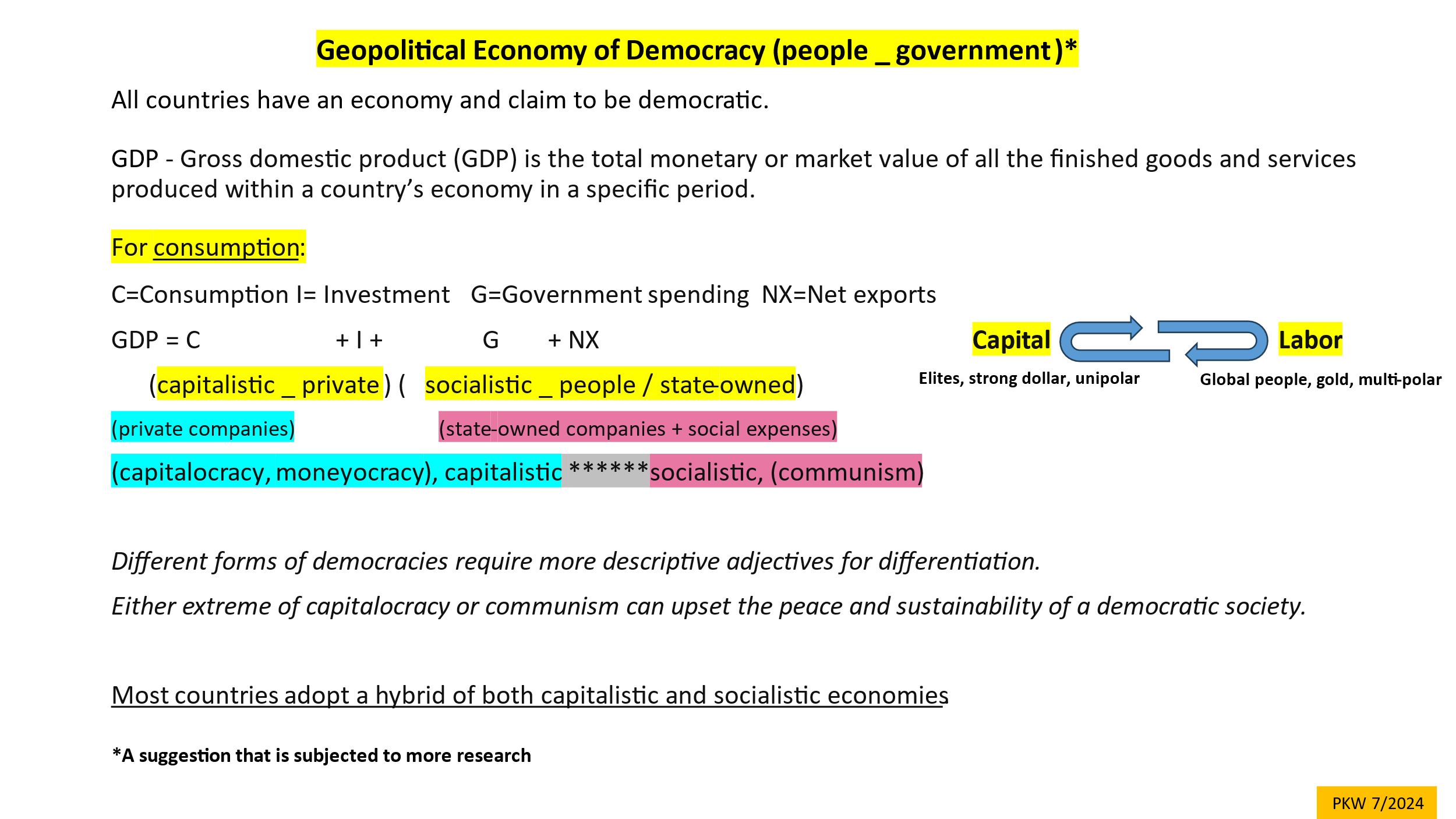

One common concept requiring reexamination is democracy, which has become capital-influenced in the West. The following discussion approaches the concept from an economic viewpoint.

pkw

A good house cost 300 ounces of gold in 1971, the same as today, which proves that gold can preserve purchasing power.

Pragmatic moderation to be tolerant of others is the key to gaining harmony among nations.

pkw

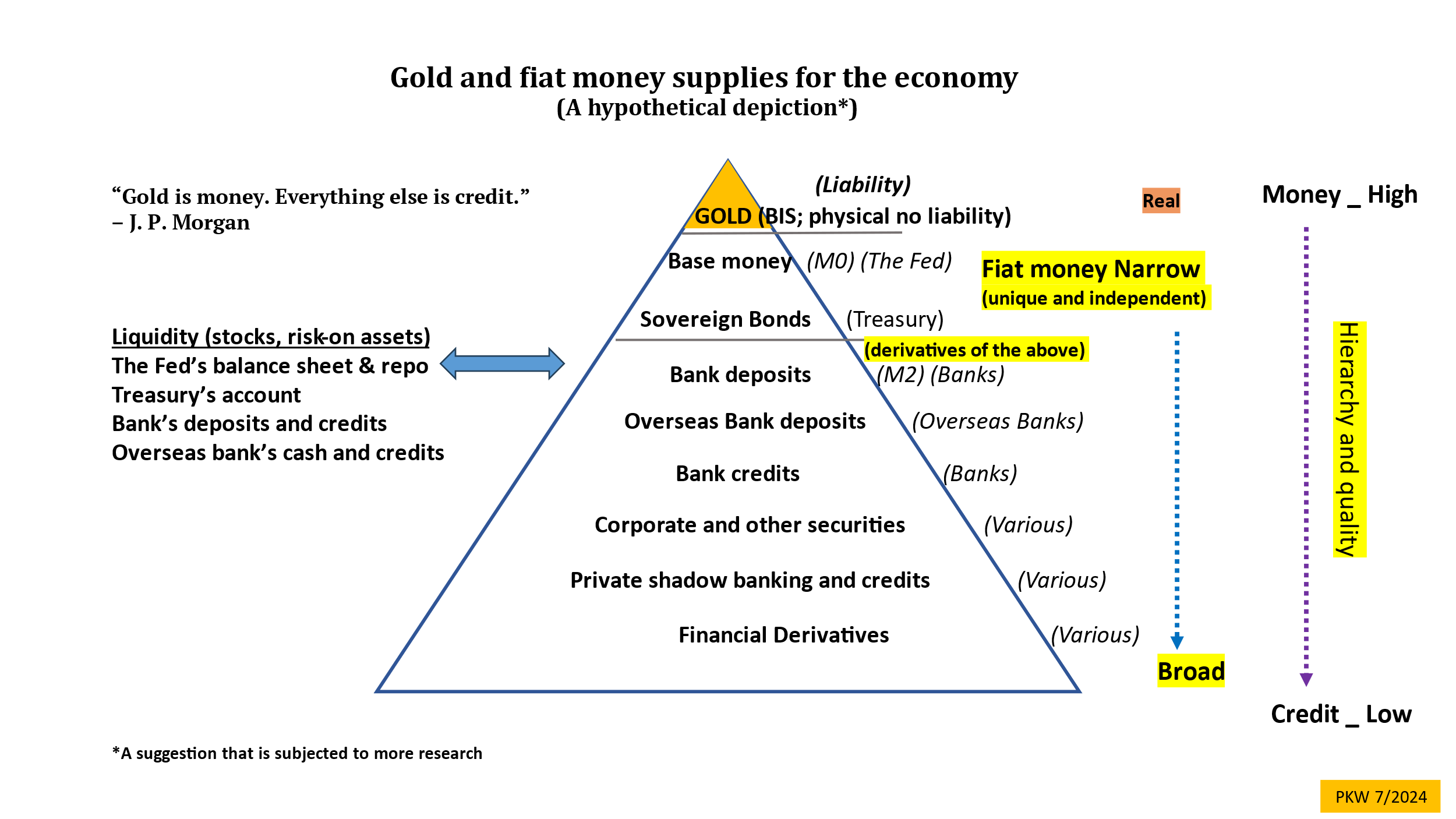

The fiat narrow money of currency and treasuries must be unique and different. The bank money and credits are derivatives of the narrow money. With the suspension of fractional bank ratio in 2020, bank credit creation has become the main source of growth for liquidity to boost risk-on assets such as stocks and real estate.

Internationally, other than in the G7 West, the central bank and treasury belong to the same department, which is liable for base money and sovereign debt. The narrow money supplies affect the economy, while liquidity influences the daily fluctuation of asset prices.

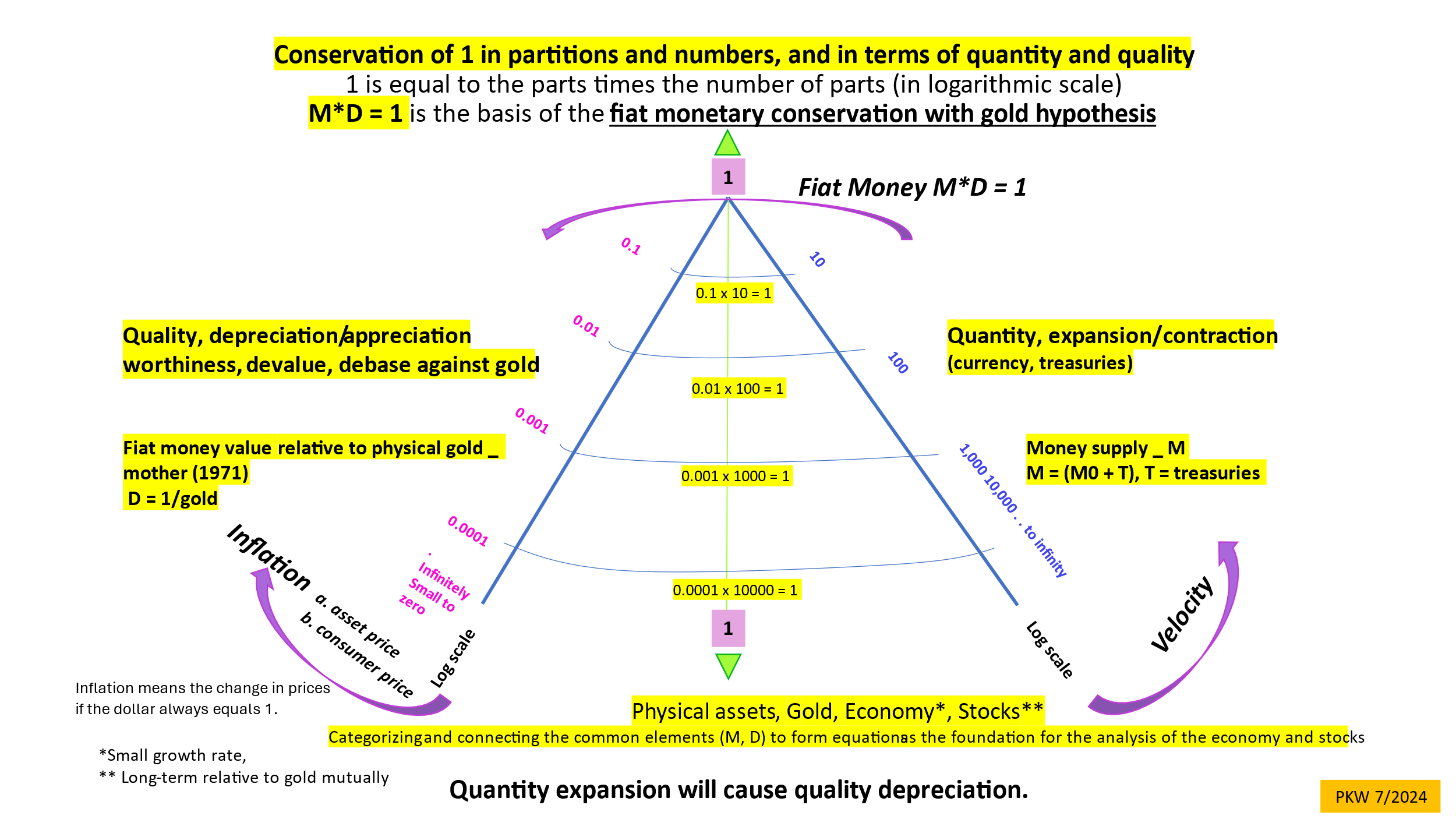

The following chart shows the need for discipline in expanding the narrow money supply, as quantity and quality are inverses of each other.

To fund the fiscal deficits, the expansion of treasuries affects the economy and assets. The quantity part can be shown as velocity, to measure the effectiveness of the narrow money expansion to the economy and stocks. The quality part can be displayed as inflation of assets and consumer prices if the dollar is assumed to be one.

pkw

The fast changes of the past years promote the status of treasuries as narrow money, accompanying and oversizing the base money (M0) of the Fed by over 10-fold. The dollar’s value as quality was pegged to gold before 1971.

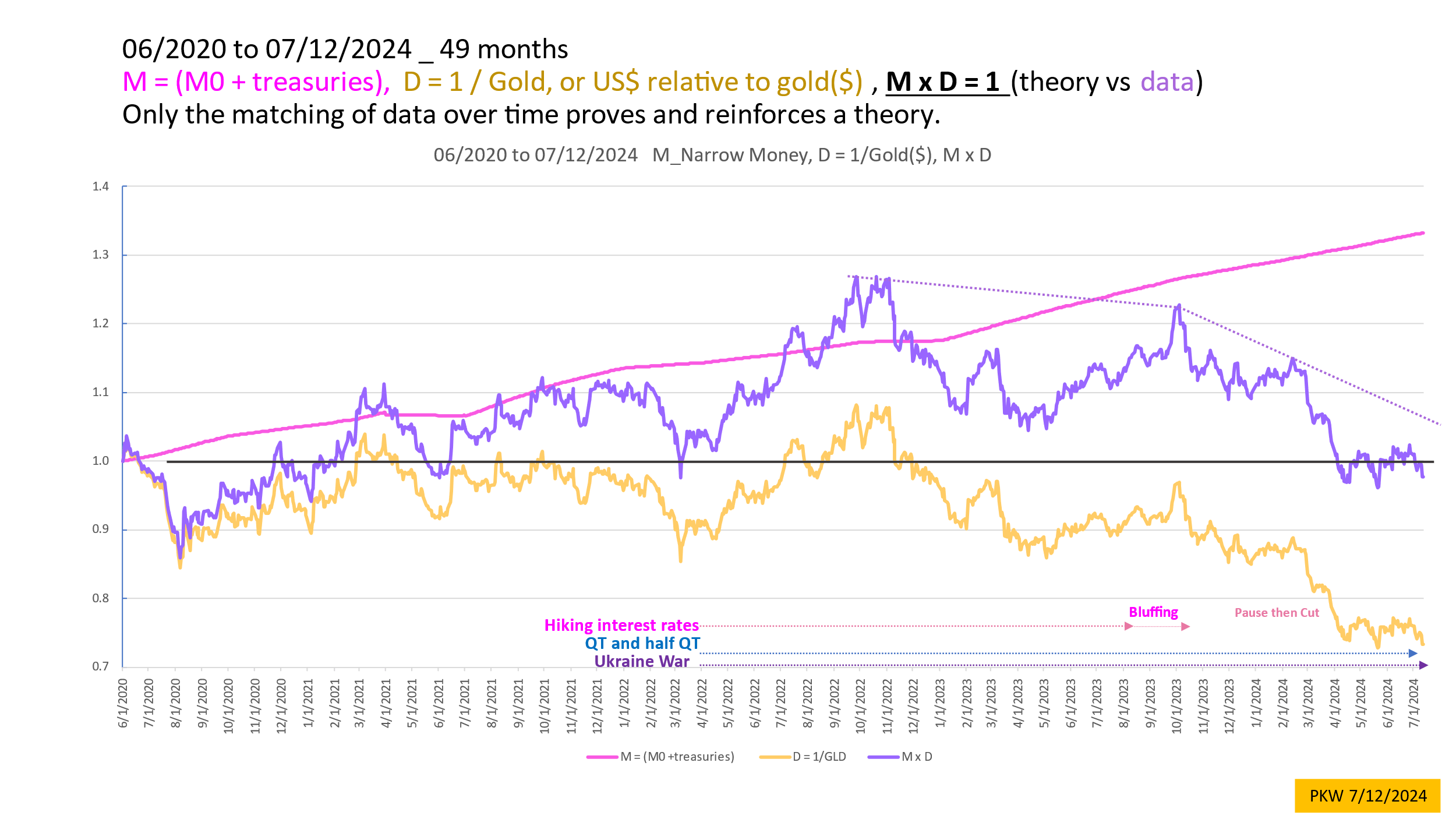

The fiat monetary conservation with gold equation involves the narrow money supply M and the dollar value in terms of gold or 1/gold. The two dissimilar factors compromise each other, as gold provides discipline. In the chart below, the self-adjustment can correct itself over time, as proof that excess money expansion will diminish its quality relative to gold. Gold will rise according to narrow money expansion in the long term.

pkw

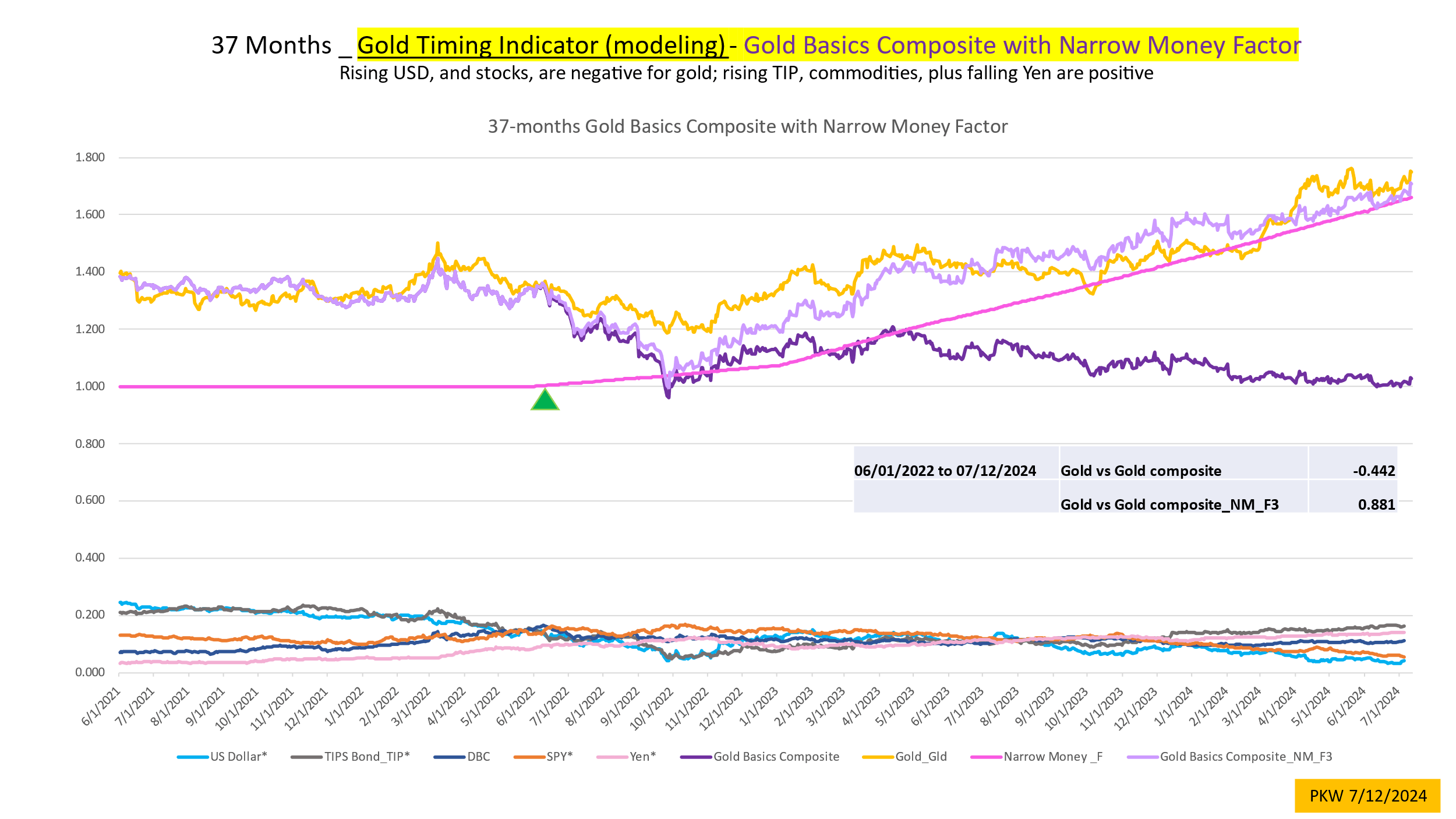

The chart below shows the quantitative modeling of the gold price. The model worked well previously but began to diverge with gold prices 2 years ago. I tried to change the modeling formula many times that resulted in vain. The daily price matching seems good. The problem suggests a missing monocline factor. Multiplying a narrow money expansion factor in pink for the last two years seems successful, as indicated by a higher correlation between the gold basic composite in lavender and gold.

pkw

Recent stock market developments

pkw

The root of the global problem is the rampant rise of national debts. These debts cannot be repaid by taxes alone, so more bond issuance as the expansion of narrow money will depreciate the value of its currency against gold. Japan is the latest example.

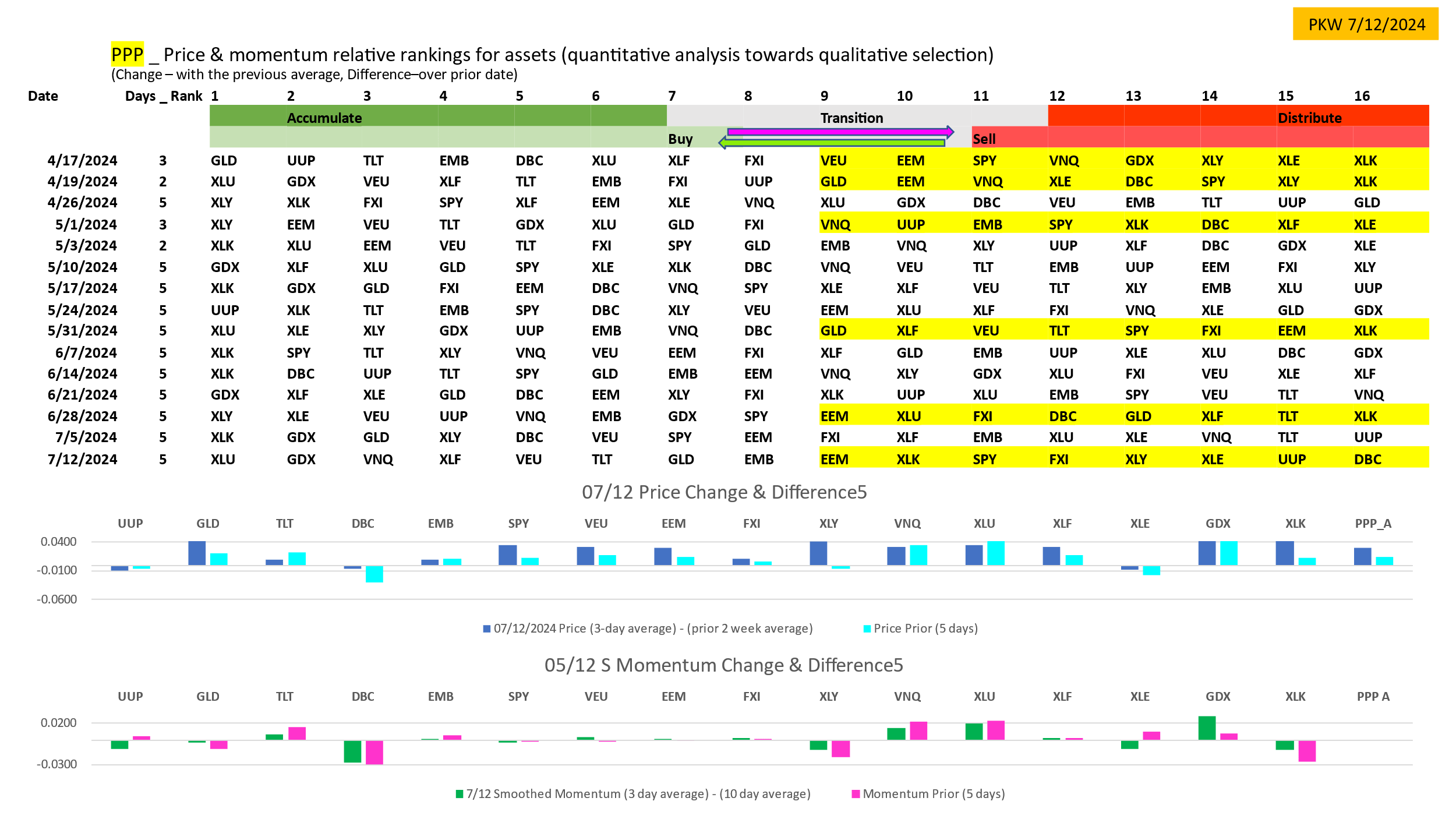

The relative ranking table shows the weekly sector rotations, according to price and momentum for timing purposes.

pkw

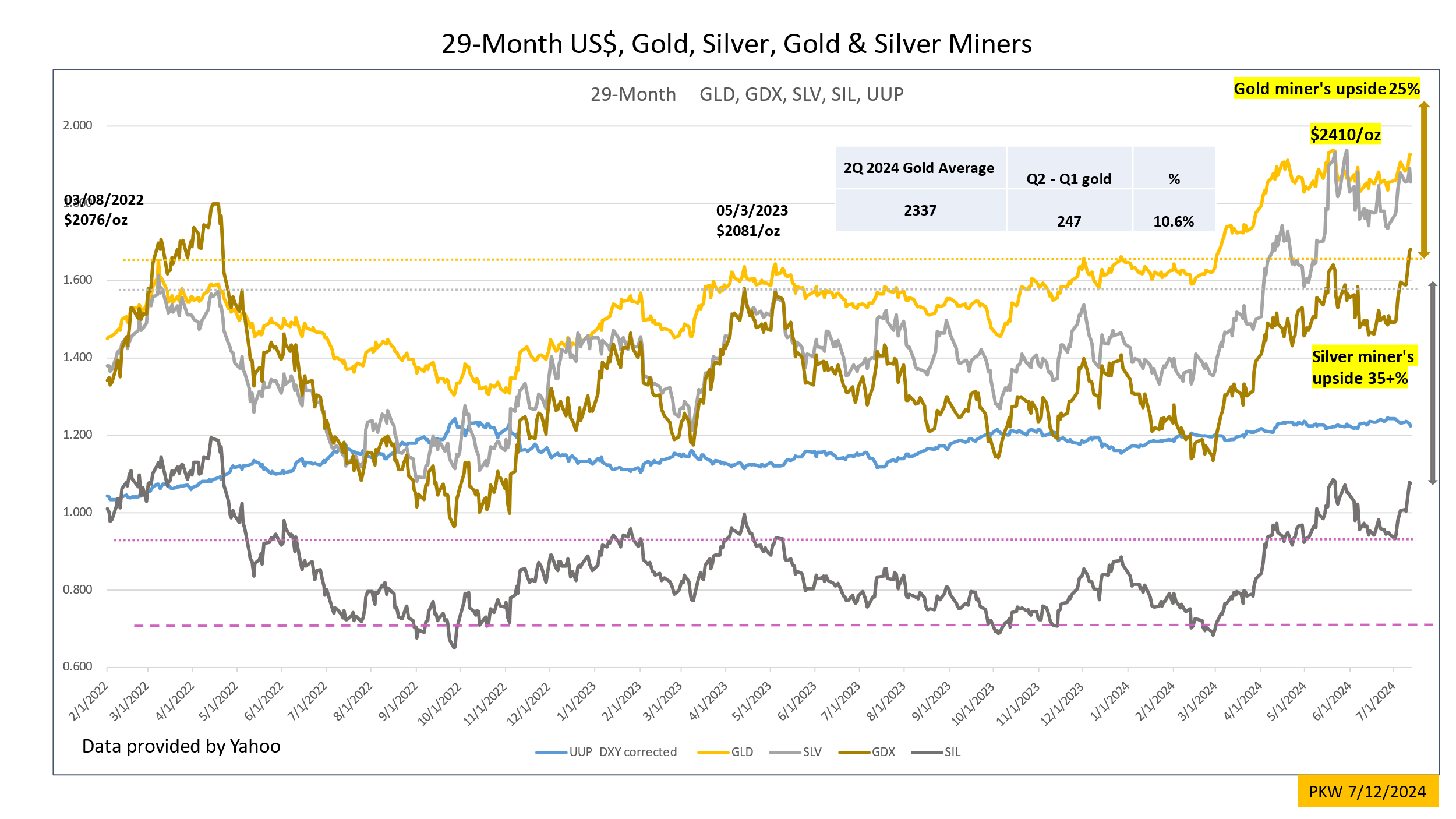

Gold and miners

The miners have been undervalued in comparison to rising prices. The potential for more gains is favorable till mid-September according to seasonality. The rise in second-quarter gold prices has been the strongest in the last year. The increase in earnings likely draws the prospective attention of fund managers.

pkw

Conclusion

The past corporate profit success based on neoliberalism, globalization, and modern monetary theory is facing stiff challenges today with higher interest costs.

Preserving people’s representation in the government, from further displacement by capital, is essential to prevent dissatisfaction among the middle class.

Gold will rise according to narrow money expansion in the long term.

The miners have been undervalued in comparison to rising second-quarter gold prices.

This article is for discussion only and is not intended for investment advice.

Be the first to comment