Davi Correa

Gol Linhas Aereas (NYSE:GOL) is one of the two largest Brazilian airlines.

I wrote hold rated articles on GOL in December 2021 (-52% since), and September 2022 (-24% since). Although the company is now trading at a market cap below that of the pandemic crisis, I still do not believe GOL is an opportunity.

The reason is that the company is far away from profitability figures that justify its current market cap, even making optimistic assumptions. Furthermore, I believe GOL’s expenses are understated with respect to Azul (AZUL), which makes its financials look better.

Note: Unless otherwise stated, all information has been obtained from GOL’s filings with the SEC.

Business

For a more detailed review, please read the articles from December 2021 and September 2022.

Undesirable industry: In general, airlines are not an industry where companies can be profitable. Fixed costs are high and that stimulates volume-based competition. Customers are savvy and look for prices. Regulators do not allow unprofitable competitors to leave the market.

Gol has a mixed strategy: Gol is supposedly positioned as a low-cost airline, and indeed it charges a lower yield per kilometer than Azul, but it also offers premium-like services like free food, entertainment in flight, and miles programs. I do not believe this is consistent.

Single aircraft model: Gol operates using only Boeing 787 (in different variations). This is supposed to provide operational advantages. I prefer Azul’s strategy of a differentiated fleet given Brazil’s diverse demographics.

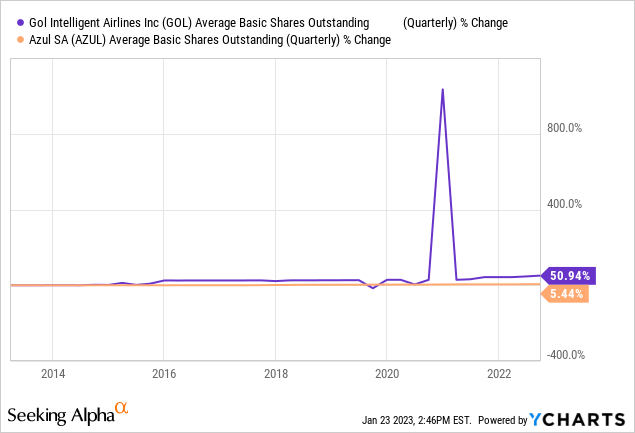

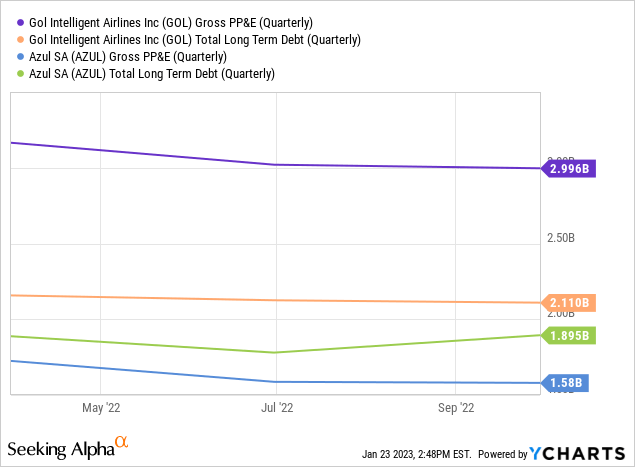

High debt and dilution: Both GOL and AZUL carry high levels of debt (about R$10 and R$12 billion each), but GOL has also issued shares in the last few years, diluting its shareholders. This has allowed it to carry a higher asset base than AZUL (second chart).

Recent developments

Recovery is still undergoing: Just like AZUL, GOL’s revenues are climbing, as well as its EBITDA margin. For the 9M22 period, the company more than doubled 9M21 revenues and reduced its operating loss from R$2 billion to almost operational breakeven. The 3Q22 quarter already presented a R$40 million operating profit.

Differing from AZUL, GOL’s traffic continues growing on a YoY basis as of December. However, GOL’s revenues are still below those of AZUL.

In terms of unit profitability, passenger-kilometer yield minus the cost of average offered seat per kilometer currently stands at R$0.09, above the negative values seen in 2021.

Debt and CAPEX still underway: While AZUL has taken a more conservative attitude in terms of CAPEX and debt, GOL has been more aggressive. The company issued shares to American Airlines for $200 million in capitalization in June, and it has signed agreements for $80 million in financing for engines and issued notes for $200 million, still not in the company’s books as of 3Q22.

Comparing AZUL and GOL

EBITDA margin: At the EBITDA level, AZUL seems to be more profitable, with margins averaging 30% for the 2016-2020 period, compared with margins of 25% for GOL, according to the company’s fundamentals spreadsheets (GOL and AZUL).

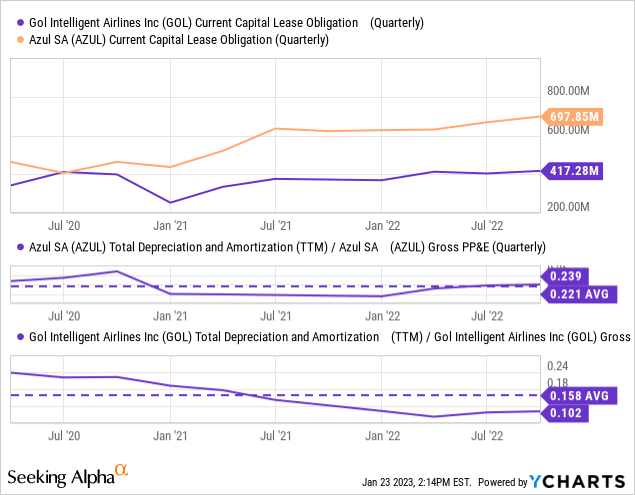

Lease financing rates: The companies differ greatly in the expense paid for their leases, for two reasons. First, AZUL has more of its fleet on lease compared to GOL. But most importantly, GOL’s rates are lower than those of AZUL. While GOL’s lease rates without purchase options stand at 12.5%, those of AZUL reach 21%. In a competitive industry like leasing, these should converge. The rates were close to 10% for both companies in 2019 (GOL and AZUL).

Depreciation rates: In this realm again AZUL is less favored. AZUL is currently depreciating at twice the rate of GOL, and on average it has depreciated about 40% faster than GOL.

Valuation

Even without normalizing AZUL with GOL (given that I consider both companies not an opportunity) I will show that GOL is far away from delivering acceptable profitability. If it cannot deliver with current financials, even less so if they converge with those of AZUL.

Similar to what we did with AZUL, we assume income tax rates of 35%. In the case of GOL, we will assume an EBITDA margin of 25% (more in line with the company’s average before the pandemic), lease and depreciation costs of R$2.8 billion (35% lower than those of AZUL), and financing costs of R$800 million (7% on R$12 billion in loans, mostly dollar-denominated).

Considering these assumptions, the company’s breakeven revenue level is R$14.5 billion, or about R$3.6 billion per quarter, about the level it posted in 3Q22. The company did not reach breakeven because its EBITDA margin was much lower than our assumption, only 17%.

Finally, in order to achieve a 10% return on its $620 million market cap, the company should generate R$16 billion in revenues, much closer than AZUL.

Again, these calculations assume a return to pre-pandemic EBITDA margins (not accomplished yet, while AZUL has reached those levels) and depreciation and interest rates on leases that are half those of AZUL. I do not believe that is sustainable. One of the two companies has an underestimated or overestimated fixed asset cost structure.

Conclusions

I believe that although GOL is trading at a market cap below that of the pandemic crisis, the company is still overvalued. The Brazilian market has already recovered and yet the stock is still away from profitability, even taking very optimistic assumptions (EBITDA margin recovery and fixed asset costs well below its competitor)

Additionally, one of the company’s most important costs, the cost of its fixed assets (through depreciation and financing cost of its leases) runs at half the rates of its competitor. I do not believe these figures can differ for long before one of the two companies has to adjust its assumptions. For that reason, I prefer AZUL to GOL, although again, both companies are overvalued.

Be the first to comment