Nils Jacobi/iStock via Getty Images

On January 10th GOOD announced a 20% dividend cut. For the last decade, GOOD has marketed itself to investors by stressing that it survived the Great Recession without reducing or suspending its dividend. For years every quarter on their conference calls the CFO or David Gladstone, the Chairman and CEO, would say as much. Below is the CFO’s statement from the second quarter call in 2022.

GOOD’s 2Q22 Conference Call

It is interesting to note on their last conference call they omitted this statement, which leads me to believe they at least had an inkling that their streak might end soon. As I noted in my piece from November (Gladstone Commercial Beats Estimates On $4.3 Million in Non-Recurring Accelerated Rents) there were plenty of signs that the business was under stress in the third quarter results.

I believe the style of the press release announcing the dividend cut, the positive business update on January 5th, together with GOOD’s announcement that they were authorized to purchase preferred shares in the open market on December 12th all indicate that GOOD was not expecting to have cut their dividend so soon. The headline of the press release which announced the dividend cut looked like every other dividend/conference call announcement the company has put out over the last several years. The only explanation that was provided for the dividend reduction was that it was prudent to strengthen the balance sheet in light of the economic headwinds. Why the change of heart from using capital to repurchase preferred shares less than a month earlier?

It does not appear they had a well-thought-out communication strategy. This stands in contrast to a REIT like SL Green (SLG) that included their dividend cut announcement in the title to their press release in December. Given that GOOD in their business update from January 5th stated that they collected all of their rents for 4Q22, had $35.6 million in available liquidity and on December 12th announced the authorization to repurchase preferred shares, something must have changed rapidly that impacted management’s comfort with or ability to pay the dividend. Since there was little information in the press release investors (or short sellers like me) are left to speculate.

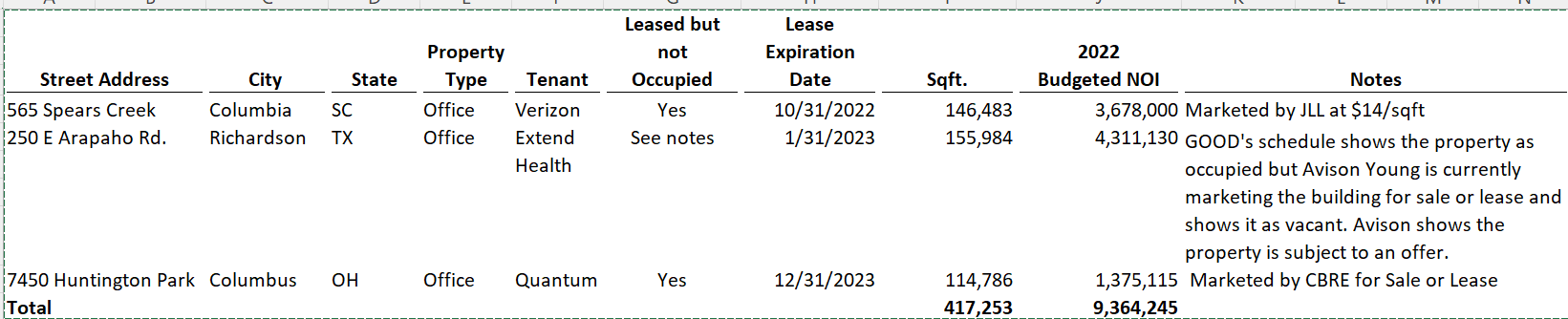

One possibility is that after looking at GOOD’s Q3 results, its lenders got nervous when they saw it made FFO through Accelerated Rents as I discussed in my piece published on November 28th. This could have led them to request that GOOD reduce its dividend. Another thought is GOOD, or its lenders based on updated projections saw that they would trip a covenant from their line of credit in the coming year and wanted to get ahead of the issue. Finally, GOOD has 7.4% of its rental revenue expiring in 2023 (GOOD’s 3Q22 Financial Supplement), in addition to the 2.7% it will lose with the expiration of the Verizon lease in Columbia, SC which I discussed in my last piece. It is possible they recently received some bad news on tenant renewals, or a new lease fell through that they thought was going to back fill an upcoming expiration. The below table, which is based on Schedule 6.25 from GOOD’s Fourth Amended and Restated Credit Agreement dated August 18th, 2023, highlights some of GOOD’s leasing challenges for 4Q22 and the coming year.

GOOD’s Fourth Amended and Restated Credit Agreement

(Links to marketing material from various brokers, 565 Spear Creek, 250 E Arapaho, 7450 Huntington)

While many of GOOD’s supporters on Seeking Alpha and elsewhere say it’s great that it cut the dividend, and now it will retain more capital and its Price FFO ratio is extremely attractive, what they are missing is GOOD’s FFO is unlikely to remain at its current level. Unlike most REITs GOOD does not provide guidance. However, it is wishful thinking to believe that if they and their lenders were internally projecting FFO in line with current analyst estimates of $1.61/share that they would be cutting their dividend.

It is also interesting to note that in the past (see GOOD’s 2016 10-K) GOOD has provided a partial credit to offset its incentive fee to ensure the dividend did not trip a line of credit covenant. Their most recent amendment to the management agreement provides for a two-quarter waiver. Perhaps GOOD is embarrassed by its inability to pay its historical dividend, and that is the reason for the suspension. I think it is more likely they either know they will not qualify for an incentive fee in the coming quarters, or their lenders told them as the business goes through a rough patch and your ratios are tight, we do not want to see you receiving any incentive fee.

Risks to Shorting GOOD

It is important for readers to understand that despite the problems I believe GOOD faces in 2023, the stock is very volatile as its investor base turns over. This means any number of things could cause the stock spike price to spike temporarily. A short seller without sufficient capital could be forced to liquidate their position at a loss in this scenario. It is easy to envision circumstances where GOOD’s stock price rises rapidly on perceived good news, For example, GOOD could report the sale of an asset at a substantial gain or they could use accelerated rents or termination fees to exceed analysts’ estimates like they did in 3Q22 as was discussed in my last piece GOOD. Alternatively, they could announce an arrangement with their line lenders that the market views as a benefit. Additionally, GOOD will likely continue to pay its reduced dividend until its lenders tell them they need to stop. Not only does the dividend represent a cost to a short seller, I believe the dividend will put a floor on the stock price for some time as there will always be investors who are seeking yield. In other words, I believe someone shorting GOOD needs to have the patience and capital to wait until the market has a clear and informed view of GOOD’s projected 2023 and possibly 2024 FFO/share.

Additionally, short-sellers need to be prepared for the possibility that if GOOD successfully leases some of their vacant office space in Columbia, SC at attractive rates, the stock could move upward.

Conclusion

In conclusion, I do not think the bad news is over for GOOD’s shareholders. They will have a challenging year coming up with lease expirations at vacant office properties and a management team that was slow to realize or communicate that they had an unsustainably high dividend. I expect additional selling will occur as analysts lower their estimates as they contemplate the reasons behind the dividend cut and GOOD’s upcoming lease expiration schedule.

Be the first to comment