Natali_Mis

Nobody likes a dividend cut, and that’s why Gladstone Commercial’s (NASDAQ:GOOD) stock sharply sold off at a time when REITs in general are rising in value. However, it’s important to look at underlying reasons behind a cut and the valuation, as a drop in price can result in a buy signal. In this article, I highlight why GOOD appears to be attractive at the current price despite a dividend cut, so let’s get started.

GOOD Stock (Seeking Alpha)

Why GOOD?

Gladstone Commercial is an externally managed REIT that focuses on acquiring, owning, and operating net leased industrial and office properties throughout the U.S. It’s led by CEO David Gladstone, who has been with the company since inception nearly 2 decades ago. Today, it owns 137 properties that are diversified across 112 tenants in 19 different industries and 27 states.

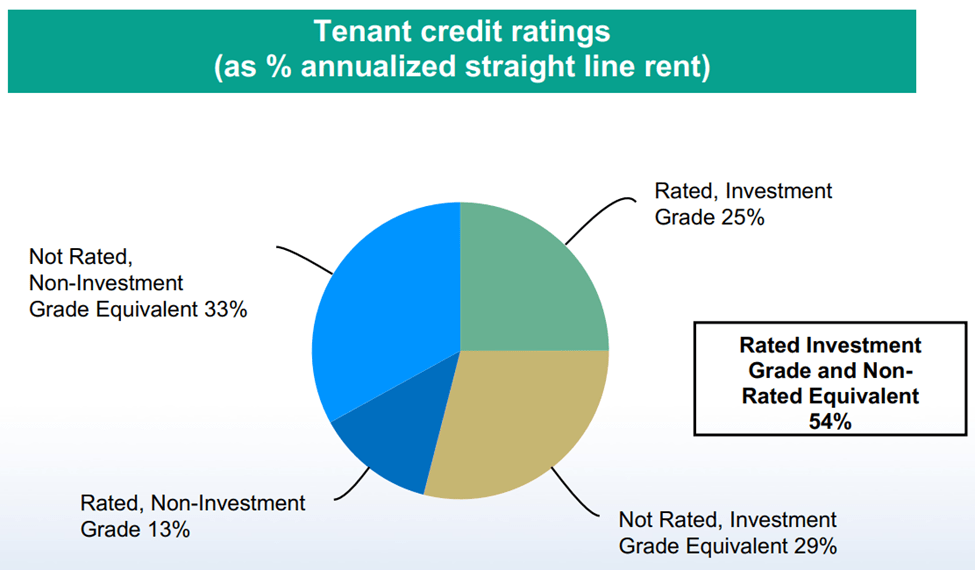

GOOD’s tenant base is spread across mostly defensive industries, with an even mix between public and private companies at a 48% to 52% ratio. Its top 3 tenants are Towers Watson, General Motors (GM), and Verizon (VZ). As shown below, over half of GOOD’s annual base rent comes from investment grade rated and non-rated equivalent tenants.

GOOD Tenant Ratings (Investor Presentation)

GOOD’s portfolio is one in transition, as it seeks to move a way from office properties, which represent 42% of its annual base rent, and towards industrial properties, which come with more attractive long-term growth prospects. This is reflected by recent industrial acquisitions totaling 362,000 square feet, including portfolios of properties in two New Jersey locations, one building in Jacksonville, Florida in a 20-year sale leaseback transaction, and a location in Alabama through an UPREIT transaction.

Notably, GOOD’s industrial allocation has increased from 32% to 54% since July 2021. This makes GOOD well-positioned to benefit from continued strong demand that outpaces supply in the industrial market. This was highlighted by management during the recent conference call:

Despite headwinds indicating an economic slowdown, national industrial market remains resilient, albeit with slightly slowing fundamentals. Per Cushman & Wakefield, net absorption exceeded 100 million square feet for the eighth straight quarter, driving vacancy down to 3.2%.

Demand continues to outpace deliveries, and rising construction costs are driving the average industrial asking rates to new heights, up 22% year-over-year, which is the strongest growth rate ever recorded. National rents are poised to continue growing ahead of inflation over the next several months given the record low vacancy rate.

Supply chain, labor and inflationary pressures have delayed development schedules, contributing to a record high construction pipeline. The industrial market is expected to remain robust.

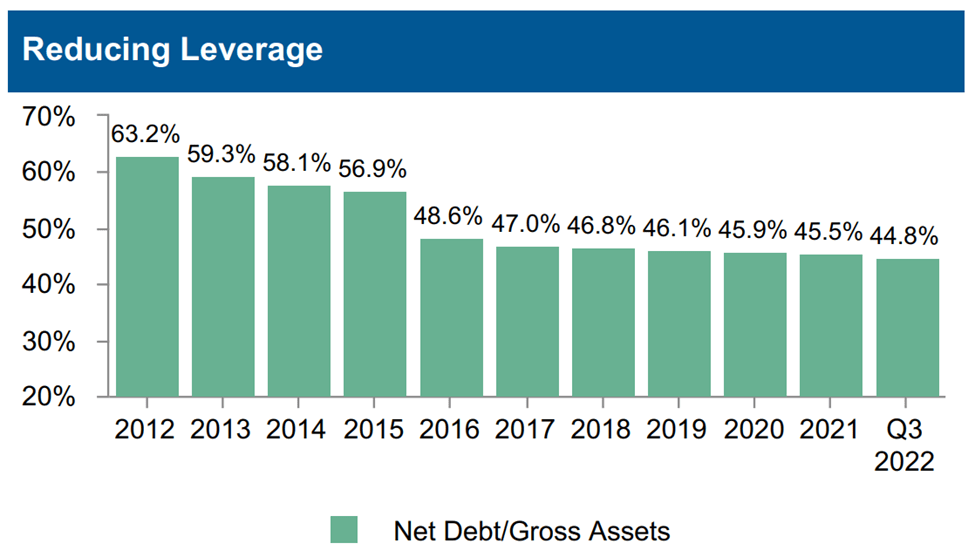

Meanwhile, management has hinted at strong portfolio fundamentals by sharing that portfolio occupancy improved by 50 basis points sequentially to 96.8% during the fourth quarter. Plus, GOOD maintains a reasonable about of leverage, with a net debt to gross assets ratio of 44.8%. As shown below, GOOD’s leverage has trended down every year over the past decade.

GOOD Leverage (Investor Presentation)

However, GOOD does have meaningful exposure to hedged floating rate debt, which comprise 49.5% of outstanding debt, while fixed rate comprises another 49.5% and pure floating rate represents 1%. While hedging helps, it’s not as secure as fixed rate.

With a pre-dividend cut payout ratio in the mid-90%’s, the dividend cut helps to free up financial flexibility for the company in a tough interest rate environment. At the current dividend rate of $0.10 per share paid monthly, GOOD carries a far safer payout ratio of 74%.

Lastly, GOOD has fallen back to value territory at its current price of $16.69 with a forward P/FFO of 10.3. Analysts expect GOOD to resume mid-single digit FFO/share growth next year, and have a consensus Strong Buy rating with an average price target of $19.50. This combined with the 7.2% dividend yield implies a potential 24% total return from the current price.

Investor Takeaway

GOOD’s diversified tenant base across mostly defensive industries, transitioning portfolio mix towards industrial properties, reasonable leverage and improved dividend safety are all positive points for the stock. While it does have significant exposure to floating rate debt, its hedging strategy helps to mitigate interest rate risk.

To be clear, GOOD isn’t a Realty Income (O) nor a W.P. Carey (WPC). However, it does throw off a much higher yield to compensate investors for higher risk. Considering all the above, I view GOOD as being a Speculative Buy for high yield.

Be the first to comment