ArtemisDiana

Ginkgo Bioworks (NYSE:DNA) Foundry business continues to grow, although visibility into downstream value capture remains limited. Ginkgo is becoming increasingly focused on the pharma and biotech vertical, which is a more mature segment and is better aligned with Ginkgo’s capabilities. The Biosecurity business may be a headwind over the next 12 months as COVID testing winds down. There creates a risk that investors will look at headline revenue numbers and dismiss Ginkgo as a company with large losses and stagnating growth. Investors will likely need to remain patient until Ginkgo customers have more commercially successful products and Ginkgo begins to realize significant downstream value.

Foundry

Ginkgo’s Foundry business continues to perform reasonably well, despite the shift in sentiment in the biotech market over the past 12 months. Reduced customer access to financing could impact demand for Ginkgo’s services in time, but Ginkgo has spun this as a positive, with customers potentially seeking to reduce costs by outsourcing development.

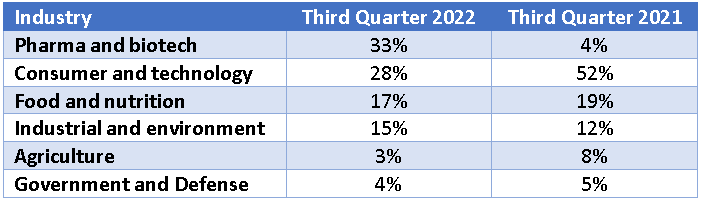

The pharma and biotech industry along with the food and ag industry segments have been areas of strength for Ginkgo, which is not surprising given that these verticals tend to be more aligned with Ginkgo’s strengths. Recent developments also suggest that these verticals are likely to become increasingly important for Ginkgo in the near term.

Table 1: Foundry Revenue Contribution by Industry (source: Created by author using data from Ginkgo)

For example, Ginkgo recently announced a collaboration with Merck (MRK) to develop enzymes using fungal strains. The project is focused on improving manufacturing processes and as such may have lower risk and a relatively fast path to value recognition. Ginkgo will engineer up to four enzymes that will be used as biocatalysts in Merck’s API manufacturing. Ginkgo will receive upfront R&D fees and will also be eligible for up to $144 million in milestone payments.

To support their pharma and biotech business, Ginkgo is acquiring Circularis, which has a circular RNA and promoter screening platform that will help drive their work in cell and gene therapy. Circularized RNA is much longer-lived in cells, which could improve its robustness as a therapeutic modality. It is hoped that the acquisition will enable new solutions across bioproduction, RNA therapeutics, cell therapy, and gene therapy partnerships. Following this development, Ginkgo announced a partnership with Esperovax to develop circular RNA-based cancer therapeutics. Ginkgo has been expanding their efforts in cell and gene therapy, with programs like improving adeno-associated virus manufacturing and the development of AAV capsids with altered tropism and immunogenicity.

Ginkgo recently opened Bioworks7, which increases their capacity in biopharmaceuticals, biomanufacturing and general mammalian programming for therapeutic applications. Bioworks7 is co-located with Bioworks4, Ginkgo’s other mammalian foundry.

Ginkgo also recently acquired Altar for their Adaptive Laboratory Evolution (ALE) platform. Altar has been focused on developing microorganisms for industrial applications. Its technology automates ALE, which helps adapt microorganisms to the conditions required by industrial companies. Ginkgo already had ALE capabilities, and this acquisition likely aims to extend these capabilities.

Ginkgo also recently announced a collaboration with Lygos to optimize and scale production of specialty ingredients. Ginkgo and Lygos will work on two programs over a 2-year period. Lygos’ organic acid targets are used to produce biodegradable formulations and polymer-based products used in consumer, agricultural, and industrial markets.

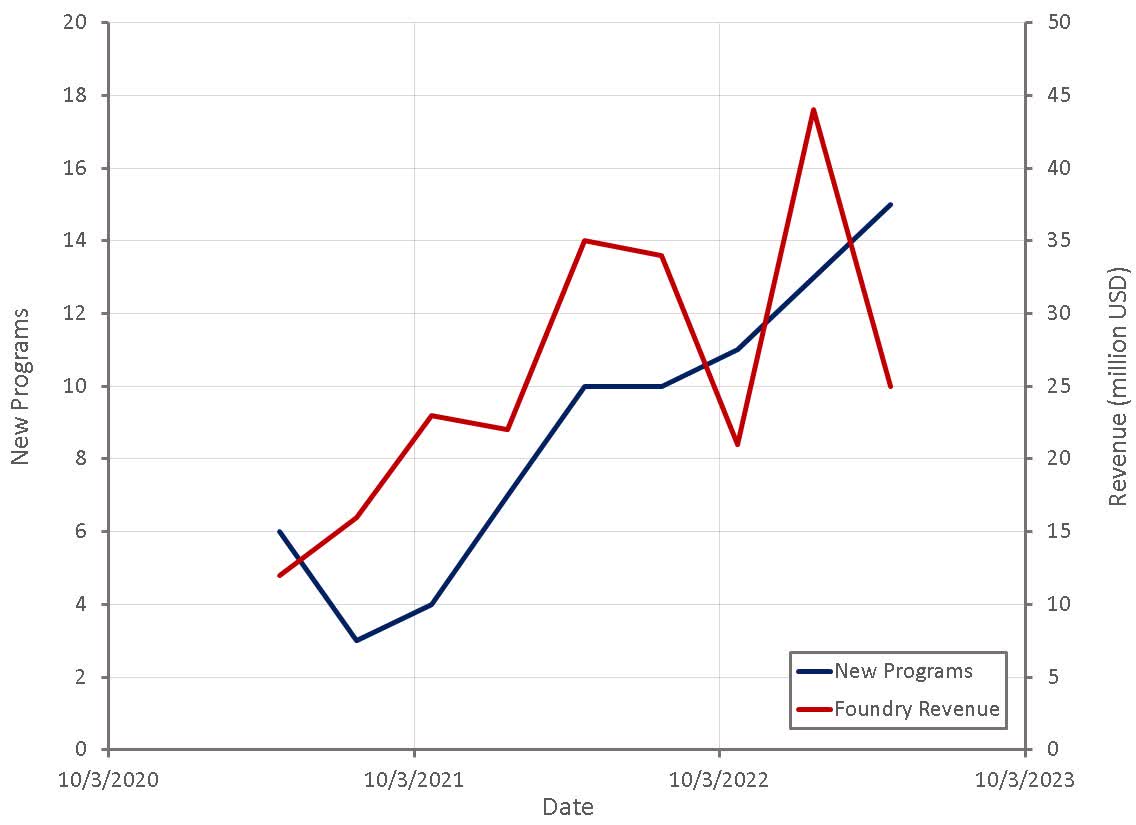

Gingko’s Foundry revenue continues to be lumpy, but is increasing over time. More importantly, they are adding new programs and the number of new programs is increasing. Given the company’s focus on capturing downstream value, adding new programs is likely to be a more important metric than short-term Foundry revenue.

Figure 1: Ginkgo Foundry Revenue (source: Created by author using data from Ginkgo)

Biosecurity

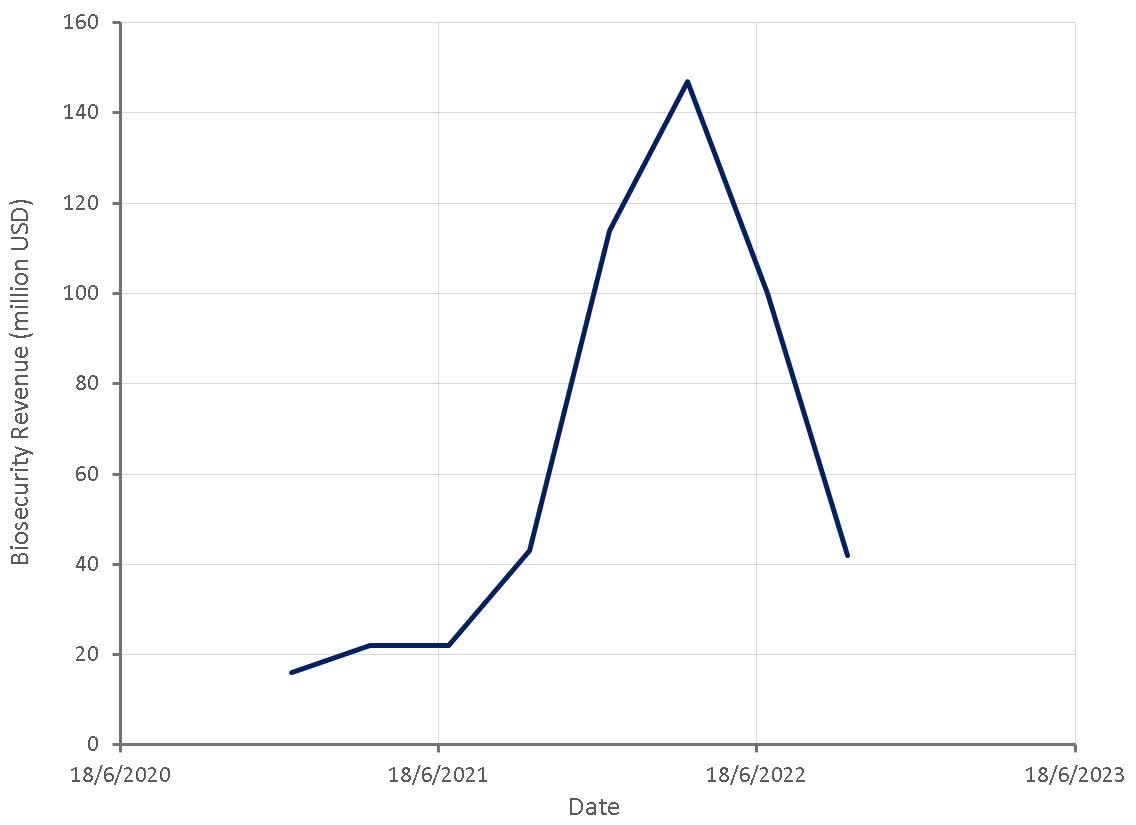

COVID monitoring services are proving to have some level of durability, which has led to Ginkgo’s Biosecurity business performing well in 2022. This business is heavily tied to education and hence should pick-up somewhat in the next quarter. COVID testing has clearly peaked though and this is going to be a headwind for Ginkgo over the next 12 months. Investors are extremely short-sighted at the moment, and if Ginkgo has low headline revenue growth and large losses over the next 12 months, the stock is likely to come under pressure, regardless of the long-term fundamentals of the business.

The Biosecurity business has potential beyond COVID testing though, with a number of governments investing in longer-term biosecurity infrastructure. Ginkgo has announced MOUs with the governments of Saudi Arabia and Rwanda, which appear to be targeted at collecting and analyzing data at ports of entry. Ginkgo’s wording when discussing this also seems to imply that they also have similar agreements that they have not publicly announced or that they are working on similar agreements. These passive monitoring programs are still nascent though and are not yet a meaningful contributor to Ginkgo’s business.

Ginkgo is also developing new technologies to detect engineered DNA in conjunction with Draper, for Intelligence Advanced Research Projects Activity (IARPA) FELIX (Finding Engineering-Linked Indicators) program. This is in the form of a suite of computational tools which aim to identify genetic engineering in next generation sequencing datasets. Potential applications include biothreat detection, environmental monitoring and food inspection, according to the company.

Figure 2: Ginkgo Biosecurity Revenue (source: Created by author using data from Ginkgo)

Expenses

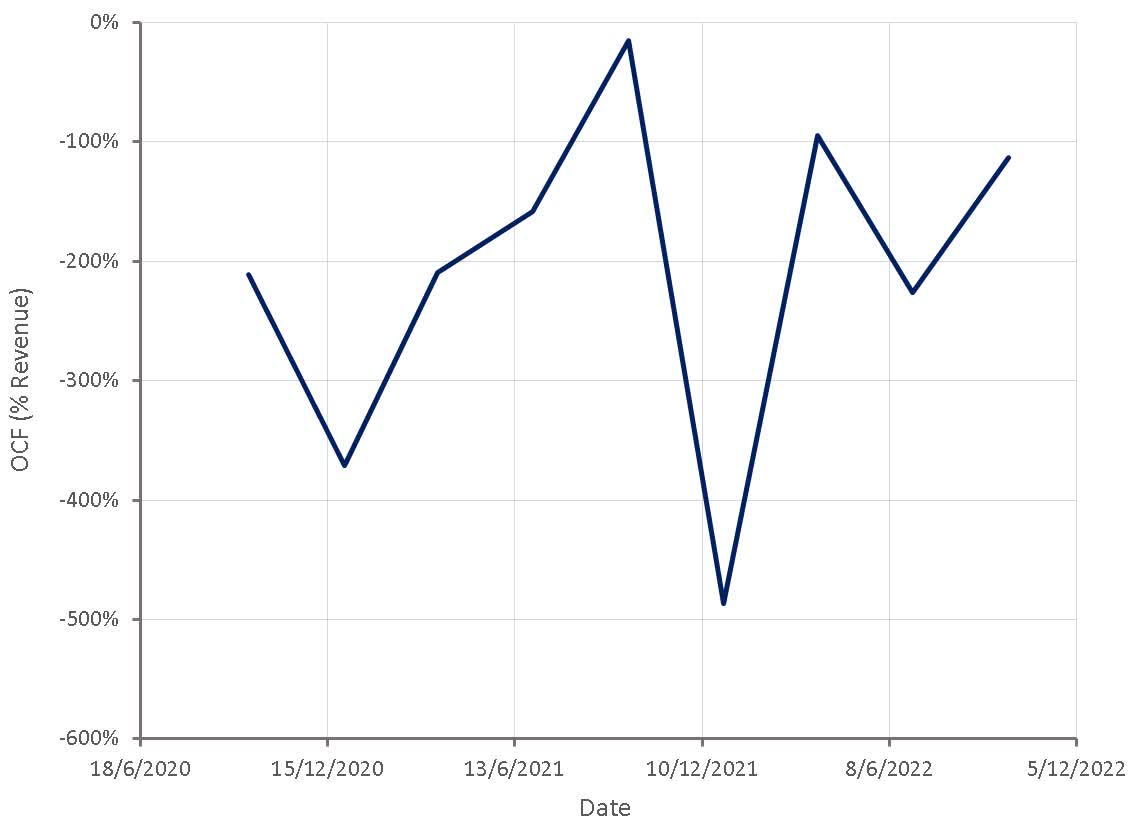

While Ginkgo’s losses are not currently a concern for investors due to the company’s large cash balance and ability to raise capital on reasonably attractive terms, there is a risk that this could change in coming years. Biosecurity has provided a temporary benefit, contributing $71 million in operating profits in the first nine months of 2022. If this goes away, Ginkgo will find itself with larger losses, particularly as recent acquisitions are expected to significantly increase operating expenses. The Foundry is still a long way from breakeven and at the current growth rate will take several years to get there.

Figure 3: Ginkgo Operating Cash Flow (% Foundry Revenue) (source: Created by author using data from Ginkgo)

It is therefore not really that surprising that Ginkgo has chosen to raise funds now, particularly in light of mounting economic uncertainty. What is surprising is the size of the raise ($100 million), which isn’t particularly meaningful given Ginkgo’s current cash balance. Ginkgo has stated that the proceeds will be used to offset cash used to finance the acquisition of certain assets and liabilities of Bayer (OTCPK:BAYRY) CropScience and for other general corporate purposes.

Valuation

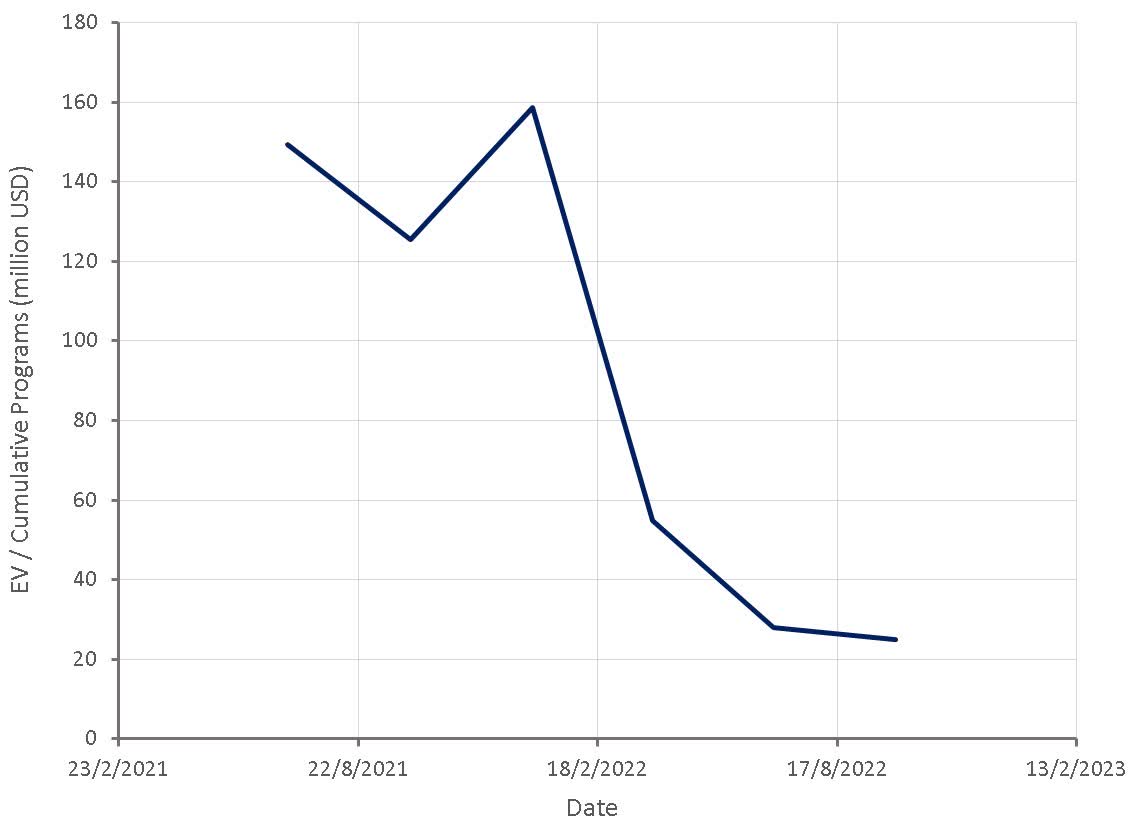

Ginkgo’s focus on capturing downstream value means that current revenue and profits are potentially less useful indicators of the health of the business than the number of programs that can provide downstream value. Ginkgo has so far given limited information on downstream economics to protect customer privacy, but has stated that going forward they will release more information, as the business is grown to the point where individual deal economics cannot be inferred from the aggregated data.

Based on the cumulative number of programs, Ginkgo’s stock now appears far less expensive than it did at the time of listing, but it is still not clear that it is undervalued.

Figure 4: Ginkgo Relative Valuation (source: Created by author using data from Ginkgo)

Conclusion

Gingko’s performance has been about as positive as could be expected in the current environment. It likely won’t be apparent whether Ginkgo’s business model will be successful for a number of years though, which could leave many investors with shorter time horizons disappointed. A reduction in COVID testing revenue could undermine investor confidence in the meantime.

Be the first to comment