turk_stock_photographer

Getty Realty (NYSE:GTY) has been one of my top REIT picks over the past several months, giving investors a 44% total return since my bullish take on the stock in June of last year, far outpacing the 7% return of the S&P 500 (SPY) over the same timeframe. In this article, I revisit the stock and evaluate whether it still warrants a buy, so let’s get started.

Why GTY?

Getty Realty is a self-managed net lease REIT with a $2 billion enterprise value, making it the largest REIT to specialize in the acquisition and development of convenience, automotive, and other single-tenant properties. At present, it holds a sizeable portfolio of 1,021 freestanding properties that are spread across 38 U.S. states and Washington D.C.

GTY is a strong REIT for a number of reasons, not least of which is its core focus on automotive related properties. This pure play focus enables management to hone in on its competency in this niche area. Plus, most properties in this segment are owned by small private owners including mom and pop type owners, resulting in less competition for deals and plenty of greenfield for GTY to consolidate this sector.

Moreover, GTY carries strong portfolio fundamentals with a very high 99.6% occupancy rate, long weighted average remaining lease term of 8.6 years, and average 1.6% annual rent escalations on existing properties. GTY’s properties are also well positioned, with 71% of properties being in higher traffic corner locations, and 65% in the top 50 metropolitan statistical areas in the U.S. Tenants also remain healthy with 2.7x average rent coverage.

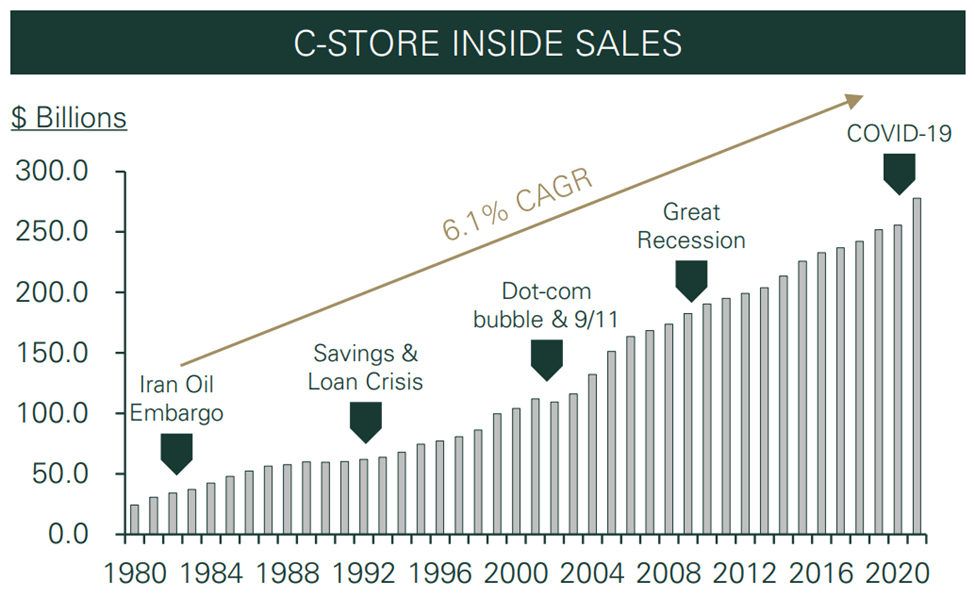

While the increase in the number of electric vehicles is a legitimate concern, it’s important to consider that most (73%) of GTY’s properties are comprised of Convenience and Gas, 12% are carwashes, and just 11% are legacy gas and repair properties. As shown below, C-store inside sales have grown just about every year since 1980 through multiple economic crises.

C-Store Sales (Investor Presentation)

Meanwhile, management has proven adept at growing the portfolio in an accretive manner, with FFO per share rising by 4.2% YoY to $0.50 during the third quarter. This was driven by base rental income growth of 7.4% through a combination of new property acquisitions and base rent growth on existing properties.

Notably, GTY recently issued 2023 guidance on January 10th, with the expectation of full year AFFO per share of $2.20 at the midpoint, which represents around 3% YoY growth from anticipated 2022 levels.

Management also announced that it had invested $157 million across 52 properties for the full year 2022 and that it currently has a committed investment pipeline of over $100 million for the development and acquisition of 28 convenience stores and car wash properties. Importantly, GTY’s rising share price in recent months is of great benefit to its cost of capital, as management noted in the same report that it raised record amounts of capital at attractive prices.

Meanwhile, GTY maintains a strong BBB- rated balance sheet, with a low net debt to EBITDA of 4.9x, well below the 6.0x level that most ratings agencies deem safe for REITs. It also has strong 4.0x fixed charge coverage ratio. In addition, I see potential for interest rates on debt to moderate. this combined with continued low gasoline prices despite the recent runup were noted in Hoya Capital’s report released a couple days ago:

Cooler-than-expected PPI inflation data, however, was enough to keep downward pressure on longer-term benchmark rates with the 10-Year Treasury Yield retreating 3 basis points to close at 3.48% – back on the cusp of the lowest levels since September and well below its peak closing high of 4.25% in October. Crude Oil and Gasoline prices continued their rebound with WTI Crude now about 15% above its recent December lows, but still 35% below June 2022 peaks.

Importantly, GTY currently yields a respectable 4.9% and the dividend is well covered by an AFFO payout ratio of 80%. It also has a 5-year dividend CAGR of 7.4% and nine years of consecutive raises.

Admittedly, GTY is no longer cheap at the current price of $35.49 with a forward P/FFO of 14.9 and value investors may want to wait for a better valuation with P/FFO closer to 14.0. Nonetheless, long-term investors can take comfort in knowing GTY has a better cost of capital at the current valuation and its long growth runway in a fragmented sector.

Investor Takeaway

Getty Realty is an attractive pure-play REIT that benefits from strong portfolio fundamentals, a healthy balance sheet, and a robust acquisition pipeline. Plus, investors get paid a respectable dividend yield while waiting for the long-term growth story to play out. As such, I find GTY to be a buy for long-term income investors who prize a pure-play REIT with plenty of greenfield opportunities.

Be the first to comment