bankrx/iStock via Getty Images

2023 has arrived. The year has started well, with Geron Corporation (NASDAQ:GERN) producing superb data, data that makes imetelstat approvable after over a decade of trial work and relative obscurity. Data published today shows that the IMERGE trial beat the placebo with high statistical significance. If we were to do a cross-trial comparison, imetelstat has roundly beaten the closest rival, Bristol-Myers Squibb’s (BMY) newly approved Reblozyl, in every comparable metric.

This has been a long time coming. For imet, it has been just over a decade and a half, and a decade since Dr. Ayalew Tefferi’s ASH13 presentation, where he first claimed imet “clearly showed anti-myeloproliferative activity,” which became controversial later when some of his data could not be replicated in the IMBARK trial. That claim originally led Johnson & Johnson (JNJ) to partner with Geron, and the IMBARK data caused them to leave. Good thing that Dr Tefferi’s claims have been borne out by IMERGE data.

IMERGE was a phase 3 randomized double blinded trial across 118 clinical sites in 17 countries. 178 patients were enrolled, with low- or lntermediate 1- risk MDS who were relapsed/refractory to ESA or EPO. Other baseline characteristics included:

• Transfusion dependent: ≥4 units RBCs every 8 weeks over 16-week pre-study • Non-deletion 5q • No prior treatment with lenalidomide or HMAs.

Patients were ringed sideroblast agnostic. This is important because ringed sideroblast positive accounts for only 25% of the post-ESA MDS population. Being agnostic opens up a larger market than Reblozyl, which only enrolled ringed sideroblast-positive patients. Primary endpoint was 8-week RBC Transfusion Independence (TI). Key Secondary Endpoints were 24-week RBC TI, Duration of TI and Hematologic Improvement Erythroid (HI-E).

Data showed that the primary endpoint of 8-week TI was met by 47 patients in the drug arm, which is 39.8%, versus 9 patients in the control arm, which is 15.0%, and this represents a p-value of <0.001, which is highly statistically significant. Patients had a continuous sustained transfusion independence, with 83% of 8-week responder patients showing such a continuous TI. As to a key secondary endpoint of TI duration, Median TI duration was 51.6 weeks for imet versus only 13.3 weeks for placebo, which had a hazard ratio of 0.23 and a statistically significant p-value of <0.001. At least 3 imet patients had TI of more than two years. 33 imet patients, or 28% of n, met the key secondary endpoint of 24-week TI, versus just 2 patients or 3.3% of the placebo group, which has a p-value of <0.001. A test drug is as good as the “unethicality” of not giving it to placebo patients, and if that is true, imet is a very good drug indeed.

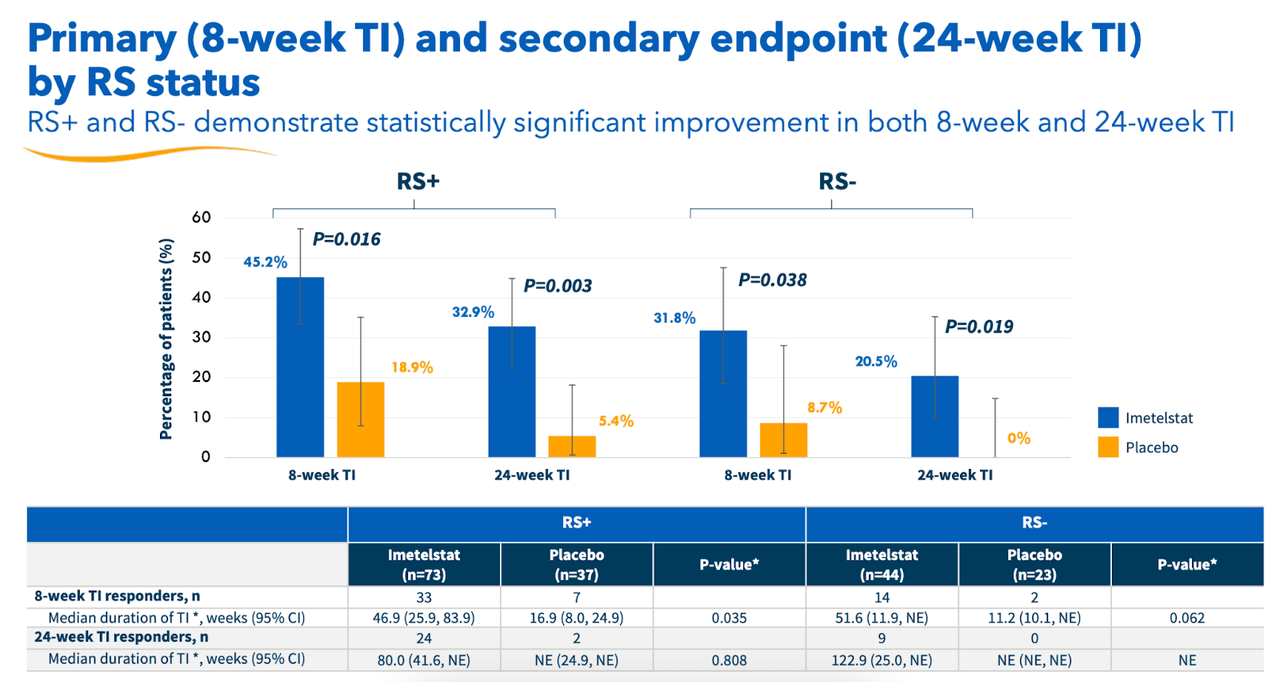

Data also showed a statistically significant improvement in haemoglobin levels among imet patients versus placebo. “HI-E per IWG 2018 criteria demonstrated a highly statistically significant (p<0.001) and clinically meaningful improvement for imetelstat-treated patients versus placebo.” This shows that imet met all the key endpoints of the trial. Both RS+ and RS- patients showed statistically significant improvements, as you can see below:

Geron RS data (Geron website)

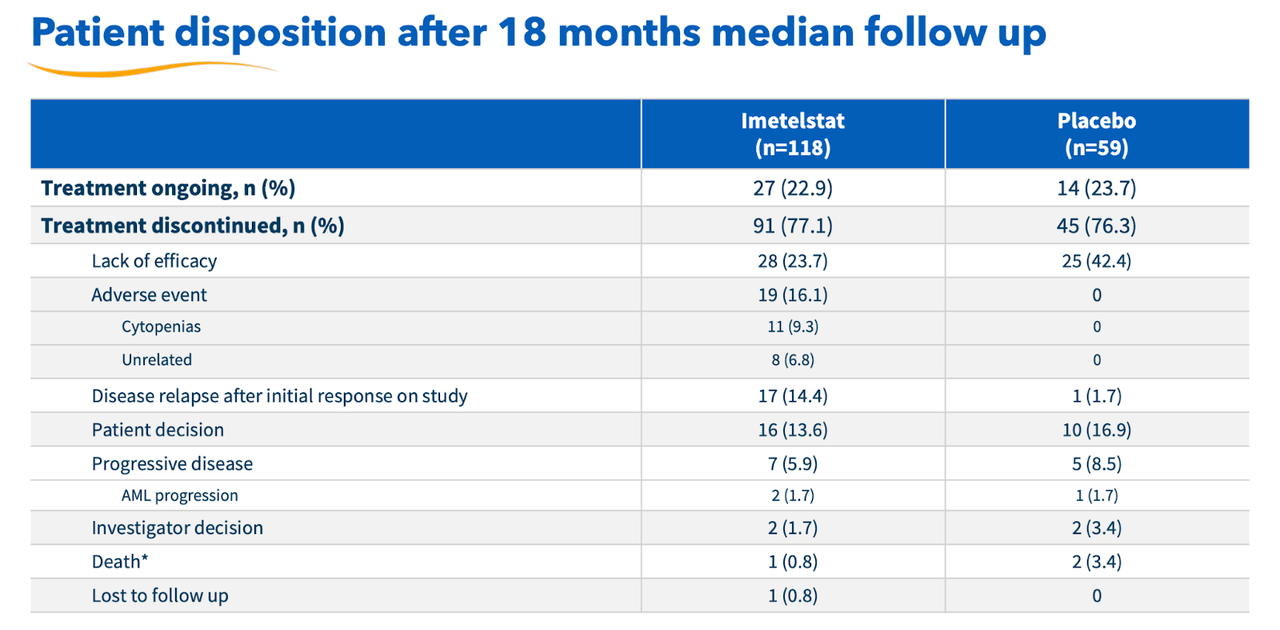

There is some minor concern with safety here. I must say that Geron has been very upfront with it all, and has highlighted the key issue – discontinuation rates – even before it discussed the actual trial. Here’s the data table:

Geron discontinuation rates (Geron website)

There’s a very high discontinuation rate in both imet and placebo group. However, looking at the granular data shows that the rate is similar across both groups, there’s double the rate in the placebo group for lack of efficacy, while very high comparative rates for adverse events in the imet group. Geron has assured us that most of these adverse events were quickly resolved, and went down from grade 3 to 2 or lower on management. In general, given the high disease burden, the safety looks okay.

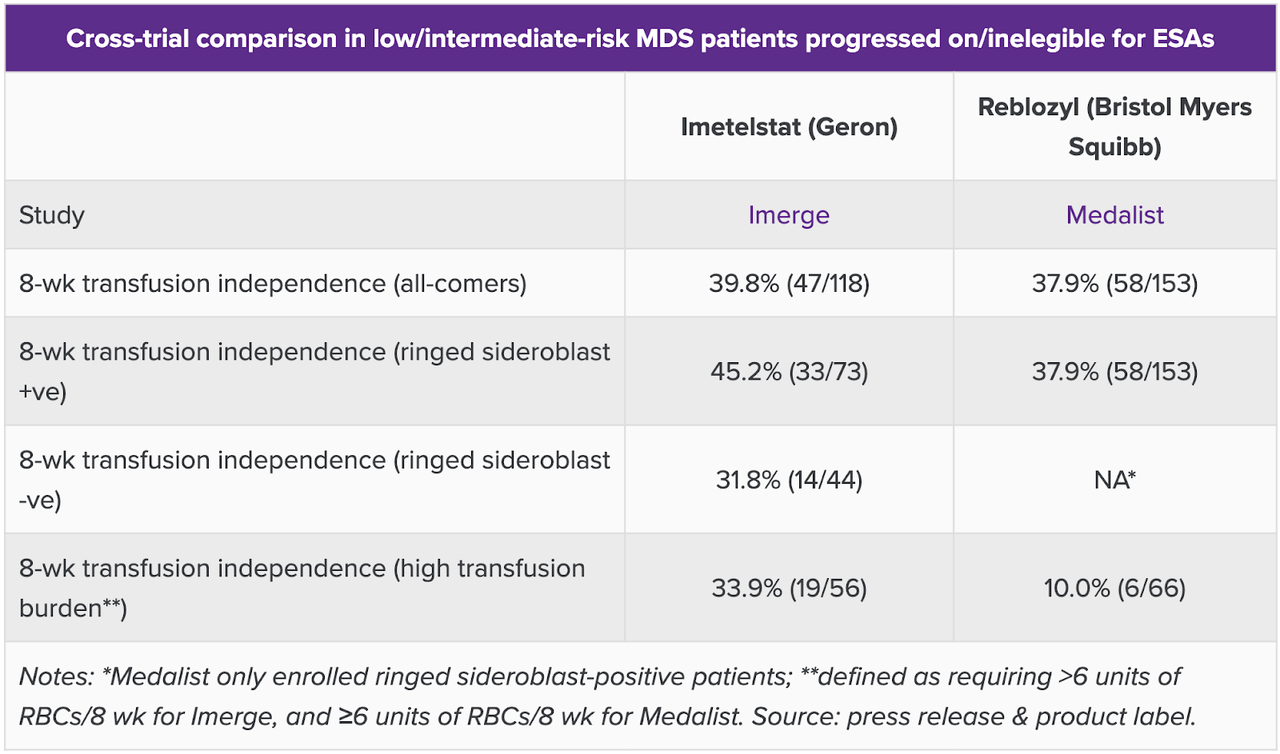

I saw on Evaluate, cited before, that they have compared this data to Reblozyl’s MEDALIST trial data. Here’s the snapshot, which says it all:

GERON comparison data (Evaluate)

While TI rates were similar, where imet scored much better was at higher-risk patients with higher transfusion burden, defined as requiring greater than 6 units of RBC per 8 weeks for imet, and equal to or greater than 6 units of RBC per 8 weeks for Reblozyl. That little thing actually makes a lot of difference if we knew how many were equal to and how many were greater than 6 units. Even if we do not know that granularity, the difference is striking, and constitutes one of the two key differentiating identities of IMERGE. The other one, of course, is the RS agnosticity of the trial, which Reblozyl does not have. Clearly, imetelstat is the winner. There’s no other competition in this patient population.

Jacob Plieth mentions another difference:

But a further complication is Reblozyl’s Commands trial – in MDS patients naive to ESAs – which was toplined positive in October. If this gives Reblozyl an earlier-line label then doctors will want to know how imetelstat performs in patients who progress on the BMS drug, and here there is little to go on.

Also, Adam Feuerstein, who has generally been a critic of Geron for years, cited the trial data positively on Twitter. However, he mentioned the discontinuation rate as a negative, without going into the detail I just discussed.

“Today is a great day for lower risk MDS patients who are living with the burden of transfusions. The results from the IMerge Phase 3 study were resoundingly positive, presenting compelling durability of transfusion independence, delivering on the promise of imetelstat and telomerase inhibition for these patients,” said John A. Scarlett, M.D., Geron’s Chairman and Chief Executive Officer. “This milestone is the first of many upcoming catalysts for Geron, with planned U.S. and EU regulatory submissions in 2023, as well as preparations for a potential U.S. commercial launch. In addition, in 2024, we expect an interim analysis of the IMpactMF Phase 3 trial of imetelstat in relapsed/refractory myelofibrosis.”

Speaking of milestones, the company has these plans, as the CEO said, and these were discussed in the conference call. The company also mentioned that Fast Track designation in lower risk MDS enables rolling submission of U.S. NDA and eligibility for priority review. Such a request for rolling submission of NDA was made, and granted by the FDA. The company claims a peak market opportunity of $1.2bn by 2030 in this indication alone. There are a total of 32,700 US patients who may be eligible for imetelstat.

Financials

GERN today has a market cap of $919mn. Other than that, everything I said last month stands:

GERN has … a cash and marketable securities balance of $195mn. The company expects to have another $121mn from the potential exercise of the currently outstanding warrants and up to $50 million from the current debt facility with Hercules Capital.

Research and development expenses for the three months ended September 30, 2022, were $24.6mn, and SG&A were $15.6mn. The company had negligible revenues but around $2mn of interest income. At this rate, it has cash for around 7-8 quarters, or through 2024. If all goes to plan, not only will imet be approved in LR-MDS by that time, but IMpactMF Phase 3 trial in refractory MF will also produce interim data.

Bottom Line

Geron has a strong following on social media, including here on Seeking Alpha. Over the years, I have come to know a number of them. I generally hold a net-negative opinion of stock fans, however, in this case, Geron seems to have paid off for its followers. I wish them well, and I believe if Geron can deliver on its promises for the next 3-4 quarters, that there’s significant upside from current levels.

Be the first to comment