Bill Pugliano/Getty Images News

Leading US automaker General Motors Company (NYSE:GM) stock was battered in 2022 after a surging run from the 2020 pandemic lows.

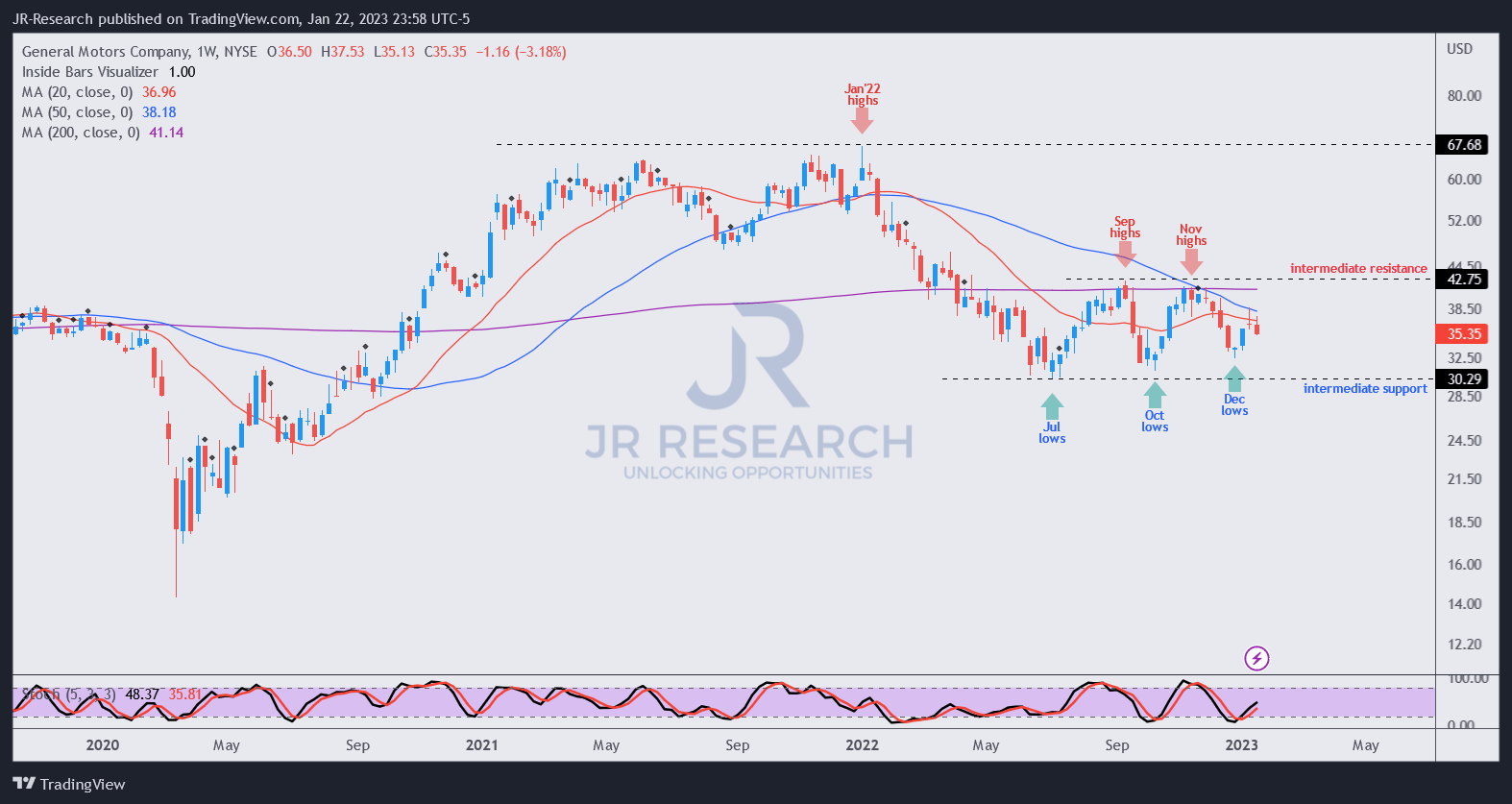

Accordingly, GM fell more than 50% from its January 2022 highs toward its December lows, despite its so-called “cheap valuations.”

We believe investors have astutely priced in execution risks amid an increasingly harsh macro environment. CEO Mary Barra was frustrated in November, as she articulated that the market did not afford GM credit for its expansion plans.

Wall Street analysts remain unimpressed, seeing further profitability decline in the company’s adjusted EBIT projections through 2024. Accordingly, analysts penciled in a 2.7% downtick in adjusted EBIT for FY22 but expect the company’s adjusted EBIT to fall another 20% in 2023.

Why is the Street so downcast on the company’s projections, despite updating its plans at its recent November 2022 Investor Day?

Accordingly, GM sees the potential to raise its North American EV production to 1M units by 2025, a highly aggressive roadmap. It also sees nearly $50B in EV sales by 2025, helping lift General Motors’ total revenue at a 3Y CAGR of 12% over the next three years.

It could still be premature to assess the cadence of the company’s success when Barra & team report their Q4 earnings release on January 31. However, a recent WSJ report indicated that General Motors and its key battery partner LG Energy Solutions could shelve plans on a fourth battery plant isn’t constructive.

Accordingly, LG was reportedly concerned with “the rapid pace of its recent US investments,” with forward visibility clouded by the uncertain macroeconomic outlook.

However, General Motors was reportedly in discussion with “at least one other battery supplier,” suggesting it’s still too early for investors to conclude.

Notwithstanding, the deal is critical for the company’s plan to scale its EV capacity in the US to 1M by 2025. Hence, we encourage investors to pay close attention to management’s commentary at its upcoming earnings conference.

Tesla’s (TSLA) recent price cuts have caused upheavals in the industry. It is not expected to impact legacy auto OEMs’ profitability like General Motors in the near term. However, it could still affect the near-term adoption cadence of their fledgling EV penetration, ceding momentum to the US EV leader.

Accordingly, the WSJ highlighted that Tesla’s move to bolster volume growth in lieu of near-term profitability had affected the “purchase decisions” of some consumers. It has also affected the used-car market, lowering its prices, following the more attractive pricing from Tesla.

As such, General Motors’ decision to continue investing in its gasoline cars in the near term to generate the required profits and cash flow to fund its EV investments is necessary. Therefore, GM could be in a better position than its pure-play EV makers likely forced to cut prices by Tesla, such as XPeng (XPEV).

It is too early to conclude whether General Motors could retain its crown as the top US automaker in 2023. We assessed that consumer discretionary stocks that have suffered over the past year could be due for recovery in 2023 as the Fed tapers its rate hikes.

Moreover, the potential for an earlier-than-expected pivot could lift GM further as investors prepare for a less downbeat macro outlook that could torpedo consumer discretionary spending in autos.

Notwithstanding, investors should still be prepared just in case the market has misread the Fed’s commitment to reach its 2% inflation target, which could force the economy into a deeper downturn.

But the question is whether the market has priced in the pessimism in GM, constructive for a medium-term recovery if Barra & team execute accordingly?

GM price chart (weekly) (TradingView)

GM has been consolidating constructively, undergirded by its July and October lows.

However, buyers still need to muster sufficient buying momentum to recover its September resistance zone before a sustained medium-term recovery could follow.

GM last traded at a NTM of 5.6x, well below its 10Y average, and thus not aggressive.

However, it’s critical for investors to avoid buying into upward surges and wait patiently for pullbacks to improve their reward/risk.

Rating: Buy (revise from Hold).

Be the first to comment