jetcityimage

General Electric (NYSE:GE) is a highly cyclical industrial conglomerate with significant profit risk during an economic downturn, which is not reflected in the company’s FCF/earnings multiple.

Despite the fact that General Electric reported strong earnings in the fourth quarter due to a recovery in the Aerospace segment, I believe the stock has risen too far.

Given that General Electric’s business is highly cyclical, and that the free cash flow forecast for 2023 is less than spectacular, I believe that the valuation multiple does not adequately reflect General Electric’s cyclical profit risks in a down economy.

Better-Than-Expected Fourth Quarter Earnings

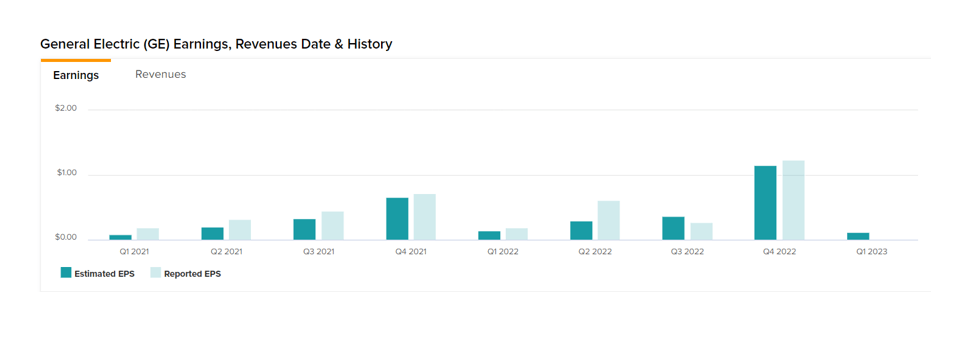

General Electric reported 4Q-22 (adjusted) earnings per share of $1.24 versus $1.15 expected, so GE delivered a nice profit beat for its fourth quarter amid, primarily, an increase in demand from the airline industry. It was General Electric’s third profit beat in the last four quarters.

Earnings (General Electric)

GE Aerospace Profits From A Recovery In The Airline Industry

General Electric’s fourth-quarter earnings were bolstered primarily by the Aerospace segment, which benefited from recovering travel industry demand following Covid-19.

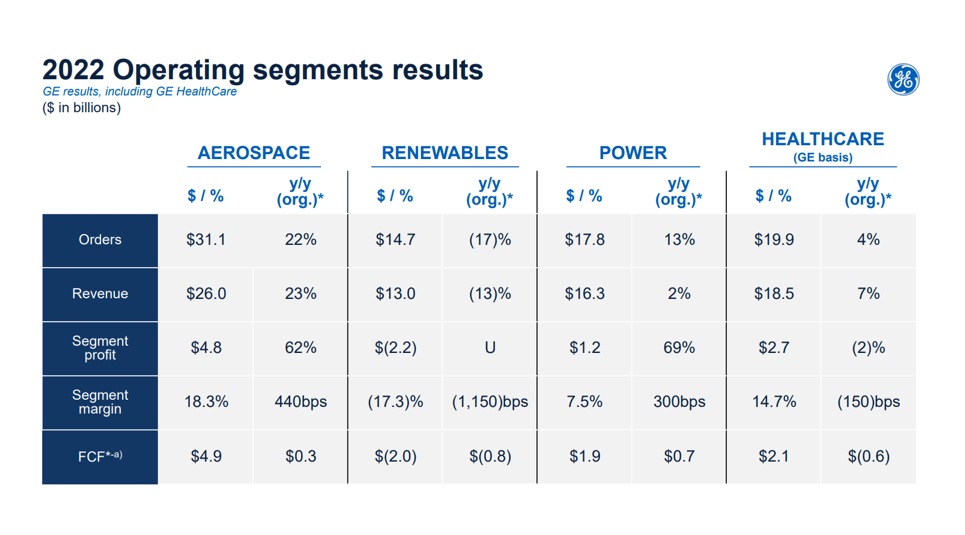

In terms of sales growth, General Electric’s Aerospace segment performed best in the fourth quarter, while the Renewable segment continued to struggle. Aerospace saw 22% YoY organic order growth and 23% YoY sales growth as the industry recovered from the worst downturn since November 9, 2001.

Renewables continued to underperform, with sales falling 13% YoY to $13.0 billion. Power had a decent (but not spectacular) fourth quarter, with sales increasing by 2% YoY to $16.3 billion. GE Healthcare was spun off in January and now trades as a stand-alone entity.

2022 Operating Segments Results (General Electric)

GE Aerospace Is Driving The Company’s Free Cash Flow Growth

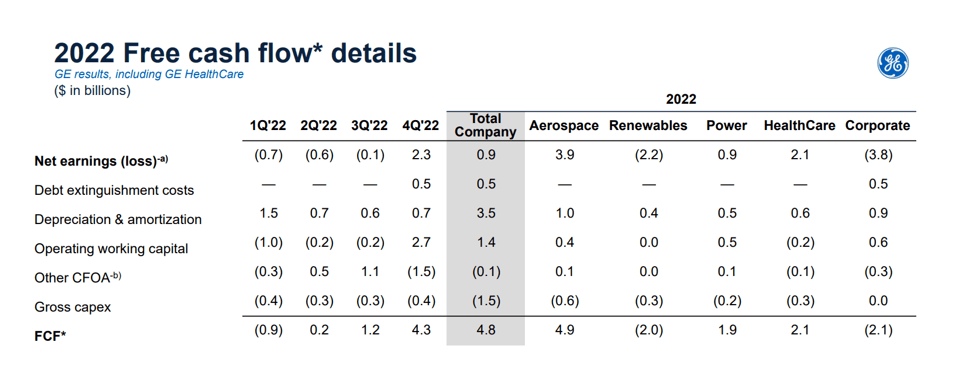

The airline industry’s recovery and the resumption of air travel have resulted in a significant increase in General Electric’s free cash flow in 2022. The conglomerate earned $4.3 billion in free cash flow in the fourth quarter, which was more than it earned in the previous three quarters combined.

General Electric’s free cash flow in 2022 totaled $4.8 billion, representing a 152% increase YoY. The Aerospace segment of General Electric was the most important source of this free cash flow, as shown in the segment breakdown below.

2022 Free Cash Flow (General Electric)

Excessive Valuation Multiple For A Cyclically Vulnerable Conglomerate

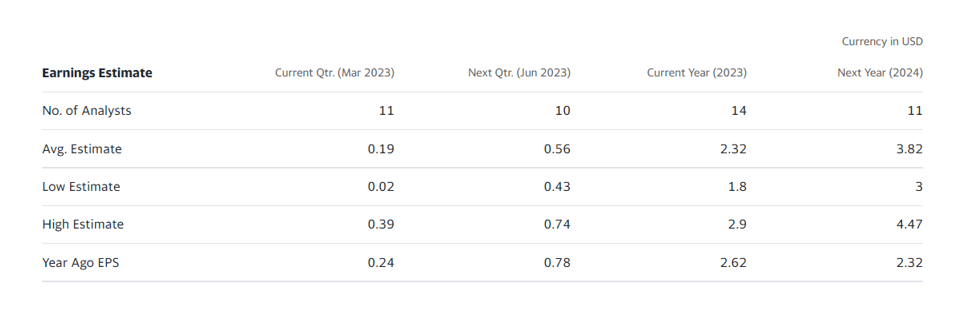

At the time of writing, General Electric’s stock is trading at $81 per share. With the market expecting $2.32 per share in earnings this year, GE trades at a P/E ratio of 34x, which is rather high given that General Electric is a highly cyclical conglomerate business.

Earnings Estimate (Yahoo Finance)

General Electric is also pricey in terms of free cash flow, with the conglomerate expecting $3.4 billion to $4.2 billion in free cash flow in 2022.

GE is valued at 23x free cash flow based on the midpoint of guidance, $3.8 billion, and a market value of $87 billion. That’s expensive for a cyclical conglomerate.

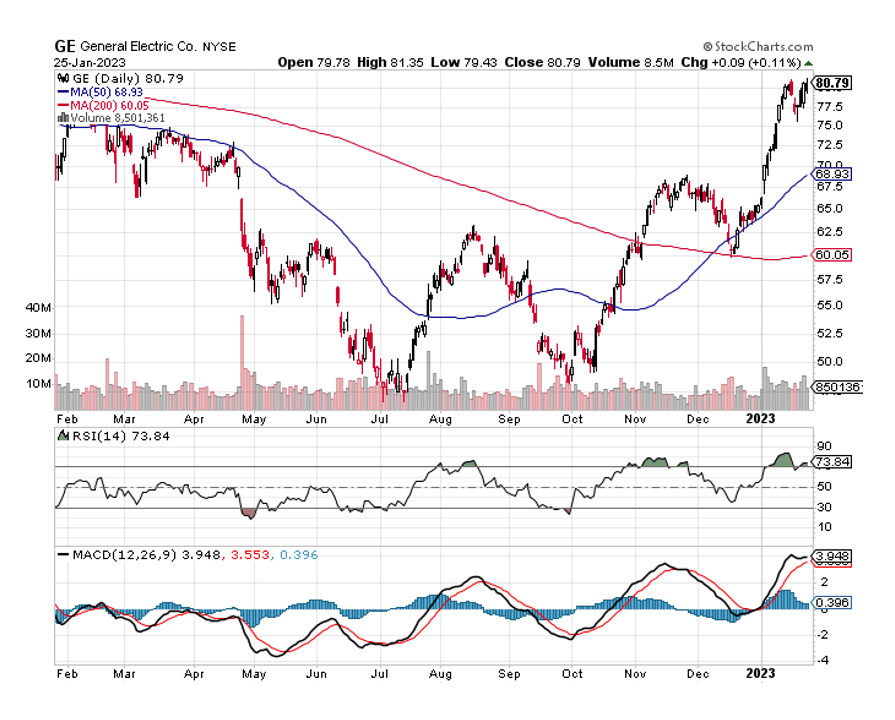

In addition to the valuation issue that I see for General Electric, I believe the chart profile is troubling. According to the Relative Strength Index, which currently stands at 73.84, General Electric’s stock is now overbought.

A value for the RSI above 70 is typically regarded as a contrarian sell signal, indicating that the market has become overly optimistic about GE in the short term, and that optimism may have gone too far. The technical situation suggests that investors exercise caution and hedge their downside risk.

Relative Strength Index (Stockcharts.com)

Why General Electric Could See A Higher Valuation

Aversion to a U.S. recession and continued strength in the Aerospace segment have the potential to boost General Electric’s stock price. Consistently high demand for jet engines and power turbines may support General Electric’s business for a while longer, but valuation multiples will eventually reach a limit.

As I stated throughout the article, General Electric’s free cash flow and earnings in 2023 are already expensive, making the risk/reward relationship unappealing.

My Conclusion

General Electric had a good fourth quarter, thanks primarily to the Aerospace segment. Recovering jet engine demand in a depressed market resulted in strong order and sales growth for GE in 4Q-22, as well as higher free cash flow. With that said, I believe investors should proceed with caution for a variety of reasons.

First, the Relative Strength Index indicates that General Electric’s stock is overbought. Second, I believe GE is overvalued, with a P/E ratio of 34x and a P/FCF ratio of 23x. Third, GE remains a cyclically exposed conglomerate with significant profit risk in a downmarket.

All things considered, I believe General Electric is due for a downside correction, and investors should be cautious not to overpay for GE’s growth.

Be the first to comment